Believe it or not, mutual funds were once exciting. If you remember the days before the internet – when investors got their information from newspapers and magazines – mutual funds were the biggest advertisers and the focus of nearly every article.

They were sexy.

The industry sold them well. It told us someone smarter than you and me would invest our money for us and make us boatloads of profits.

I remember nervously and excitedly making my first investment. Despite working an entry-level job for no money and living in Manhattan, I had saved up a few hundred dollars that I was ready to put to work.

I chose the Fidelity Select Health Care Fund (Nasdaq: FSPHX), figuring there’ll always be demand for health care, no matter what the economy was doing. I was right. The mutual fund turned my few hundred dollars into a few hundred more.

But the more I investigated these funds, the more I got turned off. The lessons I learned 20 years ago are still valid today.

In October I told you that 65% of mutual fund managers underperform the S&P 500. It was proof you should take your investments into your own hands.

And now, the numbers for all of 2012 are out. It looks like fund managers improved their performance.

This time, “only” 61% of fund managers did worse than the market.

In other words, if you invested in a stock mutual fund (not a focused fund like precious metals, health care or technology), you still had a nearly two out of three chance of underperforming the market.

Heck, you could do that yourself by throwing darts at The Wall Street Journal, without having to pay expenses to the mutual fund company.

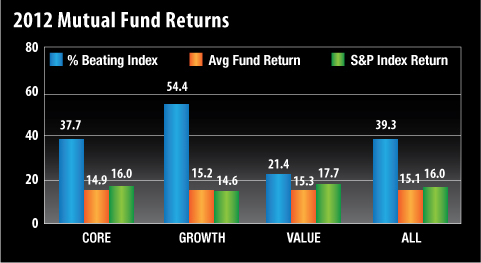

Here’s a graph courtesy of Abnormal Returns…

With a quick glance at the bars on the right, we can see just 39.3% of all mutual funds beat the S&P 500. The average fund returned 15.1% versus the S&P’s 16% gain.

With growth funds, just over half beat their benchmark indices (which performed worse than the S&P). And although 54% of growth-fund managers beat their index, the average return was 15.2% – still below the S&P 500’s gains.

Finally, value managers had a horrible year, with only 21% beating their benchmark.

The bottom line is, the majority of mutual funds will never make you rich. Which is why I present you…

THE THREE REASONS WHY YOU CAN MANAGE YOUR MONEY BETTER THAN A MUTUAL FUND MANAGER

-

Expenses – someone has to pay for that Ivy League manager’s paycheck, as well as the salaries of his analysts, traders and administrative assistants. And the company Christmas party doesn’t pay for itself. Neither do the electric bill, cleaning staff and all of the other costs associated with running a business.

While many managers do have their investors’ best interests in mind, they are still running a business. Bills have to be paid and profits have to be made. And the only way that happens is if they charge you for the privilege of letting them invest your money.

In 2011, equity fund investors paid an average of 0.79% worth of their positions in expenses to mutual funds. Note that figure is quite close to the difference between the average return for an equity mutual fund and the return of the S&P 500.

That 0.79% figure might not sound like much, but if you have a portfolio worth $200,000, you’re paying $1,580 per year in expenses. Over 10 years, that’s $15,800 worth of fees. (If the portfolio grows, you’ll pay even more.)

And that’s just an average fund. If you’re paying over 1% in expenses, you’re flushing even more money down the toilet.

Don’t forget some funds charge “loads,” or upfront fees. Often, if you’re using an investment advisor, you’ll pay an upfront fee of as much as 4.75%. That means if you give the advisor or fund $1,000, only $995.25 is invested on your behalf.

It’s going to be very tough to beat the averages starting nearly five percentage points down.

-

You can buy whatever you want. They can’t.

If you find a small stock that has big potential, you can buy a few thousand shares and see what happens. When you’re done, you can sell your shares with no problem.

A mutual fund manager doesn’t have that luxury.

With millions of dollars that need to be put to work, buying a small stock doesn’t make sense unless he can buy a ton of it.

But that fund manager can’t load up on a stock that only trades 100,000 shares a day without moving the price. It’s the same thing when he goes to sell it.

The individual investor has a lot more flexibility to acquire stocks that have the ability to outperform, while the fund manager is often stuck buying familiar names because they have the liquidity he needs.

-

No one cares more about your money than you. The fund manager’s goal is to make as much money as possible for you by December 31, because that’s when his performance is evaluated.

If he beats his benchmark, he gets a nice bonus. If he misses, there may be no big payout.

But you’re not concerned with December 31. Your focus is probably on April 5, 2015, September 21, 2027, or any other date you plan on retiring. Or perhaps you are already retired and you need consistent income or growth.

December 31 is meaningless to you except for deciding which friends to ring in the New Year with.

While the fund managers are trying to make money for their investors, you’re the one that knows your tolerance for risk, your goals and how to best handle your money. Don’t let someone else make those decisions for you.

GET SMART

With those ideas in mind, I beg you to learn as much as you can about investing so that you can handle your own money. After obtaining more knowledge, you may decide to use a portion of your money to try to beat the market and leave the rest in index funds.

Or maybe you’ll do as I consistently recommend and invest in Perpetual Dividend Raisers – stocks that raise their dividend every year. These stocks have an excellent track record of beating the market over the long term. And if you hold them for several years, the yield on your original investment will likely be substantial.

For example, let’s look at Middlesex Water Co. (Nasdaq: MSEX), a small water company that services New Jersey, Pennsylvania and Delaware. It’s a tiny stock, with a market cap of just $305 million and average daily trading volume of less than 30,000 shares. No fund manager could touch it without sending the price rocketing higher.

But the company has raised its dividend every year since President Nixon was in office.

Today it yields a respectable 3.9%. But if you had bought it 10 years ago, you’d be enjoying a yield of 6.4% due to the annual dividend hikes.

A mutual fund manager is probably not going to hold that stock for 10 years. Remember, he’s trying to post great numbers this year. The average tenure for a mutual fund manager is only four to five years. He knows he likely won’t be managing the same fund in 2023… when you’re looking to retire.

Your best chance at a wealthy retirement is to manage your investments yourself. You’ll save money, you’ll have more flexibility, and your money will be in good hands.

Click here to post a comment on WealthyRetirement.com.

© 2013 Wealthy Retirement. All Rights Reserved.

105 West Monument Street

Baltimore, MD 21201

North America: 1.800.992.0205; Fax: 1.410.223.2650

International: +1.410.223.2643; Fax: +1 410 223 2650

E-mail: WealthyRetirement@WealthyRetirement.com

Website: www.wealthyretirement.com

Keep the e-mails you value from falling into your spam folder. Whitelist Wealthy Retirement.