Remember this day – Wednesday, January 14th, 2015; as it may well be recalled as a key inflection point in financial history. I had planned on writing of just one “historically momentous” event – i.e., last night’s implosion of base metal prices, signaling the “death of manipulation” of the illicitly supported copper market. However, before I even started writing – at 8:40 AM EST – no less than seven such events littered the global economic and financial landscape.

Remember this day – Wednesday, January 14th, 2015; as it may well be recalled as a key inflection point in financial history. I had planned on writing of just one “historically momentous” event – i.e., last night’s implosion of base metal prices, signaling the “death of manipulation” of the illicitly supported copper market. However, before I even started writing – at 8:40 AM EST – no less than seven such events littered the global economic and financial landscape.

Actually, I had planned on also highlighting the utterly insane manipulations of yesterday’s markets – as the PPT desperately attempted to prevent the “Dow Jones Propaganda Average” from plunging; whilst the Fed desperately attempted to prevent the 10-year yield from closing below the October 15th “flash crash” low of 1.89%, yielding universal realization of the “most damning proof yet of QE failure”; and the Cartel desperately attempted to slow the momentum of the past two weeks’ explosion of PM prices, particularly in non-dollar currencies. Suffice to say, the piddling “salvation” achieved by yesterday’s efforts has been decidedly annihilated this morning; as care of said “historically momentous” factors, stocks, commodities, and interest rates are plunging; whilst currency markets are in chaos; and what do you know, gold prices are surging – as silver, a day after another enormous sales day at the U.S. mint, is also looking extremely strong.

And thus, in no particular order, here are today’s “historically momentous” events; which, cumulatively, will make it eminently difficult for TPTB to prevent universal realization of a far more terrifying sort; i.e., that “2008 is back.”

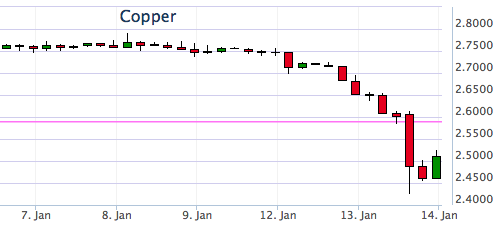

1. I could kick myself, as for the past week I’ve queued up an article topic, discussing the irrationality of copper and zinc prices holding up so well, whilst the Bloomberg Commodity Index plunges to a 12-year low. Moreover, in the case of “Dr. Copper” – the poster child of industrial commodity demand; or as I called it last year, “Dr. Death” – it is also amidst a horrific Chinese inventory scandal. In other words, it was just a matter of time before copper “met its maker.” And finally, after gradually weakening over the past week, it suddenly collapsed last night, along with zinc and all the base metals. Down 5% today alone, to $2.57/lb, it is now down 11% from the $2.90/lb level it ended 2014 at; whilst zinc is now just $0.92/lb, from $0.99/lb at year-end. Both metals have a long way to go to the $1.25/lb and $0.50/lb lows of 2008, respectively, but rest assured they’ll probably come close. And when they do – and the Bloomberg Commodity Index makes multi-decade lows, not only will BHP Billiton and Rio Tinto again teeter on bankruptcy, but the “Miles Franklin Silver All-Star Webinar Panel’s” forecast of a 25%-50% silver production decline will appear far more likely.

2. After plumbing 20-year lows for the past year, mortgage purchase applications exploded 24% last week alone; and refinancing applications, an incredible 66%! And no, this is NOT “good news”; but instead, the “sum of all fears” regarding U.S. consumer and Federal insolvency.

To wit, I spent the New Year’s holiday in Arizona with a very close friend, who said he has just refinanced his mortgage. When questioned, he said Quicken Loans now sends email “alerts” whenever rates fall enough to warrant a new mortgage, with no material costs to complete the process. Immediately after completion, he receives a letter from Fannie Mae, reiterating their ownership of hits mortgage, and the perpetual refinancing process starts anew, as Quicken prepares its next email “alert.” Frankly, I was in awe – realizing that this, in fact, is a new form of QE, as the government is directly “giving” money to the public; thus, indebting it further, whilst adding massive debts to the Federal balance sheet. Which, by the way, is conveniently hidden from view, as Fannie and Freddie’s nearly $6 trillion of nationalized debt is held “off balance sheet.” Throw in the 3%-down mortgages the FHA is now offering to subprime lenders, and you can see the Fed’s printing presses have decidedly not been “tapered” – nor its appetite for financial destruction. Of course, you can bet that few, if any, of the 24% increase in mortgage applications will actually turn into new home purchases. Or, for that matter, that the waves of refinancing will cause Americans to “spend” – as opposed to paying off other debts.

3. In my “2015 predictions,” I forecast “Retail Armageddon” following this year’s historically horrible holiday spending season. Additionally, in yesterday’s “things I’m grateful for,” I noted my incredulity in seeing the MSM and Wall Street continue to expect holiday spending to be “salvaged” despite an 11% plunge in “Black Friday” weekend sales. Well, just this morning, that illusion was decidedly shattered, when it was reported that December retail sales not only plunged by 1.0%, compared to expectations of just a 0.1% decline. Thus, the oil price plunge has decidedly NOT acted as a “tax cut”; as not only evidenced by the shockingly bad retail sales, but plunging load factors at airlines like American Air! And oh yeah, even “excluding gasoline sales,” retail sales still declined.

4. The Fed may have succeeded in closing the 10-year yield at 1.89% yesterday, mere tenths of a basis point above the October 15th “flash crash” low. However, this morning it is in FREEFALL – touching at low as 1.78% earlier this morning, and sitting at 1.81% as I speak. In other words, the market is now fully “front-running” QE4, expecting it sooner rather than later; or as I’ve deemed it, the inevitable “Yellen Reversal.” And not only here, but throughout the world – as evidenced by the Japanese five-year yield yesterday joining those of Germany and Switzerland in negative territory. I mean, can you imagine the insanity of paying the world’s most insolvent entities for the right to lend them money? I can, as “investors” are simply betting the BOJ, ECB, and SNB – among others – will monetize such bonds at still higher prices. Of course, whilst investors rush headlong to the “safety” of QE-supported sovereign bonds – no matter how insolvent their issuers – they are fleeing “2008-style” from the debt of insolvent corporations!

5. Speaking of the ECB, the Euro has plunged to another nine-year low this morning – of 1.174 at its low. “Coincidentally” before next Tuesday’s potentially momentous ECB meeting, the highest EU court essentially gave a green light to the constitutionality of QE. Thus, gold is again surging in Euro and Swiss Franc terms, as the orchestrated three-year “bear market” is decidedly OVER. It’s only a matter of time before gold in Euros, Swiss Francs, Japanese Yen, and countless other currencies join Ruble-priced gold at all-time highs; and ultimately, as I’ll discuss in tomorrow’s Audioblog, U.S. dollar-priced gold.

6. Also on the topic of CRASHES, how about Bitcoin? Down another 20% overnight – to a low of $172 – it is now down 40% this year alone, and 85% from the all-time high set barely a year ago. I’ve written exhaustively of my views on Bitcoin; and frankly, the concept of alternative currencies, whilst intriguing, has a LONG, LONG way to go, even if ultimately successful. That said, Bitcoin will NEVER meet the parameters of money ; and sadly, countless tens of thousands are finding that out the hard way.

Nor, for that matter, are mining stocks – which despite the potential for material gains, are still just shares of ownership of companies hoping to profitably mine gold and silver, amidst a “minefield” of industry and government-erected obstacles. Just look at the massively dilutive financing announced yesterday by one of the industry’s “best” miners – Yamana Gold – causing its price to plunge 13% yesterday alone. In said “2015 predictions,” I also forecast complete paralysis of the global gold and silver mining industries, from already devastated levels – and that was before the base metal implosion I started today’s article discussing. Recall, roughly two-thirds of all silver production emanates as by-product from other types of mines – for the most part, copper or lead/zinc.

7. Though not momentous today, we are but eleven days from the potentially historic Greek snap election – in which the “anti-austerity” (read “pro-default”, “anti-Euro”) Syriza party is expecting a dramatic victory. Seeing its leader, Alexis Tsirpas, claiming Greek economic data is dramatically overstated – whilst government tax receipts collapse, as citizens anticipate a “debt jubilee,” it’s awe-inspiring to see the “revenge of the people” movement I anticipated in action.

Well, that’s enough for this “historically momentous” day; other than to conclude with this news of the ongoing explosion of global physical gold demand – which will inevitably go parabolic when, likely much sooner than most can imagine – the entire world realizes the end game of history’s largest fiat Ponzi scheme, “QE to Infinity,” is not just inevitable, but imminent.

PROTECT YOURSELF, and do it NOW!