Asset protection

Is there anything Apple can’t do?

Is there anything Apple can’t do?

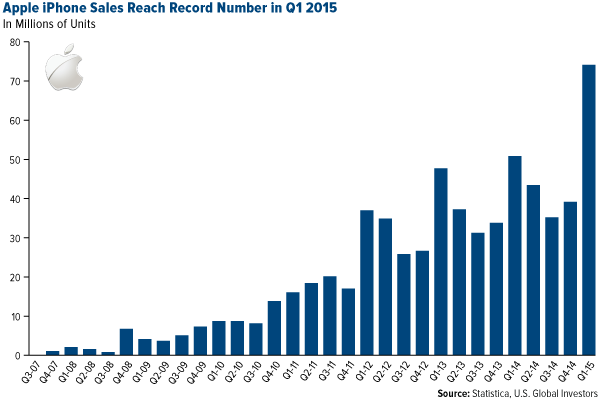

First it revolutionized the personal computing business. Then, with the launch of the iPod in 2001, it forced the music industry to change its tune. Against initial market reservations, the company succeeded at making Star Trek-like tablets hip when it released the iPad in 2010. And in Q1 2015, a record 75 million units of its now-ubiquitous iPhone were sold around the globe. The smartphone’s operating system, iOS, currently controls a jaw-dropping 89-percent share of all systems worldwide, pushing the second-place OS, Google’s Android, down to 11 percent from 30 percent just a year ago.

As you might already know, the company that Steve Jobs built—which we own in our All American Equity Fund (GBTFX) and Holmes Macro Trends Fund (MEGAX)—is history’s largest by net capitalization. In its last quarterly report, Apple posted a record $75 billion in revenue and is now sitting pretty on a mind-boggling $180 billion in cash. Many analysts believe the company will reach a jaw-dropping $1 trillion in market cap.

So what’s Apple’s next trick?

How about moving the world’s gold market?

iGold

This April, Apple will be venturing into the latest wearable gadget market, the smartwatch, joining competitors such as Samsung, Garmin and Sony. All of the models in Apple’s stable of watches look sleek and beautifully designed—just what you’d expect from Apple—and will no doubt be capable of performing all sorts of high-tech functions such as receiving text messages, monitoring the wearer’s vitals and, of course, telling time.

This April, Apple will be venturing into the latest wearable gadget market, the smartwatch, joining competitors such as Samsung, Garmin and Sony. All of the models in Apple’s stable of watches look sleek and beautifully designed—just what you’d expect from Apple—and will no doubt be capable of performing all sorts of high-tech functions such as receiving text messages, monitoring the wearer’s vitals and, of course, telling time.

But the real story here is that the company’s high-end luxury model, referred to simply as the Apple Watch Edition, will come encased in 18-karat gold.

What should make this news even more exciting to gold investors is that the company expects to produce 1 million units of this particular model per month in the second quarter of 2015 alone, according to the Wall Street Journal.

That’s a lot of gold, if true. It also proves that the Love Trade is alive and well. Apple chose to use gold in its most expensive new model because the metal is revered for its beauty and rarity.

To produce such a great quantity of units, how much of the yellow metal might be needed?

For a ballpark estimate, I turn to Apple news forum TidBITS, which begins with the assumption that each Apple Watch Edition contains two troy ounces of gold. From there:

If Apple makes 1 million Apple Watch Edition units every month, that equals 24 million troy ounces of gold used per year, or roughly 746 metric tons [or tonnes].

That’s enough gold to make even a Bond villain blush, but just how much is it? About 2,500 metric tons of gold are mined per year. If Apple uses 746 metric tons every year, we’re talking about 30 percent of the world’s annual gold production.

To put things in perspective, the Sripuram Golden Temple in India, the world’s largest golden structure, is made from “only” 1.5 tons of the metal.

To put things in perspective, the Sripuram Golden Temple in India, the world’s largest golden structure, is made from “only” 1.5 tons of the metal.

TidBITS acknowledges that the amount of gold is speculative at this point. Two troy ounces does seem pretty hyperbolic. But even if each luxury watch contains only a quarter of that, it’s still an unfathomable—perhaps even unprecedented—amount of gold for a single company, even one so large as Apple, to consume.

Ralph Aldis, portfolio manager of our Gold and Precious Metals Fund (USERX) and World Precious Minerals Fund (UNWPX), likens the idea of Apple buying a third of the world’s gold to China’s voracious consumption of the metal. As I mentioned last week, China is buying more gold right now than the total amount mined worldwide.

“If the estimates of how much gold each watch contains are close to reality, and if Apple’s able to sell as many units as it claims, it really ought to help gold prices move higher,” Ralph says.

But Can Expectations Be Met?

Here’s where this whole discussion could unravel. Although we don’t yet know what the Apple Watch Edition will retail at, it’s safe to predict that it will fall somewhere between $4,000 and $10,000, placing it in the same company as a low-end Rolex.

With that in mind, are Apple’s sales expectations too optimistic?

Possibly. But remember, this is Apple we’re talking about here. Over the years, it has sufficiently proven itself as a company that more-than-delivers on the “if you build it, they will come” philosophy. Steve Jobs aggressively cultivated a business environment that not only encourages but insists on “thinking different”—to use the company’s old slogan—risk-taking and developing must-have gadgets.

“Our whole role in life is to give you something you didn’t know you wanted,” says current Apple CEO Tim Cook. “And then once you get it, you can’t imagine your life without it.”

A perfect case study is the iPhone. When it launched in June 2007, the cell phone market was decidedly crowded. Consumers seemed content with the choices that were already available. Why did we need another phone?

Yet here we are more than eight years later, and as I pointed out earlier, 75 million iPhones were sold in the last quarter alone.

So it’s not entirely out of the realm of possibility for Apple to move 1 million $10,000 Apple Watch Editions per month.

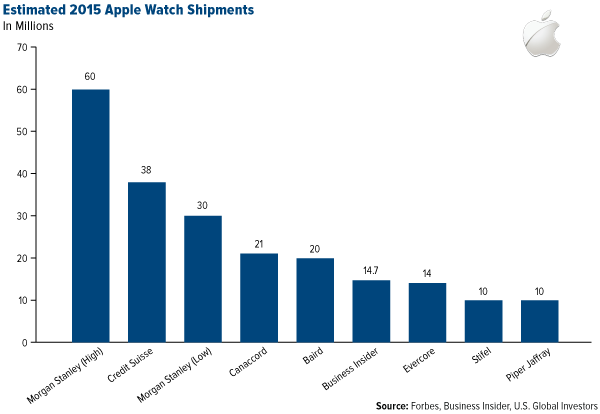

Early in January I shared the following chart, which shows various analysts’ Apple Watch shipment forecasts for 2015, ranging from 10 million to 60 million units. Of course, allmodels are included here, not just the luxury model.

Looking at it now, many of the predictions seem a little understated. After all, Apple hasn’t released a dud product in at least two decades (remember the Newton?). Come April, we’ll see for sure what the demand really is—for the Apple Watch as well as gold.

Global Metals & Mining Conference

The weekend before last, I attended the BMO Metals & Mining Conference in Hollywood, Florida, along with Ralph, Brian Hicks, a portfolio manager of our Global Resources Fund (PSPFX), and junior analyst Alex Blow.

“Generally speaking, companies have streamlined operations and are focused on shareholder returns,” Brian said.

Alex came away from the conference with renewed conviction that the global climate is conducive for gold, citing central bank easing policies and increasing volatility in world currencies, both of which support the yellow metal’s performance.

“It looks as though gold has technical support and that a bottom has been reached,” he said. “If the eurozone really picks up, gold demand should rise, which would also benefit China since its primary gold export destination is the eurozone.”

“Buy survival gear”

Economics Compacted

“This column contains everything there is to know about economics. Hereafter it will be possible to shut down university deprtments and stop talking about Keynes and the Austrian School, to the great relief of mankind. In gratitude you can send me your childrens’college funds.

In 1850 people all lived on farms and grew food, which they ate. Eating was really important to them. They liked eating. There was in 1850 tremendous demand for refrigerators and cars, but people didn’t know they wanted these things because they hadn’t been invented. Anyway, they didn’t have any money to buy them with.

Yet the demand was there, crouched to spring. Much demand for almost everything, but little supply.

Then farming automated and people all went to cities to work in factories to make refrigerators and cars, which had been invented. These weren’t as important as food, but they were pretty important. People had a little money now, and bought them. You don’t need advertising to sell what people actually want.

There was lots of demand and getting to be pretty good supply.

Soon the factories were spitting out more than anyone could use of everything that anyone could reasonably want. A family needs only so many refrigerators. Here we encounter the first crucial problem of the modern economy: too much supply and not enough demand.

Yet the factories had to make stuff so people would have jobs, and the people had to buy the stuff so they could keep having factories. Economics is thus the study of the squirrel wheel.

To keep people working and buying, the economy began making things that nobody really needed or would think to want, such as nail salons, electronic gadgets, and designer jeans. To get people to buy these things, the supply of demand had to increase. Advertising came about to manufacture demand for things that, without advertising, no one would buy. Consequently society now depends for existence on pop-ups, singing commercials at twenty minutes to the hour on television, billboards, and Google ads. Advertising thus became more important to the economy than anything it advertised.

Labor

Labor followed a similar pattern. When factories came, they needed lots of people to make the refrigerators and cars. Most work involved digging holes or lifting heavy objects, so the workers didn’t have to be smart or know much.

Automation

Then came the rolling disaster that economists don’t seem to have anticipated: automation. As factories produced the increasingly trivial goods that supported the economy, they needed fewer and fewer workers to make the trivial goods. This raised two questions: Who was going to buy the $450 running shoes that nobody needed except that advertising told them they did, and how were the workers who didn’t have work making them any longer going to get money to buy them? Or to eat?

It became obvious, except to economists, that automation could do just about everything people were paid to do. Just now, someone has invented a burger-maker machine that will presumably replace hundreds of thousands of burger-flippers who aren’t needed anywhere else. Self-driving vehicles approach practicality, and will first replace long-haul truckers and then cabbies and delivery truck drivers. Much worse is in the offing. Here is the second crucial problem of modern economics: Where to put unnecessry people?

The Theory of Increasing Uselessness

The Theory of Increasing Uselessness

A search continues, long quietly underway but now intensified, for ways to keep off the work force people for whom there is no work, or no real work. These are not necessarily lazy, shiftless, or parasitic. They just don’t have anything to do.

Child-labor laws and requirements that people finish high school helped diminish the labor force. Then society told the young that they all needed to go to college, when most of them didn’t, and since the universities served chiefly as holding pens, the quality of education dropped. Universities did however employ professors and administrators. Here was another example of selling at high price something that no one really needed, namely the appearance of education.

Swollen bureaucracies popped up to provide the appearance of work while the purported workers did little that would not better have been left undone. Military enterprise soaked up more people doing nothing that should be done. Exotic fighter planes that would never do anything to justify their existence but bomb remote goat-herds absorbed thousands of engineers and hundreds of billions of dollars. The engineers could as well have been paid for digging holes and filling them in, but this was judged unduly candid.

Finally even these measures ceased to be enough. College graduates began living with their parents and lining up for jobs a Starbucks because there was no need for them anywhere else. Resort was had to outright charity. Thus food stamps, Section Eight housing, free lunches at school, AFDC, and all the other disbursements of free money. Those receiving the free money no longer had any incentive to work even if the opportunity offered. In the cities generation after generation now lived on charity, largely illiterate and in what is never called custodial care. They are simply unnecessary. There is nothing for them to do. So they don’t do anything.

Poverty

In America this is usually a state of mind rather than an economic condition. The allegedly poor have all their time free, a luxury not available to the indentured drones who pay for this leisure. The poor have enough to eat—gobbling Cheetos instead of real food is their choice—and they have access to libraries and parks and museums. Graduate students at the same economic level used to live a life of books, music, illicit substances, and good conversation. The recipients of charity are not economically poor, but mentally empty.

Cognitive Stratification

Meanwhile an elaborate and highly effective system developed for sucking the very bright young from every cranny in the country and sending them to the remaining good universities: SATs, GREs, National Merit, ACT, and suchlike. Here the top two percent in intelligence partied, married, and made babies, not always in that order, and went into brain-intensive trades like Silicon Valley, i-banking, and medicine. As the middle class sank into the lower-middle, the brain babies increasingly formed a thin layer of dominant if not always morally impressive intellects at the top of society.

Increasingly aware of each other thanks to list-serves and web sites for the very smart, they foregathered internationally with their own kind, eschewing contact with the surrounding sea of slugs. (I will bet you are not reading this on a site where the comments are misspelled.) They prospered. Nobody else did. The battle lines were being drawn. Which brings us to:

The Minimum Wage

Conservatives harbor the curious notion that people will work if they don’t have to. This is because to them work, real actual work, is an abstraction with which they have no familiarity. Real work is usually unpleasant or boring. But to economic theorists, work means being a cardiac surgeon, talking head, columnist, or CEO. Thus they say that if we eliminate the minimum wage, black youth (these are always given as examples) will rush to labor for a dollar an hour, learn the trade, rise, and become CEOs. Horatio Alger and all that.

This implies two things: First, that anyone in his right mind would spend eight hours a day flipping burgers for a pittance when he could live on charity in leisure at the same standard, and second, that any employer in his right mind would want to hire semi-literates with bad work habits when, given our current endemic unemployment, he has a choice of much more educated and dependable workers.

In short, if the minimum wage were abolished, the bottom rungs of society would remain unemployed because their labor isn’t worth enough for them to live on, or worth anything at all. The bottom rungs creep upward. When almost everybody is unemployed, we will have to institute communism manque: “To each according to his needs and, from each, nothing much. I will then write The Theory of the Leisure Classes: A Study in Urban Chaos.”

There you have it, all of economics in a small package. Buy survival gear.

Philip Francis Stanley and Grotesque Ophthalmological Malpractice

The global economy is literally imploding.

Investors believe that China’s economy is chugging along, but the non-fraudulent data says otherwise.

China’s GDP numbers are a total fiction. And Chinese Government officials even ADMIT it! Back in 2007, no less than current First Vice Premiere of China, Li Keqiang, admitted to the US ambassador to China that ALL Chinese data, outside of electricity consumption, railroad cargo, and bank lending is for “reference only.”

As RBS Economics notes, China’s rail volumes are collapsing at a rate

not seen since the Asian Financial Crisis. The Chinese economy is literally collapsing faster NOW than it did in 2008.

As far as Europe goes, Mario Draghi just admitted in the EU Parliament that the ECB has only one tool left at its disposal: QE. After that, there is nothing left in the tool box.

And despite announcing QE a few months ago, Europe is lurching towards deflation. Greece’s banks are imploding while the Ukraine is moving rapidly into hyperinflation.

The Euro has taken out critical support and is likely going BELOW parity with the US Dollar

In the US, as Societe General’s Albert Edwards has recently noted, US corporate profits and sales are rolling over in a BIG way. The US Dollar rally is crushing profits across the board not just in the energy sector.

Stocks are set up for an absolute CRASH. They are pricing in ECONOMIC PERFECTION and the reality is that the global economy is imploding.

And the system is just as fragile as it was in 2008.

- Corporate debt is back to 2007 PEAK levels.

- Stock buybacks are back to 2007 PEAK levels.

- Investor bullishness is back to 2007 PEAK levels.

- Margin debt (money borrowed to buy stocks) is at 2007 PEAK levels.

- The leveraged loan market is flashing major warnings.

- Corporate insiders are dumping shares at a pace not seen since the TECH BUBBLE TOP

- Numerous investment legends have warned of a coming crash.

- Investor complacency is at a record LOW.

- The Fed has confirmed QE is ending this week, so the juice is cut off for now.

It is very likely that this year will go down as the end of the great Central Bank rig of the last six years. The time to prepare is now, before the big collapse hits.

Best Regards

Graham Summers

Please remember this warning when you go to the ATM to get cash… and there is none!

Please remember this warning when you go to the ATM to get cash… and there is none!

While we were thinking about what was really going on with today’s strange new money system, a startling thought occurred to us.

Our financial system could take a surprising and catastrophic twist that almost nobody imagines, let alone anticipates.

Do you remember when a lethal tsunami hit the beaches of Southeast Asia, killing thousands of people and causing billions of dollars of damage?

Well, just before the 80-foot wall of water slammed into the coast an odd thing happened: The water disappeared.

The tide went out farther than anyone had ever seen before. Local fishermen headed for high ground immediately. They knew what it meant. But the tourists went out onto the beach looking for shells!

The same thing could happen to the money supply: Cash could evaporate suddenly and disastrously – just before we drown in it.

Credit Money

Here’s how… and why:

If you look at M2 money supply – which measures coins and notes in circulation as well as bank deposits and money market accounts – America’s money stock amounted to $11.7 trillion as of last month.

But there was just $1.3 trillion of physical currency in circulation – about only half of which is in the US. (Nobody knows for sure.)

What we use as money today is mostly credit. It exists as zeros and ones in electronic bank accounts. We never see it. Touch it. Feel it. Count it out. Or lose it behind seat cushions.

Banks profit – handsomely – by creating this credit. And as long as banks have sufficient capital, they are happy to create as much credit as we are willing to pay for.

After all, it costs the banks almost nothing to create new credit. That’s why we have so much of it.

A monetary system like this has never before existed. And this one has existed only during a time when credit was undergoing an epic expansion.

So our monetary system has never been thoroughly tested. How will it hold up in a deep or prolonged credit contraction? Can it survive an extended bear market in bonds or stocks? What would happen if consumer prices were out of control?

Less Than Zero

Our current money system began in 1971.

It survived consumer price inflation of almost 14% a year in 1980. But Paul Volcker was already on the job, raising interest rates to bring inflation under control.

And it survived the “credit crunch” of 2008-09. Ben Bernanke dropped the price of credit to almost zero, by slashing short-term interest rates and buying trillions of dollars of government bonds.

But the next crisis could be very different…

Short-term interest rates are already close to zero in the US (and less than zero in Switzerland, Denmark and Sweden). And according to a recent study by McKinsey, the world’s total debt (at least as officially recorded) now stands at $200 trillion – up $57 trillion since 2007. That’s 286% of global GDP… and far in excess of what the real economy can support.

At some point, a debt correction is inevitable. Debt expansions are always – always– followed by debt contractions. There is no other way. Debt cannot increase forever.

And when it happens, ZIRP and QE will not be enough to reverse the process, because they are already running at open throttle.

What then?

The value of debt drops sharply and fast. Creditors look to their borrowers… traders look at their counterparties… bankers look at each other…

…and suddenly, no one wants to part with a penny, for fear he may never see it again. Credit stops.

It’s not just that no one wants to lend, no one wants to borrow either – except for desperate people with no choice, usually those who have no hope of paying their debts.

Just like we saw after the 2008 crisis, we can expect a quick response from the feds.

The Fed will announce unlimited new borrowing facilities. But it won’t matter….

House prices will be crashing. (Who will lend against the value of a house?) Stock prices will be crashing. (Who will be able to borrow against his stocks?) Art, collectibles and resources – all will be in free fall.

The NEXT Crisis

In the last crisis, every major bank and investment firm on Wall Street would have gone broke had the feds not intervened. Next time it may not be so easy to save them.

The next crisis is likely to be across ALL asset classes. And with $57 trillion more in global debt than in 2007, it is likely to be much harder to stop.

Are you with us so far?

Because here is where it gets interesting…

In a gold-backed monetary system prices fall. But the money is still there. Money becomes more valuable. It doesn’t disappear. It is more valuable because you can use it to buy more stuff.

Naturally, people hold on to it. Of course, the velocity of money – the frequency at which each unit of currency is used to buy something – falls. And this makes it appear that the supply of money is falling too.

But imagine what happens to credit money. The money doesn’t just stop circulating. It vanishes.

A bank that had an “asset” (in the form of a loan to a customer) of $100,000 in June may have zilch by July. A corporation that splurged on share buybacks one week could find those shares cut in half two weeks later. A person with a $100,000 stock market portfolio one day, could find his portfolio has no value at all a few days later.

All of this is standard fare for a credit crisis. The new wrinkle – a devastating one – is that people now do what they always do, but they are forced to do it in a radically different way.

They stop spending. They hoard cash. But what cash do you hoard when most transactions are done on credit? Do you hoard a line of credit? Do you put your credit card in your vault?

No. People will hoard the kind of cash they understand… something they can put their hands on… something that is gaining value – rapidly. They’ll want dollar bills.

Also, following a well-known pattern, these paper dollars will quickly disappear. People drain cash machines. They drain credit facilities. They ask for “cash back” when they use their credit cards. They want real money – old-fashioned money that they can put in their pockets and their home safes…

Dollar Panic

Let us stop here and remind readers that we’re talking about a short timeframe – days… maybe weeks… a couple of months at most. That’s all. It’s the period after the credit crisis has sucked the cash out of the system… and before the government’s inflation tsunami has hit.

As Ben Bernanke put it, “a determined central bank can always create positive consumer price inflation.” But it takes time!

And during that interval, panic will set in. A dollar panic – with people desperate to put their hands on dollars… to pay for food… for fuel…and for everything else they need.

Credit may still be available. But it will be useless. No one will want it. ATMs and banks will run out of cash. Credit facilities will be drained of real cash. Banks will put up signs, first: “Cash withdrawals limited to $500.” And then: “No Cash Withdrawals.”

You will have a credit card with a $10,000 line of credit. You have $5,000 in your debit account. But all financial institutions are staggering. And in the news you will read that your bank has defaulted and been placed in receivership. What would you rather have? Your $10,000 line of credit or a stack of $50 bills?

You will go to buy gasoline. You will take out your credit card to pay.

“Cash Only,” the sign will say. Because the machinery of the credit economy will be breaking down. The gas station… its suppliers… and its financiers do not want to get stuck with a “credit” from your bankrupt lender!

Whose lines of credit are still valuable? Whose bank is ready to fail? Who can pay his mortgage? Who will honor his credit card debt? In a crisis, those questions will be as common as “Who will win an Oscar?” is today.

But no one will know the answers. Quickly, they will stop guessing… and turn to cash.

Our advice: Keep some on hand. You may need it.

Regards,

Bill

With talks between the EU and Greece reaching the boiling point, the former White House Budget Director warned that the Greek crisis is now a threat to the entire global financial system.

With talks between the EU and Greece reaching the boiling point, the former White House Budget Director warned that the Greek crisis is now a threat to the entire global financial system.

Former White House Budget Director, David Stockman: “The Greeks owe something like $350 billion. $60 billion of it is owned by Greek banks. The rest of it is (owned by) the EU — $210 billion — and another $30 or $40 billion by the IMF.

….continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair