Asset protection

The Greek financial/political crisis is becoming an annual event. For a sense of just how long this unfortunate little country has been struggling to survive under the relative sound money regime of the eurozone, here’s a Greek Crisis Timeline that CNN published in 2011. Even back then the pattern of near-collapse followed by temporary respite had been repeating for seven years.

The Greek financial/political crisis is becoming an annual event. For a sense of just how long this unfortunate little country has been struggling to survive under the relative sound money regime of the eurozone, here’s a Greek Crisis Timeline that CNN published in 2011. Even back then the pattern of near-collapse followed by temporary respite had been repeating for seven years.

The most recent lull seemed longer than usual, so long in fact that many people probably assumed that Greece had been “fixed” and was now a more-or-less fully-functioning member of the eurozone, ready to settle back into its enviable lifestyle of hosting tourists, drinking ouzo and avoiding taxes.

But no. Nothing has really changed. Youth unemployment remains around 50% — which is even more astounding when you consider that tourism is generally a pretty good sector for young people looking for entry-level service work. And the government is still running deficits, piling new debt atop its already unmanageable 175% of GDP.

As a result, anti-euro political parties are still gaining adherents and now seem to have enough clout to start dictating terms. This month a series of elections are being held that, if I’m understanding correctly, have to go the government’s way to avoid regime change in which the far left takes over and pulls Greece out of the eurozone. The first round in this voting trilogy didn’t go the government’s way, making the next two highly problematic. And last week the situation got even more complex:

Greek lawmaker alleges bribery attempt in presidential vote

ATHENS, Greece (AP) — A lawmaker from a small right-wing party claimed Friday he had been offered a bribe worth up to 3 million euros ($3.68 million) to vote in favor of electing Greece’s new president, in the latest twist in the bailed-out country’s fraught presidential vote.

Greece faces early general elections if its 300-member parliament fails to elect a president by the third round of voting on Dec. 29. In Wednesday’s first round, the sole candidate and government nominee garnered 160 votes; 180 are needed for election.

Actor Pavlos Haikalis of the Independent Greeks claimed during a phone-in to a live television program that he was offered about 700,000 euros in cash, a loan repayment and advertising contracts, with the alleged bribe’s total value amounting to about 2-3 million euros ($2.4-$3.7 million). He didn’t identify the person, but said he had informed a prosecutor about two weeks ago and had turned over audio and video material.

Haikalis later alleged that the man who contacted him claimed to be acting on behalf of Prime Minister Antonis Samaras and a banker.

So, let’s take the status quo’s worst-case scenario, in which Greece ditches the euro and returns to the easy-to-manipulate drachma. It converts all its outstanding euro-denominated debt to drachmas and then devalues its new/old currency by 30 or so percent, pricing its hotel rooms, charter boats and restaurants back into attractive territory. That’s okay on balance for the Greek people, who benefit more from rising tourism than they’re hurt by devalued savings.

But it’s very bad for European banks and US hedge funds that now own tons of Greek debt and will therefore suffer big losses. More damaging still, once the precedent is set everyone will start looking around for the next domino to fall and will find plenty, with Italy (now in the throes of a political crisis of its own) leading the list. That’s a much bigger economy with way more euro-denominated debt, so an Italian exit from the eurozone would be apocalyptic for the whole global financial system.

Will it come to that in 2015? History says probably not. Remember, Greece has been on the verge of imploding for a decade, and each time the money has been found to save it. With the ECB inching towards a multi-year, multi-trillion euro debt monetization plan, the entire Greek economy could be tucked into that expanding balance sheet without a ripple. So expect another wealth transfer from Germany to Greece in the near future. And then perhaps one from Germany to Italy. But also expect some drama along the way.

Louis Gave is one of my favorite investment and economic thinkers, besides being a good friend and an all-around fun guy. When he and his father Charles and the well-known European journalist Anatole Kaletsky decided to form Gavekal some 15 years ago, Louis moved to Hong Kong, as they felt that Asia and especially China would be a part of the world they would have to understand. Since then Gavekal has expanded its research offices all over the world. The Gavekal team’s various research arms produce an astounding amount of work on an incredibly wide range of topics, but somehow Louis always seems to be on top of all of it.

Louis Gave is one of my favorite investment and economic thinkers, besides being a good friend and an all-around fun guy. When he and his father Charles and the well-known European journalist Anatole Kaletsky decided to form Gavekal some 15 years ago, Louis moved to Hong Kong, as they felt that Asia and especially China would be a part of the world they would have to understand. Since then Gavekal has expanded its research offices all over the world. The Gavekal team’s various research arms produce an astounding amount of work on an incredibly wide range of topics, but somehow Louis always seems to be on top of all of it.

Longtime readers know that I often republish a piece by someone in their firm (typically Charles or Louis). I have to be somewhat judicious, as their research is actually quite expensive, but they kindly give me permission to share it from time to time.

This week, for your Outside the Box reading, I bring you one of the more thought-provoking pieces I’ve read from Louis in some time. In Thoughts from the Frontline I have been looking at world problems we need to focus on as we enter 2015. Today, Louis also gives us a piece along these lines, called “The Burning Questions for 2015,” in which he thinks about a “Chinese Marshall Plan” (and what a stronger US dollar might do to China), Abenomics as a “sideshow,” US capital misallocation, and whether or not we should even care about Europe. I think you will find the piece well worth your time.

Think about this part of his conclusion as you read:

Most investors go about their job trying to identify ‘winners’. But more often than not, investing is about avoiding losers. Like successful gamblers at the racing track, an investor’s starting point should be to eliminate the assets that do not stand a chance, and then spread the rest of one’s capital amongst the remainder.

Wise words indeed.

A Yellow Card from Barry

What you don’t often get to see is the lively debate that happens among my friends about my writing, even as I comment on theirs. Barry Ritholtz of The Big Picture pulled a yellow card on me over a piece of data he contended I had cherry-picked from Zero Hedge. He has a point. I should have either not copied that sentence (the rest of the quote was OK) or noted the issue date. Quoting Barry:

Did you cherry pick this a little much?

“… because since December 2007, or roughly the start of the global depression, shale oil states have added 1.36 million jobs while non-shale states have lost 424,000 jobs.”

I must point out how intellectually disingenuous this start date is, heading right into the crisis – why not use December 2010? Or 5 or 10 years? This is misleading in other ways:

It is geared to start before the crisis & recovery, so that it forces the 10 million jobs lost in the crisis to be offset by the 10 million new jobs added since the recovery began. That creates a very misleading picture of where growth comes from.

We have created 10 million new jobs since June 2009. Has Texas really created 4 million new jobs? The answer is no.

According to [the St. Louis Fed] FRED [database]:

PAYEMS – or NFP – has gone from 130,944 to 140,045, a gain of 9,101 over that period.

TXNA – Total Nonfarm in Texas – has gone from 10,284 to 11,708, for a gain of 1,424.

That gain represents 15.6% of the 9.1MM total.

Well yes, Barry, but because of oil and other things (like a business-friendly climate), Texas did not lose as many jobs in the recession as the rest of the nation did, which is where you can get skewed data, depending on when you start the count and what you are trying to illustrate.

My main point is that energy production has been a huge upside producer of jobs, and that source of new jobs is going away. And yes, Josh, the net benefit for at least the first six months until the job non-production shows up (if it does) is a positive for the economy and the consumer. But I was trying to highlight a potential problem that could hurt US growth. Oil is likely to go to $40 before settling in the $50 range for a while. Will it eventually go back up? Yes. But it’s anybody’s guess as to when.

By the way, a former major hedge fund manager who closed his fund a number of years ago casually mentioned at a party the other night that he hopes oil goes to $35 and that we see a true shakeout in the oil patch. He grew up in a West Texas oil family and truly understands the cycles in the industry, especially for the smaller producers. From his point of view, a substantial shakeout creates massive upside opportunities in lots of places. “Almost enough,” he said, “to tempt me to open a new fund.”

On a different note, everyone is Christmas shopping and trying to find the right gift. Two recommendations. First, the Panasonic wet/dry electric razor (with five blades). I just bought a new set of blades and covers for mine after two years (you do have to replace them every now and then); and the new, improved shave reminded me how much I was in love with it when I bought it. Best shaver ever.

Second, and I know this is a little odd, but for a number of years I’ve been recommending a face cream that contains skin stem cells, which I and quite a number of my readers have noticed really helps rejuvenate our older skin. (I came across the product while researching stem-cell companies with Patrick Cox.) It clearly makes a difference for some people. I get ladies coming up all the time and thanking me for the recommendation, and guys too sometimes shyly admit they use it regularly. (It turns out that just as many men buy the product as women.) The company is Lifeline Skin Care, and they have discounted the product for my readers. If you can get past the fact that this is a financial analyst recommending a skin cream for a Christmas gift, then click on this link.

It is time to hit the send button. I trust you are having a good week. Now settle in and grab a cup of coffee or some wine (depending on the time of day and your mood), and let’s see what Louis has to say.

Your trying to catch up analyst,

John Mauldin, Editor

Outside the Boxsubscribers@mauldineconomics.com

If you wait by the river long enough, the bodies of your enemies will float

by Sun Tzu, The Art of War, fifth century BC

In The Price of Gold and the Art of War, Part I and in this Part II, the author explained how the bankers’ war on gold forced down the price of gold between 1980 and 2000. This is a brilliant short summary of the Centrall Banks action to date in simple terms that can readily be understood by most observers – Editor Money Talks

The Price of Gold and the Art of War Part III

When growth slows in capital markets, the bankers’ daisy-chain of credit and debt breaks down; setting in motion defaulting debt which ends in recession, deflation or, in extreme cases, a deflationary depression.

A deflationary depression is a fatal monetary phenomena where the velocity of money—circulating credit and debt—falls so low capital markets are no longer self-sustaining. This happens after the collapse of massive speculative bubbles such as the collapse of the 1929 US stock market bubble which resulted in the world’s first deflationary depression, the Great Depression of the 1930s.

Throughout history, gold and silver have offered safety in times of economic chaos. Today is no different. What is different is the response of governments and bankers to the collapse of the current economic paradigm—the bankers’ war on gold.

In the midst of the Great Depression, the US passed the 1934 Gold Reserve Act which prohibited the ownership of gold by US citizens, forcing Americans to keep their wealth invested instead in capitalism’s paper assets.

The Gold Reserve Act outlawed most private possession of gold, forcing individuals to sell it to the Treasury, after which it was stored in United States Bullion Depository at Fort Knox and other locations. The act also changed the nominal price of gold from $20.67 per troy ounce to $35. This price change incentivized foreign investors to export their gold to the United States, while simultaneously devaluing the U.S. dollar in an attempt to spark inflation.

http://en.wikipedia.org/wiki/Gold_Reserve_Act#U.S._economic_historical_narrative

The attempt to ‘spark inflation’ in order to overcome a deflationary depression is the 1930s version of today’s similarly futile ‘inflation-targeting’. The resultant rise in the consumer price index from 1934-1937 was only nominal and, by 1938, powerful deflationary pressures had again re-exerted themselves and the US and the world would remain mired in a moribund deflationary depression for the remainder of the decade.

Although the devaluation of the US dollar against gold by the Gold Reserve Act didn’t ‘spark’ the inflation bankers hoped would end the 1930s depression, it would cause large amounts of gold to flow into the US Treasury after 1934 as foreign sellers took advantage of the US Treasury’s offer of a 70% higher price for gold.

In 1944, this unprecedented flow of gold to the US allowed the US to make the dollar fully convertible to gold, officially making the US dollar the world’s reserve currency at Bretton-Woods. However, due to excessive military spending, the US would overspend its entire hoard of gold by 1970, forcing the US to suspend the gold backing of the US dollar in 1971.

When the US ended the gold convertibility of the US dollar, the US also set in motion capitalism’s end game; as the removal of the bankers’ golden fetters (which previously tied money creation to gold reserves) now allowed governments and banks the fatal freedom to print money and create credit without limits.

http://www.financialsensearchive.com/fsu/editorials/bms/2006/0511.html

The final link between the dollar and gold was broken. The dollar became nothing more than a fiat currency and the Fed was then free to continue monetary expansion at will. The result… was a massive explosion of debt.

John Exter quoted in Gold Wars, Ferdinand Lips, Foundation for the Advancement of Monetary Education, New York, 2001

It was the explosive growth of money and credit after 1971 that would set in motion Ludwig von Mises’ ‘crack-up boom’. Excessive money printing and credit creation would lead to a series of larger and larger speculative bubbles which inevitably would culminate in monetary chaos.

The credit boom is built on the sands of banknotes and deposits. It must collapse… If the credit expansion is not stopped in time, the boom turns into the crack-up boom; the flight into real values begins, and the whole monetary system founders.

Ludwig von Mises, Human Action, 1949

GOLD AND DEFLATIONARY DEPRESSIONS

Although the ownership of gold by US citizens was outlawed in 1934, the shares of Homestake Mining, the world’s largest gold mining company, acted as a proxy for gold during the Great Depression giving investors the same protection gold has given throughout history in times of monetary distress.

[Shares in] Homestake Mining.. rose from $65 per share in 1929 to more than $300 per share in 1933 and then climbed to a $480 bid and $534 ask in December of 1935…During the next six years after the 1929 stock market crash, Homestake Mining paid out a total of $128 in cash dividends. Its dividend in 1929 was $7 per share which then climbed to a staggering 1935 dividend of $56 per share…Homestake Mining earned a compound rate of return of 35% per year from 1929 thru 1935, excluding dividends.[bold, mine]

http://www.worststockmarketcrashes.com/featured/homestake-mining-after-the-1929-crash/

Today, the world is on the verge of another, even greater deflationary depression than the 1930s Great Depression. But governments and bankers have pooled their considerable resources to hide that truth from the public in order to protect their vast wealth and power achieved through their use of paper money and leveraged debt.

Nonetheless, powerful deflationary forces unleashed by the collapse of today’s even larger speculative bubbles—the 1990 Nikkei bubble, the 2000 dot.com bubble, the 2008 US real estate bubble and the serial global real estate bubbles—are again moving through global economies; and, just as in the 1930s, the velocity of money is now so low capital markets are no longer self-sustaining.

If today’s investors knew that gold provided not only safety but explosive profits in times of economic chaos, the bankers’ paper markets would have emptied long ago as the majority of investors would have bought gold at the first sign the bankers’ house of cards could go up in flames.

But most investors didn’t know and didn’t buy; and, because of the bankers’ ongoing war on gold, they still haven’t.

This is the time of the vulture, for the vulture feeds neither upon the pastures of the bull nor the stored up wealth of the bear. The vultures feeds instead upon the blind ignorance and denial of the ostrich. The time of the vulture is at hand.

DRSchoon, Time of the Vulture, 3rd ed. 2012

In The Price of Gold and the Art of War, Part I and Part II, I explained how the bankers’ war on gold forced down the price of gold between 1980 and 2000. Next, in The Price of Gold and the Art of War, Part IV, I will explain gold’s price rise after 2000, how the bankers’ responded and how high the price of gold could go in the bankers’ end game.

In my current Dollars & Sense video on youtube, The Economy 2014/2015, I explain the economy in terms that can hopefully be understood by most observers, see https://www.youtube.com/watch?v=YHQNYUdEsGc&feature=youtu.be

As we continue to move deeper into uncharted territory, I believe that good times will succeed the bad times, that love will replace hate and that peace and goodwill towards men and women will prevail.

Buy gold, buy silver, have faith.

Darryl Robert Schoon

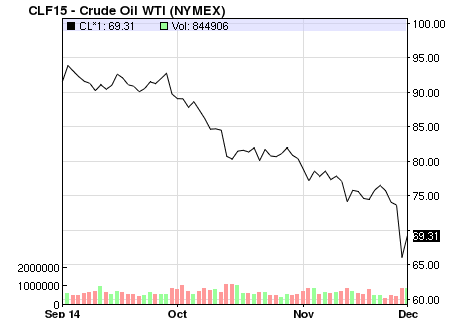

The free-fall in oil prices…WTI down $50 (47%) since June…hit Market Psychology HARD last week…risk aversion soared…credit spreads widened with a vengeance…Treasury yields fell to near All Time Lows…credit risk inspired contagion hit all asset classes…the DJIA…which had closed at a Record All Time High Friday Dec 4…fell 680 pts (3.7%)…creating a Classic Key Reversal Down…closing lower than all FIVE previous weeks!

Crude: WTI closed the week at $57.50…down $50 (47%) from June highs…down $20 (26%) the last 3 weeks….benchmark Canadian Crude (Western Canada Select) traded at a $17.50 discount…at only $40!

NatGas: NYMEX January delivery Nat Gas was $4.65 mid-November…contagion knocked it down 21% in 3 weeks.

Coal: the Market Vectors Coal ETF (overall performance of the global coal industry) closed last week at its lowest since early 2009…down over 70% from 2011 highs…down 25% since August.

The TSE lost 1400 pts (9.25%) the last 3 weeks and is barely positive YTD.

Interest Rates: US Treasury bonds were bid aggressively higher all week…the 10 year closed the week at 2.08% yield…a 2 year low…only a hair away from All Time Lows…Best performing asset 2014? US long term Treasury bonds…up 25%…compared to the S+P 500 up only 8%….BUT…

Junk and High Yield Credit…especially Energy related…got HAMMERED last week…with yields at 3 year HIGHS for the sector…energy yields were worse…credit spreads widened with a vengeance!

Currencies: CAD closed at 86.40…its lowest since 2009…it takes C$1.155 to buy US$1.00. CAD was 94 cents at the end of June when Crude began to fall…CAD is down only 8% since June…while WTI is down 47%. Other oil producing country currencies are down much more that CAD…CAD in NOT just a “commodity currency” but while Market Psychology is in its current “shoot first and ask questions later” mood CAD will get sold.

Mexican Peso: Since June the Mexican Peso is down 15%…the Norwegian Krone is down 23%…the Australian Dollar is down 11.5%…the Russian Ruble is down 70%.

The USD Index weakened ~1% last week as Euro and Yen “bounced”…nearly all other currencies fell Vs. the USD.

Gold: closed last week at 6 week highs…following a very interesting Reversal from the December 1 lows.

Short Term Trading:

We’ve been making US Dollar bullish trades in the currency markets all year. Since early November we’ve been especially shorting (and writing calls against) CAD and AUD futures as commodities generally…and Crude specifically…tumbled. We’ve added to short CAD positions each of the last 2 weeks as CAD weakened past 1.14 and then 1.15. On Friday…as CAD fell to 5 ½ year lows we wrote short-dated OTM puts (profit lock) as IV soared.

We bought gold early December…we were very impressed with the Dec 1 Reversal…we would add if gold rallies above $1250.

We sold short the S+P early last week…added to the position Thursday…then sold very short-dated OTM puts against part of our short position Friday (profit lock) as put values soared with the tumbling stock market.

Trading Perspective:

We expect global deflationary pressures to intensify…inflicting pain on the “Reaching for Yield” trade. We remain USD bulls…USD Cash is King! We are near-term bearish stocks.

With only two weeks left in the year money managers may try to lock in YTD performance by selling or hedging…margin calls and tax-loss selling may create additional pressure…credit market contagion worries will keep Market Psychology risk averse…currency markets may be especially choppy on thin year-end volumes.

Oil prices plunged to their lowest prices in five years last week after the International Energy Agency (IEA) downgraded its forecast for global oil demand for the fifth time in six months.

The IEA report told markets that global growth will remain weak in 2015, triggering an across-the-board sell-off in stocks and junk bonds on Friday that left the major indices with some of their worst percentage losses in three years.

Unfortunately, stocks are still trading within a few percentage points of record highs reached only a week ago and remain severely overvalued in the context of seriously deteriorating economic fundamentals.

Investors that were complacently expecting stocks to melt up to “Dow 18,000” and “S&P 2,100” by year-end are now facing a the much grimmer reality of a correction and even the potential of a bear market in 2015.

By the Numbers

On the week, the Dow Jones Industrial Average plunged by 678 points or 3.8% to close at 17,280.82, its largest point and percentage drop since 2011. Only a week ago on December 5, the Dow hit a record closing high of 17,958.79.

The S&P 500 collapsed by 73 points or 3.5% to end the week at 2002.53 after closing a week earlier in December 5 at a record closing high of 2,075.37. The Nasdaq Composite Index fell by 127 points or 2.7% to end at 4653.6 and the small cap Russell 2000 dropped 29.99 points or 2.5% to end the week at 1,152.45. European stocks also got hammered and saw their biggest losses since 2011.

Falling Oil Prices are Taking Stocks With Them

Stocks followed oil lower. Crude futures fell $8.03 per barrel or 12.2% to $57.81, their lowest level since the depths of the financial crisis in 2009, down 46% from crude’s 52-week closing high of $102.26 per barrel in June. More alarmingly, the price has completely fallen out of bed in the last three weeks, plunging by 24%. For the uninformed, which appears to include the entire financial media and most of the so-called experts who appear on their television shows, prices do not collapse that quickly due to oversupply; demand is melting away like a glacier in the summer sun because the global economy is deteriorating under the weight of too much debt and geopolitical problems. The question now is how quickly stocks will catch up to this inexorable reality and how widespread the damage will be.

Why This Flattening Yield Curve Signals a Gaining Bear

Anyone who questions the burgeoning economic weakness rearing its ugly head in the oil patch but about to spread far beyond North Dakota and South Texas and OPEC should pay careful attention to what is happening in the bond market. The U.S. Treasury curve flattened significantly this week, a phenomenon that has been occurring all year but is accelerating.

While moves in the yield curve are somewhat technical, they are extremely important for investors to understand because they establish the price of money in the economy. A flattening yield curve means that the difference in the price between short-term money and long-term money is diminishing which is a sign that lenders expect the economy to slow. On the shorter end, the 2/10 curve flattened by 21 basis points from 175 to 154 basis points last week and is down sharply from 261 basis points at the beginning of 2014. On the longer end, the 2/30 curve flattened by 13 basis points last week to 219 basis points and is down from 353 basis points at the beginning of the year.

Equally important, absolute yields are now moving down to levels that suggest that economic growth is slowing with the yield on the benchmark 10-year Treasury falling 21 basis points on the week to close at 2.1% and the yield the 30-year falling 22 basis points to close at 2.75%. Despite the fact that the U.S. economy has seen real growth (i.e. growth ex-inflation) of better than 3% during five of the last six quarters, these yields are signaling a coming slowdown.

We are taught that a bear market cannot begin until the yield curve inverts, but we are about to learn whether this rule-of-thumb still applies when interest rates have been pushed to the zero boundary by Federal Reserve policies that have distorted the value of all financial assets. Low interest rates are a sign of a weak economy. The fact that interest rates are so low suggests that something is amiss and should be flashing a warning sign to investors in stocks.

This month marks the sixth anniversary of the Fed’s decision to drop the Federal Funds rate to 0-25% and keep it there long past the ostensible end of the financial crisis. What markets are going to find out – and what some of us have been warning all along – is that the crisis never ended but instead morphed from a fast-moving study in chaos theory and contagion to a slow moving event in which the Fed was praying for fiscal policy makers to come to their rescue with pro-growth policies.

Such policies are desperately needed to create sufficient productive capacity in the economy to generate enough income to service and repay the more than $100 trillion of debt that now exists in the world. Alas, no such miracle has occurred and the world is now left to figure out how to deal with this unsustainable debt burden. The options are both obvious and distressing (literally and psychologically). Fiat currencies will have to be further debauched and financial assets that have been inflated in value will now have the air let out of them. The only question is how quickly these adjustments will occur.

This Subtle Change in the Junk Bond Market Will Signal Real Distress

The drop in oil prices is just the first wave of deflation that will hit markets over the coming years. In addition to the deflationary signals being emitted by commodity prices led by oil, Japan and Europe are also exporting deflation through their central banks’ easing policies. The world is experiencing a massive currency war and one of the currencies now in play is oil. Geopolitical pressures have added to world’s tolerance for low oil prices or, phrased more bluntly, the Saudis are willing to bear the pain of lower oil prices to hurt Iran, ISIS and Russia and have the full backing of the U.S. and other Western nations to do so.

When $1 trillion and counting of money is removed from the global economy, which is what is happening with the price of oil effectively being cut in half, economic activity drops sharply and inflation morphs into deflation. Commodity prices and the yield curve are telling us that the U.S. is heading for both a growth scare and a recession. The question is whether an economy as leveraged as the United States is still capable of experiencing a mere recession or whether something much worse is in store.

The bloodbath that is unfolding in the energy sector of the high yield bond market could easily spread to the rest of that market, which has been trading at grossly overvalued levels for the last three years as investors have been duped into believing that five and six percent yields are sufficient compensation for owning what remain hybrid debt/equity instruments that pose a real risk of principal loss. The average yield on energy bonds has jumped to 9.42% from a record low 4.87% just six months ago (a level that should have told holders of these bonds to be selling). The average energy sector bond now trades at 87.7 cents on the dollar, a level that could easily move 10 or 20 points lower if contagion spreads.

Energy bonds approximately 15% of the junk bond market but oil itself has an impact on a much broader array of industries. The option-adjusted spread on the Barclays High Yield Index has widened out to 504 basis points but the average yield on the index is still only 6.83%, far below distressed levels. If current trends continue, spreads and yields could easily widen by another 300 basis points which would still leave them far shy of distressed levels.

Absolute yields will continue to be suppressed by lower benchmark Treasury rates so the telling sign that investors should look for is whether junk bond investors stop basing their valuations on spreads and start looking for absolute returns that accurately represent the risks they are taking.

When that happens, the market will truly be in crisis mode. Today’s junk bond market is characterized by thin dealer inventories, a buyer’s strike among distressed and event-driven sellers, and concentrated ownership among ETFs and large institutions which has led to a truly horrible liquidity picture. Despite the bold talk from Wall Street and some large investors like Blackstone and Oaktree, it won’t take much more pain to send the market into a full-throated selling panic.

What Investors Should Do Now

What investors should be doing to prepare for them depends on their individual situations but at the very least they should be either significantly reducing or hedging their stock and junk bond exposures.

More aggressive and sophisticated investors can take steps to profit from the coming correction through options strategies and short selling strategies.

And everyone should be buying physical gold. What is happening is entirely a consequence of a failing monetary policy regime.

This may not be the end of that regime, but this is what the death rattles sound like.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair