Asset protection

This week’s Outside the Box continues with a theme that I and my colleague Worth Wray have been hammering on for some time: the very real potential for a rising dollar to trigger the next global financial crisis.

We are concerned about the consequences of multi-speed economic growth around the world and the growing divergence between major central banks. In our opinion, if these trends persist, they likely mean (1) a major US dollar rally, (2) a rapid unwind of QE-induced capital flows to emerging markets, (3) a hard slide in fragile emerging-market and commodity-exporter currencies, and (4) financial shocks capable of ushering in a new global financial crisis.

Alongside true macro legends like Kyle Bass, Raoul Pal, Luigi Buttiglione, and Raghuram Rajan, Worth and I have written about this theme extensively in 2014 (“Central Banker Throwdown,” “Every Central Bank for Itself,” “The Cost of Code Red,” “Sea Change,” “A Scary Story for Emerging Markets”). Now it’s quickly becoming a mainstream macro theme on almost everyone’s radar. Virtually every economist and investment strategist on Wall Street has a view on the US dollar and the QE-induced carry trade into emerging markets… and anyone who doesn’t should start looking for a different job.

Policy divergence is really the only macro theme that matters right now. And on that note, the Bank for International Settlements just released its predictably must-read quarterly review, with an urgent warning:

The appreciation of the dollar against the backdrop of divergent monetary policies may, if persistent, have a profound impact on EMEs [emerging-market economies]. For example, it may expose financial vulnerabilities as many firms in emerging markets have large US dollar-denominated liabilities. A continued depreciation of the domestic currency against the dollar could reduce the credit worthiness of many firms, potentially inducing a tightening of financial conditions.

Echoing those comments on Twitter, the “bank for central banks” reiterated how this trend affects all of us (feel free to follow us at @JohnFMauldin and @WorthWray):

@BIS_org: US dollar as global unit of account in debt contracts means a stronger dollar constitutes tightening of global financial conditions.

This is in spite of continued efforts by central banks to ease monetary conditions. Calling attention to that very risk in our Halloween edition of Thoughts from the Frontline, Worth explained that the catalysts are already in position to spark a collapse in a number of fragile emerging markets if the dollar moves even modestly higher (into the low 90s on the DXY Index); but we have struggled to quantify the actual size of the nebulous USD-backed carry trade that could now come unwound at any moment.

Reasonable estimates range from $2 trillion to $5 trillion. The true number could be even larger if more speculative money has slipped through the cracks than has been officially reported in places like China; or it could be smaller if a significant portion of recent inflows represents a more permanent deepening of emerging-market financial systems rather than an attempt to escape financial repression in the developed world. It’s hard to know for sure, and that’s why this week’s Outside the Box is so important.

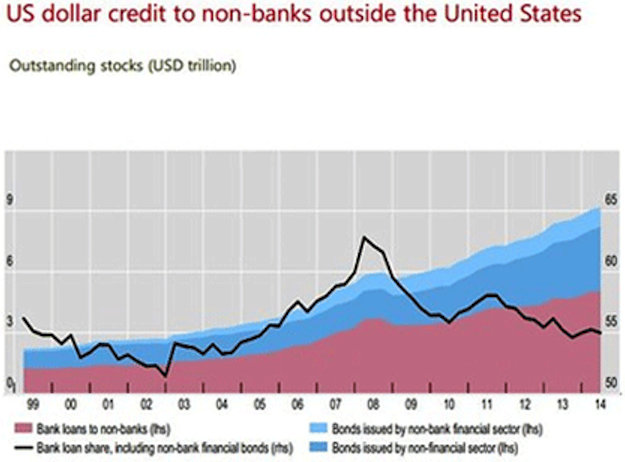

In a recent presentation at the Brookings Institution, BIS Head of Research and Princeton University Professor Hyun Song Shin shared his research revealing that dollar-denominated credit to non-bank offshore borrowers is now more than $9 TRILLION and at serious risk in the event of continued policy divergence.

I’d encourage you to listen to or download an audio recording of Dr. Shin’s presentation, and take some time to flip through his slides; but David Wessel’s cogent summary, which follows in today’s Outside the Box, will give you an idea of what may happen as the US dollar rallies. It’s short, sweet, and REQUIRED READING for anyone who wants to understand where the global financial system is heading in the coming quarters.

Then we wrap up with an essay on the same theme by my friend Mohamed El-Erian, who is typically not as strident in his wording; but for those of us who know Mohamed, this is the equivalent of him pounding the table:

Avoiding the disruptive potential of divergence is not a question of policy design; there is already broad, albeit not universal, agreement among economists about the measures that are needed at the national, regional, and global levels. Rather, it a question of implementation – and getting that right requires significant and sustained political will.

The pressure on policymakers to address the risks of divergence will increase next year. The consequences of inaction will extend well beyond 2015.

For readers interested in this theme, let me also offer a link to some on-the-record remarks from Claudio Borio, the head of the Monetary and Economic Department at the BIS, and Dr. Shin, preceding the release of the BIS quarterly report. For a representative of such a staid and sober organization, Mr. Borio uses a lot of rather disconcerting terms. He is clearly very concerned. Again, you can read the full BIS quarterly review here.

I’ve spent some time this week working with Jack Rivkin and our respective teams at Altegris and Mauldin Economics, putting together the lineup for our 2015 Strategic Investment Conference. I think it will be our best conference ever. You should definitely save the dates April 29 through May 2, as this will be a can’t-miss conference. We will get you more details soon.

I trust your week is going well. We are planning for the holidays and looking forward to some great family time. We’ll see if a new grandchild shows up in time for Christmas or decides to become a New Year’s baby.

Your thinking about 2015 analyst,

John Mauldin, Editor

Outside the Boxsubscribers@mauldineconomics.com

How the Rising Dollar Could Trigger the Next Global Financial Crisis

By David Wessel

Wall Street Journal, Dec. 7, 2014

A slide from Hyun Song Shin’s presentation to the Brookings Institution on financial stability risks shows the Bank for International Settlement’s analysis of dollar lending to non-banks outside of the United States.

Bank for International Settlements

Hyun Song Shin, who is on leave from Princeton while chief economist at the Bank for International Settlements in Basel, spends a lot of time wondering what could cause the next financial crisis. He suspects it will be something different from the leveraged bets on housing that were at the root of the last crisis.

So, what might it be? Perhaps the steady rise of the U.S. dollar on global currency markets.

In recent presentations at the Brookings Institution, Mr. Shin documented the growing use of the U.S. dollar by borrowers and lenders outside of this country. U.S. banks and bond investors have lent $2.3 trillion outside the U.S. Foreign banks and foreign bond investors have lent much more: $6.5 trillion.

(Mr. Shin and colleagues at the Bank for International Settlements elaborated on his latest analysis in the bank’s new Quarterly Review posted Sunday.)

Here’s how Mr. Shin sees the world: A manufacturer in an emerging market borrows in dollars, perhaps because it sells a lot of goods in dollars and sees borrowing in dollars as a hedge. A local bank lends the dollars, borrowing from some big global bank. When the emerging-market currency is strong and the dollar is weak, that manufacturer’s balance sheet looks sturdier–and the local bank sees that and lends more readily. Thus a weak dollar can lead to a global credit boom.

When the dollar rises, though, all this runs in reverse, effectively tightening global financial conditions, particularly in emerging markets. The emerging-market currency falls. The manufacturer has trouble making payments on its dollar loans; so do its peers. Banks lend less readily. Capital investment stalls. Global money managers–the ones with lots of short-term wholesale deposits that search the world for the best yields–see a falling local currency and a weakening economy and pull money from the emerging-market banks.

Then, global asset managers who had been lured by a high-growth story see that it is now over and do the same thing, selling emerging-market corporate bonds. That pushes up interest rates that businesses in emerging markets have to pay, and weakens them further in a vicious cycle.

“Even if you have long-term investors and you don’t have [leveraged investors], if events in the financial markets translate into events in the real economy, you can get a feedback loop,” Mr. Shin says. And this, he adds, is a very different mechanism than the insolvency of highly leveraged financial institutions that was at the heart of the recent global financial crisis.

All this is a timely reminder that all the important steps taken to strengthen the foundations of the world’s banks in response to the last crisis aren’t a cause for complacency.

David Wessel is director of the Brookings Institution’s Hutchins Center on Fiscal & Monetary Policy and a contributing correspondent to The Wall Street Journal. He is on Twitter: @davidmwessel.

One of my old rules of trading is that whenever a major asset class, index, or other benchmark has a sudden, rapid move in price, something blows up. Sky high. (related by John Mauldin – How the Rising Dollar Could Trigger the Next Global Financial Crisis – Editor Money Talks)

One of my old rules of trading is that whenever a major asset class, index, or other benchmark has a sudden, rapid move in price, something blows up. Sky high. (related by John Mauldin – How the Rising Dollar Could Trigger the Next Global Financial Crisis – Editor Money Talks)

That’s because people get used to regimes. They get used to a certain state of affairs with a lack of volatility. They become complacent. Maybe they stop hedging. Maybe they allow themselves to have unbounded downside risk. Maybe they start gambling.

In the last month, we’ve seen massive moves in the dollar and oil—and I assure you, someone is going to get hurt.

So far I haven’t said anything controversial. Energy companies are going to get hurt by lower oil prices. Exporters are going to get hurt by a rising dollar. A chimpanzee could figure this out.

But there are second-order effects. People are starting to figure out that Canadian banks are going to get hurt by the lack of investment banking business from the energy sector, and the stocks are getting punished.

And there are third-order effects too, which people will soon discover.

If you sit around and think hard enough, you can make these sorts of connections. Some people are very good at this. A commodity price moves fast, and they can figure out the point of maximum pain for some company far down the supply chain from the actual commodity.

I’m not that smart. But I’m smart enough to get out of the way when something big and important like oil moves 40%.

Let’s step into our time machine and set the dial to 1994. That was the year when interest rates backed up a couple of percentage points. Remember the bond market vigilantes? They were pricing in Hillarycare and a Democratic Party wish list, and they caned the bond market until interest rates were making borrowers squeal.

But what was interesting about 1994 was that in the grand scheme of things, interest rates didn’t go up all that much. Just a couple of percentage points. Now, if I asked you who you thought would get hurt by rising rates, you might say banks, hedge funds. And you would be wrong. Who got hurt by rising interest rates?

Procter & Gamble.

Orange County, CA.

Mexico.

Why did the first two blow up? Derivatives.

By the way, I’m not referring to derivatives pejoratively. I’ve spent most of my adult life trading them. They’re not financial weapons of mass destruction. What they do is take risk over here and move it over there. So if bank XYZ was negatively exposed to higher interest rates, they were able to offset that exposure to Orange County through derivatives.

Of course, the derivatives Orange County was trading were very exotic and clearly unsuitable for a municipality, but that’s a discussion for another time over a burger and a beer. The point is that rates moved, and they moved fast, and stuff blew up.

But not the stuff you thought would blow up.

Buying Volatility on the Cheap

So I know what you’re going to ask me next: What’s going to blow up?

Who knows? By definition, you can’t know, especially when the risk has been laid off through derivatives.

But this is how it works: Oil moves 40%, the dollar moves 10-15%, and someone’s out of business. It could be someone big. It could be someone systemically important, someone that could really spook the markets. So when stuff like this happens, I get myself exposure to things that gain from disorder (paraphrasing Black Swan author Nassim Taleb).

With the S&P 500 Index (SPX) at 2,050 and the CBOE’s Volatility Index (VIX) at about 15, systemic risk is vastly underpriced.

I’m not saying that stocks are too high, that I’m bearish. I’m just saying that the derivatives markets aren’t pricing in what could be a big unwind based on these oil and dollar moves.

Translation: volatility is cheap.

Is $60 oil bullish for stocks, long term? Absolutely. It is one of the most bullish things I can think of. One of my clients recently told me that this decline in oil will result in $100,000 in annual fuel savings for his business. Multiply that times everyone. So bullish. And the dollar, also long-term bullish. But in the short term, there’s an Amaranth out there somewhere, potentially.

Maybe it’s not a hedge fund. Maybe it’s a company like Coca-Cola (KO) that gets the majority of its earnings from overseas. Maybe it’s the railroads. The person who can figure this out wins the prize.

As I said before, I’m not that smart… just a former trader with scabs on his knuckles. But the funny thing about those traders—especially the ones over 40—is they have a nose for trouble. I’m all in favor of bullish developments, just not when they happen really fast and nobody is ready, which is how people get maimed.

Position: long three-month SPY puts, short Canadian Imperial Bank of Commerce (CM) and Toronto-Dominion Bank (TD) (the US-listed shares).

Jared Dillian

A glance at any gold price chart reveals the severity of the bear mauling it has endured over the last three years.

More alarming, even for die-hard gold investors, is that some of the fundamental drivers that would normally push gold higher, like a weak US dollar, have reversed.

Throw in a correction-defying Wall Street stock market and the never-ending rain of disdain for gold from the mainstream and it may seem that there’s no reason to buy gold; the bear is here to stay.

If so, then I have a question. Actually, a whole bunch of questions.

If we’re in a bear market, then…

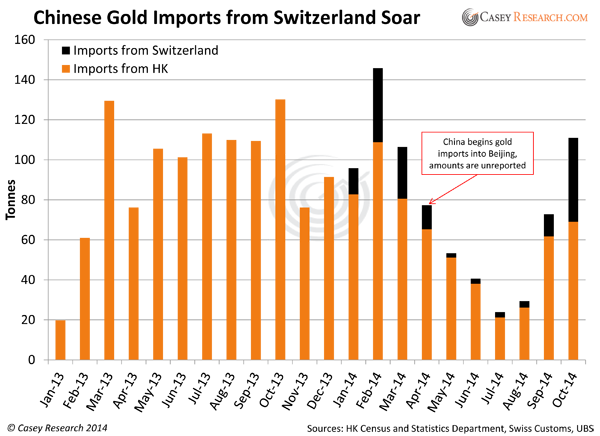

Why Is China Accumulating Record Amounts of Gold?

Mainstream reports will tell you Chinese imports through Hong Kong are down. They are.

But total gold imports are up. Most journalists continue to overlook the fact that China imports gold directly into Beijing and Shanghai now. And there are at least 12 importing banks—that we know of.

Counting these “unreported” sources, imports have risen sharply. How do we know? From other countries’ export data. Take Switzerland, for example:

So far in 2014, Switzerland has shipped 153 tonnes (4.9 million ounces) to China directly. This represents over 50% of what they sent through Hong Kong (299 tonnes).

The UK has also exported £15 billion in gold so far in 2014, according to customs data. In fact, London has shipped so much gold to China (and other parts of Asia) that their domestic market has “tightened significantly” according to bullion analysts there.

Why Is China Working to Accelerate Its Accumulation?

This is a growing trend. The People’s Bank of China released a plan just last Wednesday to open up gold imports to qualified miners, as well as all banks that are members of the Shanghai Gold Exchange. Even commemorative gold maker China Gold Coin could qualify to import bullion. Not only will this further increase imports, but it will serve to lower premiums for Chinese buyers, making purchases more affordable.

As evidence of burgeoning demand, gold trading on China’s largest physical exchange has already exceeded last year’s record volume. YTD volume on the Shanghai Gold Exchange, including the city’s free-trade zone, was 12,077 tonnes through October vs. 11,614 tonnes in all of 2013.

The Chinese wave has reached tidal proportions—and it’s still growing.

Why Are Other Countries Hoarding Gold?

The World Gold Council (WGC) reports that for the 12 months ending September 2014, gold demand outside of China and India was 1,566 tonnes (50.3 million ounces). The problem is that demand from China and India already equals global production!

India and China currently account for approximately 3,100 tonnes of gold demand, and the WGC says new mine production was 3,115 tonnes during the same period.

And in spite of all the government attempts to limit gold imports, India just recorded the highest level of imports in 41 months; the country imported over 39 tonnes in November alone, the most since May 2011.

Let’s not forget Russia. Not only does the Russian central bank continue to buy aggressively on the international market, Moscow now buys directly from Russian miners. This is largely because banks and brokers are blocked from using international markets by US sanctions. Despite this, and the fact that Russia doesn’t have to buy gold but keeps doing so anyway.

Global gold demand now eats up more than miners around the world can produce. Do all these countries see something we don’t?

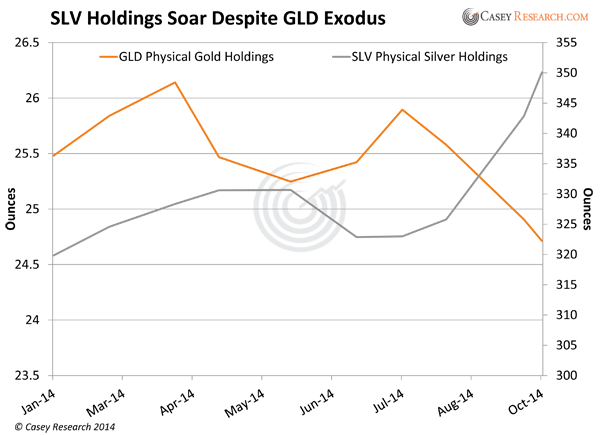

Why Are Retail Investors NOT Selling SLV?

SPDR gold ETF (GLD) holdings continue to largely track the price of gold—but not the iShares silver ETF (SLV). The latter has more retail investors than GLD, and they’re not selling. In fact, while GLD holdings continue to decline, SLV holdings have shot higher.

While the silver price has fallen 16.5% so far this year, SLV holdings have risen 9.5%.

Why are so many silver investors not only holding on to their ETF shares but buying more?

Why Are Bullion Sales Setting New Records?

2013 was a record-setting year for gold and silver purchases from the US Mint. Pretty bullish when you consider the price crashed and headlines were universally negative.

And yet 2014 is on track to exceed last year’s record-setting pace, particularly with silver…

- November silver Eagle sales from the US Mint totaled 3,426,000 ounces, 49% more than the previous year. If December sales surpass 1.1 million coins—a near certainty at this point—2014 will be another record-breaking year.

- Silver sales at the Perth Mint last month also hit their highest level since January. Silver coin sales jumped to 851,836 ounces in November. That was also substantially higher than the 655,881 ounces in October.

- And India’s silver imports rose 14% for the first 10 months of the year and set a record for that period. Silver imports totaled a massive 169 million ounces, draining many vaults in the UK, similar to the drain for gold I mentioned above.

To be fair, the Royal Canadian Mint reported lower gold and silver bullion sales for Q3. But volumes are still historically high.

Why Are Some Mainstream Investors Buying Gold?

The negative headlines we all see about gold come from the mainstream. Yet, some in that group are buyers…

Ray Dalio runs the world’s largest hedge fund, with approximately $150 billion in assets under management. As my colleague Marin Katusa puts it, “When Ray talks, you listen.”

And Ray currently allocates 7.5% of his portfolio to gold.

He’s not alone. Joe Wickwire, portfolio manager of Fidelity Investments, said last week, “I believe now is a good time to take advantage of negative short-term trading sentiment in gold.”

Then there are Japanese pension funds, which as recently as 2011 did not invest in gold at all. Today, several hundred Japanese pension funds actively invest in the metal. Consider that Japan is the second-largest pension market in the world. Demand is also reportedly growing from defined benefit and defined contribution plans.

And just last Friday, Credit Suisse sold $24 million of US notes tied to an index of gold stocks, the largest offering in 14 months, a bet that producers will rebound from near six-year lows.

These (and other) mainstream investors are clearly not expecting gold and gold stocks to keep declining.

Why Are Countries Repatriating Gold?

I mean, it’s not as if the New York depository is unsafe. It and Ft. Knox rank as among the most secure storage facilities in the world. That makes the following developments very curious:

- Netherlands repatriated 122 tonnes (3.9 million ounces) last month.

- France’s National Front leader urged the Bank of France last month to repatriate all its gold from overseas vaults, and to increase its bullion assets by 20%.

- The Swiss Gold Initiative, which did not pass a popular vote, would’ve required all overseas gold be repatriated, as well as gold to comprise 20% of Swiss assets.

- Germany announced a repatriation program last year, though the plan has since fizzled.

- And this just in: there are reports that the Belgian central bank is investigating repatriation of its gold reserves.

What’s so important about gold right now that’s spurned a new trend to store it closer to home and increase reserves?

These strong signs of demand don’t normally correlate with an asset in a bear market. Do you know of any bear market, in any asset, that’s seen this kind of demand?

Neither do I.

My friends, there’s only one explanation: all these parties see the bear soon yielding to the bull. You and I obviously aren’t the only ones that see it on the horizon.

Christmas Wishes Come True…

One more thing: our founder and chairman, Doug Casey himself, is now willing to go on the record saying that he thinks the bottom is in for gold.

I say we back up the truck for the bargain of the century. Just like all the others above are doing.

With gold on sale for the holidays, I arranged for premium discounts on SEVEN different bullion products in the new issue of BIG GOLD. With gold and silver prices at four-year lows and fundamental forces that will someday propel them a lot higher, we have a truly unique buying opportunity. I want to capitalize on today’s “most mispriced asset” before sentiment reverses and the next uptrend in precious metals kicks into gear.

It’s our first ever Bullion Buyers Blowout—and I hope you’ll take advantage of the can’t-beat offers. Someday soon you will pay a lot more for your insurance. Save now with these discounts.

On the heels of continued chaos around the globe and with many stock markets hitting new highs, today a 40-year market veteran sent King World News a powerful piece discussing the fact that the New World Order “gangs” are now pushing the world to the brink. Below is what Robert Fitzwilson, founder of The Portola Group, had to say in this exclusive piece for King World News.

Continue reading the Robert Fitzwilson piece HERE

Everyone always says, I want to buy low and I want to sell high. So I think for me, of course I own a lot of gold, and I need to buy more to keep asset allocation between 25% in Real Estate, 25% in equities, 25% cash and bonds, and 25% gold. I need to buy more. So for me this is a very happy event. I don’t like to buy gold at $1,900 like in 2011. I like to buy it here or lower.

Everyone always says, I want to buy low and I want to sell high. So I think for me, of course I own a lot of gold, and I need to buy more to keep asset allocation between 25% in Real Estate, 25% in equities, 25% cash and bonds, and 25% gold. I need to buy more. So for me this is a very happy event. I don’t like to buy gold at $1,900 like in 2011. I like to buy it here or lower.

Gold Broker: Do you think it will break under $1,000 like some people say?

Marc Faber: Look. The forecasting record of people is horrible, in particular, the forecasting record of the Federal Reserve. So, I don’t know, maybe it will go below $1,000 but my sense is that it will not stay below $1,000. …. I would use the current weakness as a buying opportunity. … I’m telling everybody, you as an investor, and me as an investor, we cannot trust the government. … I am my own central banker. I keep my own physical gold. I do not trust anyone of these (unprintable word).

…the above posted on Marc’s website Dec 4th. The following on Dec 3rd & Dec 2nd.

In Europe we have a flat inaudible Economy

Fed Monetary Policy Will Destroy World

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair