Asset protection

Protectionist trade policies have really been whipsawing the market. The S&P 500’s seven-day defiant rally in the face of ongoing trade war bluster has suddenly been stopped in its tracks after president Trump escalated China tariffs from $34 billion to $200 billion—or at least has threatened to. Still, there are stocks that remain on the upswing and are likely to continue riding long-term trends despite ongoing trade wars and geopolitical instabilities…. CLICK for the complete article

Perhaps the most interesting observation of how Trump handles negotiations is that he approaches them as a businessman rather than a politician. He certainly does not play nicely or puts on the pretends that everything is wonderful in the land of politics. Indeed, NATO officials were on edge and nervously welcomed President Trump who arrived in Brussels on Tuesday night. They were afraid he would behave “badly” over the two-day meeting. Normally, NATO summits are fixed in advance and proceed in an orderly fashion to create the image that everyone is in solidarity. This summit began strikingly differently on a most divisive footing in NATO’s 69-year history.

From the opening bell, Trump’s first words signaled this meeting was not going to be boring or politically correct. Trump openly complained that Germany was totally controlled by Russia and that German politicians had been working for Russian energy companies after leaving politics and said this was inappropriate. As the head of NATO Mr. Stoltenberg immediately looked very uncomfortable, Trump continued his assault in a very unrelenting manner as you would in a business negotiation in a hostile takeover. Trump said: “I think it is very sad when Germany makes a massive oil and gas deal with Russia.” He continued saying that “we” are supposed to be guarding against Russia, and Germany goes out and pays billions and billions of dollars a year to Russia. “We are protecting Germany, we are protecting France, we are protecting all of these countries and then numerous of the countries go out and make a pipeline deal with Russia where they are paying billions of dollars into the coffers of Russia. I think that is very inappropriate.”

Trump kept up the aggressive negotiating stand. “It should never have been allowed to happen. Germany is totally controlled by Russia because they will be getting 60-70% of their energy from Russia and a new pipeline. … You tell me if that’s appropriate because I think it’s not. On top of that Germany is just paying just a little bit over 1% [of GDP on NATO defense contributions] whereas the United States is paying 4.2% of a much larger GDP. So I think that’s inappropriate also.”

For decades, American politicians complained about European tariffs against American products while the US was paying the bulk of the cost for both the United Nations and for NATO expanding the US national debt year after year. Trump was the first President to openly come out and say publicly: “I think it is unfair,” Trump said. No other American president had ever raised European defense spending as a major negotiating tactic linking it to trade. Trump openly came out and bluntly said: “We can’t put up with it!”

After things calmed down, Merkel herself, speaking through an interpreter, said that the meeting was an “opportunity to have an exchange about economic developments … and also the future of our trade relations.” Trump managed to convert the normally separate NATO boring meeting and linked it to trade. Of course, the American press will not report the real tactics going on. They are too busy trying to impeach him.

one year ago Harley Bassman, more familiar to Wall Street traders as the “Convexity Maven” – a legend in the realm of derivatives (he helped design the MOVE Index, better known as the VIX for government bonds) – decided to retire (roughly one year after his shocking suggestion that the Fed should devalue the dollar by buying gold).

But that did not mean he would stop writing, and just a few days after exiting the front door at 650 Newport Center Drive in Newport Beach for the last time, Bassman started writing analyst reports as a “free man”, in which the topics were, not surprisingly, rates, derivatives, cross asset interplay and, of course, convexity.

And, in his latest note, Bassman takes on a topic that has become especially dear to the Fed and most market observers: the continued flattening of the yield curve, the timing of the next recession, and what everyone is looking but fails to see, or – as he puts it – what is truly different this time…. CLICK for the complete article

Classic and collectible cars have been the best-performing asset for the last two-, five- and 10-year periods (see “Return on investment,” below). This proves that they are no longer simply a novelty for the wealthy collector, but a genuine alternative investment strategy. WMG recently launched its Collectable Car Fund to exploit that fact.

The last decade for classic cars has been lucrative. Certain marques have risen four-fold in value — the rising tide has lifted almost every boat. A Ferrari 250 GTO built for Sir Stirling Moss was sold for $8.5 million in 2002; a decade later the same car was sold for a staggering $35 million. In 2014 a 250 GTO sold for just over $38 million — a record for a car sold publicly. However, in 2016 Simon Kidston, founder of the K500, sold a Ferrari 250 GTO for an undisclosed sum that reportedly exceeded that record. Talk on the street is the car sold for more than $60 million.

In 2013, RM Auctions sold a Ferrari F50 with 10,000 kilometers on the clock for €560,000 ($783,044). In early 2017, RM Auctions sold an F50 with 2,000 kilometers on the clock for €2.64 million ($3.18 million).

Historically speaking, classic cars have been a buoyant, liquid market, but one that requires discipline and deep knowledge of the underlying asset class. The pitfalls of sloppiness are deep and costly. However, it does offer resilience to wider traditional market trends. During the financial crisis of 2008 to 2011, smart money flowed into the asset class as a safe haven. The K500 Classic Car Index outperformed all investment benchmarks during the 2008 crash (see “Port in a storm,” page below).

The Trend is Your Friend

Alternatives grew to over $3.6 trillion in 2016, up 3% on 2015 according to a Financial Times report citing a major U.S. bank released in early 2017. This was a significant increase, as investors steer away from traditional long-only, value-driven investment classes. It doesn’t come as much of a surprise that the modern ultra-high net worth individuals (people with investable assets of at least $30 million, excluding personal assets) are ensuring investment portfolios include an exposure to much higher yielding alternative asset classes, including classic and collectible cars.

Until now there hasn’t been a regulated investment fund to get exposure to collectible cars, which as an asset class is up more than 400% in the last decade (see “Return on investment”). If you’re a high-net worth investor, family office or wealth manager, portfolio exposure to wine or stamps is a common investment. So, why not cars? Well, unless you have a large storage facility, a team of mechanics, detailers, insurers, transporters, security guards and a concierge to rotate the tires, investing in collectible cars can be complex and expensive.

Pedigree

Compare a 1982 Chateau Lafite and a Series 1 Ferrari 250 GTO; both investable assets, both valuable and likely will come with a magnificently documented history. While both are investments of passion, only one of them can truly be enjoyed without value erosion. In reality, a 50-kilometer journey in the 250 GTO isn’t going to materially change the car’s value. Enter it into a classic race or Concours event and it could even enhance it, but the ‘82 Lafite should you dare remove the cork after paying 20% tax on delivery, becomes worthless. Investments in classic cars are also free from capital gains tax.

Ferrari 250 GTO

So why have several attempts at starting a classic/collectible car fund in the UK failed? Because regulation has made it cumbersome. WMG Advisors LLP, as the appointed Fund Manager, is regulated by the Financial Conduct Authority (FCA) for investment business. Serious investors rarely commit capital to funds that are not regulated or where a team has little or no investment experience, regardless of their knowledge of the underlying asset. As an investment professional/collector of classic cars myself, the only risk to my investment should be the performance of the underlying asset. The UK’s FCA is one of the toughest regulators in the world, so it makes perfect sense for WMG to operate the car fund under its scrutiny. Second, investors will always look closely at the pedigree of the fund management team, which is where WMG’s USP becomes apparent – the team.

WMG’s Chairman Mehmet Dalman has a long career in investment banking/asset management, including managing director of Deutsch Morgan Grenfell and the only non-German Vorstand Member of Germany’s second-largest bank Commerzbank, where he founded the Securities division. It was on Commerzbank’s trading floor where Dalman and I met in the late 1990s and connected through a mutual life-long passion for exotic automobiles.

Dalman would often wander the London trading floor – then home to more than 300 trading professionals – engaging in conversation to get a feel for the mood in the market. We would spend two minutes discussing stock prices, but much longer on the market prices of the latest and greatest Ferraris, of which Dalman had already amassed an eye-watering collection, many of which he still owns today.

As a petrol-head with a 30-year track record of motorsport competing at both club and professional levels and a 20-year career as an investment banker, I would often assist Mehmet on new car specifications, helping choose color, wheel types and bespoke options. At the time I was driving a BMW, flirting with some of the most exotic car manufacturers in the world — on behalf of my boss, of course. I have built a huge automotive network in doing so, which lives on today — enter part 2 of WMG’s USP, the network.

With an aptitude for Capital Goods stocks, Automotive and Aerospace in particular, and after a 20-year career on some of London’s busiest trading floors, I quit the brokerage world due to an increasingly punitive environment ahead MiFID 2.

A meeting with Dalman at WMG’s Mayfair office in early 2016 revealed a joint aspiration to build and launch a car fund. Knowing he was a reputable collector, I went to see Mehmet to discuss a business idea — an ultra-high net worth individuals-based car concierge service that I had recently launched. It wasn’t long before my attention switched to the prospect of launching a proper investment grade car fund. I’d seen a few attempts previously, but knew what we could offer under WMG would be different; it would work.

As with any investment portfolio, diversity is key. A single car is not an investment, it’s a bet, same as a single-stock portfolio. WMG can offer the financial rewards of owning a McLaren F1 (up 1,000% since new) with none of the expenses or hassle. Classic car ownership costs can be considerable, but WMG has them comfortably controlled, thanks largely to efficiencies from the network.

One month ago, in a surprising reversal, we reported that Bridgewater was outperforming peers this year even after losing money in April, largely as a result of a a massive derisking, i.e. turning bearish. As Bloomberg further added, “the fund has also reduced its net long bets on U.S. equities to about 10 percent of assets from 120% earlier this year, and that overall, the fund is net short equities.”

And now we know why.

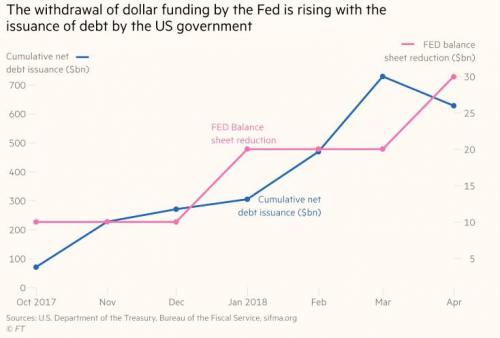

In one of Bridgewater’s latest Daily Observations authored by co-CIO Greg Jensen, the firm writes that “2019 is setting up to be a dangerous year, as the fiscal stimulus rolls off while the impact of the Fed’s tightening will be peaking” a point echoed yesterday by the head of the Indian central bank, Urjit Patel, who warned that unless the Fed ends its balance sheet reduction which comes as a time when the Treasury is soaking up dollar liquidity by issuing substantial amounts of Treasuries to fund the Trump budget, the tightening in financial conditions could lead to a global conflagration started by emerging markets.

And since asset markets lead the economy, Bridgewater continues, “for investors the danger is already here” and explains as follows:

Markets are already vulnerable, as the Fed is pulling back liquidity and raising rates, making cash scarcer and more attractive – reversing the easy liquidity and 0% cash rate that helped push money out of the risk curve over the course of the expansion. The danger to assets from the shift in liquidity and the building late-cycle dynamics is compounded by the fact that financial assets are pricing in a Goldilocks scenario of sustained strength, with little chance of either a slump or an overheating as the Fed continues its tightening cycle over the next year and a half.

….continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair