Asset protection

Mohamed A. El-Erian is the chief economic advisor for Allianz SE. Before joining Allianz, Dr. El-Erian held positions as chief executive and co-chief investment officer of PIMCO and president and CEO of Harvard Management Company, the entity that manages Harvard’s endowment and related accounts. Dr. El-Erian was also a managing director at Salomon Smith Barney/Citigroup in London and spent 15 years with the International Monetary Fund in Washington, DC.

Mohamed A. El-Erian is the chief economic advisor for Allianz SE. Before joining Allianz, Dr. El-Erian held positions as chief executive and co-chief investment officer of PIMCO and president and CEO of Harvard Management Company, the entity that manages Harvard’s endowment and related accounts. Dr. El-Erian was also a managing director at Salomon Smith Barney/Citigroup in London and spent 15 years with the International Monetary Fund in Washington, DC.

Dr. El-Erian has published widely on international economic and finance topics. His 2008 best-seller, When Markets Collide, was named a book of the year by The Economist, and one of the best business books of all time by The Independent (UK). He was one of Foreign Policy’s “Top 100 Global Thinkers” for four years in a row, and is a contributing editor for the Financial Times. His newest book – The Only Game in Town: Central Banks, Instability and Avoiding the Next Collapse – is another New York Timesbest-seller.

He replied to my questions in an email exchange on November 15.

What is your assessment of the overall health of the U.S. economy? In particular, do you agree with the narrative that the low unemployment rate (4.1%) indicates that we don’t suffer from a lack of aggregate demand?

The US economy is gaining momentum, on a standalone basis and as part of a synchronized pickup in global growth. This process would be turbocharged were Congress able to work with the administration to pass pro-growth measures, including tax reform and infrastructure. And, on the demand side, it would be further aided by an increase in the labor participation rate and higher wage growth in response to the sharp decline in the unemployment rate.

Last month, you wrote that investors must consider whether they are placing implicit bets on three scenarios: endogenous economic and financial healing, long-awaited policy breakthroughs and bigger liquidity waves. I’d like to ask about each of these. You’ve expressed optimism that the U.S. and Europe are on a path to sustained growth. Are you as optimistic about China and Japan?

Yes. All three factors have been important drivers of the impressive rally … and not just in stocks, but also other risk assets. They speak to actual liquidity support and endogenous economic improvements being reinforced by the prospects for policies that unleash the economy’s stronger growth potential. It is a critical policy handoff in order for fundamentals to eventually validate asset prices.

As regards the other two countries you ask about, China continues to navigate one of the most difficult phases in development economics – what the technocrats call the “middle income transition.” It’s a phase that requires changes to how the economy operates, and it is one that calls on the Chinese government to implement midcourse adjustments as needed.

Japan is in a tougher structural position, having acquired cyclical movement forward but lacking the secular momentum that China has. As such, it is even more critical that Prime Minister Abe’s recent poll victory translate into the implementation of what the government has called the “third arrow” – that is, measures aimed at improving growth responsiveness.

With regard to policy breakthroughs, what specific measures would be most positive for economic growth?

Tax reform, infrastructure and de-regulation, followed by further improvements in the actual and future functioning of the labor market – that in the context of educational reforms and greater skill acquisition. And all accompanied by better international policy coordination, including in order to reduce currency and trade tensions.

With regard to liquidity, you wrote that investors have been “enticed to become increasingly exposed to historically illiquid asset class segments.” Are there any of those historically illiquid asset classes that investors should be wary of, because their liquidity will not withstand a market downturn?

Yes, those whose dedicated investor base is relatively narrow in comparison to the potentially more volatile “cross-over” money that has flowed in. As an illustration, this would include parts of the high yield corporate bond markets and certain segments of emerging markets.

On November 1, you said that the Fed is on a “beautiful normalization” as it ends its easy-money policies. Could you elaborate?

The reference to a “beautiful normalization,” a phrase that I adapted from Ray Dalio’s concept of “beautiful deleveraging” which he popularized a few years ago, speaks to the Fed’s ability to stop asset purchases (QE), hike interest rates, and set out a plan for gradually reducing its $4.5 trillion balance sheet – all this without disrupting markets or derailing economic growth. I suspect that the Fed is able to continue on this orderly path of gradual and careful normalization of monetary policy.

The big question in central banking has morphed and migrated. It refers to whether more than one systemically important central bank – and, perhaps, as many as four more (the ECB, the Bank of Japan, the People’s Bank of China, and the Bank of England) can eventually also normalize at the same time.

The most serious forecast that we see from our computer models has been a rise in agricultural prices caused by Global Cooling – not Global Warming. Crops cannot grow without the sun and water. Historically, when the weather turns cold, the crops fail.

The most serious forecast that we see from our computer models has been a rise in agricultural prices caused by Global Cooling – not Global Warming. Crops cannot grow without the sun and water. Historically, when the weather turns cold, the crops fail.

Our database on wheat from 1259 forward (excluding our data on the Roman Empire grain prices), reveals that there is a serious risk of famine from 2020 onward. It appears that we may very well enter a 12-year rally into the year 2032. Our Bifurcation Models are reflecting also a gap in time between 2020 and 2031 suggesting a trend appears to last for that period of time.

The downside of taxation, and particularly inheritance taxes, has driven farmers to sell their land to conglomerates just to pay the inheritance taxes. This has resulted in genetically altering crops to increase yield. While genetically altered crops do not really appear to present a major health concern as many seem to argue, the real danger is the fact that during the past 100 years, 94% of the world’s edible seed varieties have vanished.

…also from Martin:

The Political Crisis in Germany Changes the Game

Merkel faces the worst crisis of her career and many behind the curtain are starting to wonder if she will even survive. The German Federal President Steinmeier could not actually order new elections immediately. The procedure in this regard is quite complicated in Germany. The earliest possible alternative would be to hold new elections come the spring of 2018. It is likely that the AFD is likely to gather even greater support from new elections. Nonetheless, the CDU will continue to support Merkel at least right now. However, the CDU has been severely weakened by the election and if we do not see new elections until the spring, there is a distinct possibility that Merkel’s support even within the CDU could collapse if they see the AfD will win even greater support.

The head of the Federation of German Industries (BDI), Dieter Kempf, has chastised the political leaders calling on the SPD, FDP and Greens to form a coalition. The price that the SPD will demand is that Merkel leaves before they would consider any compromise. There is just bad blood now between the SPD and CDU. Of course, this makes it even more likely we see and even more difficult Brexit. The practical crisis is the fact that Merkel must attend to domestic issues and will not truly have the time or authority to assume a leadership role in Brussels.

This turmoil in German politics is actually shifting the stage to Macron. The uncertainty in Germany may be opening the door for Macron to reform the EU and the Eurozone pushing Germany to second place. The political fortunes for the EU may be far more uncertain than many suspects.

From a market perspective, political uncertainty in Europe still creates uncertainty in markets rather that confidence.

For the third consecutive year now, I’ve made the trans-continental trek to Martin Armstrong’s World Economic Conference, and each gathering provides new learning on deeper levels. This year’s conference exceeded my expectations for unexpected reasons.

For the third consecutive year now, I’ve made the trans-continental trek to Martin Armstrong’s World Economic Conference, and each gathering provides new learning on deeper levels. This year’s conference exceeded my expectations for unexpected reasons.

The session content was (in my opinion) deeper and richer and more relevant than the previous two conferences that I had attended…by a longshot. Marty’s instructional sessions were the best I’ve personally witnessed; he was the most focused and calm I’ve seen him, with a real clarity of vision and perspective. I couldn’t do justice to the content even it were mine to share, so I won’t attempt to cover it here, with one exception below. When it becomes available, I recommend buying the video of WEC 2017.

This year’s WEC in Orlando was several levels better in terms of organization, structure and flow. Marty was the keynote speaker that everyone came to see and hear, of course, but there was an expansion of role players who really added depth and texture to both days’ sessions. Mike Campbell tied it all together and kept everything flowing very elegantly by interviewing Marty and moderating a panel discussion. Overall, the sessions were tight and rich.

Over the last couple years, Marty Sr. has gradually added key team players to their organization. Princeton Economics’ CEO Ashley Warren shared more of their corporate vision; Erwin Pletsch shared his insights on interpreting and trading with the Socrates model, and a fine middle-aged fellow (whose name escapes me at this moment) told the story of how he connected with the Armstrong team. He has spearheaded the modernization of the computer source code that Marty risked his life to preserve. Marty Jr. has come into the corporate family…and he seems to complete the executive team.

At every conference there are usually a few bombastic idiots, and the larger the group, usually the higher the number. At this year’s event, I only noticed one such huckster who prognosticated at full volume in the foyer…straight out of a Barnum & Bailey circus movie. He was the exception that proved the rule. Some of the most intelligent and genuine people I’ve ever met are those I’ve met for the first time (or 10th time) at Marty’s conferences. He attracts my favorite kind of people, i.e. kind people. Thanks M and D.

One small piece of Marty’s conference material I feel comfortable sharing is how he emphasized the need to survive our own trading and investment decisions over the next decade. Even with an accurate sense of the big picture, and an uncannily accurate system like Socrates, it’s quite easy to make destructive investment decisions. Time, training & temperament; but the greatest of these is temperament.

The 2016 WEC confirmed for me that we are on the right track in respect of our quest to launch a pooled fund using the Socrates system as the primary information source. In the last year we’ve connected with and engaged experienced young trading specialists who have immersed themselves in the Socrates program, and created a beta-test account which has produced very favorable results. Most importantly, we’ve formed a cohesive team of grounded people – people who genuinely like and care about each other’s well -being, in addition to having complementary skills. We connected with the right people in Orlando, and have followed through on submitting our request. Now we wait.

And while we wait, we continue offering ideas and services that actually help people, like this 30 minute webinar called “The Super RRSP for Private Corporation Shareholders.” Click here for free access…

http://integratedwealthmanagement.ca/super-rrsp-private-corporation-shareholders-archived/

Cheers,

Andrew H. Ruhland, CFP, CIM

Elliott Wave International recently put together a chart (click here or on the chart to watch the accompanying video) that illustrates a recurring theme of financial bubbles: When good times have gone on for a sufficiently long time, people forget that it can be any other way and start behaving as if they’re bulletproof. They stop saving, for instance, because they’ll always have their job and their stocks will always go up.

Then comes the inevitable bust.

On the following chart, this delusion and its aftermath are represented by the gap between consumer confidence (our sense of how good the next year is likely to be) and the saving rate (the portion of each paycheck we keep for a rainy day). The bigger the gap the less realistic we are and the more likely to pay dearly for our hubris.

Where are we today? Worse than in 2006 and nearly as bad as 1999. Both of those years were followed by several really bad ones.

QUESTION: Mr. Armstrong; Thank you for an excellent conference. I have been attending since 2011. Each time you deliver a different conference and they are always better than the last. I could not help to notice on Zero Hedge they ran a piece about a Harvard University’s visiting scholar at the Bank of England who claims:

“We trace the use of the dominant risk-free asset over time, starting with sovereign rates in the Italian city states in the 14th and 15th centuries, later switching to long-term rates in Spain, followed by the Province of Holland, since 1703 the UK, subsequently Germany, and finally the US.”

Besides claiming to calculate the 700-year average real rate at 4.78% suggesting that rates will rise sharply when your models are 5,000 years, the two ridiculous statements are a 700-year average as if this really means something in the near-term when rates have been below that for nearly 10 years, and second the statement that he traces “the dominant risk-free asset over time.” You have demonstrated that moving averages are not valid in forecasting and that government routinely defaults.

You forecast at the conference that rates would rise very rapidly as we move into the Monetary Crisis Cycle. When I returned home to Greece, the latest news here is that so many people do not even have the money left to pay taxes. Is this part of the first stone in the water that sets off the waves of the Monetary Crisis Cycle?

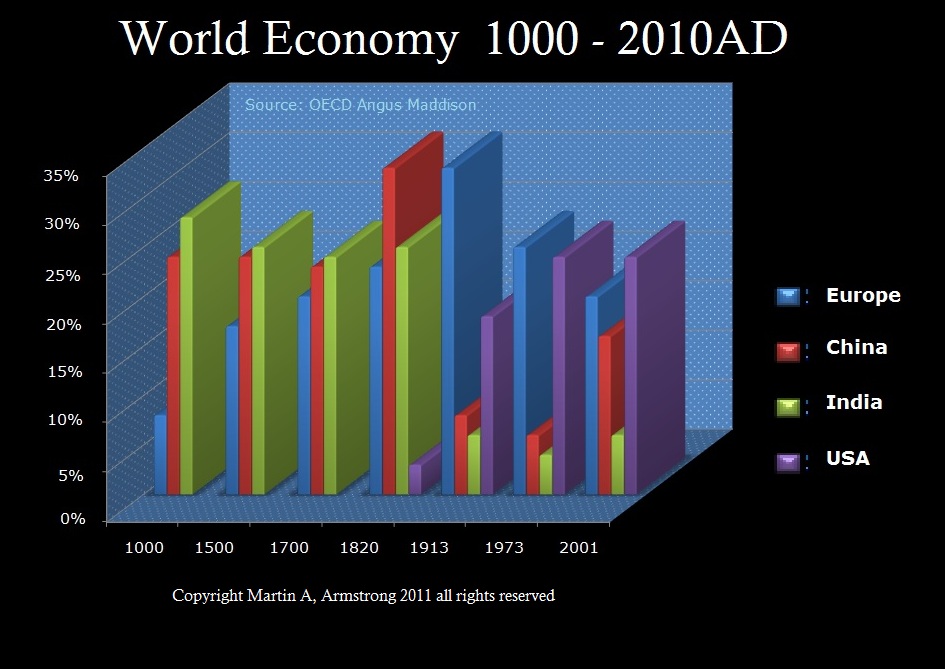

ANSWER: It is very nice to trace 700 years and come up with the average of 4.78% by switching to the dominant economy as the financial capital of the world moved. However, starting the study in the 14th century skips the crazy part. There was the Great Financial Crisis of 1092 in Byzantium. This was really a watermark event that set in motion the decline thereafter. This study of moving from Spain to Holland, UK, Germany, and then the USA, is interesting, but regionally biased.

The fall of Byzantium resulting in the financial capital of the world moving to India – not Spain. That is why Columbus set sail trying to get to India, which was the financial capital of the world after Byzantium.

We hit a 5,000 year low. The Reversals we provided at the conference show we are looking at a near doubling in rates when we cross that number.

….also from Martin:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair