Asset protection

Ludwig von Mises and Friedrich Hayek, the most prominent “Austrian” economists of the time, anticipated the 1929 stock market crash and correctly predicted the dire consequences of government attempts to artificially stimulate economic growth in the aftermath of the crash. John Maynard Keynes, on the other hand, was totally blindsided by the stock market crash and the economic disaster of the early 1930s. And yet, Keynes’s theories gained enormous popularity during the 1930s whereas the work of Mises and Hayek was largely ignored. Why was it so?

Ludwig von Mises and Friedrich Hayek, the most prominent “Austrian” economists of the time, anticipated the 1929 stock market crash and correctly predicted the dire consequences of government attempts to artificially stimulate economic growth in the aftermath of the crash. John Maynard Keynes, on the other hand, was totally blindsided by the stock market crash and the economic disaster of the early 1930s. And yet, Keynes’s theories gained enormous popularity during the 1930s whereas the work of Mises and Hayek was largely ignored. Why was it so?

Keynes became popular because he told the politically powerful what they wanted to hear. In particular, he provided power-hungry politicians with intellectual support for the schemes they not only already had in mind, but in many cases were already putting into practice. Despite being riddled with errors, Keynes’ theories also appealed to many economists because the implementation of these theories would confer a lot more influence upon the economics fraternity. The fact is that in a free economy there wouldn’t be much for an economist to do other than teach economics. He/she would certainly never have the opportunity to be involved in the ‘management’ of the economy.

The points outlined in the above paragraph, along with Keynes’ charisma and salesmanship, explain why “Keynesian” economic theories became dominant, but it doesn’t explain how they managed to stay dominant in the face of an ever-growing mountain of evidence indicating that they result in long-term economic decline.

As far as I can tell, the theories have stayed popular for three main reasons. First, not only do they mesh with the personal goals of almost all current politicians, but also there is now a huge government apparatus in place that depends upon the continued application of these theories. In other words, a large chunk of the population now has a vested interest in perpetuating the myth that the government should ‘manage’ the economy. Second, it usually isn’t possible to disprove an economic theory using data, because the same data can usually be interpreted in different ways and used to justify opposing theories. The hard reality is that in the science of economics you must start with the correct theory in order to correctly interpret the data. Third, Keynesianism is more like a stream of anecdotes than a coherent theory, in that under this so-called theory most things are ‘explained’ by unforeseeable events and unpredictable shifts in “animal spirits”. It is impossible to invalidate an intellectual position that is constantly changing.

A good example of how the same data can be interpreted in different ways in order to support conflicting theories is provided by the 1937-1939 collapse of the US economy. According to the “Austrians”, the fact that the US federal government propped up prices, drastically increased its spending, inflated the money supply, began interfering with many industries and generally did whatever it could to prevent the corrective process from running its course following the 1929 stock market crash guaranteed that all signs of economic recovery would quickly disappear as soon as the artificial support was scaled back. The mistake, according to the “Austrians”, was to provide the artificial support. According to the “Keynesians”, however, the mistake was to remove the artificial support prematurely. They argue that the government and the Fed should have continued to do whatever was needed to postpone a collapse, the idea being that with enough government assistance in the form of new money, new regulations, handouts, price controls and job-creating public works projects the economy would eventually gain enough strength to become self-supporting.

Unfortunately, when throwing ‘Keynesian stimulus’ in the form of more government spending, more credit and more monetary inflation at an economic downturn doesn’t lead to a self-sustaining recovery, the followers of Keynes will always have two comebacks. They can always assert that the stimulus would have worked if only it had been done more aggressively and/or that as bad as the economy has performed it would have performed even worse if not for the stimulus.

You can’t argue with that. At least, it’s an assertion that can never be unequivocally invalidated because it is never possible to go back in time and show what would have happened with different policies.

We know much is currently wrong with our financial world, as discussed in the James Rickards book “The Road to Ruin” and elsewhere.

- The official U.S. government debt is nearly $20 trillion. Unfunded liabilities are 5 – 10 times larger. Debt has doubled every 8 – 9 years for decades – since the Federal Reserve was put in charge of devaluing the dollar. Debt will continue to grow, obviously out of control.

- Millions of Americans are out of work, regardless of the official statistics.

- Prices increase, some rapidly, regardless of the official statistics on consumer price inflation.

- More government spending and debt are looming on the horizon. New and escalating wars are likely. Expect more deficits, debt, and inflation.

- The U.S. stock market is selling at all-time highs, levitated by “easy money” and unsupported by fundamentals or breadth.

Option A:

Trust the professionals who manage our digital and paper wealth which is backed only by debt, promises, fantasy, and confidence in the Federal Reserve and government. Believe official statistics and mainstream media that tell us things are peachy and not to worry.

Option B:

Use gold and silver bullion (not the paper stuff) as financial insurance to protect the buying power of some or most of our net worth. Based on a century of experience, we can depend upon central banks and global governments to devalue currencies, create more debt, and propel gold and silver prices far higher.

Really? Those options seem extreme. Why? Read on!

STOCK MARKETS:

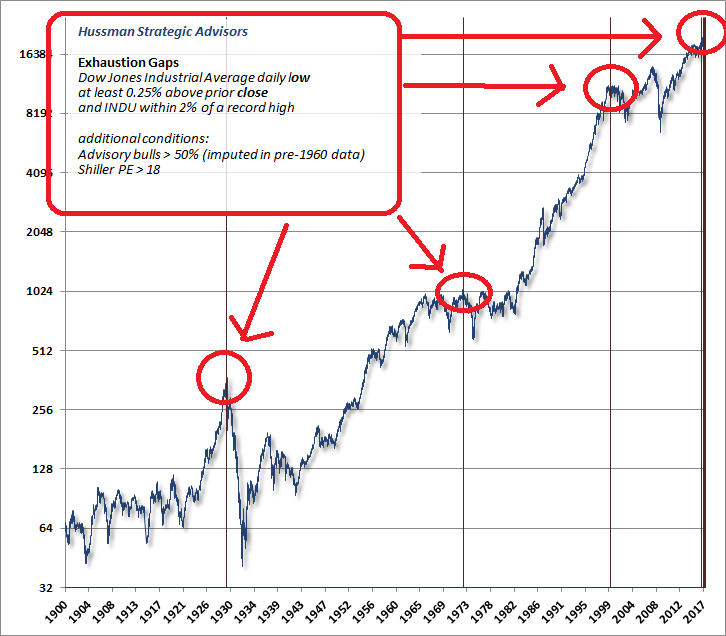

Consider John P. Hussman’s Exhaustion Gaps and the Fear of Missing Out.

Read David Stockman: Market Crash to Occur

“Our country needs a good shutdown in September to fix mess!”

“There will be no bid for the stock once the panic sets in.”

BUBBLES:

Mike Maloney created an easily understood video which is 35 minutes long and explains the “everything bubble.” Watch it! Stocks, bonds, real estate and more are discussed.

Bill Holter discusses “The End of the Empire.” (31 minutes) Watch it!

PENSION PLANS:

Constantin Gurdgiev discusses “U.S. Public Pensions System:

“Or, put more cogently, the entire system is insolvent.”

“… in … California, New Jersey, Illinois, etc. we are already facing draconian levels of taxation, and falling real incomes of private sector workers.”

“In other words, there is not a snowball’s chance in hell these gaps can be funded from general taxation in the future.”

GOLD AND SILVER:

Read Steve Warrenfeltz: Silver and Gold Pop!

Lior Gantz interviewed Gary Christenson (author) on his book “Buy Gold Save Gold! The $10 K Logic.” This youtube interview (62 minutes) discusses historical gold prices, on-going dollar devaluations, consumer price inflation, gold prices rising to $10,000 as the dollar is devalued, silver, and much more.

CONCLUSIONS:

- It is possible we will enjoy a century of global peace, return to honest money, eliminate the overhanging debt, balance the budget, and – insert your favorite fantasy here!

- Otherwise, bet on Option B – buy gold and silver bullion and store it outside the banking system. Prices will rise substantially as all fiat currencies are devalued further.

Gary Christenson

The Deviant Investor

I discuss the ongoing devaluation of the dollar in my book: Buy Gold Save Gold! The $10 K Logic.” It is available at Amazon, or at gechristenson.com in paper and pdf for non-US readers.

Last week, when looking at the the distortion and absurdity unleashed by the ECB’s asset purchase program upon European capital markets, we showed the unprecedented collapse in European junk bond yields as captured by the effective yield of the BofA/ML Euro High Yield Index, which is now trading just shy of all time lows, having dropped below 3% at the end of April, and printed at 2.79% on May 23, within bps of record lows…

… roughly 50 bps wider than where the the US 10Y is trading at this moment, and inside the 30Y US Treasury. Assuming a 1.9% European CPI (as of April), this means that the real rate of return on Europe’s junk yields is now 0.89%. But we digress.

When Nassim Nicholas Taleb looks at President Donald Trump, he doesn’t see “a trainwreck.” The real trainwreck, according to the trader turned author, is “unfettered globalization.” That’s the real danger that members of “the resistance” should be worried about, Taleb says during an interview with Bloomberg.

…for more written commentary go HERE or click image below:

…also from zerohedge:

Marc Faber sees the risk of an Economic collapse and financial crisis rising and it could occur at any moment. Getting informed about a collapse and crisis may earn you a lot, or at least prevent you from losing money. Interview May 15th/2017

….also from Marc: Marc Faber: The Markets to Crash within 12 Months

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair