Asset protection

An investment timing genius with an amazing stock track record is returning to the Weiss Research team of experts!

His name is Tony Sagami, and with the market still climbing a wall of worry, the timing couldn’t be better.

I first met Tony in the 1990s, and we’ve been very good friends ever since. Here’s a transcript of our latest conversation …

Martin Weiss: Welcome back, Tony! I suspect many of the people reading this already know who you are; we started working together so many years ago …

Tony Sagami: More than 20, actually! When we both had black hair and black beards.

Martin: Haha. That’s what you remember. What I remember best is the day the Nasdaq Composite Index was trading below 1,000, you told me it could double or triple from there, and I said you were nuts.

Tony: I was nuts, I agree. But the Nasdaq was nuttier. It didn’t double. It didn’t triple. It surged by over five times — to 5,132. And by that time, I was turning so bearish I couldn’t see straight.

Martin: You told our subscribers to dump all their tech stocks. Every single one. That was gutsy. But then you took it one step further. You told them to buy put options on the Nasdaq index to directly profit from the decline. So while nearly all other investors were losing their shirts in the biggest tech stock disaster of all time, our subscribers were making some of the biggest profits of all time. It was one of the boldest and most accurate market calls I’ve seen in my life.

Of course, it’s easy today to look back and say the signs of the dot-com bubble were obvious. But for the thousands of so-called “pros” caught up in the frenzy, it wasn’t so obvious, was it?

Tony: No. But it was crystal clear to us in early 2000. The Wall Street crowd, the mainstream media, individual investors. They all had collectively lost their minds. They had driven stock prices — including pieces of pie-in-the-sky companies with scant sales and no profits — to ridiculously high prices. The risk hugely outweighed the reward. It wasn’t a sandbox I was willing to play in anymore.

Martin: You nailed it that time. Then you did it again. After riding the market up from 2003, you took your profits and ran, avoiding the excruciating pain of the worst Debt Crisis of modern times.

Tony: Thanks, but investors don’t need a history lesson right now. What they need now is solid, reasoned, no-nonsense direction for the future, which is what I’m here for.

Martin: A perfect segue to my main question: Is the stock market now poised for another tumble?

Tony: A tumble? Yes. A crash like the dot-com bust or the Debt Crisis? No. Sure, this current bull market is getting old in the tooth. Through last Thursday, the S&P 500 went 102 straight days without a 1% downward move. Just since Trump’s election, the S&P 500 has added $3 trillion of market value.

And sure, that type of enthusiasm is unsustainable. But unlike in 2000, the stock market is NOT grossly overvalued. It’s at 18.4 times forward earnings. That’s not cheap by any means, but we’re not talking about nosebleed territory either.

Here’s the key. This is a very timely conversation because I’m starting to see some cracks in the stock market’s armor.

Martin: What cracks?

Tony: Here are three that worry me.

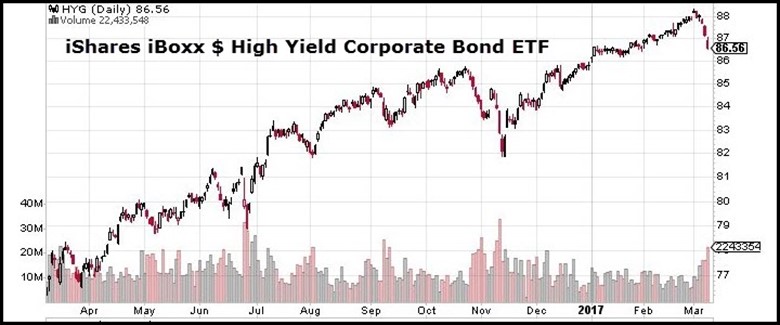

Crack number one is the default rate on sub-prime auto loans. It hit 9.1% in January (the most recent data available). That was the highest level since the Debt Crisis, a first warning sign of consumer distress.

Crack number two is in the junk bond market. Last week’s decline alone was enough to wipe out all the interest investors could have made in the last year. The junk bond market has historically been a reliable risk-on/risk-off indicator. I watch it like a hawk.

Bull markets never die or correct for one reason alone. But one of the most common bear market triggers is an overzealous Federal Reserve. That could be crack number three in the market’s armor.

The Fed is slated to announce three rate hikes in 2017, a scenario that the Wall Street crowd seems oblivious to. Never forget: The Fed can kill a party faster than the police at a high school kegger.

Martin: Are you saying it’s time to run for the hills?

Tony: Not at all, Martin. What I am saying is that you need a plan — a defensive strategy to protect yourself for the day when the rally runs out of steam. It was your father who told me “buy, hold, and pray is not a strategy.”

Martin: What strategy do you recommend, then?

Tony: One of the easiest is to monitor the major stock market indices for a drop below a long-term moving average. On the Dow, for example, as long as the index is above its 200-day moving average, hold. As soon as it falls below, start selling.

Martin: Some people might think that’s cliché. But I’ve seen it work. Back in 1987, for example, my father and I saw the Dow fall below its 200-day moving average. It was Thursday, October 15, and that evening, we recorded a hotline alerting our subscribers to an imminent crash. Sure enough, October 19 was Black Monday, the worst single-day crash in Dow history.

Tony: I knew your father well and learned a lot from him. But the key is not to over-anticipate a crash, not to run for the hills too soon, which leads me to another defensive strategy.

This strategy recognizes that bull markets can greatly exceed valuations, that the Trump rally could last even longer, and it still has the potential to make investors richer than they’re inclined to think.

You have the best example right here and now: Anybody sitting on the sidelines since the election missed out on a mountain of profits.

This strategy also recognizes the explosion in Exchange Traded Funds (ETFs). There are hundreds of low-cost, effective ways to profit from falling stock and bond prices.

Martin:And you’ve been very successful at making money from ETFs, on the upside and the downside. Why?

Tony: Because after predicting markets for as long as I have, I find that the strong bullish and bearish trends are easier to identify than ever.

Martin: How so?

Tony: When you and I first entered the investment business, the focus was on corporate profits. All the big Wall Street firms had dozens of accountants and finance majors squirreled away in back rooms, poring over balance sheets, financial statements, annual reports. Good old fundamental analysis. But it was hard to make money with it because nearly all the news, whether good or bad, was almost invariably old news.

Martin: Are you saying corporate profits don’t matter anymore?

Tony: No. They still matter, but the focus has shifted to economic and political news as the main drivers of asset prices.

Let me give you two current examples:

Whenever the Federal Reserve releases a policy statement or Janet Yellen gives a speech, the numbskulls on Wall Street pore over every word, every syllable that comes out of her mouth. Heck, a degree in linguistics may be more valuable than a degree in finance these days.

Whenever the Federal Reserve releases a policy statement or Janet Yellen gives a speech, the numbskulls on Wall Street pore over every word, every syllable that comes out of her mouth. Heck, a degree in linguistics may be more valuable than a degree in finance these days.

Meanwhile, the real action is what I call “Revenge of the Nerds II.”

I’m talking about high-frequency trading based on computerized models. They’re dominating the stock markets. They’re used by large investment banks, hedge funds, and institutional investors. They’re using computers to transact a massive number of orders at extremely high speeds. And all this is totally unrelated to the fundamentals of a company.

Martin: So what else is new?

Tony: What’s new is that now more than 70% of equity trading is done by high-frequency traders. And as I said, what’s even newer is that the factors driving some of the biggest momentum in the market (which their computers pick up on) are often major geo-political events. Like Brexit. Like the Trump election. And most important, like the Great Money Tsunami that Larry talked about.

Martin: I’m glad you brought up the Revenge of the Nerds. Because I remember that you were one of the first “nerds” to apply computerized trading to mutual fund and ETF investing.

Tony: I did. Back in the 1990s, I pioneered the use of complex computerized algorithms to analyze markets. I created software that helped thousands of sophisticated individuals and investment advisers.

Martin: You called it “computerized investing,” and you were one of the early pioneers. But the big question now is, how do you combine everything into a single, integrated investment strategy that’s exactly right for this time frame?

Tony: First, I determine what news events — both political and economic — really drive the markets. For example, Federal Reserve releases have more impact than Durable Goods orders. So I have figured out the 10 key economic/political events that affect stock market prices the most.

Second, I have created a rating system that quantifies the strength of any current trend. I call that the “Trend Persistency” rating.

Third, I buy into trends with the highest bullish trend persistency rating, and I sell into trends with the highest bearish persistency rating. Or, when there’s no strong signal either way, I sit on the sidelines. That way I take full advantage of the high-frequency trading crowd.

The profit opportunities are as regular as clockwork because the scheduled release dates of the 10 key economic/political events that drive the markets are known months in advance. You know exactly when they’re going to come out.

For example, I know that the next Dallas Federal Reserve Manufacturing Index numbers will be released on March 27, 2017. I know that the index has shown a consistent renewed strength over the last four months. (See chart above.) I know it’s one of the top ten events that will drive markets. And I know how it ranks in pure firepower compared to the other nine.

It’s a market-moving event with a strong trend persistency… and a strong opportunity to make money.

We call this kind of trading calendar profits, and it works. Of course, nothing is guaranteed in this crazy world. But never underestimate the power of the calendar to time the market, especially when you use the trading tools I just told you about.

Martin: Thanks, Tony. We look forward to hearing a lot more about this.

“A fanatic is a man that does what he thinks the Lord would do if He knew the facts of the case.” ~ Finley Peter Dunne

Not too long ago this bull market was one of the most hated in history; that no longer appears to be the case. Throughout the unpopular phase of this bull market, we consistently and much to the dismay of many penguins, oops we mean experts, stated that every pullback should have been treated as a buying opportunity. There were two reasons for this; market sentiment was consistently negative, and the trend was up.

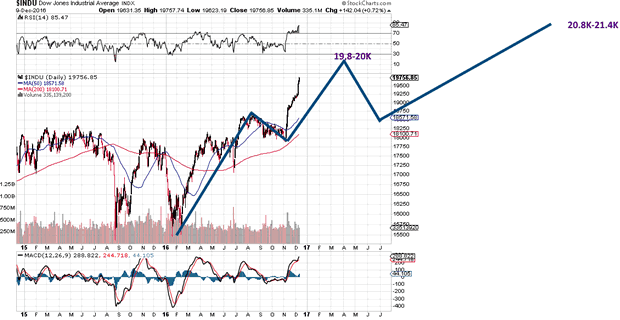

We even penned an article before Trump won stating that a Trump win like Brexit would prove to be a buying opportunity. As expected after the initial panic of having to deal with A Trump Presidency, the markets recouped their losses and never looked back. We were so bullish that on De 15, 2016 we provided our subscribers with the Path we expected the Dow to take in 2017.

To be fair, we expected the markets to let out some steam as indicated the chart above, but the Dow only hesitated at 20,000 for a bit before surging like a rocket. Many experts were predicting the end of this bull at that time, some of which had for the most part been on the right side of the market. A stock market crash is not something we were ready for, and we voiced this sentiment in several articles in late 2016 and in Jan and Feb of this year. We were waiting for a pullback as the sentiment at the time (Dec 2016) had turned quite bullish. Long story short our targets have been hit and they have been hit a lot faster than we expected. One would almost be tempted to state that we are in the feeding frenzy stage which usually represents the last stage of a Bull Market. However, the Crowd is not Euphoric, so this would rule that option out at least for now. So what’s going on? Well, it appears to be fanaticism or madness. The markets are operating out of the realm of reality.

Fanaticism is a different emotion from Euphoria; it is a form of madness, and it is hard to analyse an insane person as there is no discernible pattern; at least not immediately. History is not replete with such situations, so we need to spot these new patterns in real time. This emotion does not expire as fast as Euphoria or Fear; it can be maintained for a prolonged period. Thus, when one encounters it, the safest play is to take a defensive position. Assume the outlook is worse than it is, but without letting the panic factor seep into the equation.

The data is twisted; on the one hand, the sentiment is far from Bullish, but on the other hand, more money is flowing into the markets, and our indicators are now in the extremely overbought ranges on the long term weekly and monthly charts. Just because the outlook is different does not mean we need to start becoming anxious. Panic is not something we favour or look kindly at; panic is a useless emotion. One has to be prudent when it comes to the markets, and we have been right on the money regarding this bull market for a long time. We do not want to let arrogance take over; common sense which we value highly dictates that caution, and not fear is warranted. Thus, prudent traders would do well to tighten their stops and if committing new funds, look for companies that are selling at a huge discount or trading in the extremely oversold ranges. If the markets pull back suddenly your risk will be limited.

This market will pullback, however, no one call tell it when to pull back especially when the primary emotion driving this market is fanaticism. It is relatively easy to determine a market’s trajectory if the emotion is Euphoria or Fear, but Fanaticism is something different. As stated it is a form of madness and insanity is not easy to spot, especially if it is in stealth mode.

We are not going to pen another thousand words telling you why this Stock Market should crash or soar or anything like that. The bottom line is the market does not care about what if scenarios? What if scenarios are for people that have too much time on  their hands to talk about useless concepts that most likely will not come to pass? Let’s deal with reality

their hands to talk about useless concepts that most likely will not come to pass? Let’s deal with reality

Let’s first take a look at the data

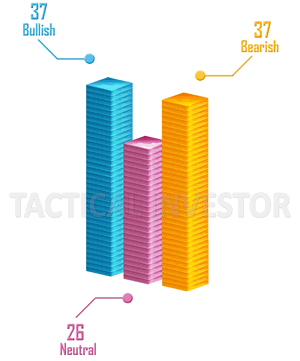

Polarisation is spreading or contaminating the Bullish and Bearish Camps. It has been a long time since we have the sentiment so evenly divided between the two camps. This week exactly 37% are bullish, and exactly 37% are bearish, with 26% falling in the neutral camp. One would normally expect the bullish sentiment to soar through the roof; euphoria is clearly not gripping the market, and neither is panic. When we combine the bears with the individuals from the neutral camp, we arrive at a figure of 63%. The masses appear to be uneasy; the key word is “appear” for insanity is operating in stealth mode for now.

We spotted traces of fanaticism late last year, and that is why we briefly addressed this topic in late Dec of 2016 and early January. The trend is gathering in intensity, and it could be with us or for some time. If this trend picks up, then this bull market could last longer than the most ardent of bulls ever envisioned, but there will be at least one correction that will break the backs of almost all the bulls and make the bears believe that a new bear market has started. Sadly, both of these chaps will be wrong. A stock market crash, a bear market, etc, all come down to perception as is the case with the truth or a lie. Alter the angle of observance and the perception changes; it all depends on when you got into the market or out of it.

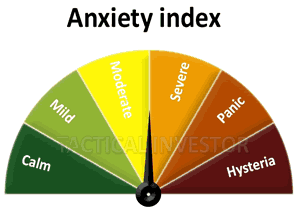

Our proprietary anxiety index is also getting infected with the polarisation flu; it is sitting right at the 50% mark. These are all subtle clues that something new is taking place in the background. Trend investing comes down to identifying the primary trend; it does not mean that the market cannot and will not pull back while it is an uptrend. In the long run the market tends to revert to the mean; currently, the market is trading almost two standard deviations from the mean. Thus regardless of the trend, one of the two things needs to happen

Our proprietary anxiety index is also getting infected with the polarisation flu; it is sitting right at the 50% mark. These are all subtle clues that something new is taking place in the background. Trend investing comes down to identifying the primary trend; it does not mean that the market cannot and will not pull back while it is an uptrend. In the long run the market tends to revert to the mean; currently, the market is trading almost two standard deviations from the mean. Thus regardless of the trend, one of the two things needs to happen

-

Our indicators pullback into the oversold ranges, preferably the extremely oversold ranges. Currently, they are trading in the extremely overbought ranges on the weekly charts and overbought ranges on the monthly charts

-

A sharp correction that drives many bulls to join hands with the Bears. A long-term bull market has to experience one back breaking correction. We do not know when this will occur, but the sooner, the better as, the higher it trades, the more painful the correction will be especially for those that embraced this bull market very late in the cycle

Ideally, both of the above occur simultaneously, and at that point, one could start conjuring images of Dow 24K. To do this, the above two need to occur simultaneously.

Shockingly V readings have surged a whopping 100 points in just two days. In just one week they have moved 160 points; a new three-day record and a new record. What can we say, expect what will appear to be chaos regarding human emotions, weather, politics and market movements? However, remember there is no such thing as true chaos as chaos has a pattern. Thus embrace this development for we are trend players and not chickens that squawk the moment we smell change. For the umpteenth, we are going to raise all the overbought and extreme ranges as V readings show no sign of letting up. If you look at the reading going back to Dec 16, 2009, you can see how insanely high this indicator is trading. Note that when we launched this indicator, readings were in the 300 ranges. This further cements the argument that the central driving theme in the world (and not just the U.S) is going to be to “polarise the masses”. Do not become part of the crowd for they are going to go insane and lose a lot in the process; you, on the other hand, could stand to benefit tremendously provided you do not lose control. ~ Market Update Feb 20, 2017

The crowd has gone insane at least when it come to the markets. Remember, that the mass mindset does not refer to just the small players. Hedge fund managers and even big players are all part of the mass mentality. Look at Bill Ackman, he finally conceded defeat and sold his position in Valiant Pharmaceuticals at what could very well turn out to be the bottom. Would it not have made sense to sell it earlier, why now, when the stock is trading close to the levels it was trading in 2005 well before it took off?; a classic example of the mass mindset in action; buying when you should have been selling and selling when buying probably makes more sense.

Individuals falsely assume that big hedge funds or mutual funds cannot be part of the mass mindset. Some of the biggest players are nothing but cattle, they just give the impression that they know what they are doing, but in the end, they are just following each other to the Promised Land, which usually turns out to be den full of vipers. Insanity (madness) is a very powerful force; never underestimate it.

Conclusion

As insanity is the main driving force, caution is called for, and we are going to change our tactics. At this point, the Markets are trading in the extremely overbought ranges on both the weekly and monthly charts. We are not stating that the markets are going to crash or that they need to crash. What we are stating is that common sense says that an old bull market such as this one needs to let out a healthy dose of steam. At this point, the risk to reward ratio is not strongly in our favour. We still view substantial pullbacks as buying opportunities unless the trend changes, but the pullback would have to sharp in nature.

“A fanatic is one who can’t change his mind and won’t change the subject.” ~ Winston Churchill

With all the oil-related headlines we’re exposed to each day, you might assume that “black gold,” along with other fossil fuels like coal and natural gas, matter to humanity’s future. You’d be wrong. Like Keynesian economics and fiat currencies, fossil fuels are near the end of their run. From here on out, solar is the story.

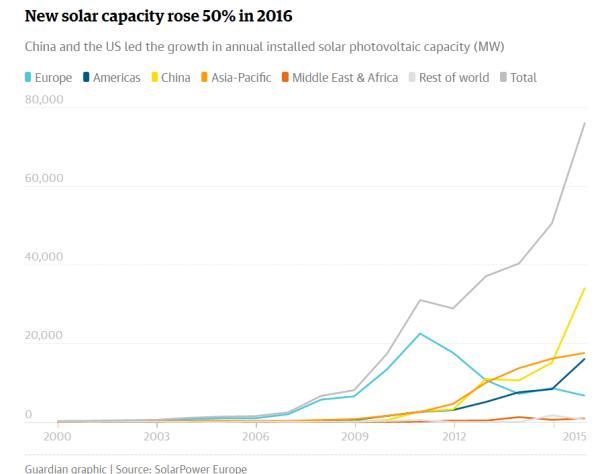

The following chart shows the decline in the cost of solar power and the resulting surge in solar installations through 2015. The relationship is clear: as prices plunge demand surges — in both cases exponentially.

Pretty impressive, right? But nothing compared to what happened in 2016:

And here’s one more chart showing how China — that insanely polluted coal burning urban dystopia — is leading the way on solar:

This is shocking to people who A) are dependent on fossil fuels through work or investing or B) don’t understand the way exponential growth can change a market in an eye blink. So let’s hear from the father of exponential analysis, Google’s director of engineering Ray Kurzweil:

Ray Kurzweil: Here’s Why Solar Will Dominate Energy Within 12 Years

(Fortune) – Ray Kurzweil has made a bold prediction about the future of solar energy, saying in remarks at a recent medical technology conference that it could become the dominant force in energy production in a little over a decade. That may be tough to swallow, given that solar currently only supplies around 2% of global energy — but Kurzweil’s predictions have been overwhelmingly correct over the last two decades, so he’s worth listening to.

Kurzweil’s basic point, as reported by Solar Power World, was that while solar is still tiny, it has begun to reliably double its market share every two years — today’s 2% share is up from just 0.5% in 2012.

Many analysts extend growth linearly from that sort of pattern, concluding that we’ll see 0.5% annual growth in solar for the foreseeable future, reaching just 12% solar share in 20 years. But linear analysis ignores what Kurzweil calls the Law of Accelerating Returns — that as new technologies get smaller and cheaper, their growth becomes exponential.

So instead of looking at year over year growth in percentage terms, Kurzweil says we should look at the rate of growth—the fact that solar market share is doubling every two years. If the current 2% share doubles every two years, solar should have a 100% share of the market in 12 years.

Okay, technically, that would suggest solar would have a 128% share of the market in 12 years. Some might love that — but it highlights the fact that Kurzweil’s prediction is only partially grounded in the real world. Even 100% share is extremely unlikely — fossil fuel giants are definitely not going down without a fight.

But even those giants ignore Kurzweil at their own peril. He predicted the mobile Internet, cloud computing, and wearable tech nearly 20 years ago — all on the basis of the same principle of accelerating returns that’s behind his solar call.

If this sounds outrageously aggressive, consider what happened to Kodak, the dominant player in film photography for most of the 20th century. Early digital cameras were expensive and complicated and therefore not an obvious threat. But their prices plunged and film photography died. Here’s that process translated into Kodak’s share price:

Also recall that Nokia was once the dominant maker of cell phones. Then Apple introduced the iphone and phones that just made calls were pushed off the stage.

This fate awaits most of today’s fossil fuel companies. The only question is when the death spiral begins.

Why is something like this appearing on a gloom-and-doom blog? Because one of the basic tenets of sound-money investing is that during periods in which society is destroying its fiat currencies, real assets will tend to outperform financial assets. So swap your government bonds (and certainly your bank stocks!) for farmland, well-chosen rental houses, gold, silver, and energy assets.

For the past century that last category was dominated by oil wells, coal mines and the stocks of the companies that owned them. But if the above trends continue – and it’s a near certainty that they will, given the torrent of advances in solar panels and batteries pouring out of labs around the world – then “energy assets” of the future will likely be solar and wind farms, advanced battery makers and the like. So the thesis remains the same while technology causes the names to change.

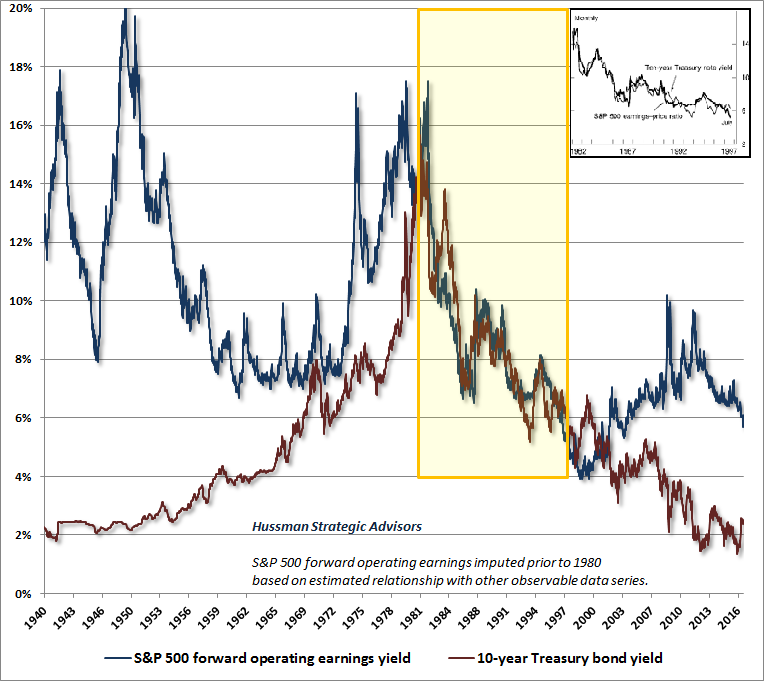

On Wednesday, the consensus of the most reliable equity market valuation measures we identify (those most tightly correlated with actual subsequent S&P 500 total returns in market cycles across history) advanced within 5% of the extreme registered in March 2000. Recall that following that peak, the S&P 500 did indeed lose half of its value, the Nasdaq Composite lost 80% of its value, and the tech-heavy Nasdaq 100 Index lost an oddly precise 83% of its value. With historically reliable valuation measures beyond those of 1929 and lesser peaks, capitalization-weighted measures are essentially tied with the most offensive levels in history. Meanwhile, the valuation of the median component of the S&P 500 is already far beyond the median valuations observed at the peaks of 2000, 2007 and prior market cycles, while our estimate for 10-12 year returns on a conventional 60/30/10 mix of stocks, bonds, and T-bills fell to a record low last week, making this the most broadly overvalued moment in market history.

Donald Trump’s election and subsequent comportment stirred emotions and provided entertainment.

Donald Trump’s election and subsequent comportment stirred emotions and provided entertainment.

But the critical question was always simple: does this administration represent a break with the pattern of the last 40 years… or a continuation of it?

All Too Human

Reagan, Bush, Clinton, Bush II, Obama – all of them have taken our political economy in essentially the same direction. More debt. More Deep State control. More consolidation of power in the executive branch (including the military).

A new president always has some influence. Typically, he can rearrange the furniture and hand out some choice sinecures.

But not since John F. Kennedy has any president dared to change the direction the government is going or challenge the real power of those who run it.

And today, it would take an almost superhuman leader to do so.

Mr. Trump sounded, at times, as if he posed a threat to the elite. Liberals acted as though he were a devilish scourge sent by evil gods.

Conservatives allowed themselves to believe he was the long-awaited messiah.

And now we see that “The Donald” – for all his late-night tweets and bull-in-a-china-shop bluster – is all too human, prone to sin and error… just like the rest of us.

Most likely, the important trends of the last four decades will intensify as the insiders use the chaos and distraction of the Trump team as cover to take even more power and wealth from the American people.

In short, our guess is that there will be plenty of little surprises coming from this administration, but no big ones.

President Trump has already proposed to shuffle more cash to the generals and to the jailers. Soon, we will see more money grabs… from the insiders in finance.

No Correction

Among the coming non-surprises will be the feds’ reaction to a crash on Wall Street… or a recession on Main Street.

Here’s a shorthand for how it will probably go down: crash and/or recession = QE4, direct asset purchasing by Fed, and helicopter money = more wealth for the cronies.

The U.S. economic expansion – albeit weak by historic standards – has gone on for 93 months. That makes it the third longest in history.

If it goes on another 27 months, it will set a new record: the longest expansion on record uninterrupted by a recession.

Although that sounds like an achievement, it is like setting a new record for eating jalapeno peppers: you know you’re going to be sick soon.

Economies make mistakes; corrections clean them up. Typically, the interest rate serves as a “hurdle.” If your project can’t produce enough money to pay for the cost of the capital that went into it, it gets eliminated.

But if you reduce the cost of capital to almost nothing by way of ultra-low interest rates, you never have to reckon with your mistakes. Today, the hurdle is so low, you can’t even trip over it.

The errors stay in place – misallocating more precious savings and consuming more real wealth.

Irrelevant Rate Hike

Meanwhile, the stock market is at record levels.

On a CAPE ratio basis – which looks at stock prices relative to the average of the last 10 years of earnings – only three times since 1929 has the S&P 500 been so pricey, all of them in the last 18 years: first in 1999, then in 2007, and again now.

And like the business expansion, this bull market must contain trillions of dollars of uncorrected errors.

And for the same reason: when capital is almost free, it’s hard for businesses to stumble. They don’t go out of business… They just refinance… merge… acquire a competitor… and buy more of their own shares.

But wait… CBC News reports:

Federal Reserve chair Janet Yellen gave investors a pretty clear sign on Friday that the U.S. central bank is likely to raise its benchmark interest rate later this month – and more hikes to follow later this year.

In a speech on the central bank’s economic outlook at the Executives’ Club of Chicago on Friday, the Fed chair told the gathered audience that a slight increase to the federal funds rate would be “appropriate” when the bank next meets for a two-day policy meeting on March 14 and 15.

And here we can be clear about what the Fed won’t do…

There will be no big surprise coming from that quarter either: the Fed will only raise rates to the extent that it is irrelevant.

In its meeting, the members of the Fed’s policy setting committee, the FOMC, will vote on whether to raise rates one-quarter of a percentage point.

We don’t know which way that will go. But we know it won’t matter. Because if it did matter, they wouldn’t do it.

That’s really what Ms. Yellen means by “appropriate.” It will only be appropriate if it doesn’t cause or exacerbate a correction; that is, they will only raise rates as long as it doesn’t interfere with the debt bubble.

If the Fed’s “data” appear weak… and even a tiny increase might prick the bubble… there’ll be no rate increase.

In Sync

The deeper meaning of this is that the Fed, Wall Street, the Pentagon, and Team Trump are all in sync.

None wants to upset this apple cart. It would reveal too many rotten pieces of fruit in the pile. All now collude with the media to keep the public distracted and off-balance, while the whole shebang keeps rolling along.

The Trump administration picks unnecessary fights with unimportant adversaries… pretending to be defending the common man. The media is confused… and confuses the public even further.

The Pentagon goes about its business… happily scaring the public in order to transfer money and power to itself and its crony pals.

Wall Street provides the illusion of prosperity… bidding up stock prices as though they were made more valuable by the administration’s dumb-head policies.

And the Fed provides as much fake money as necessary to keep the scam alive.

But the first big test can’t be long in coming. The feds are running up against their debt ceiling.

There again, the sound and fury will sell newspapers. Democrats will fume. Republicans will fret. But it will be essentially meaningless agitprop.

All of the main players are firmly committed to more spending. They won’t let prudent legislation or a $20 trillion deficit stand in their way.

Here’s pseudonymous blogger Tyler Durden at Zero Hedge:

While in recent weeks there has been a material increase in Fed balance sheet normalization chatter, according to a new report from Deutsche Bank analysts, it may all be for nothing for one simple reason: should the U.S. encounter a recession in the next several years, the most likely reaction by the Fed would be another $1 trillion in QE, delaying indefinitely any expectations for a return to a “normal” balance sheet.

No return to “normal.” Not voluntarily. Empires don’t back up. And bubbles don’t prick themselves.

Regards,

Bill

Market Insight

BY CHRIS LOWE, EDITOR AT LARGE, BONNER & PARTNERS

What’s the best-performing global stock market since President Trump’s inauguration?

The answer may surprise you…

Because it’s also the worst-performing global stock market since Trump’s win over Hillary Clinton on Election Day.

The answer to this riddle: Mexico.

Today’s chart is of the iShares MSCI Mexico Capped ETF (EWW). It tracks the performance of a broad range of Mexican stocks.

And as you can see, EWW is down 9% since Election Day – making it the WORST-performing country stock market over this period.

But it’s up 12.5% since Inauguration Day – making it the BEST-performing country stock market over the following period.

Why such a roller-coaster ride?

One explanation is that investors panicked and dumped Mexican stocks based on candidate Trump’s fiery rhetoric on trade south of the border.

They then started to re-evaluate this bearish stance based on what they’ve since learned of President Trump.

Further evidence, as Bill says, that never before has politics been so important for markets.

– Chris Lowe

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair