Asset protection

Leaders faced with unrest, rising demands and dwindling coffers always debauch their currency as the politically expedient “solution.”

Leaders faced with unrest, rising demands and dwindling coffers always debauch their currency as the politically expedient “solution.”

They continue to ramp up big time. This phenomenon is not going away any time soon, not until it crests in 2020 or 2021.

They continue to ramp up big time. This phenomenon is not going away any time soon, not until it crests in 2020 or 2021.

In times of scarcity, the entire social fabric of society can give way.

Lack of trust in banks. In brokers. In local governments. In religion. In institutions. In law. In the police. In any kind of authority. Not your usual suspects, like food and water, or energy. I’m talking about the lack of trust that is now exploding to the surface all over the world.

Just think it all through. Have you ever seen such a swift collapse in trust and confidence in the world?

But of that day and that hour knoweth no man, no, not the angels which are in heaven, neither the Son, but the Father. – Mark 13:32

Again, not much movement in the U.S. stock market.

All eyes were on U.S. politics.

The Ides of March came… and yea, went… with poor Marco Rubio out of the race…

Yes, it was “Goodbye, Rubio Tuesday”… leaving Donald Trump and Hillary Clinton way ahead of the pack in the race to win their parties’ nominations.

Meanwhile, a dear reader wrote in to complain that the Dow was up some 1,500 points since he acted on our gloomy view… and sold out of the market.

But we hold to our opinion: This ship is sinking.

As an investor, you face two kinds of risk: the risk of missing out on gains and the risk of taking losses.

It’s up to you whether you continue to bet on rising U.S. stocks. But our view is you will be glad you got out when you did.

Death Sentence

We all live under a death sentence. Markets… societies… and our very lives must follow an unstoppable pattern.

We breathe in… and then we breathe out. We are born… and every mother’s son ever born from the beginning of time until today is programmed for death. Every ship ever built is destined for the bottom of the sea… or the scrap yard.

Up, down… in, out… expansion, contraction. Hey, don’t blame us! We didn’t invent it. That’s just the way it is. And since that is the way it is: Vive la mort!

We don’t necessarily want it. But since it is inevitable, we will look forward to it, like a pair of new boots yearning for mud.

There are times to go forward… and times to back up. There are times to buy. And there are times to refrain from embracing stocks.

This is one of those times.

The Fed has stood pat on rates since December. But the Japanese, the Chinese, and the Europeans have continued to try to goose up their economies with increasingly crackpot monetary policies.

Much of the money thus created has found its way into U.S. markets… which probably explains the refusal of the Dow to go down.

Day of Reckoning

It could be, of course, that we are totally wrong… and that some trend is in place we don’t recognize.

Stock markets are said to “discount the future.” Maybe they see something we don’t.

Or maybe they are simply preparing for a more spectacular day of reckoning by drawing more mom-and-pop investors into deeper water; as always, we wait to find out.

Still, it looks as though the bull market that began in the U.S. in March 2009 is over. And the contraction is not limited to the stock market.

Our economy, our society, and our body politic are all closing up… looking inward… turning their backs on the wider world.

Yes, we are connecting the dots. It is not just the world of money that contracts and expands. The economy breathes, too… and so does our political world.

Why is Donald J. Trump running so strongly in the Republican primaries?

Why is National Front leader Marine Le Pen doing so well in France?

How did Jeremy Corbyn – otherwise a nobody – become the leader of the second-largest party in Britain?

Why is world trade plunging?

Why are inflation expectations running at about 1% for the next decade… despite the biggest increase in central bank balance sheets – the monetary footings of the entire system – in history?

Why are growth rates in Europe, Japan, and the U.S. at their lowest levels since World War II?

And why is $7 trillion of government debt – about one-third of all issuance – now trading at sub-zero yields?

Warning Shot

“Economists fire warning shot on risks of negative interest rates,” reported the Financial Times in a front-page story last week.

“Japan’s negative interest backfire…” it added, again on the front page, two days later.

Why?

Because we are breathing out. Borders are tightening up. Barriers are erected. The “globalism” heralded by New York Timescolumnist Thomas Friedman and others as a solution to all the world’s problems is giving way to “nationalism.”

The expansive EZ money world of the last 30 years is losing air.

Yesterday brought news that consumer savings from the lower price of oil is NOT leading to greater consumer spending… not even in autos. Bloomberg:

U.S. retail sales dropped in February and the prior month’s gain was revised to a decline, calling into question the narrative that bigger gains in consumer spending would propel economic growth at the start of 2016.

The decrease in purchases, which included auto dealers, department stores, and furniture outlets, showed Americans were salting away money saved at the gas pump amid volatile financial markets. The disappointing reading on the biggest part of the economy comes as Fed officials meet to gauge whether growth is strong enough to eventually warrant another increase in interest rates.

“We’re seeing higher rents, higher healthcare expenses, so that may be offsetting a lot of the benefit of lower gasoline prices,” said Scott Brown, chief economist at Raymond James Financial Inc. in St. Petersburg, Florida.

The New Subprime

While current spending slacks off, past spending continues to rattle its chains. Newsmax:

Delinquencies on subprime auto debt packaged into securities reached a high not seen since October 1996, as late payments continued to worsen in February, according to Fitch Ratings.

The number of car borrowers who were more than 60 days late on their bills in February rose 11.6% from the same period a year ago, bringing the delinquency rate to 5.16%, Fitch wrote Monday in a report. During the financial crisis delinquencies peaked at 5.04%, Fitch wrote.

You’ll recall that when we left you yesterday, we promised a look at a deeper malaise. This is it. It is not just the threat of a bear market on Wall Street. Not just a grumpy mood of the voters threatening the Establishment.

It is something bigger… deeper… something unstoppable…

More dots tomorrow…

Regards,

Bill

Market Insight

BY CHRIS LOWE, EDITOR AT LARGE

It’s not just negative-yielding bonds that are spreading like wildfire.

Today’s chart looks at the range of yields on bonds issued by governments in developed countries.

While almost $7 trillion in global government debt now carries a negative yield, another roughly $9 trillion yields between 0% and 1%.

About another $6 trillion yields between 1% and 2%.

Less than $3 trillion in government debt yields 2% or more.

A recent observation by Warren Buffett that the babies being born in America today are the luckiest crop in history. It was his and my generation who were the luckiest — coming along in the wake of WWII, when the U.S. stood astride the world. Opportunity was abundant for anybody who had even the slightest modicum of ambition and was prepared to put in some effort.

A recent observation by Warren Buffett that the babies being born in America today are the luckiest crop in history. It was his and my generation who were the luckiest — coming along in the wake of WWII, when the U.S. stood astride the world. Opportunity was abundant for anybody who had even the slightest modicum of ambition and was prepared to put in some effort.

However, we and the generations after us have left an absolute mess for the children being born in North America today, and I believe it will take decades to sort this out. I really am surprised that a person of Warren’s intelligence would make such an insensitive and patently false remark.

In fact, I totally agree with Egon von Greyerz when he says that this will be the biggest wealth transfer in history. And the money being lost will be from those holding paper instruments, and it will be won by those holding real things. To me that is an absolute self evident and it’s just in the early stages of starting to unfold.”

Question: If there’s another financial catastrophe, can the government save the day again?

Question: If there’s another financial catastrophe, can the government save the day again?

Until recently, nearly all experts would have responded with a stubborn “yes.” They used to think that the Fed and the Treasury, along with their cohorts overseas, could simply spend, print and pump as much money as needed to avoid another global meltdown.

Now, though, they’re not so sure. And some astute analysts are saying the true answer is a flat “no.”

I’ll tell you who in just a moment. But first, I want you to remember one thing: Over the last two weeks, I’ve shown you precisely how to achieve maximum protection from such a disaster. I gave you 5 ETFs for Protection in Another 2008 and my 7-Step Portfolio Protection Strategy.

Today, I’m taking this story one step further. I will show precisely why you can’t rely on anyone else — especially the government — to provide that kind of protection for you. If you want it, you must build it yourself.

The Pundits Throw in the Towel

Let’s not forget who these experts are: They’re the same guys who swore on a stack of Bibles that the almighty Fed would always keep the economy afloat.

Now, however, Barron’s writes, “Based on what is happening in global markets today, central banks won’t be able to ride to the rescue this time.” The Telegraph declares that “the lifeboats are all used up.” And most seem to agree that the next big government rescue could fail — or even fail to materialize — for three reas

Reason #1. The central banks’ latest weapon of mass desperation — below-zero interest rates — could cause more fright that fight … and more market panic than market rally.

Reason #1. The central banks’ latest weapon of mass desperation — below-zero interest rates — could cause more fright that fight … and more market panic than market rally.

Barron’s put it succinctly…

“Negative interest rates are a sign of desperation, a signal that traditional policy options have proved ineffective and new limits need to be explored.”

Reason #2. Instead of prodding banks to make more loans, below-zero interest rates will kill bank profit margins and prod banks to make fewer loans. Instead of easy money, they’ll bring tighter money.

Reason #3. Bank share prices will plunge, weaker banks will go bankrupt and the whole rescue scheme of recent years will backfire.

How big is that scheme? Brace yourself for the answer …

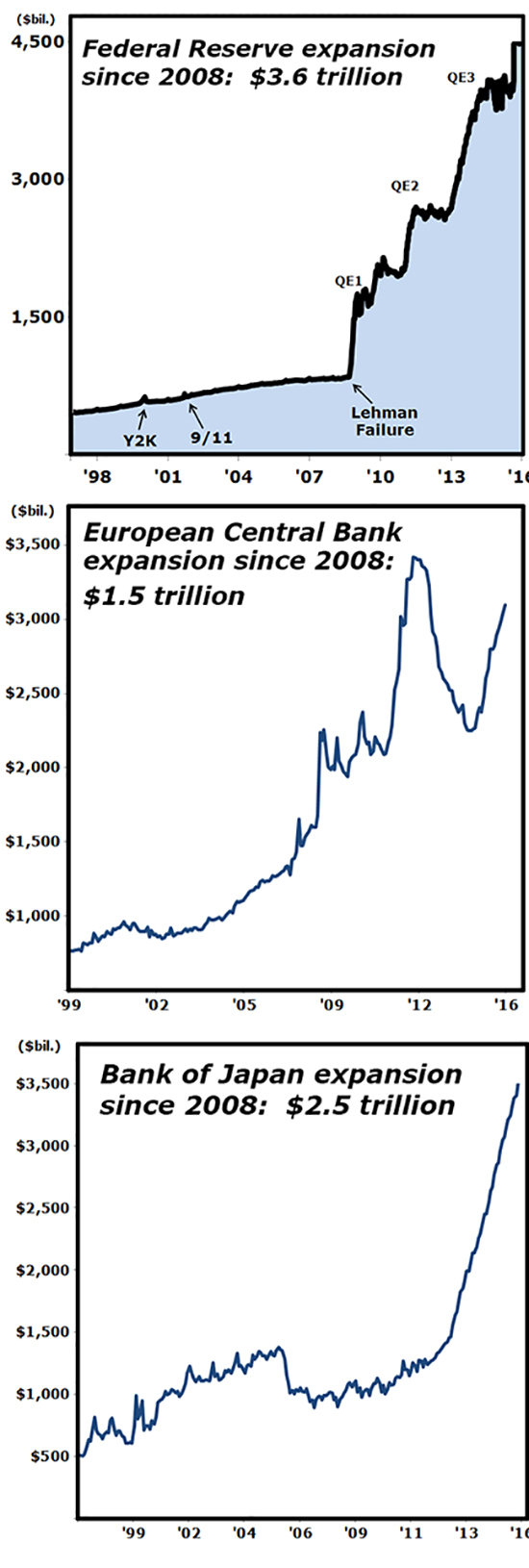

Since the Big Bang of all financial disasters — the collapse of Lehman Brothers on Sept. 15, 2008 — central banks have been expanding their rescue mission at a mind-boggling pace, creating a whole new universe of monetary excess.

The U.S. Federal Reserve went stark, raving mad, abandoning any semblance of restraint, and expanding its assets by a mammoth $3.6 trillion.

Two prior emergency expansions — on the eve of the Y2K turnover and immediately after the terrorist attacks of 9/11 — were minuscule by comparison.

And in just a matter of weeks, all the rule books of Fed policy, written by generations of Fed chairmen, were dumped into the Potomac River.

A set of completely new rules was created on the fly.

And quantitative easing (QE) was born.

The European Central Bank immediately followed in the Fed’s footsteps, expanding their assets by $1.5 trillion.

At one point, they also tried massive lending to banks in a different form, which temporarily replaced their central bank expansion. But now they’ve resumed their quantitative easing, throwing in below-zero interest rates for extra measure.

The Bank of England, although smaller, was equally aggressive, expanding its balance sheet by $435 billion since 2008.

After the Lehman Brothers failure, their money printing went ballistic; and during the European debt crisis, it went ballistic again.

Now it’s on hold temporarily. But the $435 billion in new money is locked in place with no sign whatsoever of retreat.

If you think all of the above is crazy, wait till you see what the Bank of Japan has done:

Since the Lehman Brothers blow-up in 2008, the BOJ has expanded its balance sheet by a whopping $2.5 trillion.

Adjusted for the smaller size of Japan’s economy, that’s the equivalent of a $9.4 trillion expansion in the United States, or more than 2½ times more than the Fed’s.

Even excluding all the other central banks of the world, this big-bang expansion is absolutely unprecedented in all of recorded history:

The Fed’s $3.6 trillion … PLUS … the Bank of England’s $435 billion … PLUS … the European Central Bank’s $1.5 trillion … PLUS the Bank of Japan’s $2.5 trillion … add up to a grand total of more than 8 trillion dollars in monetary expansion just since the Lehman Brothers big bang.

This $8-trillion monster is what had been fueling all the government rescues since the 2008 debt crisis.

This is what’s not working anymore.

This is fundamentally what the experts are now so worried about.

And this is why you need your own portfolio defenses.

Whatever you do, don’t get caught off guard.

Good luck and God bless!

Martin

Dr. Weiss founded Weiss Research in 1971 and has dedicated the past 40 years to helping millions of average investors find truly safe havens and investments. He is president of Weiss Ratings, the nation’s leading independent rating agency accepting no fees from rated companies. And he is the chairman of the Sound Dollar Committee, originally founded by his father in 1959 to help President Dwight D. Eisenhower balance the federal budget. His last three books have all been New York Times Bestsellers and his most recent title is The Ultimate Money Guide for Bubbles, Busts, Recesssion and Depression.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair