Asset protection

Demographics may not rule absolutely, but they likely will dominate investment markets and returns for the next few decades until the Boomer phenomena fades away. The 1% – in addition to the 99 – will need extra doses of Xanax, or additional slices of cake, to cope in the next few decades. Let the games begin.

Demographics may not rule absolutely, but they likely will dominate investment markets and returns for the next few decades until the Boomer phenomena fades away. The 1% – in addition to the 99 – will need extra doses of Xanax, or additional slices of cake, to cope in the next few decades. Let the games begin.

On December 16th 2008, in what Ben Bernanke said took a tremendous amount of “moral courage,” the Federal Reserve officially arrived at its Zero Interest Rate Policy. ZIRP was a huge win for borrowers because it drove down the carrying cost of debt to historic lows. Unfortunately, savers didn’t fare as well…

On December 16th 2008, in what Ben Bernanke said took a tremendous amount of “moral courage,” the Federal Reserve officially arrived at its Zero Interest Rate Policy. ZIRP was a huge win for borrowers because it drove down the carrying cost of debt to historic lows. Unfortunately, savers didn’t fare as well…

Those frantic savers were forced to reach for yield far out along the risk curve. And an obliging Wall Street issued over $1 trillion in new junk bonds at the lowest spreads to Treasuries in the 35 year history of the junk debt market. To put this in perspective, the entire high-yield market had previously hit its frothy peak of $1.2 trillion in the bubbly days of 2007. But in October of last year.…

One of the (many) fascinating things about this latest global financial crisis is that there’s no single catalyst. Unlike 2008 when the carnage could be traced back to US subprime housing, or 2000 when tech stocks crashed and pulled down everything else, this time around a whole bunch of seemingly-unrelated things are unraveling all at once.

China’s malinvestment binge is crashing global commodities, an overvalued dollar is crushing emerging markets (most recently forcing China to devalue), the pan-Islamic war has suddenly gone from simmer to boil, grossly-overvalued equities pretty much everywhere are getting a long-overdue correction, and developed-world political systems are being upended as voters lose faith in mainstream parties to deal with inequality, corporate power, entitlements, immigration, really pretty much everything. For one amusing/amazing example of the latter problem, consider Germany’s response to the mobs of men that suddenly materialized and began molesting women: Cologne mayor slammed after telling German women to keep would-be rapists at arm’s length.

Why do causes matter at times like this? Because where previous crises were “solved” with a relatively simple dose of hyper-easy money, it’s not clear that today’s diverse mix of emerging threats can be addressed in the same way. Interest rates, for instance, were high by current standards at the beginning of past crises, which gave central banks plenty of leeway to comfort the afflicted with big rate cut announcements. Today rates are near zero in most places and negative in many. Cutting from here would be an experiment to put it mildly, with myriad possible unintended consequences including a flight to cash that empties banks of deposits and a destabilizing spike in wealth inequality as negative interest rates support asset prices for the already-rich while driving down incomes for savers and retirees.

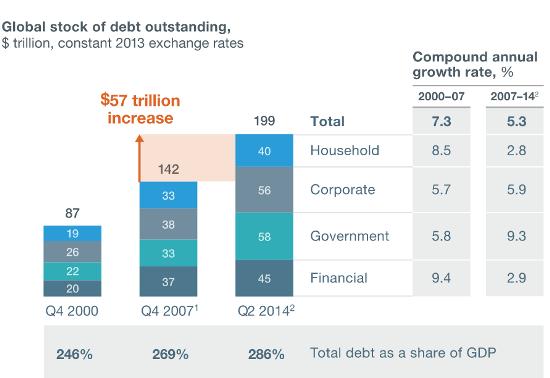

And with debt now $57 trillion higher worldwide than in 2008, it’s not at all clear that another borrowing binge will be greeted with enthusiasm by the world’s bond markets, currency traders or entrepreneurs. Here’s that now-famous chart from McKinsey:

Easier money will have no effect on the supply/demand imbalance in the oil market, which is still growing. The

likely result: Sharply lower prices in the year ahead, leading to a wave of defaults for trillions of dollars of energy-related junk bonds and derivatives.

As for stock prices, in the previous two crises equities plunged almost overnight to levels that made buying reasonable for the remaining smart money. Today, virtually every major equity index remains high by historical standards, so the necessary crash is still to come — and will add to global turmoil as it unfolds.

The upshot? It really is different this time, in a very bad way. And this fact is just now dawning on millions of leveraged speculators, mutual fund and pension fund managers, individual investors and central bank managers. Right this minute virtually all of them are staring at screens, scrolling over to the sell button, hesitating, pulling up Bloomberg screens showing how much they’ve lost in the past few days, calling analysts who last year convinced them to load up on Apple and Facebook, getting no answer, going back to Bloomberg and then fondling the sell button some more. Think of it as financial collapse OCD.

What happens next? At some point — today or next week or next month, but probably pretty soon — the dam will break. Everyone will hit “sell” at the same time and find out that those liquid markets they’d come to see as normal have disappeared and yesterday’s prices are meaningless fantasy. The exits will slam shut and — as in China last night where the markets closed a quarter-hour into the trading session — the whole world will be stuck with the positions they created back when markets were liquid and central banks were omnipotent and government bonds were risk-free and Amazon was going to $2,000.

And one thought will appear in all those minds: Why didn’t I load up on gold when I had the chance?

China’s stock drop rocked oil raising concerns of a global market meltdown.

China’s stock drop rocked oil raising concerns of a global market meltdown.

When China went limit down hitting its new circuit breaker in the first 13 minutes of trading, it drove global equity and commodity markets into a tailspin. It drove Hong Kong’s Hang Seng index down 4.2% to the lowest level since Oct. 6, 2011. This took oil below the levels seen in the depths of the great recession and the comparison is making many folks feel that we are in a new great recession (see chart below). Yet what is real and what is imagined is hard to determine when China does not allow its market to do what it needs to do.

The record in U.S. overall energy stockpiles look even more ominous after the weakness in China. Yesterday the Energy Information Administration reported record petroleum stockpiles led by a 10.5-million-barrel surge in U.S. gasoline supply.

Crude oil saw a 5.1 million barrel drop but the lack of diesel demand due to warm weather still pressures the market. Strong refining margins are keeping refineries going and was helped by low crude prices. Stockpiles at Cushing, OK increased by 917,000 barrels last week.

But if history is a guide, oil prices will spike later this year as bankruptcies and low price inspired demand will start to kick in. Bloomberg News reported that the drop in crude to start the year has wiped off more than 100 billion off its Bloomberg World Oil and Gas index, the worst start since 2004.

Last year, oil and gas bankruptcies totaled $13 billion in North America, 42 companies with $17 billion in debt filed in 2015, the highest level since the financial crisis in 2008. Of these filings, 36 companies with $16.7 billion in debt filed in the United States. There are many companies in the space they call the walking dead that will file, especially if prices don’t rebound soon.

About the Author

Senior energy analyst at The PRICE Futures Group and a Fox Business Network contributor. He is one of the world’s leading market analysts, providing individual investors, professional traders, and institutions with up-to-the-minute investment and risk management insight into global petroleum, gasoline, and energy markets. His precise and timely forecasts have come to be in great demand by industry and media worldwide and his impressive career goes back almost three decades, gaining attention with his market calls and energetic personality as writer of The Energy Report. You can contact Phil by phone at (888) 264-5665 or by email at pflynn@pricegroup.com. Learn even more on our website at www.pricegroup.com.

Yesterday was the worst year-opening for trading in the U.S. markets in 84 years. It was prompted by a 7% drop in the Chinese CSI 300 benchmark index, which led to a halt in Chinese trading.

Yesterday was the worst year-opening for trading in the U.S. markets in 84 years. It was prompted by a 7% drop in the Chinese CSI 300 benchmark index, which led to a halt in Chinese trading.

And all it took to send Chinese stocks spiraling downward was a proposal to lift the ban on major stakeholders selling their shares of Chinese stocks – almost identical to a proposal implemented just six months ago to halt that sell-off. This isn’t working, and it could well be the start of a more precipitous drop.

It’s important to remember that China is much more than the sum of its markets, but investors will have to contend with the chaos that’s spreading out from Chinese stocks. The research and recommendations in this report will help you do just that. You can even find ways to profit from the crash, too.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair