Asset protection

The following is part of Pivotal Events that was published for our subscribers October 28, 2015.

Stock Markets

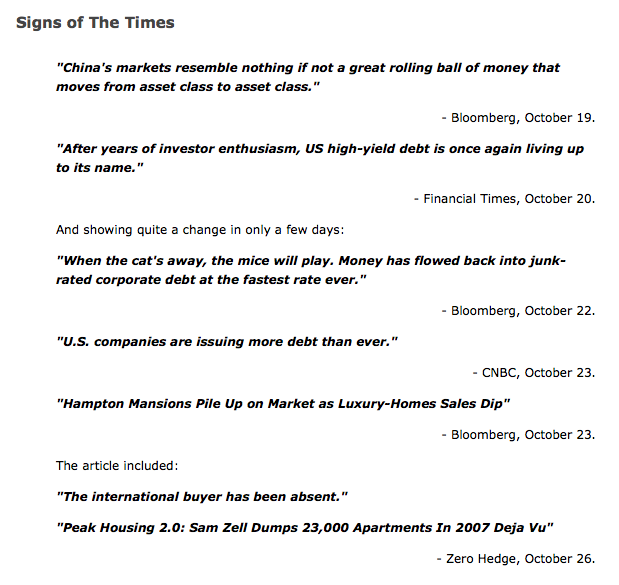

The top headline included a “great rolling ball of money”, as speculators dashed from one sector to another. The problem is that the hit to the SSEC amounted to a $3 trillion loss in market cap. The latest dash has been to the Chinese corporate bond market, which now appears vulnerable.

The ball of speculative money is not only fickle it is diminishing.

The irony is that policymakers still believe that central bank easing drives the economy up. The public isn’t impressed with such theories and bids up what it wants, when it wants. And then it bids them down. Usually, unintentionally.

On the latest bidding up, the ChartWorks had the DJIA reaching the Keltner Band targets at 17505 to 17870. The high has been 17712 earlier today.. This is now generating a Sequential (9) Sell set up. The last one was on May 20th.

The path to the next decline has to face two days of FMOC posturing.

Over in the financial sector, XBD (Broker-Dealers) took the hit and has accomplished a couple of dead-cat bounces. Nothing very constructive. Action in the yield curve has been non-supportive, but the correction in credit spreads has been positive.

Considering the impressive rebound in the S&P, this sector is concerning.

Resources sectors such as base metals and the oil patch have accomplished somewhat better rebounds. Slipping below the 50-Day moving averages would be unhealthy.

As noted a couple of weeks ago, massive interventions could be seasonal. So far the Bank of Japan has not made a sensational headline. Nothing bad can be allowed to happen in October.

Credit Markets

Credits spreads widened out to 242 bps on October 2nd, the day the dreadful employment number was released. This was followed by a massive REPO operation and equally massive short squeeze.

The spread has come in to 224 bps, which is a greater correction than the one that began on August 24th.

The point to be made is that serious widening preceded two sharp hits to global financial markets.

The Treasury curve was very friendly to banks and financials from the first of the year until early July. Then unfriendly to August 20th, and then has been in a narrow range since.

As noted last week, this is trying to breakdown. At 141 now, slipping below 139 would be a negative for the financial markets.

Out of the hit that ended on October 2nd, JNK has had the best rally since things started to go wrong in June. The low was 35.10 and the high was 36.65 on Friday. This is struggling against the declining 50-Day ma and another failure seems likely.

We have been out of lower-grade stuff since the peak in June 2014.

The long bond (TLT) spiked up to 126.21 on October 2nd and declined to 121.66 a couple of weeks ago. It has recovered to 124.90 and the rally has had a target at the Keltner band, near 126.

This pattern could generate a MCD Sell.

We’ve been standing aside since the high of 128.37 on Black Monday.

China Corporate Bond Bubble

• The February high in the Chinese market was very close to that salient peak in US Treasuries.

• Subsequent highs were not coordinated with swings in the US market.

• The Euro bond market followed the US peak by setting its high in April and failing.

• Treasuries are getting close to the mext significant price decline.

• Chinese bonds have rallied against the decline in the Shanghai Stock Market.

• Has the bond buying been equivalent to the frenzy in the SSEC that peaked in June?

Link to October 30 Bob Hoye interview on TalkDigitalNetwork.com:http://talkdigitalnetwork.com/2015/10/will-us-interest-rates-rise-in-december/

Listen to the Bob Hoye Podcast every Friday afternoon at TalkDigitalNetwork.com

With continued volatility in global markets, today one of the top economists in the world sent King World News an incredibly powerful piece warning about global fiscal and monetary madness, economic chaos and the first worldwide inflationary depression.

With continued volatility in global markets, today one of the top economists in the world sent King World News an incredibly powerful piece warning about global fiscal and monetary madness, economic chaos and the first worldwide inflationary depression.

“Today features a piece by a man whose recently released masterpiece has been praised around the world”

‘During the press conferences of the recent FOMC meetings, millions of well-educated investment professionals will have been sitting in front of their screens, chewing their fingernails, listening as if spellbound to what Janet Yellen has to tell them. Will she finally raise the federal funds rate that has been zero bound for over six years?”

…read it HERE (fascinating article – Money Talks Ed)

NORMANDY, France – “Now, I think I’ve seen everything” is an expression that – like “this is the end of history” and “I’ll never leave you” – usually turns out to be premature.

But it is what we found ourselves saying yesterday.

Not out loud. We just moved our lips in mute amazement.

On Tuesday, the Italian government sold a 2-year note yielding MINUS 0.023%.

We don’t know what is more preposterous: that the Italians were able to borrow money at a negative nominal interest rate or that the press reported this transaction with a straight face.

The Fed’s Big Pivot

It should have provoked howls of laughter, withering scorn, and unvarnished derision.

But here at the Diary, we will not point the finger and chuckle. We will not invoke our usual tone of sarcasm. We will not damn the whole thing to Hell with loud and blustery cussing.

Instead, we’ll take the high road; we just want to know what it means.

But before we get to that, let us pick up the news. Here’s the latest, from Bloomberg:

Federal Reserve officials pivoted toward a December interest-rate increase, betting that further job gains will lead to higher inflation over time and allow them to close an unprecedented era of near-zero borrowing costs.

The Federal Open Market Committee dropped a reference to global risks and referred to its “next meeting” on Dec. 15-16 as it discussed liftoff timing in a statement released Wednesday in Washington, preparing investors for the first rate rise since 2006.

“Pivot” has become the latest fad verb. It seems to mean “move” or “go toward.” You can use it in practically any setting.

Investors pivoted toward higher prices yesterday, with a 198-point increase in the Dow. You might tell your husband that you’re pivoting toward buying a new Tesla. And we pivoted back to France last night… after a few days in Ireland.

It is a gray day in Normandy this morning. But the leaves have pivoted to such glorious shades of orange that the effect is a profound and melancholy splendor.

But let us pivot back to our subject for today…

An Odd World

A negative nominal interest rate – meaning a negative rate before you account for inflation – implies an odd world…

…maybe even a world that cannot really exist.

To lend at less than zero suggests you believe the present value of money is less than its future value – in other words, deflation. And you must assume that the risk of default or inflation is near zero.

This allows the Italians to go out and build roads or pay pensions with money that cost them less than nothing.

How long this will last, we don’t know. But as long as rates remain below zero (and they could go lower!) money is not just free… it’s a cost not to borrow!

Imagine you are buying a house. (Now, you can see the mischief afoot!) If lenders are willing to grant a loan at a negative nominal interest rate that’s secured by nothing more than the full faith and credit of the Italian government, then lenders should surely be willing to extend credit to you against the value of your house.

That would leave you with a curious mortgage – one that pays you interest. At the Italian rate, a $1-million house would come with an extra income of about $19.16 a month.

This raises profound metaphysical issues. If a mortgage carries negative interest, it implies that the house (an equal capital value) also has negative value.

After all, you have to pay someone to live in it. And if houses are worth less than nothing, we have to wonder what a car is worth… or a diamond ring… or a luxury cruise?

Does that mean that money has no value? Or even negative value?

After all, you can no longer give it to someone in exchange for a positive interest payment. Now you must pay him to store it for you, as though it were furniture that won’t fit in your house. You don’t like it anymore. But you don’t have the heart to throw it away.

And if money has no value, what happens when you hire, say, a gardener to pull out weeds? Should you pay him? Or should he pay you? How many hours should he have to work for you before you consent to take his money?

The whole thing is so contrary to nature we gasp when we think of it. We are flummoxed.

But you are a smart person, dear reader: Maybe you can figure it out for us.

The Strange Case of Sweden

This is all prelude to taking up the strange case of Sweden…

All we know about Sweden is what we learned by watching the movie The Girl with the Dragon Tattoo.

And all we learned from that was that Swedes tend to be murderers, sadists, lesbians, and pock-marked wimps.

Maybe that accounts for the torturous financial system the Swedes are creating.

Reports Business Insider:

“Sweden is shaping up to be the first country to plunge its citizens into a fascinating – and terrifying – economic experiment: negative interest rates in a cashless society.

The Swedish central bank, the Sveriges Riksbank, on Wednesday held its benchmark interest rate at -0.35%, the level it has been at since July.

Though retail banks have yet to pass that negative rate on to Swedish consumers, they face increased pressure to do so as long as the rates remain where they are. That’s a problem, because Sweden is the closest country on the planet to becoming an all-electronic cashless society.

Remember, Sweden is the place where, if you use too much cash, banks call the police because they think you might be a terrorist or a criminal. Swedish banks have started removing cash ATMs from rural areas, annoying old people and farmers. Credit Suisse says the rule of thumb in Scandinavia is: “If you have to pay in cash, something is wrong.”

A resistance is forming, and some people are protesting the impending extinction of cash. Björn Eriksson, former head of Sweden’s national police and now head of Säkerhetsbranschen, a lobbying group for the security industry, told The Local, “I’ve heard of people keeping cash in their microwaves because banks won’t accept it.”

Alert readers will recognize this negative interest story as one we have been following. We believe it won’t be long before we have negative rates in the U.S., too”.

The feds will pivot to even stricter controls on cash to gain more control over the economy and practically unlimited power to tax and spend – without congressional approval.

Sweden is ahead of the U.S. feds on this one. We can only hope it goes far ahead, fast, and blows itself up before the U.S. pivots down that path, too.

Regards,

Bill

Further Reading: Yesterday, we began a special Diary series with currencies expert Jim Rickards on governments’ ongoing war on cash. Catch up on Part I of our three-part Special Edition here.

Tech Insite

[Editor’s Note: We’ll soon be launching a new investment advisory, Exponential Tech Investor, to help you profit from game-changing innovations. Below, editor Jeff Brown identifies an exciting area of breakthrough technology.]

DNA sequencing is an area of tech I’m keeping a close eye on. That’s because it’s undergoing exponential change…

The technology has been around for decades. But it was far too expensive to be practical. We just didn’t have the abundance of low-cost computing power that’s available today.

The first human genome was sequenced in 2000 at a cost of $2.7 billion. Today, the cost of sequencing has dropped to less than $1,000. Within two years it will be less than $100. By 2020, I expect it will essentially be free.

Why will DNA sequencing be free? Because companies will pay for the information, so you won’t have to.

Facebook is free because it sells your valuable personal information to companies all around the world. Similarly, DNA sequencing will be free because companies will pay to have access to the data they collect.

Which industry players would want access to DNA data?

Biotechnology and pharmaceutical companies want the data to accelerate their testing and developing of new medicines. This will help bring new products to market more quickly. Drugs will be personalized for individuals. Fewer side effects, better efficacy, more revenue, higher profits.

Health insurance companies want the data for preventive medicine techniques. This will help reduce costs.

Employers have similar interests. DNA-sequencing would help reduce their costs by improving the health of their employees.

Highly personalized and preventive medicine will lead to longer lives. Living to 120 will not be unusual for anyone young and in good health today… 100 will be the new 60.

The DNA-sequencing market is expected to grow to $20 billion by 2020. And right now, Illumina (NASDAQ:ILMN) is the global leader in sequencing equipment.

“Central banks have been pulling out all the stops with their financial repression to keep their over-indebted, bloated welfare states alive. Just as importantly, we can see from the U.S. government’s precarious financial position how close it is walking along the edge of the precipice.”

“Central banks have been pulling out all the stops with their financial repression to keep their over-indebted, bloated welfare states alive. Just as importantly, we can see from the U.S. government’s precarious financial position how close it is walking along the edge of the precipice.”

related at King World News:

Global Economy on the Verge of Collapse as it Turns Down in an Already Bankrupt World

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair