Asset protection

Most analysts assume inflation is low because they watch government statistics that track prices across the economy. But Marc Faber is no ordinary analyst.

Most analysts assume inflation is low because they watch government statistics that track prices across the economy. But Marc Faber is no ordinary analyst.

Over the last several years, he vehemently opposed quantitative easing programs from the Federal Reserve which Wall Street officials welcomed with open arms.

The Fed’s easy money policies were reactions to the stock market crash, a crisis management technique to stop asset prices from collapsing. Low interest rates were a central feature of the plan.

Making it easier to borrow money was supposed to boost spending, but Faber argues it caused near-irreparable damage. He was typically contrarian when asked whether the Fed missed its chance to raise interest rates.

“They should have raised the rates, in my view, in 2011 already, or never lowered them to such a low level,” said Faber. “Now the problem is the global economy is slowing down […] it would be very difficult to raise interest rates at the present time.”

also:

Marc Faber on Greece Doom & Gloom

Massive artificial stock, bond wealth will be looking for a place to go

By the time Goldman Sachs published its widely referenced warning of a third wave in the global financial crisis (mid October), the physical precious metals’ markets were already feeling the strain of very strong demand against a rapidly dwindling supply. China, the country seemingly at the epicenter of the developing emerging market crisis, by itself had taken 911 tonnes of gold off the market in the first half of 2015 – a number when annualized that represents nearly two-thirds of the world’s mine production. India, another of the so-called BRICS nations (Brazil, Russia, India, China and South Africa) was a strong second at 400-500 tonnes. In the occident, gold demand was strong, but silver demand was even stronger. Global mints were reporting off-the-charts demand for silver bullion coins. Coin premiums were on the risein extremis at one point reaching almost $6 per ounce on the propular silver American Eagle.

Now with warnings of the next leg of the financial crisis surfacing almost daily, that demand could accelerate

to an even higher lever. The massive, artificial wealth built-up in the world’s stock and bond markets will be looking for a place to go and one likely beneficiary will be the underpriced gold and silver markets. If premiums in the silver market are telling us anything, it is that the migration to precious metals has already begun, and that it is being led by Main Street.

Goldman says that “increased uncertainty about the fallout from weaker emerging market economies, lower commodity prices and potentially higher U.S. interest rates are raising fresh concerns about the sustainability of asset price rises, marking a new wave in the Global Financial Crisis.” The Guardian, a British newspaper, draws similar conclusions. The IMF’s recently released Global Stability Report, it says, “makes for a sobering read, saying sustainable recovery has failed to materialise and cheap money has led to bubbles and debt. The next financial crisis is coming, it’s a just a matter of time – and we haven’t finished fixing the flaws in the global system that were so brutally exposed by the last one.”

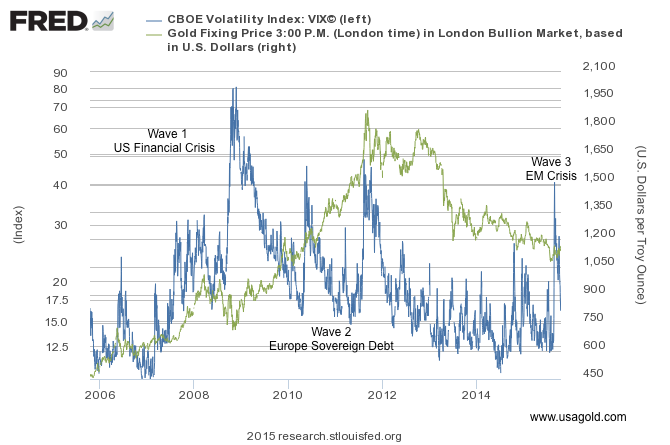

Editor’s Note: With reference to the chart above, this overlay, modeled on Goldman’s third wave thesis, shows the relationship between the Volatility Index (blue line) and the price of gold (green line). “The CBOE Volatility Index,” according to Investopedia, “shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options. This volatility is meant to be forward looking and is calculated from both calls and puts. The VIX is a widely used measure of market risk and is often referred to as the ‘investor fear gauge.'” As you can see, gold lags the Volatility Index which, as Investopedia points out, is forward looking. If Goldman’s analysis is correct, and we are early in the process, the recent breakout in the gold price could be a harbinger of things to come. Please note the recent surge in volatility index – the investor fear gauge. Gold’s inflation hedge characteristics are well-known, but what is not widely understood or publicized is gold’s practicality as a disinflation and deflation hedge – a characteristic prominently illustrated in the chart which covers a distinctly disinflationary period.

“Volatility provides exposure to our collective insecurity towards an unknowable future. Likewise, to short volatility is to express personal confidence in the status quo of market affairs despite a broader fear of change. To go long volatility is to express fear that change is coming.” Artemis Capital Management

Instead of going long volatility, perhaps a simpler, more direct approach is called for:

“A recent IMF paper showed that gold was viewed by central banks as an asset that could be used to reduce risk. These results are consistent with a survey ANZ (Australia and New Zealand Banking Group) conducted with central banks and sovereign wealth fund managers in early 2014 which found that almost half of the respondents believed that gold was a safe haven asset over the long-term. Additionally, over 60% of respondents believed that gold would constitute a larger proportion of central bank reserves over the next two years, with just over 20% expecting a decline. Further, around half of the respondents thought holding more gold could mitigate portfolio risks, most of which were central bankers from ‘low-middle income’ countries.” – ANZ Research, “East to Eldorado: Asia and the Future of Gold”

Something happening in Shanghai

Quietly gold has started to register gains in the overnight Shanghai market. For a very long time, the overnight market (from a U.S. perspective) more or less followed along with the prevailing trend in London and New York. Over the past few weeks, the Shanghai market has taken on a life of its own with solid gains over the London and New York closes registered on a regular basis. In fact, as the chart below illustrates, a case could be made that much of the recent rise in the price of gold has occurred in the Hong Kong-Shanghai markets. These overnight price adjustments could foreshadow the gold market’s future. By this I do not mean to say that the direction is going to be exclusively to the upside. The real point is that China’s presence is going to be felt – up or down – and that presence is going to play significantly in the flow of real metal. The Shanghai Gold Exchange, as readers of this newsletter are already aware, is slated to launch its new fix by the end of 2015. In addition, the new London price setting regime already includes one Chinese bank with two others scheduled to join in the near future. As a result, China’s influence in the gold market, already a key factor, should increase markedly.

With its appetite for the physical metal now a well-established fact of life, China will likely serve as a foil to the current paper-based pricing regime. Chinese banks in London will be on the constant lookout for arbitrage opportunities that can be purchased and shipped to their home country. Meanwhile, the price posted in Shanghai will be for physical delivery only – no paper settlements or rollovers. In this new gold market, China, perhaps inadvertently, will act as a proxy for gold coin and bullion owners all over the world.

For deeper background and details on the London-Shanghai gold trade and what it might mean for the average gold owner, please see the following:

Will the Shanghai Fix ‘fix’ the gold market? China takes a seat at the gold pricing table

The Shanghai stock crash and China gold demand – What it means for the future of the gold market

Is helicopter money in our future?

“I certainly was not eager to bail out Wall Street,” Ben Bernanke reminisces, “and I had no reason to want to bailout Wall Street itself. But we did it because we knew that if the financial system collapsed, the economy would immediately follow.” With that Bernanke revealed the thinking behind the money printing extravaganza that followed thereafter – nearly $4 trillion added to the Fed’s balance sheet, billions in bailouts for Wall Street, and precious little for Main Street. Bernanke, in short, is saying that “the devil made me do it.” Now seven years later, we find ourselves no better off as a nation economically and staring a situation in the face that looks very much like the previous crisis, only this time with Wall Street likely to lead the slide into potential chaos, rather than the housing market.

More and more, investors and analysts alike are beginning to believe that another round of quantitative easing is in our collective futures and that, more than likely, is part of the psychology driving gold out of the doldrums. Some think that since quantitative easing had little impact the first time around, policy makers will try fiscal stimulus instead – infrastructure projects or even an outright universal helicopter money drop like manna from the heavens. That could become reality, but don’t rule out another helicopter drop on Wall Street for good measure. If you liked Ben Bernanke’s reaction to the economic crisis, you are going to love Janet Yellen’s. She wasn’t appointed by Barrack Obama because she had a problem letting the dogs loose if the situation warranted it.

We will end this short overview with a quote from billionaire hedge fund manager Paul Singer: “Although the levitation of financial assets has yet to levitate gold, we will grit our collective teeth on that score and await either ‘asset price justice’ or the ‘end times,’ whichever comes first.” Along with levitating gold, asset price justice is likely to lift silver as well.

American Eagle gold and silver bullion coins (Photo by USAGOLD’s Jen Dentry)

We invite you to visit USAGOLD’s Piles of Gold image gallery.

FYI – If you appreciate the kind of gold-based analysis you are now reading, you would probably find value in subscribing to News & Views and receiving regular issues and special reports promptly by e-mail. It comes free of charge and you can opt out of the service at anytime. Last, we will not deluge you with e-mails. Over 20,000 subscribe to this newsletter – one of the best and most widely read in the field. Never miss another issue. . . Please register here.

“A toxic combination of forces coming our way”

“A toxic combination of forces coming our way”

“Recent comments by Fed officials of possibly “going negative” in the US show how desperate the situation has become with growth weakening in the US, a global economy in trouble, and a whole host of geopolitical problems brewing overseas”

With continued uncertainty in global markets, the Godfather of newsletter writers, 91-year-old Richard Russell, warned that Americans are scared to death and he also declared what will confirm a new bull market in gold.

With continued uncertainty in global markets, the Godfather of newsletter writers, 91-year-old Richard Russell, warned that Americans are scared to death and he also declared what will confirm a new bull market in gold.

Quick Summary: War, central banks are losing control, and a derivative disaster – will lead to rising gold prices.

Quick Summary: War, central banks are losing control, and a derivative disaster – will lead to rising gold prices.Gold Prices Will Rise Because …

A) War in Syria, Ukraine, Middle East, South China Sea and other places seems more likely each month. History shows that wars are inflationary, commodities increase in price, and governments finance wars with debt and fiat currency. We want higher gold prices and no war, but the “powers-that-be” will do what is necessary to increase their power and wealth, and if that requires war, then expect more war.

When armies invaded other countries throughout history, were they more interested in confiscating gold or paper currencies? Who wants fiat currency when it is circling the drain on its way toward zero? In troubled times the preferred asset is gold, not devaluing paper currencies issued by insolvent countries and central banks.

B) Central banks will lose control over interest rates and that will pose a huge risk to the global financial system. Expect much higher gold prices as rising interest rates force insolvent governments to more aggressively monetize debt and devalue their currencies.

Unless you believe that central banks can hold interest rates low for decades, regardless of what markets, investors, and individuals believe is appropriate, there is significant risk of rising interest rates.

C) A derivative disaster as a consequence of rising interest rates – is a bomb waiting to explode. The fuse is probably burning at this moment…

- There are over $500 Trillion in interest rate derivatives outstanding. We can safely assume that banks have taken an initial skim for their commissions, and that the derivative contracts are substantially under-margined.

- The current plan is that those derivative contracts will protect borrowers from interest rate risks in the future, just like the previous plan was that derivative contracts would protect from the sub-prime mortgage markets in 2008.

- The plan in 2008 failed, the financial system nearly “froze up” and the Fed cranked out over $16 Trillion in new currency, swaps, guarantees, bailouts, and other paper. Debt has dramatically increased but economies have not recovered.

- The global system is now more leveraged than in 2008, debt is roughly $60 Trillion higher, and the derivative contracts “protecting” borrowers are currently many times larger than in 2008.

- New York, London, Brussels, Frankfurt, and Tokyo – we have a problem.

- The problem is structural, increasing, and highly dangerous. The “snowflake” that will start the “avalanche” of financial destruction could fall at any moment or not for several years.

- Unless the “powers-that-be” allow a highly destructive deflationary depression that will result from such an implosion, central banks are likely to print hundreds of trillions of currency units to “paper over” the problem.

- Currency units will devalue, the purchasing power of savings will disappear, and gold prices will revalue HIGHER.

- Place your trust in gold (and silver) … or trust that your assets, savings, and purchasing power will be protected by bankers, politicians, and fiat currencies. It should be an easy choice.

From Daniel Ameriman:

“One could even say that by having created such a fantastically large level of risk the financial firms are effectively blackmailing the governments to make sure they never have to pay out, and the governments are allowing this because 1) so much money is being made by connected insiders; 2) it hasn’t actually blown up yet; and 3) the voters have no clue about what is actually happening.

There is an elaborate vocabulary and mathematics for derivatives that goes well beyond the knowledge of most financial professionals, let alone the general public. They are created by the largest and most prestigious financial firms in the world. Yet, once the veneer of these layers of impenetrable mathematics, jargon, “expertise” and the perception of overwhelming financial authority is pierced – what is left is nothing more than a basic form of insurance scam, i.e. collecting premiums for policies that can’t be honored. And if something does go wrong with that scam – then it is all of us who are the ones who will pay together, as taxpayers and investors.”

Gold prices will rise …

- Because of war, increasing debt to pay for those wars, and the inevitable destruction of purchasing power of fiat currencies.

- Because insolvent, hopelessly indebted countries owe far more than can ever be repaid in CURRENT dollars, euros, pounds and yen – and therefore central banks will “print” and devalue.

- Because, regardless of the story promoted by politicians and bankers, it is unlikely that interest rates can be maintained at multi-generational lows for several more decades.

- Because the inevitable derivative disaster will make the 2008 crisis look like a summer rain compared to the financial hurricane that approaches.

-

Because “if something does go wrong with that [derivatives] scam – then it is all of us who are the ones who will pay…”

- Because history shows that people trust gold more than fiat currencies. It should be an easy choice.

When gold prices rise in earnest (ask the High Frequency Traders for a precise date) they are likely to rise rapidly and cause financial media comments such as, “Nobody saw that coming…”

Gary Christenson

The Deviant Investor

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair