Bonds & Interest Rates

The Check and Balance is the Debt Itself

QUESTION:

Today it appears that we will first eliminate the paper currencies and move to a new electronic version to make avoiding taxes impossible. Hence people will flee to tangible assets and the velocity of money will decline taking the economy with it. That will most likely then result in civil unrest/war and then we will see a new type of Bretton Woods rebuilding the global economy adopting some new electronic world reserve currency.

Why will the governments not print new fiat money to infinity to delay the civil unrest/war?

Regards

FK

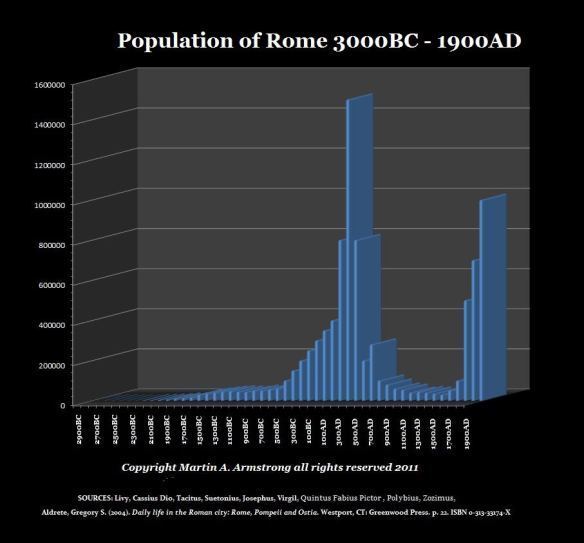

ANSWER: Besides hyperinflation has only taken place in a post-revolutionary government or one that has NO BOND market, the core economy has ALWAYS collapsed by deflation WITHOUT EXCEPTION. It is war upon the people which causes society to collapse. The population of Rome collapsed because taxes kept rising and people just walked away from their property and that began the Dark Age and serfdom.

This story of hyperinflation has been the greatest bullshit sales job I have ever seen. It has zero basis in fact and it is simply a fraud upon the people to sell them gold. This nonsense has been used as the primary sales tool since the 1970s. It works unbelievably for it is purely sophistry.

There is the check and balance in a viable economy. Politicians will not turn to hyperinflation but default on obligations (pensions) because they understand the debt must be maintained or they lose power. I have explained numerous times that this absurd nonsense of hyperinflation is propaganda just to sell gold. It is factually incorrect as to the cause, and it is a complete distortion of history. Hyperinflation followed the German communist revolution where they DEFAULTED on all debt of the previous government and wanted to join Russia. They could not sell bonds and capital withdrew from the banks.ALL tangible assets rose in value against fictional money. It was real estate that ultimately became the backing of the new currency in the aftermath.

In our case, there is no wholesale default on debt. That would wipe out pensions including the Social Security system that has bonds in the drawer. It is the debt that is the check and balance. They will raise taxes trying to hold the system together. You will get war if you default both internationally and domestically. As they say – damned no matter what we do.

DEFLATION is the ONLY way empires, nations, and city states collapse. That is a historical fact! You can count the hyperinflations on one hand historically – you need a computer to count the defaults by deflation of numerous government since 6000 BC. Those in power shake-down the people to retain power. This is what they do! We have massive debt at the state and local levels that cannot print money. They can only default and that is the second force behind deflation as we saw in the City of Detroit.

No government has ever survived indefinitely. It has been debt that is ALWAYS the great destroyer.

also:

EU Wants to seize money from All European Banks on a Flat Rate Basis

Today Canadian legend John Ing warned King World News that the moves by the ECB and other central planners will end in disaster. Ing, who has been in the business for 43 years, said it is just a matter of time before disaster strikes, and he also spoke about key events in a number of other markets:

Today Canadian legend John Ing warned King World News that the moves by the ECB and other central planners will end in disaster. Ing, who has been in the business for 43 years, said it is just a matter of time before disaster strikes, and he also spoke about key events in a number of other markets:

Ing: “Thursday was what I consider a turnaround day as Draghi dropped European rates to negative territory”

Continue reading the John Ing interview HERE

Prediction: European Central Bank leader Mario Draghi is going to disappoint people tomorrow. We just don’t know who they will be.

Tomorrow’s ECB action will be a huge media event, much like last year‘s Federal Reserve meetings. Ben Bernanke kept us all in suspense for months over the “taper“ decision, and then most Fed news went back to being routine and unexciting.

The same may happen tomorrow …

Most of Europe is still stuck in recession, or at least close to it. The ECB is the central bank for countries in the euro currency system. The U.K. doesn’t use the euro — but Germany, France, Spain, Italy, Greece, and others do. Draghi is their version of Janet Yellen or Ben Bernanke.

As far as I can tell, most Europeans want Draghi to “do something“ that stimulates economic growth.That’s where the agreement ends. Many Germans worry about inflation, while Greeks want more inflation.

Draghi can’t please everyone. So what will he do?

The expectation as of this afternoon is that the ECB will cut its “deposit rate,” which is the amount of interest it pays for reserves that European banks must deposit with the ECB. That rate has been 0% since July 2012.

How do you cut rates below zero? Draghi is probably about to show us exactly how.

If the deposit rate goes to -0.1% or -0.15%, banks will have to start paying the ECB for the privilege of complying with laws that make them deposit money there. The theory is that discouraging banks from holding cash at the ECB will make them increase lending to people and businesses, thereby stimulating growth.

I don’t believe it will work that way. Loan rates in Europe are already over 5%. If the spread between 0% and 5% isn’t enough to make banks start lending, another 0.1% won’t make much difference.

So why go to the trouble? Draghi and his colleagues may think the psychological jolt of negative interest rates will have some kind of positive impact. They’re also trying to discourage foreign capital from entering Europe and making the euro currency stronger.

It’s also possible the ECB will launch an asset purchase program, similar to the Fed’s quantitative easing policy. We don’t know what assets they would buy, or whether a European QE will work any better than QE did over here.

Some of our analysts are on the other side of that opinion. In fact, my colleague Geoff Garbacz made a bet today: a bottle of Chilean Malbec wine if the ECB does asset purchases.

***

Bond traders already presume the ECB will pull the negative interest rate trigger. Markets have “priced in“ that change, so reaction will be minor if that’s all we get.

All bets are off if Draghi surprises the markets with a Euro QE or other new schemes. The news will break in the morning hours for Americans, so our markets could get crazy.

Warning: If you’re planning any portfolio changes, tomorrow is probably not a good day to implement them. Friday may not be, either, if the U.S. jobs report contains any big surprises.

Even if you aren’t trading anything directly exposed to Europe, events like this one can create gyrations for everyone.

If you’re not a professional trader, the best move is to watch from the sidelines. The near-term forecast will be a lot clearer once these two events are behind us.

***

Speaking of Europe, President Obama is over there right now. Today in Warsaw he met with Ukrainian president-elect Petro Poroshenko.

From there, Obama went to Brussels for a meeting with the former G-8 group, which is now down to G-7 with Vladimir Putin’s ejection. Putin was originally supposed to host this meeting in Sochi, Russia.

Obama and Putin will still cross paths when both attend a ceremony Friday marking the 70th anniversary of the Allied invasion at Normandy. According to press reports, Putin’s schedule includes private meetings with French president Francoise Hollande, German chancellor Angela Merkel, and British PM David Cameron.

No Obama-Putin meeting shows up on any schedule I’ve seen — but they will both be inside the same big French chateau for several hours. Maybe something will happen once the cameras are off. They certainly have plenty to discuss.

FOMO.

I heard this acronym on a podcast last week. Having no clue what it meant, I consulted Google.

Turns out it stands for “Fear of Missing Out.” Kids use it to describe their anxiety about missing a social event that all of their friends are attending.

It struck me that investors experience FOMO too. And it usually leads to bad decisions

From Prudent to FOMO

In the comfort of your home office, investing rationally is pretty easy. You think a bull market might be emerging, so you invest in the S&P 500.

But you’re not stupid. No one really knows where the stock market is headed, so you keep a healthy allocation of cash on the side to deploy the next time stocks trade at bargain prices. A prudent, rational plan.

But leave the house and things start to change. You notice that others seem to be making more money than you. First it’s the “smart money” raking in the dough — those who had the foresight and fortitude to buy during the last panic, when everyone else was retreating. You’re OK with that. Investing is their full-time job. You can’t expect to compete with them.

But as the bull market charges higher, the caliber of people making more money than you sinks lower. The mailman starts giving you stock tips. And your gardener’s brand-new Mustang, parked in your driveway just behind your sensible, 2011 Toyota Corolla, starts to irritate you.

Your brother-in-law is the last straw. He thinks he’s so smart, but he’s really just lucky to somehow always be in the right place at the right time. I mean, just last month you had to pick him up from a NASCAR tailgate after security kicked him out for lewd behavior — and now he’s taking the family to Europe with his stock market winnings?

If that guy can make $30,000 in the market in six months, you should be a millionaire.

Now you feel like a sucker for holding so much cash. Why earn a pitiful 0.5% interest when you could be making… hang on, how much did the S&P 500 gain last year? 29.6%?

Some quick extrapolation shows that if you invest all of your cash right now, you can retire by 2023. Factor in a couple family trips to Europe, and we’ll call it 2024 to be safe.

Cash Is Trash… Until It’s King

Such is the (slightly exaggerated) psychology of a bull market. FOMO is a powerful motivator and causes smart investors to do stupid things, like go all-in at the worst possible moment. Which is no small concern, since it undermines one of the most powerful investment strategies: keeping liquid cash in reserve to invest during market panics.

Take the roaring ’20s as a long-ago but pertinent example. The surging stock market of that era caused a whole lot of FOMO. Seeing their friends get rich, people who had never invested before piled into stocks.

Of course, we know how that ended.

But there’s a fascinating angle that you may not have given much thought. I hadn’t until yesterday, when I finished reading The Great Depression: A Diary. It’s a firsthand, anecdotal account written by attorney Benjamin Roth.

Roth emphasized that during the Great Depression, everyone knew financial assets were great bargains. The problem was hardly anyone had cash to take advantage of them.

Here are a few quotes from the book:

August 1931: I see now how very important it is for the professional man to build up a surplus in normal times. A surplus capital of $2,500 wisely invested during the depression might have meant financial security for the rest of his life. Without it he is at the mercy of the economic winds.

December 1931: It is generally believed that good stocks and bonds can now be bought at very attractive prices. The difficulty is that nobody has the cash to buy.

September 1932: I believe it can be truly said that the man who has money during this depression to invest in the highest grade investment stocks and can hold on for 2 or 3 years will be the rich man of 1935.

June 1933: I am afraid the opportunity to buy a fortune in stocks at about 10¢ on the dollar is past and so far I have been unable to take advantage of it.

July 1933: Again and again during this depression it is driven home to me that opportunity is a stern goddess who passes up those who are unprepared with liquid capital.

May 1937: The greatest chance in a lifetime to build a fortune has gone and will probably not come again soon. Very few people had any surplus to invest — it was a matter of earning enough to buy the necessaries of life.

In short, by succumbing to FOMO and investing all your cash, you might be giving up the opportunity to make a literal fortune. You can’t shoot fish in a barrel without ammunition.

Of course, the parallels from the Great Depression to present-day crises aren’t exact. The US was on the gold standard back then, meaning the Fed couldn’t conjure money out of thin air to reflate stock prices. Such a nationwide shortage of cash is unthinkable today, as Yellen & Friends would create however many dollars necessary to prevent stocks from plummeting 90%, as they did during the Great Depression.

That’s exactly what happened during the 2008 financial crisis, as you can see below. The Fed injected liquidity, and stocks rebounded rapidly. Compared to the Great Depression, the stock market crash of 2008 was short and sweet:

What does that mean for modern investors?

When the next crisis comes — and it will — there will be bargains. But because of the Fed’s quick trigger, investors will have to act decisively to get a piece of them.

What’s more, now that the US government has demonstrated beyond the shadow of a doubt that it will prop up the economy, bargains should dissipate even quicker next time around. After all, the hardest part of buying stocks in a crisis is overcoming fear. But that fear isn’t much of a detriment when Uncle Sam is standing by with his hand on the lever of the money-printing machine, ready to rescue the market.

Crises can creep up on you faster than you think. You may never know what hit you–unless you knew what to look for ahead of time. Watch Meltdown America, the eye-opening 30-minute documentary on how to recognize (and survive) an economic crisis — with top experts including Sovereign Society Director Jeff Opdyke, investing legend Doug Casey, and Canadian National Security Council member Dr. Andre Gerolymatos.

Be prepared… it can (and will) happen here. Click here to watch Meltdown America

Gold has not closed outside the range of 1,282 to 1,311 US per oz. since April 14, 2014. It has made the market action over the last six weeks decisively boring. That being said, the low level of volatility in the metals market has been accompanied by seesawing equities. Fridays close on the S&P500 above 1900, despite sitting on record levels, marks the fourth time since March the benchmark US index has attempted to breakout past that physiological barrier. Nonetheless, the one market that has made a significant move in one direction has been US treasuries. While it remains difficult to draw conclusions from passive metal prices or volatile stock markets, it’s the bond market that highlights the perplexities of the western economies stalling economic recoveries. Additionally, it questions whether the outlook for increasing long term interest rates is still intact.

The prospect of the US economic recovery yet again losing pace seems to be what has brought investors back into the US bond market. This too is what has prompted many analysts and money managers to suggest the equity markets are long overdue for a correction; however, the inflation story is what is retarding the earlier notion of an all but certain rise in interest rates. Minutes from the US Federal Reserve’s most recent April meeting even revealed that inflation expectations still remain relatively low for the remainder of 2014, and markets were left indecisive as to whether policy will return to normal perhaps sooner than later.

To make matters even more complex, New York Fed District President William Dudley (who may be one of the more recognized voting members amongst the FOMC) suggested this past week that the Fed keeps their 4.3 trillion dollar balance sheet status quo (see chart below). Quantitative easing was accomplished by expanding the Fed’s balance sheet to purchase Mortgage backed securities and treasury bonds. As these debt instruments mature, instead of removing the proceeds from the Fed’s balance sheet, Dudley suggests they reinvest in what is still a struggling mortgage market. Thus, the question of the long term implications or consequences of an inflated Federal Reserve balance sheet hangs over financial markets.

Famed bond investors have grabbed headlines over the last year for the comments on the end of the bull market in bonds. Most memorable was a tweet from Bill Gross of PIMCO, which read, “The secular 30-yr bull market in bonds likely ended 4/29/2013…” The misconception might have been that bonds were now entering a bear market as the economy springs back to life, but this leaves out another scenario, and perhaps the one currently playing out. And that is that interest rates are at historical lows, but they will remain at historical lows for some time. There is no question that is what a country like Canada has seen, when our 10 year yields recently touched a level not seen since June of last year. Furthermore, maybe some of the forecasts for 2014 like an 85 cent Canadian dollar, 3 percent GDP growth in the US, or US investment banks calling for $1,000 gold prices have to be rethought.

All investments contain risks and may lose value. This material is the opinion of its author(s) and is not the opinion of Border Gold Corp. This material is shared for informational purposes only. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. Border Gold Corp. (BGC) is a privately owned company located near Vancouver, BC. ©2012, BGC.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair