Bonds & Interest Rates

One of the men who runs the Federal Reserve System is worried about the potential effects of the central bank’s own policies, which involves printing more money.

One of the men who runs the Federal Reserve System is worried about the potential effects of the central bank’s own policies, which involves printing more money.

Philadelphia Federal Reserve President Charles Plosser also acknowledged that he and his colleagues don’t understand all the policies’ effects.

“Well I am very worried about the potential for unintended consequences of all this action,” Plosser said on CNBC’s Squakbox program. The action Plosser was referring to is quantitative easing, the Federal Reserve’s attempt to simulate the economy by buying $65 billion worth of bonds each month.

Some observers believe QE is what is driving the stock market to new highs. There also are those who think a stock market crash and an economic downturn will result when QE ends.

Plosser thinks that the economy is recovering but that the effects of quantitative easing could threaten that recovery. Quantitative easing is supposed to stimulate the economy by keeping interest rates low. Keeping interest rates low encourages lending and economic activity. Critics have called it printing money and easy money.

full article HERE

Nothing to report from Wall Street. Dow down a little yesterday. Gold up a little. The most telling stories are coming from the world economy, not its manipulated markets.

The price of copper is collapsing. The Baltic Dry Index is dragging along the bottom. Seven years after the start of the debt crisis the global economy is still struggling.

Hedge-fund-turned-family-office-manger George Soros says Europe could be in for a 25-year slump. Bloomberg reports:

Billionaire investor George Soros said Europe faces 25 years of Japanese-style stagnation unless politicians pursue further integration of the currency bloc and change policies that have discouraged banks from lending.

Europe “may not survive 25 years of stagnation,” Soros said in the interview with Francine Lacqua.

It was in the spring of 2007 that the first crack appeared in the weakest part of the debt structure: US subprime mortgages. By March 2007 the value of subprime mortgages had risen to $1.3 trillion. But mortgage rates were rising. Defaults and foreclosures followed.

The following autumn, the rate of subprime mortgage delinquencies had tripled from the year before. By January 2008, it had quadrupled. And by May it had quintupled.

It was a classic debt deflation. Homeowners had taken on more debt than they could afford. Now, the debt was going bad and investors were getting queasy.

Defaults were bad news for marginal homeowners. They lost their houses. They had to move.

They were bad news to the people who owned the mortgages, too. Wall Street had sliced and diced America’s mortgage deluge and sold it all over the world in the form of mortgage-backed securities – structured products that cleverly concealed, with the tacit backing of the ratings agencies, the junk hidden beneath the surface.

Sellers, too, seemed to forget what was in this sausage; they didn’t realize it was about to make them throw up.

First, Bear Stearns ran from the room, holding its stomach. Then it was Lehman Brothers. At that point, the feds came in with every quack cure they could think of. Bailouts, cash for clunkers, ZIRP, QE – one estimate put the total cost at more than $10 trillion, or about three times the cost of World War II.

The problem with the cures was always a fundamental one. The crisis was caused by too much debt. And all the feds had to offer was… more debt. As Bloomberg reported last week, the world’s stock of toxic sausages has exploded to $100 trillion:

The amount of debt globally has soared more than 40% to $100 trillion since the first signs of the financial crisis, as governments borrowed to pull their economies out of recession and companies took advantage of record low interest rates.

The jump in debt as measured by the Basel, Switzerland-based BIS in its quarterly review is almost twice the US economy.

Stopping the Future

Debt is an obligation laid upon the future by the past. The larger it gets, the harder it is for the future to happen.

There is a correlation between extreme levels of public debt and low economic growth. This has been demonstrated by several studies, most prominently by professors Rogoff and Reinhart. There were some errors in their math, which critics rejoiced in, but the conclusion was solid: High levels of debt-to-GDP have been historically associated with low levels of economic growth.

That is what has been happening in Japan for the last 23 years… and in Europe and the US for the last seven. These economies are still fighting deleveraging, resisting debt deflation and pretending that they can continue to add debt forever… and that somehow this will get them out of their debt traps.

But they are doomed. Without growth they can’t pay the debt. With so much debt, they can’t grow.

Regards,

Bill

These Two “C”s

Will Send Gold Higher

From the desk of Chris Hunter, Editor-in-Chief, Bonner & Partners

Two “C”s threaten widespread market instability: Crimea and China

Let’s look at each one… and why both are bullish for our favorite metal, gold.

Russian forces remain in Crimea, against international law. The government in Kiev is raising a 600,000-strong national guard to buttress its defenses against the Russians. A referendum will be held in Crimea on Sunday to determine whether the autonomous region should become part of Russia. The government in Kiev does not recognize the referendum.

The West is ratcheting up the economic tension. German chancellor Angela Merkel, who is usually relatively quiet on foreign affairs, has warned that Russia faces “massive damage” economically and politically, if it doesn’t back down over Crimea.

Meanwhile, China has gone from being the “engine of global growth” to the locus of concern over a global slowdown.

Chinese exports have collapsed 18% from a year earlier (versus expectations of a 7.5% increase). Chinese GDP growth is slowing. And there are concerns that bond defaults in the Chinese corporate sector may trigger a Chinese credit crunch.

It’s also quickly becoming clear that currency devaluation in Japan to boost exports is a zero-sum game. Japan can steal business from China and Korea, but this just prompts retaliation.

This is the “currency war” scenario many have feared Global QE would trigger. If the US and Japan are devaluing their currencies, it forces competitors to respond in kind… or lose critical export business.

Against this backdrop of uncertainty, it’s no wonder gold has been in rally mode in 2014.

Gold is not just a hedge against fiat currency debasement. It is also “disaster insurance” – a tangible asset with no counterparty risk investors seek out when return of capital, instead of return of capital, becomes a priority.

As you can see from the chart above, the spot gold price just broke above its recent October 2013 high. A break to the upside like this signals higher prices ahead.

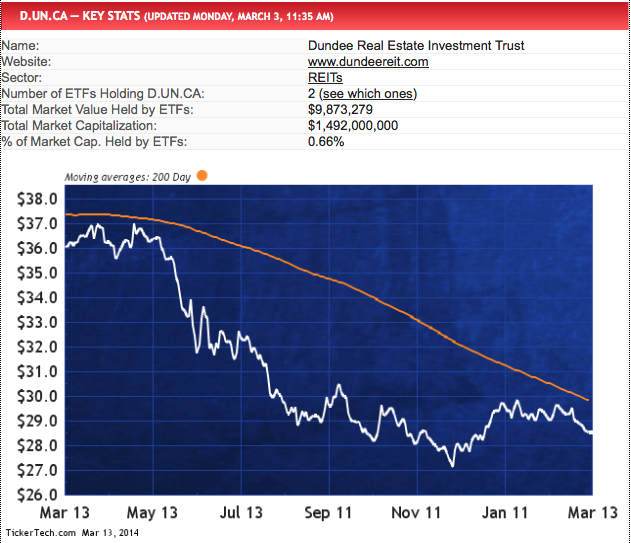

Yielding from 4.8% – 8.7% these 10 mostly Real Estate Investment Trusts. So if you are in need of income and a fan of Real Estate, this collection of investments sought out by the Canada Stock Research Staff are something to take a look at in an environment where you can barely get any return at all on money sitting in a savings account. As you can see the first example is selling significanly cheaper (thus yielding more) than it was a year ago – Editor Money Talks

(1) Dundee Real Estate Investment Trust (TSE:D.UN.CA) — 7.8% YIELD

Dundee Real Estate Investment Trust is an open-ended investment trust. The trust is engaged in the provision of business premises and management services to its tenants and other businesses in Canada. As of Dec 31 2010, Co. owned a diversified portfolio of 111 office and industrial properties offering approx. 12,300,000 sq. ft. of gross leasable area.

![]()

Everyone agrees that the winter just now winding down (hopefully) has been brutal for most Americans. And while it’s easy to conclude that the Polar Vortex has been responsible for an excess of school shutdowns and ice related traffic snarls, it’s much harder to conclude that it’s responsible for the economic vortex that appears to have swallowed the American economy over the past three months. But this hasn’t stopped economists, Fed officials, and media analysts from making this unequivocal assertion. In reality the weather is not what’s ailing us. It’s just the latest straw being grasped at by those who believe that the phony recovery engineered by the Fed is real and lasting. The April thaw is not far off. Unfortunately the economy is likely to stay frozen for some time to come.

Everyone agrees that the winter just now winding down (hopefully) has been brutal for most Americans. And while it’s easy to conclude that the Polar Vortex has been responsible for an excess of school shutdowns and ice related traffic snarls, it’s much harder to conclude that it’s responsible for the economic vortex that appears to have swallowed the American economy over the past three months. But this hasn’t stopped economists, Fed officials, and media analysts from making this unequivocal assertion. In reality the weather is not what’s ailing us. It’s just the latest straw being grasped at by those who believe that the phony recovery engineered by the Fed is real and lasting. The April thaw is not far off. Unfortunately the economy is likely to stay frozen for some time to come.

Over the past few weeks, I have seen just about every weak piece of economic news being blamed on the weather. First it was lackluster retail sales that were chalked up to consumers being unable or unwilling to make it to the mall. (This managed to ignore the fact that online sales were similarly weak – which would be unexpected for a nation of snowed in consumers). Then came the weak auto sales that were ascribed to similarly holed up potential car buyers. However, this ignores that while GM and Chrysler sales were way down, sales for luxury cars like BMW, Mercedes and Maserati, surged to record high levels (more on that later). No one offered a reason why wealthier motorists were able to brave the cold. A number of other data points, such as lower GDP, productivity, ISM and factory orders were also ascribed to the elements.

Analysts also blamed the weather for weak housing sales and mortgage applications, which both hit multi-year lows. The idea being that hibernating buyers could not get to real estate open houses or to the bank to process loans. This idea ignores the fact that the weakest home sales over the last few months have come from the states west of the Rockies, where temperatures have been above average.

Of course the biggest weakness ascribed to the snow and ice has been the very disappointing employment reports over the last few months. Analysts faced a very difficult task in squaring these reports, which showed fewer than 187,000 new jobs created in December and January combined, with the accepted narrative that the recovery was firmly underway and that the economy was no longer dependent on the Fed’s monetary support.

For these desperate economists the weather was a godsend. Mark Zandi had virtually guaranteed that job creation was being deferred by the weather and that hiring would come roaring back once the mercury started rising. The weather has become such a handy and versatile tool for economic apologists that we may expect that financial news stations will start featuring meteorologists more heavily than financial analysts. Move over Jim Cramer, hello Al Roker.

The weather continued to be horrible in February and as a result, there were wide expectations that today’s February jobs report would be similarly bleak. But this morning’s release detailed a slightly better than expected 175,000 new jobs, thereby convincing economists that the economy was so strong that it is overcoming the drag created by the weather. This lays aside the fact that 175,000 jobs should not be causing any optimism. After years of sub-par job growth, I believe a recovering economy would be expected to create more than 300,000 jobs per month in order to make a real dent in underemployment. Those levels, once routine in past decades, seem untouchable today. But weather-related pessimism had caused economist to ratchet down their predictions to just 150,000 jobs in February. Based on that, today’s numbers were seen as a win.

But economists are ignoring the likelihood that the weather was never a major factor. Take the cold out of the equation and you would be left with a mediocre February number following two consecutive monthly disasters. This does not change the downward trajectory. In fact, the number may be revised lower in future months, as has been the norm in the years since the economic crisis began.

Drilling deeper into the report will provide little reason for optimism. The labor force participation rate stayed at a generational low and the unemployment rate edged up. On the other hand, the long-term unemployed (those out of work for more than 27 weeks) increased by 203,000 to 3.8 million. Furthermore, over half of the jobs created were low-paying or part-time jobs in education, health care, leisure and hospitality, government, and temporary services. Higher paying information jobs declined by another 16,000 following last month’s 8,000 loss, and manufacturing added a scant 6,000 jobs.

The report also contained data that shows how older workers are coming out of, or postponing retirement. This trend is likely caused by inadequate savings rates, low interest rates, and increases in the cost of living that are rising faster than official CPI numbers. Not only does this point to falling living standards, but the jobs being taken by these older workers would normally be filled by younger, less skilled workers, who are left unemployed, buried beneath a pile of student debt and living in their parent’s basements.

In truth, economic activity persists in good weather and bad. Winter is largely predictable. It comes around once a year, basically on schedule. Consumers are used to the patterns and know how to deal with them. But don’t tell this to today’s economists.

A much more plausible explanation to me is that the economy has been weak recently because it is weak fundamentally. The data deterioration corresponds not just to unseasonably low temperatures but also to the diminishment of monthly QE from the Federal Reserve. If you recall the highly anticipated “taper” finally began in mid- December. From my perspective the Quantitative Easing has become the sunshine that drives our phony economy. Diminish that sunshine and the economic winter spreads.

But the sad fact is that QE can push up prices in stocks and real estate, but can do very little to affect positive change in the real economy. That’s why I believe that BMW’s are selling like hotcakes even as Chevies sit on the lot. Our current policies help the wealthy at the expense of everybody else. Unfortunately, I don’t think the economy will improve as long as the QE keeps us locked into a failing model. What’s worse, once the weather warms and the economy does not, look for Janet Yellen to first taper the taper, then to reverse the process completely.

Subscribe to Euro Pacific’s Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

To order your copy of Peter Schiff’s latest book, How an Economy Grows and Why It Crashes – Collector’s Edition, click here.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

Nihilo ex nihilo fit. Out of nothing, nothing comes. First put forward by ancient Greek philosopher Parmenides in the 5th century BC, Thomas Aquinas and St. Augustine later used this axiom to prove that the universe needed a “first mover,” to get things going.

Even if the whole thing began with some kind of “Big Bang” moment, it still needed a banger to bang it.

Who? God, of course.

We don’t know. But our jaw dropped when we saw how the bangers over at the Federal Reserve have helped add $20 trillion in US household wealth since 2009 – setting yet another new record. The Wall Street Journal reports:

American’s wealth hit the highest level ever last year, according to data released Thursday, reflecting a surge in the value of stocks and homes that has boosted the most affluent US households.

Ex nihilo? Who cares. It’s there. It’s spendable.

And yet… what kind of wealth comes from nothing? Is it solid and real, like the earth, the moon and the stars? Or is it something else?

It is clearly something else. But what?

The Great Fed Wealth Transfer

Let’s begin by looking at where all that new wealth comes from. Not from the hand of the Almighty, of course…

We are led to believe that the Fed’s policies are designed to produce a general prosperity; the Fed keeps rates near zero so the entire economy benefits.

But it isn’t true. Only some prosper. Even the headline in the WSJ says so: “US Wealth Rises, But Not All Benefit.”

The Fed’s activist policies distort and corrupt the economy. First, prices are bent. Then, taking their cues from bad prices, bad decisions are made. Before you know it, everything is twisted in one direction or another.

As we noted on Friday, the Fed is largely to blame for the dinosaur houses we see all over the US. Low rates and rising prices tricked Americans into believing that the more house you had the more money you would make.

We didn’t mention it last week, but factories in China can also trace their genesis to the Fed’s low-down interest-rate policy. Americans were lured to borrow and spend; Chinese manufacturers benefited.

Record high earnings, record high margin accounts, record high junk bond issuance, record household wealth gains – all are products of Fed policies.

We quote from the book Paper Money Collapse: The Folly of Elastic Money and the Coming Monetary Breakdown. The author, Austrian School economist and former Wall Streeter Detlev Schlichter, was kind enough to send us an advance copy. Says Schlichter,

[The financial authorities] can never enhance all economic activity evenly or‘stimulate‘ the economy in some all-encompassing, general way. Every injection of new money must lead to changes in resource used, to a redirection of economic activity from some areas to others, and change income and wealth distribution. Inflows of new money inevitably change the economy and must create winners and losers.

That $20 trillion in new wealth I alluded to earlier is in the hands of America’s winners. It added little to US GDP… or to Americans’ incomes. It was merely a transfer of wealth. Owners of stocks and houses got richer. Wage earners and savers got poorer.

Take Your Money off the Table

We have some advice for those on the receiving end of the stock market bonanza: Take your money off the table before it disappears.

After all, it is only a claim on wealth, not wealth itself. And that claim will expire worthless when the Fed changes its policies. The Fed giveth, and the Fed taketh away.

Either the Fed will taper… ending the bonanza. Or it will lose control of interest rates. And when they rise, all the broken records we have been citing become like broken bottles in a street fight. Somebody is gonna get hurt.

For the moment, the 12 members of the policy-setting Federal Open Market Committee are more powerful than God. Since the beginning of the universe, it took about 13,798,000,000 years for the market value of all the world’s assets to reach $20 trillion. The Fed’s “Big Bang” accomplished the same trick in only six years – start to finish.

That does it for us. No more worshipping a guy who has been dead for 2,000 years… or his dad, for that matter. In this Lenten Season, we bow to no man. But for the lady who runs the Fed, the entire economy bends in whatever direction She commands.

Regards,

Bill

From the desk of Chris Hunter, Editor-in-Chief, Bonner & Partners

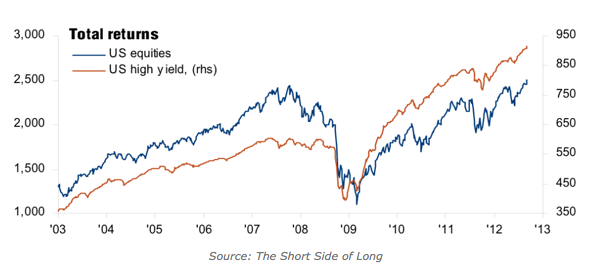

Another effect of the Fed-driven economy is something Bill alluded to last week: the big rally in high-yield, or “junk,” corporate bonds.

Over the last 10 years the high-yield bond market has returned 131%. This compares to a return of 69% for investment-grade corporate bonds.

In fact, as you can see from the chart below, junk bonds have been more or less in line the US equities since 2003.

And with the Fed now leaning heavily on Treasury bond yields, fresh funds are pouring into the high-yield bond sector.

According to data from Lipper, $559 million flowed into high-yield funds and ETFs for the week ending February 26. That came hot on the heels of $804 million in inflows in the previous week… and $1.45 billion the week before that.

All that money is chasing an average “junk” yield of just over 5% – or about two percentage points over the benchmark 10-year T-note yield of 2.79%.

This big influx of money into the junk-bond market is happening at the same time as corporate default rates are on the rise. Ratings agency Standard & Poor’s estimates a 2.5% default rate by the end of this year – up from a default rate of 1.7% at writing.

That’s not extreme (the long-run average is about 4.5%), but the direction of travel is a concern.

And just like the rally in US stocks, the rally in junk bonds is heavily dependent on the Fed keeping Treasury yields low. After all, it’s the lack of yields available on relatively safe government bonds (by historic standards at least) that is pushing so many investors out on the risk spectrum in search of yield in the junk-bond market.

Junk bonds are a popular trade right now. But just like US stocks, much of the easy money has already been made. And a 5% yield, from our perch at least, is poor compensation for the risks involved.

Think twice before you join the crowd pouring money into junk bonds. Mom and Pop are big buyers. And just like stocks, this is a highly distorted market… and therefore unsuitable for prudent investors.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair