Bonds & Interest Rates

It might have gone against the conventional wisdom to see the markets trade higher on the basis that the US Federal Reserve will begin, come January, to be less accommodative to the US economy, but it’s not exactly as if the markets have had a perfectly rational last few years. Amidst one of the shakiest recoveries from the greatest recession to plague the US economy since the Great Depression, we continue to see equity markets trader higher as all the disbelievers missed out on the seventh greatest annualized gain in the American stock markets since World War II. No question, it was the US Federal Reserve’s influence on long term borrowing rates that bestowed confidence in American consumers, and nonetheless fueled this American recovery, but as the Fed begins to adapt their stimulus measures to adequately reflect the necessities of this continued recovery, we can be certain the party’s not over yet.

Ben Bernanke, in his final press conference as the Chairman of the US Federal Reserve, assured investors of one thing, and that was that the Fed will continue to adapt to the needs of the economy. And just as easily as they could trim asset purchases by 10 billion a month equally split between Treasury bonds and mortgage back securities, they could increase by 10 billion as well. But as we at Border Gold have argued in past newsletters, the taper of the fed’s asset purchases was very much an inevitable occurrence; moreover, it is absolutely not to be confused with the end of an era of easy money policies in the months and years to come.

Ben Bernanke, in his final press conference as the Chairman of the US Federal Reserve, assured investors of one thing, and that was that the Fed will continue to adapt to the needs of the economy. And just as easily as they could trim asset purchases by 10 billion a month equally split between Treasury bonds and mortgage back securities, they could increase by 10 billion as well. But as we at Border Gold have argued in past newsletters, the taper of the fed’s asset purchases was very much an inevitable occurrence; moreover, it is absolutely not to be confused with the end of an era of easy money policies in the months and years to come.

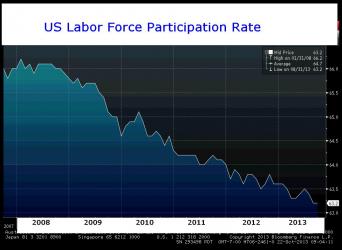

And as the easy money policies will continue the biggest influence on the market will be near zero short term interest rates, controlled by the Federal Funds Rate. Offered in the form of forward guidance, Bernanke made clear in his policy statement that rates will remain low “well past the time that the unemployment rate declines below 6-1/2 percent.” And that low of emergency level interest rates will be the fuel to the fire for the markets. It makes sense for the stock markets to be able to trade higher, almost in relief to the fact the world’s largest economy is no longer so desperately in need of such extraordinary stimulus. But it is the caveat that the highly accommodative economic environment will remain in place.

As the Berkley Economist Barry Eichengreen phrases it, a reduction “by $10bn a month is best dismissed as a taper in a teapot… $10bn of monthly security purchases are a drop in the bucket for a central bank with a $4tn balance sheet.” And in fact, by Bernanke beginning the taper, he began the very seamless hand off to Janet Yellen to fulfill the role of an accommodative central banker. This is as the markets can now digest the milestone that a measure once dubbed “QE Infinity” has the possibility of coming to an end.

***

A Note on Gold:

Following what was a supposed short covering rally with the rest of the market given the Fed’s decision to taper, gold immediately sold off heading for that June low of 1180 US/oz. Thursdays close on the Comex, below 1200 US/oz. was the yellow metals lowest in three years’ time. From a technical stand 1180 stands out as an important number, but as this market faces tax loss selling pressure going into year end precious metal markets are giving an indication that they are in the process of forming a bottom in Q1 of 2014.

The Consumer Price Index (CPI) rose 0.9% in the 12 months to November, following a 0.7% increase in October. November marked the 7th time in the last 13 months in which the CPI increased less than 1.0% on a year-over-year basis.

Canadian dollar futures traded below 93.00 briefly but have since recovered to 93.30.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 –

604 664 2666 – Fax

800 810 7022 – Toll Free

Japan’s central bank held its massive monetary expansion unchanged on Friday, and played down chances of the need for an extra dose next year as it took heart from the U.S. Federal Reserve’s decision to begin tapering its own mega-stimulus.

Speaking after a Bank of Japan policy-setting meeting, Governor Haruhiko Kuroda welcomed the Fed’s move as a sign that the U.S. economy is recovering steadily, which bodes well for global growth and Japan.

The widening interest rate gap between Japan and the United States, as the BOJ maintains its ultra-easy policy while the Fed winds down its stimulus, is likely to keep the yen weak against the dollar, analysts say.

The dollar hit a fresh five-year high of 104.59 yen on Friday, extending the weak-yen trend that has helped Japan’s export-reliant economy emerge from stagnation.

…full article HERE

While the Fed’s decision to taper back its monthly asset purchase program to $75 billion has received a lot of attention, many have overlooked the news out of China.

The seven-day repurchase rate was up to a six-month high of 7.6% in Shanghai on Friday. It closed at 7.06% on Thursday. The People’s Bank of China [PBoC] injected money through short-term liquidity operations on Thursday.

We already saw a severe credit crunch in China back in June, and some are worried that we’re going to see a repeat of that.

Hedge fund manager Jim Chanos described this week’s run up in money market rates as “a bit of a banking crisis,” in a CNBC interview.

Read more: http://www.businessinsider.com/chinese-interest-rates-are-spiking-again-2013-12#ixzz2o0jVR5MD

With all the excitement over the Fed’s Taper of QE3 yesterday, it is beginning to dawn on bond market investors that someone will need to come in and pick up the slack in demand caused by the Taper. In January, there will be $5 billion in Treasury bonds and $5 billion in mortgage-backed bonds that would be normally scooped up by the Fed that will need to find a buyer.

When the Fed began QE3, Treasury bonds were on the cusp of entering a secular bear market after enjoying a secular bull market for the previous three decades (see the charts above). However, because it was early (and because investors weren’t listening to our warnings!), investors were still piling into bonds and bond mutual funds. It was hard to break a habit that had been so fruitful for 30 years.

As a result, at the beginning of QE3, the Fed was essentially “crowding out” relatively enthusiastic bond buyers.

Now, 16 months after the Fed starting buying mortgage-backed bonds and 12 months after the Fed started buying longer-term Treasuries, investors are transitioning out of these areas and into equities and other higher-yielding investments. Besides being lured by better returns elsewhere, who wants to buy a 10-year Treasury and get hammered as market rates really only have one way to go?

The bond market vigilantes have already begun to make an appearance, selling longer-dated bonds this morning rather than holding on to them into January when it might require an even higher yield to entice very reluctant investors to soak up the $10 billion in excess supply.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair