Bonds & Interest Rates

….versus the Bernanke “Put”

….versus the Bernanke “Put”

If the Janet Yellen testimony before the Senate Banking Committee this week illustrated anything, it is that the transition from Ben Bernanke to the incoming chair of the US Federal Reserve will be seamless. It is the typical story of the US Federal Reserve being dependent on the data driven recovery of the US economy that will affect their asset tapering decisions. Unfortunately though, it has become a distraction as to shift investor’s concentrations away from the perils of unproductive fiscal policy (at any level of government) and instead focus on the financial markets, which for the sixth consecutive week saw the S&P 500 and Dow Jones trade higher.

The unfortunate realization or perhaps lack of realization is that central banks, led by the US Federal Reserve, will continue to be the only game in town, and that was the message Janet Yellen implicitly provided last Thursday. US economic growth sits at that inflection point of around 2 percent where we will still wait to see whether the economy is ready to reach former Bank of Canada and current Bank of England Governor Mark Carney’s coined term “escape velocity.”

But the biggest reason that the credit easing policies will continue is because of the lackluster inflation levels seen all around the world. Until inflation actually becomes a credible threat to the worlds developed economies, there is no pressure on central banks to begin tightening their policies, or even talk about it. This is especially true given the average inflation rate in the OECD developed countries has fallen from 2.2 percent in 2012 to 1.5 percent so far this year. And reports out of the European Union last week highlight that deflation was more of threat than inflation with October’s inflation numbers registering at .7 percent. That creates a major threat to the nations of Europe, where the risk of seeing prices decline will create yet another impediment to their recovery from a triple dip recession.

The other issue, however, with forecasted paltry inflation levels is what countries with low inflation are associated with, and that is persisting levels of high jobless rates and mediocre growth. For this reason alone, the world’s central banks continue their aggressive policies, but it does truly illustrate their positions between a rock and a hard place as any opportunity to spur or revitalize economic growth is jeopardized by an unwavering price level. As Mohammad El-Erian argues, central bankers in today’s world are only destined to fail because our expectations for what they can deliver is far too inconceivable, given the “the much-sought-after trifecta of greater financial stability, faster economic growth, and more buoyant job creation.”

So it is not so much that there is a responsibility among the central bankers to instill the prior mentioned trifecta of economic goals, it is rather the shortfall of elected policy makers that force us to rely on the independent institution of a central bank. And just as it was the “Greenspan Put” beginning in the early 2000’s that saw the Federal Funds Rate drop every time the economy hit a speed bump to the “Bernanke Put,” which commenced the greatest era of manipulation of the Federal Reserve’s balance sheet in order to stimulate the economy, investors now eagerly await what will be the “Yellen Put.” Whether its offered forward guidance of low interest rates into the unknown future, or perhaps quantitative easing continuing longer than anticipated, one thing is certain, and that is for this economic recovery to continue central bankers are still needed more desperately than ever.

More Articles from Robert Levy HERE

Yesterday during her Senate confirmation hearings, Janet Yellen, the presumptive next Chairman of the U.S. Federal Reserve, was quoted saying: “There is limited evidence of reach for yield.” I can only assume that Dr. Yellen does not have access to a Bloomberg machine, or is not following the markets, or is not reading my blog comments and tweets! (https://twitter.com/McIverWealth)

In order to assist Dr. Yellen, I will take the opportunity to present a number of pieces of evidence that she has apparently missed.

1.The popularity of Rwandan government bonds is evidence of a reach for yield. Because investors have suffered from interest rate suppression, they have had to venture far and wide to find ways to supplement yield. They have even ventured as far as “frontier markets” such as Rwanda! (That’s right, the agrarian country that is synonomous with savage ethnic cleaning that claimed 100,000s of lives in the 1990s). As the first chart above points out, investor enthusiasm is such that the Rwandan government 10-years are currently yielding a miserly 7.86% despite being a country that has seen explosive inflationary bursts over the past decade.

2.The popularity of U.S. Real-Estate Income Trusts (REITs) is evidence of a reach for yield. Although as a whole this sector was whipsawed a bit during the first utterance of Fed “Taper Talk” in May, it has largely held onto gains made over the past two years (see second chart above) as investors find it hard to ignore the yields.

3.The popularity of High Yield Bonds is evidence of a reach for yield. In fact, the higher yields from lower quality bonds have been so seductive, investors in these bonds have ignored the fact that the market for conventional safer bonds has been in a Bear Market since July 2012 (see third chart above).

I am a bit surprised that an ocean of Ph.D.’s at the Fed wasn’t enough to help Dr. Yellen with her talking points. However, if she is able to read some of the “tip of the iceberg” evidence about the “reach for yield” that I have presented here, she’ll be a little more prepared then next time she comments on the subject.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

U.S. manufacturing output rose for a third straight month in October even as automobile production fell, suggesting a broadening in activity in a sector regaining momentum after a slump early this year.

Other data on Friday showed factory activity fell in New York state early this month, but economists said that was probably a delayed reaction to last month’s 16-day partial shutdown of the federal government.

National manufacturing output increased 0.3 percent after edging up 0.1 percent in September, the Federal Reserve said. In the 12 months through October, factory production was up 3.3 percent, the fastest since December 2012.

The monthly increase, which matched economists’ expectations, was despite a 1.3 percent fall in auto production. Auto assembly fell for the first time since July.

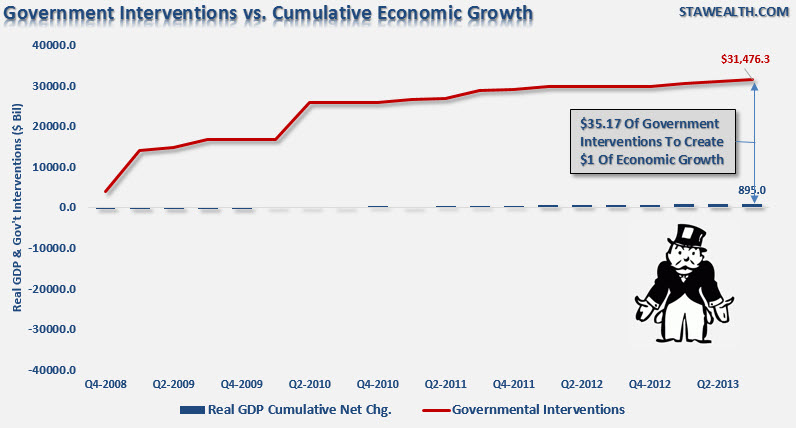

Despite Janet Yellen’s commitment to continue supporting the economic recovery the transmission system of government interventions is clearly broken. As STA Wealth Management’s Lance Robertss hows in the simple chart below, it has taken $35.17 of government intervention to generate $1 of economic growth over the past 5 years. More importantly, the rate of diminishing returns is increasing. In other words, it is taking consistently more dollars of intervention to create an incremental increase in economic growth.

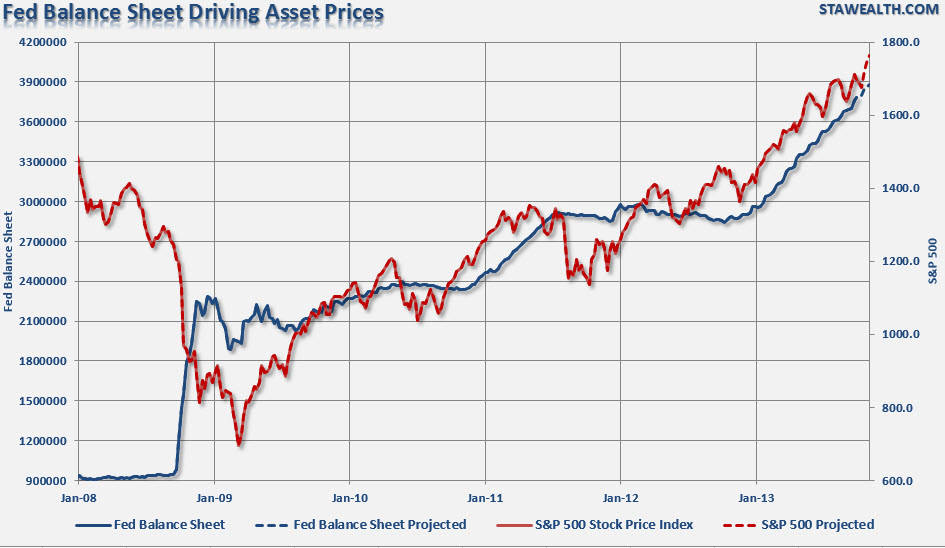

In the meantime, as shown below, the continued liquidity programs from the Federal Reserve continue to boost asset markets towards more exuberant levels.

However, despite signs of a potential market “bubble” Janet Yellen clearly sees no such thing…

More from ZeroHedge:

EU Citizenship Goes On Sale, Price War Breaks Out

Academic Insanity Costs You 2% Of You Purchasing Power Per Year

* Yellen’s Fed Chair nomination hearing in focus * U.S. to complete refunding with $16 bln 30-year bond sale * Fed to buy $2.75-$3.50 bln in medium-dated bonds By Richard Leong NEW YORK, Nov 14…….full article HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair