Bonds & Interest Rates

Although the Fed may realize (though I doubt it) that the current asset purchases have minimal impact on the real economy of the majority of American people, they probably think that continuous monetary stimulus is the lesser of two evils. This is a wrong assumption, in my opinion, because prices are rising far more than wages and salaries.

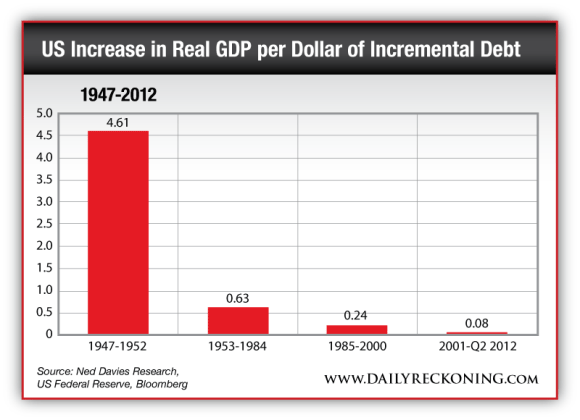

Moreover, the Fed wants to stimulate credit growth with its artificially low interest rates. But again, credit growth has largely lost its impact on the real economy. The multiplier on GDP of an additional dollar of debt is now negligible.

I suppose that the conclusion we can draw from it is that the larger the debt as a percentage of the economy becomes, the less will be the impact of an additional dollar of debt. I actually think that there is a tipping point where additional debt has a “contractionary” effect on the economy, because at this tipping point, the debt becomes so large that interest rates will increase no matter how much a central bank monetizes the debt. (Subsequently, inflation accelerates and the currency collapses, which leads, contrary to Mr. Bernanke’s view, to a general impoverishment of the population.)

But as I contended before, the probability that we have embarked on permanent asset purchases by the Fed is very high (until QE99 — or at least until the system breaks down, as just outlined).

Given my negative outlook for the global economy, I believe that 10-year Treasury note yields could decline once again to between 2.2-2.5%.

To Mr. Bernanke’s credit, and to be fair to him, I need to point out that his economic sophism is shared by most central bankers around the world. We can see that the global monetary base has exploded more than fourfold since 2003. These universally common monetary policies are, of course, applauded by fund managers, bankers and the investment community, all of which benefit (including myself) from rising asset prices. (Within 24 hours of the Fed’s announcement that there would be no “tapering,” the value of my assets increased by about 3%.)

But what is good for me as an asset holder doesn’t imply that it is the right monetary policy for the economy and for society as a whole. (Bill de Blasio’s policy of increasing taxes on high-income earners is a direct consequence of the growing wealth and income inequality brought about by expansionary monetary policies.)

For investors, the challenge is the following. Despite record buying of Treasuries and mortgage-backed securities, since September 2012, interest rates are up, not down. This proves clearly that the Fed is not all powerful.

Similarly, commodities and precious metals are still well below their peaks. The majority of stock markets around the world are well below their peaks, as are the majority of stocks in the U.S. In other words, it is not likely that the Fed and other central banks can boost further all asset prices, since this would require them to accelerate the expansion of the balance sheets ad infinitum.

The global monetary base expanded at 35% in 2009. Thereafter, its growth slowed to an annual rate of 10% in early 2012. The global monetary base expansion then re-accelerated to an annual rate of over 20% in late 2012. However, it has since slowed to an annual growth rate of around 5%. Simply put, even without tapering, there is a relative tightening of the turbocharged monetary expansion.

Above, I mentioned that the Fed has lost control of the bond market. Now let us consider two extreme cases of monetary policies: The Fed announces an immediate stop of its asset purchases (policy A), or it announces an immediate increase in its asset purchases to $200 billion monthly (policy B). How would the bond market react to these announcements, and what would the subsequent performance be? I suspect that on the announcement of policy A, the bond market would sell off for a day or two.

But then the bond buyers would figure out that no asset purchases by the Fed would likely be somewhat deflationary and, therefore, beneficial for bonds. The announcement of policy B would likely lead to an immediate bounce in bond prices (though likely not a new high) and likely not to a new low in interest rates. In fact, I would assume that if the Fed’s and other central banks’ balance sheets were to expand forever at a rapid pace, the bond market would tank.

…even without tapering, there is a relative tightening of the turbocharged monetary expansion.

For what it’s worth, when yields on the 10-year U.S Treasury note rose toward 3% I bought some of the notes. Sentiment was extremely bearish (small traders were heavily short the bond market) and I thought that “tapering” (I expected $10-15 per month) would be favorable for the bond market. I was wrong in my assumption, but right about buying the notes, since they rallied subsequently. That’s the confusing world of investments we live in. Given my negative outlook for the global economy, I believe that 10-year Treasury note yields could decline once again to between 2.2-2.5%.

However, longer term, I remain bearish about bonds. Yet there is one point we need to consider. Is it wise to sell U.S. bonds of America? Its “Bank of America, Merrill Lynch (BofAML) private client flow data” shows a complete aversion to bonds and a strong appetite for equities.

According to BofAML’s chief investment strategist, in the week ended Sept. 11, 2013, private investors put $14.3 billion into equity mutual funds and withdrew $3.5 billion out of bonds. (It was the largest weekly move out of bonds in the last three years.) I am raising this question because, based on current U.S. stock valuations, the future returns will be relatively small.

According to Robert Shiller’s current P/E ratio, the five-year expected return will be 4% and the 10-year return just 1%. In the near term, I was also concerned that stocks had become extremely overbought following the strong rebound from their late August low, and that the current advance had not been confirmed by numerous technical indicators. From the Aug. 28 low at 1,627, the S&P 500 rose in a straight line to 1,729 on Sept. 29 (by 6.3% in three weeks, or by more than 100% when annualized).

As a reminder, the S&P 500 is also up 61% from its Oct. 7, 2011, low at 1,074 (two years). So I can understand why the phones are ringing at BofAML’s retail offices from clients who want to switch their funds out of bonds into equities. But this doesn’t imply that equities are a good value at present.

I want readers to perfectly understand that when I recently bought my Treasury notes yielding over 2.9%, I didn’t think they were of particularly good value either. But within my asset allocation of 25% of total assets in emerging market bonds and cash, I held a lot of dollar cash, which was in the banking system and yielding next to zero. So by moving some cash into 10-year Treasury notes, I gained some additional income and a higher level of security (at least for now) as compared with holding bank deposits.

I should also mention that according to Shiller’s current P/E ratio, the five-year expected return for emerging market equities will be 19% and the 10-year return 13.8%. I have to say that I consider these emerging market return expectations to be completely unrealistic. Given my negative outlook about the Chinese economy, which I have outlined in earlier reports, I think that emerging markets’ returns could be as low as zero (or even less) for the next few years.

As James Burgh, a British Whig politician who stood up for “free speech” (1714-75), observed: “In prosperity, prepare for a change; in adversity, hope for one.”

Faber: The Feds Next Move To $1 Trillion

Marc Faber, publisher of The Gloom, Boom & Doom Report, told CNBC on Monday that investors are asking the wrong question about when the Federal Reserve will taper its massive bond-buying program. They should be asking when the central bank will be increasing it, he argued.

“The question is not tapering. The question is at what point will they increase the asset purchases to say $150 [billion] , $200 [billion], a trillion dollars a month,” Faber said in a “ Squawk Box ” interview.

The Fed-which is currently buying $85 billion worth of bonds every month-will hold its October meeting next week to deliberate the future of its asset purchases known as quantitative easing .

(Read more: Treasury yields will still spike to 5%: Societe Generale )

Faber has been predicting so-called “QE infinity” because “every government programthat is introduced under urgency and as a temporary measure is always permanent.” He also said, “The Fed has boxed itself into a position where there is no exit strategy.”

The continuation of Fed bond-buying has helped support stocks, and the Dow Jones Industrial Average (Dow Jones Global Indexes: .DJI) and S&P 500 Index (^GSPC) are coming off two straight weeks of gains, highlighted by record highs for the S&P.

While there may be little inflation in the U.S., Faber said there’s been incredible asset inflation. “We are the bubble. We have a colossal asset bubble in the world [and] a leverage or a debt bubble.”

Back in April 2012, Faber said the world will face “massive wealth destruction” in which “well to-do people will lose up to 50 percent of their total wealth.”

In Monday’s “Squawk” appearance, he said that could still happen but possibly from higher levels because of the “asset bubble” caused by the Fed.

“One day this asset inflation will lead to a deflationary collapse one way or the other. We don’t know yet what will cause it,” he said.

More from Marc: Bond Burglars to Bring Bears Out of Hibernation

Former Federal Reserve Chairman Alan Greenspan said the stock market has room to rise from record levels.

Former Federal Reserve Chairman Alan Greenspan said the stock market has room to rise from record levels.

“In a sense, we are actually at relatively low stock prices,” Greenspan, who guided the central bank for more than 18 years, said in an interview with Sara Eisen on Bloomberg Television today. “So-called equity premiums are still at a very high level, and that means that the momentum of the market is still ultimately up.”

Greenspan said the stock market is “just barely above 2007” and the average annual increase in stock prices “throughout the postwar period” is 7 percent, which leaves room for a rise.

“Price-earnings ratios are not hugely up,” he said. The market has “gone up a huge amount, but it’s not bubbly,” according to Greenspan.

Ed Note: Mike Shedlock has put together a thorough analysis of Alan Greenspans forcasting record. Here is a short summary:

Succinct Historical Synopsis

- In 1973 Greenspan said “There is no reason to be anything but bullish now” – The market topped that month, then crashed

- In 1996 Greenspan warned of “Irrational exuberance” – The market, fueled by Greenspan’s incompetent actions roared for four years

- In 1999 Greenspan was extremely worried about Y2K – The programming rollout on January 1, 2000 was exceptionally smooth

- In 2000 Greenspan fully embraced the internet productivity miracle – The dotcom bust soon began

- In 2001 Fed minutes show Greenspan was worried about inflation – A month later the Fed was fighting deflation

- In 2006 Greenspan said “Housing Prices Won’t Fall Nationally” – Prices peaked summer of 2005, then crashed over the next seven years

Today Greenspan Says

- “In a sense, we are actually at relatively low stock prices”

- “The momentum of the market is still ultimately up.”

- “The market has gone up a huge amount, but it’s not bubbly.”

The full analysis can be read HERE

We really can’t forecast all that well. We pretend that we can but we can’t. And markets do really weird things sometimes because they react to the way people behave, and sometimes people are a little screwy.

“Jobs Report Leaves Fed in Doubt,” was a big headline yesterday morning.

Later in the day came this:

“Dow down 54 on jobs concern.”

What is the Fed in doubt about? To taper, or not to taper, that is the question.

And why should a jobs report make any difference?

Oh, dear reader, where have you been? Don’t you know everyone now sits on the edge of his seat wondering when and how the Fed will back off from its massive QE program? And don’t you know the future of civilization hangs in the balance?

On that point, we have a position… a thought… a reaction. Civilization hangs in the balance, but not in the way you think.

We have been trying to introduce a new way of looking at civilization. In short, we’ve tried to make it more civilized.

What is the difference between a civilized community and a barbaric one? We have introduced a simple test. The civilized community relies mostly on cooperation and consent. The uncivilized community depends heavily on force and violence.

A French historian first introduced the word “civilization” less than 300 years ago. Since then there has been much argument about what it means. We enter the fray gingerly, but sure of ourselves. It only makes sense on our terms. A civilized community is peaceful; a barbaric one is not.

“Okay, Bill,” you may be saying to yourself. “I’ll give you that one… I guess. But what the hell difference does it make? What has it got to do with the jobs report?”

Good questions. Glad you asked.

We know from bitter experience that trying to force economies to do what you want is a thankless task. Markets are fundamentally based on free exchange, cooperation, trust and trade. Force them in one direction or another and you are just asking for trouble.

As Alan Greenspan described this week, in an interview with John Stewart on “The Daily Show,” people are a little “screwy” from time to time. Which means they don’t necessarily go along with your central planning, no matter how good you think it is.

But still economists insist that, if they are allowed to monkey around with it, they can make an economy better. This is occasionally true. Said occasion is usually when they have already messed it up. By withdrawing some of their planning and programs, they may allow it to recover.

Otherwise, there is no example in history where force has been successfully applied to economics.

But that doesn’t stop the PhDs from trying. The jobs report showed about 60,000 jobs missing – fewer jobs than economists had projected.

Now, the erring economists will most likely compound their error by continuing to try to force the economy to do their bidding – force up the rate of consumer price increases and force down the number of Americans out of work.

If they really wanted to increase employment, that would be easy enough. They would encourage the feds to withdraw some of the laws that bully employers (health insurance… EEOC threats… overtime, etc.)… or some of the schemes that make it easy for potential employees to remain unemployed (disability… unemployment benefits… food stamps). As far as we know, those things are not on the table.

What is on the table is more QE.

With regards to QE, the poles of possibility are as follows:

- QE does nothing important. If this were so, there would be no reason to keep it.

- QE is essential to the economy. If this were so, they couldn’t get rid of it… no matter what the jobs report says.

Most likely, QE lies somewhere in between… perhaps lost in the horse latitudes. It probably has little effect on the real economy. That is why the jobs report is so disappointing. But it probably has a great effect on the financial economy. That’s why the Dow sets new record highs almost every session.

The Fed is probably stuck with QE. Were it to stop, the stock market would likely tumble and the “wealth effect” the PhDs have been aiming for would quickly turn into a poverty effect.

Janet Yellen couldn’t stand it. She believes the Fed should use all its available weapons to force the economy to do what she wants it to do. She won’t be able to stand by, dagger in hand, when the market turns its back on her. Instead, she will stab.

And the Fed, which has lived by the sword of QE, will probably die by it too.

Regards,

![]()

Bill

Yesterday, the Labor Department reported that nonfarm payrolls (jobs) increased by 148,000 in September. Today’s chart provides some perspective in regards to the US job market. Note how the number of jobs steadily increased from 1961 to 2001 (top chart). During the last economic recovery (i.e. the end of 2001 to the end of 2007), job growth was unable to get back up to its long-term trend (first time since 1961). More recently, the number of nonfarm payrolls has been working its way higher but at a pace that is not fast enough to close the gap on its 1961 to 2001 trend. It is interesting to note that the current number of US jobs recently surpassed its 2001 peak. However, the job market has yet to reach the peak levels obtained back in early 2008.

Notes:

Where should you invest? The answer may surprise you. Find out right now with the exclusive & Barron’s recommended charts of Chart of the Day Plus.

Quote of the Day

“People who work sitting down get paid more than people who work standing up.” – Ogden Nash

Events of the Day

October 24, 2013 – United Nations Day

October 31, 2013 – Halloween

November 02, 2013 – Breeders’ Cup

November 03, 2013 – Daylight Saving Time ends (US) – New York Marathon

Stocks of the Day

— Find out which stocks investors are focused on with the most active stocks today.

— Which stocks are making big money? Find out with the biggest stock gainers today.

— What are the largest companies? Find out with the largest companies by market cap.

— Which stocks are the biggest dividend payers? Find out with the highest dividend paying stocks.

— You can also quickly review the performance, dividend yield and market capitalization for each of the Dow Jones Industrial Average Companies as well as for each of the S&P 500 Companies.

Mailing List Info

Chart of the Day is FREE to anyone who subscribes. Click HERE to subscribe

To ensure email delivery of Chart of the Day, add mailinglist@chartoftheday.com to your whitelist

The bank of Canada has decided to maintain the overnight lending rate at 1%. That was expected, they did however remove their slight hawkish bias and lower thier GDP expectations (added and highlighted below) in their statement.

In Canada, uncertain global and domestic economic conditions are delaying the pick-up in exports and business investment, leaving the level of economic activity lower than the Bank had been expecting. While household spending remains solid, slower growth of household credit and higher mortgage interest rates point to a gradual unwinding of household imbalances. The Bank expects that a better balance between domestic and foreign demand will be achieved over time and that growth will become more self-sustaining. Real GDP growth is projected to increase from 1.6%(was 1.8%) in 2013 to 2.3% (was 2.7%) in 2014 and 2.6% (was 2.7%) in 2015. The Bank expects that the economy will return gradually to full production capacity, around the end of 2015.

On this release the Canadian Dollar futures traded to $96.25, down over 0.75 on the day.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair