Bonds & Interest Rates

Stall Speed?

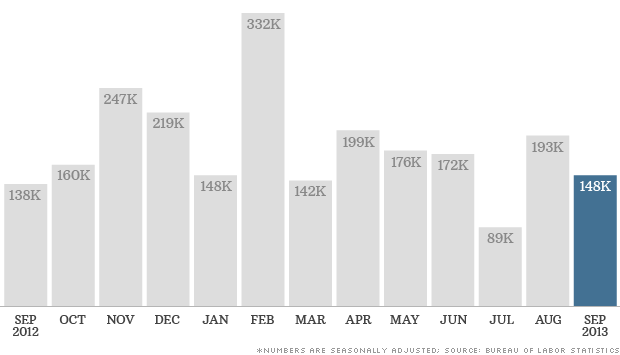

- The September unemployment report was released in the US yesterday and it was a mess

- 148,000 jobs were “created” and the unemployment rate ticked down to 7.2%

- The unemployment rate fell once more due to workers leaving the labor force, putting the labor force participation rate at 63.2% – its lowest since 1978

- Quantitative Easing will continue now until at least January 2014 as the wobbly economy and lack of clarity due to the recent Government shutdown have combined to increase uncertainty about economic health

“Weak Job Data May Weigh on Fed’s Decision on Stimulus” – New York Times, October 22, 2013

The above headline from the New York Times wins the award for Understatement of the Year. “May” weigh on the Fed’s decision? The September unemployment report1, released Tuesday by the Bureau of Labor Statistics was a disappointment. Though 148,000 jobs were added and the unemployment rate ticked down to 7.2%, the consensus add was for 185,000 net new jobs. The unemployment rate fell due to citizens leaving the labor force, which kept a lid on the labor force participation rate at 63.2% – still at its lowest since 1978.

Perhaps more ominous, the data used in this employment report was collected BEFORE the recent shutdown of the US government. This will no doubt weigh on the fourth quarter economic statistics yet to come.

Though manufacturing data demonstrates evidence of a growing industrial base, other metrics including new home sales and CPI show evidence of an economy struggling to live up to its potential. If increasing bond yields (see the US 10 year bond below) and commodity prices are true harbingers of inflation, we can surmise that inflationary expectations are well contained in the US. In short, the Federal Reserve’s attempts to reflate the US economy through multiple rounds of QE, Operation Twist, etc. haven’t worked.

Chairman Bernanke first mentioned the idea of tapering here and sent yields higher and emerging market currencies and current account balances into a tailspin.

Chairman Bernanke first mentioned the idea of tapering here and sent yields higher and emerging market currencies and current account balances into a tailspin.

The “head fake” Chairman Bernanke gave the markets in September when tapering was postponed, gave emerging markets like India another chance to prepare their economies for the possibility of tapering asset purchases in 2014.

What About Earnings?

….read pages 2-5 HERE

I doubt that Apple is introducing the latest version of the iPad today to deflect other issues, but it probably helps that people are focusing on the product launch and not the performance of the 30-year bonds issued by the Company back in May!

I was reading Institutional Investor magazine last night and a story had mentioned that the bonds were down 17% since being issued to massive fanfare in May. Investors couldn’t get enough of the bonds as they perceived the puny-sized coupon of 3.85% in a Zero-Rate Fed World to be sufficient to compensate for the risks of holding the bond for the next three decades.

(Apple’s common shares have had a good month recently and are now up 15% since the bonds were issue in May)

To be fair, it is was subsequent decision of Ben Bernanke to utter the word “Taper” which broadsided the bond market, including the bonds of Apple Inc, and had nothing to do with the management of Apple itself.

However, the whole episode points to the risks of blindly buying an investment simply because of a high-profile corporate name and because of a relatively low interest rate environment. Apple can’t do much about the fact that the bull market in bonds which began in 1980 finally came to an end in the summer of 2012. A generation worth of tailwinds has now shifted to mild headwinds.

I wonder if the features of the new iPad are enough to ease the nuisance of being down 17% on a bond position in six months? Well, at least the holders of the Apple 30-year will be getting their first semi-annual coupon payment on November 4th at the whopping coupon rate 1.925%.

Neither Apple Inc. shares nor the Apple Inc. 30-year bond are held in the McIver-Jasayko Model Portfolios. Comments about these investments are not intended as advice and do not constitute a recommendation to buy, sell, or hold.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

The dollar fell to its lowest in nearly two years against the euro on Tuesday after data showed the U.S. economy added just 148,000 jobs last month, cementing expectations that the Federal Reserve is likely to keep its stimulus plan for the rest of the year.

Economists were expecting jobs gains of 180,000 and the report covered the period before the government shutdown earlier this month. With the two-week shutdown already expected to have damaged the U.S. economy, the conviction that the Fed will not reduce its asset buying anytime soon became even more entrenched.

“Is the Fed getting tired of being right? Today’s underperforming jobs number fully justifies September’s cautious FOMC,” said Joseph Trevisani, chief market strategist at WorldWideMarkets in Woodcliff Lake, New Jersey.

“Full-bore quantitative easing will probably be with us through the first quarter and speculation for an increase (in QE) may be no further than another weak payroll.”

The unemployment rate did dip to 7.2 percent last month, the lowest level since November 2008, but that has become irrelevant in the wake of the U.S. government’s closure. Economists estimate the 16-day government shutdown shaved as much as 0.6 percentage point off annualized fourth-quarter gross domestic product, through reduced government output and damage to both consumer and business confidence.

In early New York trading, the euro hit a high of $1.3748 against the dollar, its strongest level since November 14, 2011. It was last at $1.3726, up 0.3 percent.

Against the yen, the dollar fell as low as 97.86. It last traded at 98.16 yen, flat on the day.

U.S. employers added far fewer workers than expected in September, suggesting a loss of momentum in the economy that would likely add to the Federal Reserve’s caution in deciding when to trim its monthly bond purchases.

Nonfarm payrolls increased 148,000 last month, the Labor Department said on Tuesday. While the job count for August was revised to show more positions created than previously reported, employment gains in July were the weakest since June 2012.

Economists polled by Reuters had expected the economy to add 180,000 jobs in September.

“This report on the labor market will soften people’s assessments of current conditions,” said Cary Leahey, a senior economist at Decision Economics in New York.

But there was some silver lining in the report, with the unemployment rate dropping a tenth of a percentage point to 7.2 percent, the lowest level since November 2008.

The jobless rate is derived from a separate survey of households, which showed an increase in employment last month.

U.S. Treasury debt prices rose on the report, while the dollar fell against the euro and the yen.

The closely watched monthly employment report was released more than two weeks later than originally scheduled because of the partial shutdown of the federal government earlier this month.

Signs the economy lost steam even before the acrimonious budget fight could convince the Fed to hold off any decision on scaling back its bond buying until the extent of the economic damage from the fiscal standoff is clear.

Economists estimate the 16-day government shutdown shaved as much as 0.6 percentage point off annualized fourth-quarter gross domestic product, through reduced government output and damage to both consumer and business confidence.

Fed officials will meet next week to discuss monetary policy, on October 29-30. They surprised markets last month by sticking to their $85 billion per month bond-buying pace, saying they wanted to see more evidence of a strong recovery.

Now, many economists think the Fed will hold off on scaling back economic stimulus until next year.

“With the possibility of a replay of the budget showdown as early as mid-January, why would the Fed want to pull any levers now? It’s hard to expect any tapering of the Fed’s bond purchases until the budget mess straightens itself out,” Leahey said.

There are fears lawmakers will engage in another bruising round early next year when Congress must agree on a budget to fund the government and once again raise the nation’s borrowing limit.

Employment gains in September were mixed last month, with government payrolls increasing 22,000 jobs after rising 32,000 in August. Both state and local governments added jobs last month, offsetting the decline in federal employment.

There was surprise weakness in the leisure and hospitality industry, which has been adding jobs consistently over the past years. The industry shed 13,000 jobs, the most jobs since December 2009.

The information sector failed to recoup all the jobs lost in August as the motion picture industry shed workers, with payrolls only rising 4,000 last month.

But there was good news in the construction industry, where payrolls increased 20,000, which could ease fears of a leveling off in home building. Construction employment had barely increased over the prior two months.

The manufacturing sector added a meager 2,000 jobs as automobile assemblies shed some jobs.Retail employment increased 20,800, slowing somewhat from the solid gains seen for much of this year.

Average hourly earnings increased three cents in September. They have risen 49 cents or 2.1 percent over the past 12 months. The length of the average workweek held steady at 34.5 hours.

(Reporting by Lucia Mutikani; Additional reporting by Ellen Freilich in New York; Editing by Andrea Ricci)

How do you thank someone who has taken you from crayons to perfume? It isn’t easy, but I’ll try…

How do you thank someone who has taken you from crayons to perfume? It isn’t easy, but I’ll try…

– Lulu, To Sir, With Love (1967)

There is so much to say about the United States government not defaulting.

I’d like to start with a thank you.

It isn’t easy, but I’ll try.

Thank you, Congress, for showing the world there’s nothing wrong with the full faith andcredit of the United States… and for showing the world that having full faith and credit in the United States government is a total bust.

An extension? Really? So, we go through this again in a matter of weeks?

Thanks.

But let’s move on. Let’s talk about Janet Yellen. She’s far more relevant.

She’s about to become the most powerful person in the United States – in the entire world, for that matter.

Here’s the first thing Yellen could do with all that power – if she wants to save America.

So, just how powerful is Janet Yellen going to be?

The (Real) Most Powerful Person in the World

The power to make or break America, to enslave it or free it, is vested in one person: the chairman of the Federal Reserve Board.

You see, it isn’t the president of the United States that has the real power. Presidents come and go. The pimps and panderers of Congress come and go, too. And too many stay for too long.

It’s not that presidents and Congress are a sideshow, or that they act on the periphery of the economy – even though they have marginalized themselves to the point of being bit players in the game.

It is simply that the power to control the money supply, the power to control interest rates, and the power to supervise – or more aptly the power to supersize – the banks that have become the arbiters of our daily lives and our manifest destiny (manifesting money in their bonus pools) resides at the Federal Reserve.

You want prosperity? Alan Greenspan gave it to us – not any president or Congress.

You want a crisis and a Great Recession? Alan Greenspan obliged us.

You want to stop the financial systems of the world from going over a cliff? Ben Bernanke saved all the Too Big to Fail banks from imploding into nothingness.

You want to make those Too Big to Fail banks (that all essentially failed) a lot bigger? That would be Ben Bernanke.

You want to enrich the 1% and eviscerate the middle class? You guessed it: Ben Bernanke.

Yellen, the now vice-chairman of the Federal Reserve Board, has been nominated to the chairman’s seat to run America. She will be confirmed.

There are a lot of questions about what Yellen will do and not do with her power.

But will she free us, or continue to enslave us?

What’s the first thing Yellen should do when she puts on that bejeweled crown?

Should she address how she’ll steer monetary policy?

Should she address where she’ll steer policy and execution on bank supervisory issues?

If she delves into monetary policy, should she get into the weeds on tapering quantitative easing?

Or should she refrain from tapering… at least until there’s pheasant under glass on every table – and two Bentleys in every garage – in the homes of her banker “constituents” and their crony capitalist comrades?

If she delves into bank supervision, should she support higher, stronger capital standards, surcharges on Too Big to Fail behemoths, or beefed-up liquidity standards?

Should she limit short-term wholesale funding, and mandate transparent capital plans?

Would she advocate for orderly resolution laws that trigger automatically when institutions are insolvent…. or when they’re adjudicated criminal enterprises?

Or should she just pretend she’s going to make changes while enforcing the status quo?

Or would she begin to change things for the better?

A Change in the Role of the Fed?

There is one thing she could do, one thing she should do – if she wants to save America.

And it’s the first thing she should do. It should be the thing that guides her every policy position, her every decision, and her every proclamation to the American people.

Janet Yellen, immediately upon being confirmed, should hold a press conference. Here’s what she should tell America – and the rest of the world:

“As Chairman of the Federal Reserve Board, I will free America from the economic shackles the Federal Reserve System – a system forged on behalf of the banks and institutions that have used it to commandeer our free markets. I am starting right now, by asking the American people to tell Congress to take back the Fed’s dual mandate and take 100% sole responsibility for fiscal policies to ensure full employment.

“I am serving notice, right here and now, that the Federal Reserve will never again be the president’s or Congress’ piggybank. If they don’t want to raise taxes to pay for wars, or programs and giveaways they hope to buy votes with, they’ll have to pay whatever interest rate their creditors demand. Never again will we manipulate interest rates to finance government deficits.

“And as far as being a lender of last resort: Starting today, we’re out of that business. If banks are too big to fail, we will dismantle them. If banks are found guilty of criminal acts, we will jail guilty parties and dismantle them. Any capital markets products that cause inordinate systemic risk, in any way, will be either limited to use by bona-fide hedgers or outlawed.

“The Fed’s mandate under my rule will be simply to free capital markets from manipulation, engender open competition that serves the public good, and ensure price stability commensurate with proactive growth across America.”

Now that would take us from crayons to perfume!

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair