Bonds & Interest Rates

The “Bubblespan Dynasty” at the U.S. Federal Reserve is going through its second succession during a reign that has now extended past a quarter of a century.

The Dynasty began when Alan Greenspan replaced Paul Volcker in 1987. Volcker was more of a career civil servant than an academic or a professional economist. Greenspan started his career has a practicing professional economist and then, by virtue of political connections, became Chairman of President Ford’s Council of Economic Advisers for a couple of years in the mid-1970s. He was always a politically-friendly guy. This contrasts sharply with the astoundingly apolitical Volcker who had absolutely no sympathy for politically-legislated fiscal policy and completely tuned out the election cycle, much to the chagrin of President Reagan and his Treasury secretaries.

With the original appointment of Greenspan a politically-friendly era at the Federal Reserve returned after an eight year hiatus.

One feature of the political friendliness was a greater degree of cozy alignment between fiscal and monetary policy. Rather than opposing and challenging the White House and Congress, the Fed accommodated the growth in spending with progressively greater liquidity that would lower the cost of borrowing to finance that spending.

It was this regime with all of its rationales for greater liquidity that ran headlong into Subprime Mortgage Crisis, the Global Credit Crisis, and the Great Recession. Its forecasting missed everything. All the while, they were enlightening us with platitudes of what it thought was the new era of the Great Moderation, a fiscal and monetary nirvana where politicians and central bankers would become the paragons of global economic growth.

Those at the Fed during the run-up to the crisis appeared to fully believe their own headlines. They were not modest about the role of monetary policy in the economy. This includes the new Federal Reserve Chairman nominee, Janet Yellen.

Now that Yellen has inherited the post-crisis monetary quagmire, it would be a stretch to think that she would be able to bring some fresh perspective to the challenges. To be that objective would raise the possibility of self-indictment. She was one of the navigators that flew the American economy into the side of Mount Subprime. Don’t expect her to tell us what went wrong.

With that, the question is “How effective of a leader can she be if she was part of the problem that she is now charged with fixing?”

It is akin to promoting an arsonist to Fire Chief to put out the fires that they started. Her predecessor, Ben Bernanke, famously said last year that he did not think that low interest rates, which he had advocated in the early 2000’s, contributed to the Housing Bubble and the Subprime Mortgage Crisis that ensued. That provided some pretty good insight as to why his policies weren’t enough to solve the lingering mess six years after the height of the panic.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

“The rate suppression that QE has imposed on developed countries since 2009 triggered a search for yield that flooded emerging economies with short-term ‘hot’ money.”

~ Stephen Roach, former chairman of Morgan Stanley Asia

Dear Mountaineers,

According to Moody’s, the consequences of a US “shutdown” would be negligible for growth in the U.S., and the debt ceiling “will be raised under certain conditions, but should not propel the U.S. into a bankruptcy situation”. As I write this letter, this no worries stance is shared by most analysts. And, financial markets largely reflect this view as well. So far, in financial markets, it’s been pretty much a non-event.

For instance, one might expect US interest rates to start rising in light of America slipping and sliding towards default. Reuters, on Monday, October 7th, reported that “The three main credit rating agencies have all warned, in varying degrees, the United States rating could be cut should it hit an expected October 17 deadline when Washington is set to run out of cash, endangering its ability to pay its debt.”

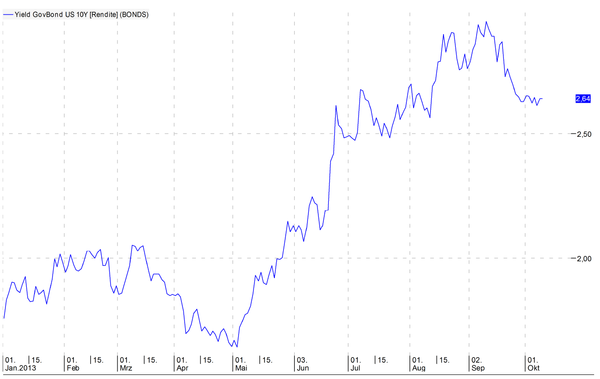

Yield on 10Y US government bond, Oct. 9th 2013

Source: BFI Wealth Management, VWD Group data source

Yet, so far, with exception of some short-term rates, yields have not budged. As depicted in the chart above, the yield on 10-year Treasury paper has even come down over the past few weeks and, at this point, is moving sideways.

What’s interesting about the chart above is the fact that the 10Y yield shot up starkly starting in May, and has been dropping since early September. As we all know, this was the market’s prompt and loud response to the tapering comments made by Ben Bernanke. When the US Fed so much as whispers the possibility of tapering off, bond and stock markets react immediately, in worry of QE being removed. Equally, when Mr. Bernanke removes his threat of rehab, i.e. taking away the “cheap money drug”, financial markets go back into party mode, and the recovery story is back on track.

What sticks out here, really, is the fact that the Fed runs the show. Being the print manager of the world’s (currently still) number one reserve currency, apparently, entails all the power. What the US Treasury and politicians do in Washington appears largely irrelevant. As long as the Fed continues printing money to the tune of some USD 85 billion a month, the party may go one, irrespective of the Obama-Boehner showdown.

When trust is lost

So, as investors, can we all sit back, relax and watch the show in amusement and indifference? I’m not so sure. The credibility of the US dollar, its Treasury papers, and the US economy overall, to this day, are still very solid.

However, trust is a fickle thing. The concerns of investors around the world are growing. They are starting to put pressure on financial markets as we move closer toward October 17th. More and more analysts are concerned that, unless the U.S. government is able to show the rest of the world a desire to move forward and resolve its issues – at least until the next budget and debt ceiling will arrive with certainty – the trust and confidence in the US leadership, the US economy and its currency could take a severe hit. The potential consequences of a loss of trust in the world’s leading economy and number one currency should not be underestimated.

While I too am of the opinion that a last-minute resolution or back-door maneuver will most probably be found –we’ve been here before, several times over – one should not count out that OTHER possibility. In fact, warnings and official alerts abound. If this gets ugly, the “how could I have known?” excuse will not easily fly.

IMF world economic outlook and warnings

In its latest World Economic Outlook, the International Monetary Fund (IMF) warns that the world will “settle into a subdued medium-term growth trajectory” unless leading economies change course to improve prospects for recovery.

Launching its twice-yearly forecasts, the IMF trimmed its predictions of global expansion for 2013 and 2014, with the downgrade as a result of weaker prospects in emerging economies. The IMF still expects a “modest acceleration of activity” next year, led by advanced economies and particularly the United States with an expected 2.6% growth next year, “so long as US politicians manage to resolve the government shutdown and extend the debt ceiling.”

“Activity will move into higher gear as fiscal consolidation eases and monetary conditions stay supportive,” the IMF said. In other words, if the US doesn’t take away the drugs, we’ll be able to enjoy an extended party. But, the IMF did also very clearly warn of dire consequences if the drugs and punchbowl were removed, i.e. if the US government shutdown morphs into a failure to raise the debt ceiling next week.

Olivier Blanchard, the fund’s chief economist, said it would lead to “an extreme fiscal consolidation and [would] almost surely derail the US recovery” with wider global disruption. “If there was a problem lifting the debt ceiling, it could well be that what is now a recovery would turn into a recession or even worse,” he added.

Of course, the global economy has been on drugs – cheap and cheaper money – for over three decades now. Money creation and quantitative easing has turned into an addiction and getting off that addiction will not happen without pain. In fact, at this point, we are sailing into uncharted territory in terms of scope and scale of the monetary and fiscal imbalances we face.

US fiscal and monetary profligacy unveiled by the Treasury

If you live under the assumption that the US government operates in a fiscally sustainable manner and that the US economy is growing strongly, you need to re-adjust your compass. If the latest shutdown spectacle hasn’t already changed your mind, possibly a recent report from the U.S. Treasury Department will help.

The report is nothing short of an official admission and confirmation of the decades’ long woeful mismanagement of U.S. economic, fiscal and monetary policy. The assumption widely held is that the political impasse will likely be resolved in the 11th hour just as it has been during prior showdowns. But, the report describes a broader background and its implications.

The U.S. Treasury Department warns that the economy could plunge into a downturn worse than the Great Recession if Congress fails to raise the federal borrowing limit and the country defaults on its debt obligations. A default could cause the nation’s credit markets to freeze, the value of the dollar to plummet and U.S. interest rates to skyrocket, according to the Treasury report released Thursday.

Keeping a cool head in this situation is probably the right decision. We’ve seen these kinds of shutdowns and showdowns before over and over again. Economically, and in financial markets, these episodes generally have had little impact. Raising the debt ceiling has become the thing to do regularly.

Yet, the intensity of quantitative easing has increased over the past few years. Keeping markets in party mode requires more and more intervention, more and more debt. There’s no turning back and no way out without a painful rehab.

What to expect? Can game theory give us some answers?

Can game theory be employed to explain, or even better “de-code”, the budget showdown in Washington? Game theory, as defined inWikipedia, is the study of strategic decision-making. More formally, it is “the study of mathematical models of conflict and cooperation between intelligent rational decision-makers”.

In an interesting interview with Professor Daniel Diermeier, a specialist in game theory in politics, whether game theory can be used is addressed. He compares the uncompromising positions in the current “budget game” with the situation found during the Cuba Crisis in 1962, when America and the Soviet Union almost unleashed a nuclear war.

The situation is also comparable to a game of chicken, where two cars are driving at each other and the first one to swerve away loses. Swerving is worse for you than not swerving, but if nobody swerves then you die. Similarly, John Boehner doesn’t want to “swerve” (pass a clean continuing resolution or debt ceiling increase) and Obama doesn’t want to “swerve” (sign a CR that defunds Obamacare, or sign a non-clean debt ceiling increase). But if neither swerves, then the shutdown continues and/or we default.

A rational strategy in any case would be to give in and make way because there is much more to lose than there is to win. But if one assumes that the other guy will do that for rational reasons, then you better keep your course. Therefore, to act or appear to act rational in this kind of showdown is a risk in itself, especially if you want to win.

All bets are off

Professor Diermeier’s interview is interesting indeed. However, unfortunately, we can’t say that game theory will give us any certainty or help recognize the “chicken” in this game, at least not in advance.

All bets are off. Beware!

Sincerely,

Frank Suess

About Frank Suess & Switzerland Based Mountain Vision

Frank R. Suess, CEO & Chairman of BFI Capital Group, is the chief editor of Mountain Vision. An advocate of free-market principles, Mr. Suess frequently speaks and writes on global economic, geo-political and financial matters, spanning from the US to China. Mr. Suess started his career in management consulting, having held senior positions with Andersen Consulting and PricewaterhouseCoopers, where he consulted a number of international corporations. He has an MBA, cum laude, from the Haas School of Business, UC Berkeley, CA, USA and a Bachelor´s degree in Finance, magna cum laude, from Saint Mary´s College, Moraga, CA, USA.

Janet Yellen, the nominee for Chairman of the Federal Reserve Board, will likely try in some ways to convince markets that she is not the Super Dove which her previous comments and actions suggested that she is.

But, we have seen this play before. Prior to ascending to Fed Chairman in 2006, Ben Bernanke was already known has “Helicopter Ben” after a 2002 speech in which he said that the Fed could always fight deflation simply by dropping money from helicopters.

He appeared to be constrained during the first year and a half of his tenure as Chairman. Then, in the summer of 2007, the winds began to shift. A few months after HSBC admitted to having problems with subprime mortgages in its U.S. division, news came out that a couple of Bear Stearns funds which invested in subprime mortgages, collapsed. Despite a trickle of subprime naysayers at the time, the HSBC and Bear Stearns episodes were generally a surprise to the rest of the market.

As details of the Bear Stearns debacle emerged beginning in June and accelerating through July, Bernanke casually noted that the U.S. subprime mortgage situation was “contained.” He and U.S. Treasury Secretary Hank Paulson spoke together a number of times stating that the worst of the situation had passed. They downplayed the need for any bailout at all. And then, to reassure markets even more, Paulson said that he had a bailout “bazooka” ready to use if the situation did take a turn for the worse and began to impact the main government mortgage insurers, Fannie Mae and Freddie Mac.

Seven weeks later Paulson was firing his bailout “bazooka” and, in an effort to calm markets, Bernanke cranked open the liquidity spillways around the dam and never looked back. For the last six years of his tenure, it has been full on “Helicopter Ben”, artificially suppressing interest rates and printing trillions in money whenever it looked like the U.S. economy might have a hiccup. After the early brave talk, he reverted back to his old ways.

So, when Janet Yellen tries engaging in some early brave talk of her own and the markets give her the benefit of the doubt, remember her predecessor.

Although there is almost no chance that bond yields will fall back to the generational lows that we saw in July 2012, a dovish Yellen could mean that bonds will tread water for a while longer before the relatively young secular bear market in bonds resumes.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

Initial Jobless Claims spiked 66k this week, up to 374k, the 2nd highest level of the year. The high number is being blamed on the government shutdown issues along with the 15,000 government workers that filed claims.

The S&P Futures are now up 20pts on the day to 1669 with gold futures trading down $10 to $1296.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

David Kotok, Chairman and Chief Investment Officer of Cumberland Advisors (and our host at “Camp Kotok” for the annual “Shadow Fed” fishing expedition), leads off today’sOutside the Box by meticulously dissecting the roadkill that is our federal government’s process for deciding whether they will continue to pay their bills and federal employees’ wages.

David Kotok, Chairman and Chief Investment Officer of Cumberland Advisors (and our host at “Camp Kotok” for the annual “Shadow Fed” fishing expedition), leads off today’sOutside the Box by meticulously dissecting the roadkill that is our federal government’s process for deciding whether they will continue to pay their bills and federal employees’ wages.

Will the US default? David doesn’t think so, and neither do I; but oh, the foolishness, even to tempt the economic fates (read: the markets) this way. David notes that global investors think differently about US default risk than we US-centric types do. Well, David Zervos is with me here at Barefoot, and we just heard that one foreign prime broker (and now maybe two?) is calling hedge funds to say they will not take short-term T-bills as collateral and will mark T-bills down to zero in the event of an actual default. The ultimate risk-free asset is now full of risk? REALLY? This is an unthinkable event. This broker is a Primary Dealer, and I assume they will very shortly get some irate phone calls; but these things start with one bank and then it turns into a herd.

David Zervos, Managing Director at Jefferies, gives us his own slant on the ups and downs and ins and outs of default in today’s second OTB selection. He fills us in on some key constitutional history regarding default and makes it clear what is legal, what is illegal, and what is downright perverted about the process playing out in Foggy Bottom. David remains confident that the Fed is the “one adult in the room that can (and will) put a stop to the madness if we go down the highly unlikely path to default.” We’ll see.

As we confront that possibility, let’s note that Social Security is a trust fund, so the money is set aside in bonds. Not to make Social Security payments would be an administrative decision, not one due to a lack of funds. Other entitlements, you can argue. It will be interesting to see what gets priority if it comes to that, as money comes into the Treasury every day, so there is plenty to cover the interest on the debt, and rollovers could be done under the limit.

However it shakes out, we can only hope that the parties who made the decision to close down the public memorials as a way to demonstrate the “costs” of the government shutdown will not be allowed to come anywhere near the decisions on prioritizing payments. Those idiots should be fired and barred from ever having any level of public responsibility. It cost far more to put up barricades and man them than it would have cost simply to leave the memorials open. To tell WW2 veterans that they cannot see their own public memorial when they have come, perhaps for the last time, to acknowledge the lives of those with whom they served, is beyond appalling. The Tomb of the Unknown Soldier? The Lincoln Memorial? These are public places that could and should have been left open. To barricade them was a petty, punitive act with the most venal of political motives.

It is one thing to disagree on budgets and process and the constitutional order of things. I know that many of my readers are very passionate about which side the bulk of the blame belongs to. But I come down on both sides with almost equal frustration. I understand the American political process and know some of the history of how business gets done in Washington, but some things are just beyond the pale. I would say to our “leaders,” cultivate some perspective and get a grip.

And since we’re getting all the nitty-gritty on federal sausage-making today, I just had to toss in a note from the incomparable, indomitable Joan McCullough, who dredges up for us an esoteric but not irrelevant gem called the Feed and Forage Act of 1861. I will let Joan explain, as only she can.

I get to spend the next three days at the Barefoot Ranch, partaking of an intensive economic/investment festival (calling it a conference simply misses the energy in the room). All hosted Texas-style by Kyle Bass. His connectivity is astounding: the people gathered represent some of the finest thinking anywhere – and he has managed to get them in one room. Some of the names are old friends to this letter (Lacy Hunt, Niall Ferguson, Anatole Kaletski, Jon Sundt, Mark Yusko, Larry Lindsey, and David Zervos), and others are names that ride under the radar, yet run some of the best trading funds in the world. I can’t tell you how excited I am to be allowed in the room. I will report back this weekend on what I learn.

And now I’m off to try to figure out where the world is going, eat a lot of BBQ and chuckwagon food, and just have some fun. Life can be so good at times.

Your forever amazed at the US political process analyst,

John Mauldin, Editor

Outside the Box

Ed Note: Read the articles in a nice clear .pdf link HERE, or continue to John’s Outside the Box Main Page

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair