Bonds & Interest Rates

President Obama announced today that he is nominating Janet Yellen, currently the Vice-Chairman of the Federal Reserve Board, to role of Chairman.

Yellen has been on my radar screen since the Clinton Administration when she served as Chairman on Clinton’s Council of Economic Advisers. She is a known entity.

In 2008, she spoke at the CFA (Chartered Financial Analyst) Institute’s Annual Conference which happened to be held in Vancouver that year. At the time she was serving as President of the Federal Reserve Bank of San Francisco (one of the 12 regional Federal Reserve Banks). During her presentation, she struck me as a potentially autocratic leader. Prior to listening to her in person, my sense was that she was might have been a more diminutive personality and a wide consensus builder.

In the Q&A session, she came across as extremely confident in what the Fed was doing and that it had done a great job during the decade during which she held on-and-off roles within the Federal Reserve System. This was about four months before the Lehman Brothers collapse which might tell you that there was some over-confidence present. However, during the Q&A she also exhibited some tone deafness as some extremely well qualified delegates had some great but serious questions. Her answers suggested that either she did not grasp the importance of some of the question topics, or dismissed them because they did not fit her perspective or beliefs.

My impression at the time was that she was especially concerned with maintaining economic growth at almost any cost. She appeared to be more concerned about Americans enjoying a high standard of living, even if it resulted from financial engineering. She didn’t seem especially focused on traditional central bank issues such as the general stability of the financial system and the things that could disrupt that. To be fair, Alan Greenspan and Ben Bernanke also fell into this category of central banker. Generally, these central bankers have pushed and pushed for wider powers and much more broad mandates. They see themselves more as general economic guardians as opposed to strictly central bankers.

Yellen will almost certainly be friendly to the current presidential administration and its ambitions for greater spending and bigger government. These ambitions are facilitated by low interest costs on the Federal debt and Yellen is just the person to fight for that.

That said, monetary has lost much of its potency over the last five years with respect to spurring employment and economic growth. If she maintains the rate of money-printing, or Quantitative Easing, well into next year, we could see a situation where the market not longer believes in the efficacy of the policy. It will be very interesting to see what she does in this case which would be an extremely challenging period for someone who sees themselves as an economic guardian.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

The news over the last two weeks has suggested that if U.S. lawmakers are unable to pass an increase to the federal debt ceiling, the U.S. will default on its Treasury bond obligations.

Not so fast.

There is no law that stipulates that there will be a halt on maturing bonds being redeemed and on interest paid to current bondholders.

Instead, the scenario would be more like this:

The U.S. Treasury Department has three agencies which make payments to cover the cost of running the government. This covers almost everything including the wages of government workers, wages of military personnel, civil and military procurement, and interest on the bonds that it issues. Since they have not had to prioritize in the past, there is no existing method of prioritization. Because the debt ceiling has been perpetually higher than the amount of outstanding debt in the past, all these payments have been on autopilot over the years.

So, in the event of hitting the debt ceiling, the U.S. Treasury will probably have to manually prioritize expenditures. Jack Lew, the Secretary of the Treasury, and his staff will have to carry out these decisions. Jack Lew’s boss is President Obama. Therein lies the source of Obama’s panic. Hitting the debt ceiling would be akin to a hot, flaming ball landing in his half of the court. He will be forced to decide whether to keep things like the National Parks open, or to pay interest to the bondholders. Considering that some of America’s largest trading partners are significant bondholders, and that the Treasury will have to roll-over $3 trillion in maturing bonds over the next twelve months, they certainly don’t want to upset those bondholders.

So, with that, what are the chances of a default? Low.

That does not mean that it cannot happen. Back in the late 1970s, the U.S. bumped into the debt ceiling for a short-period of time but the ceiling was quickly raised. However, there was a glitch with some word processing software that bungled the administration of the interest payments and those payments were delayed. The bond market got hit has investors became unnerved. And, it took a number of months before bond prices rose back to where they were before the problem.

Barring some similar glitch, a default will probably be avoided at all costs and bonds should sail relatively smoothly through this period.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

As you know, Detroit was recently flattened.

As you know, Detroit was recently flattened.

Now, it’s being scrapped…

It’s the largest municipal bankruptcy in US history. Detroit was once one of the richest… and most dynamic… cities in the world. And it was the center of the United States’ most profitable industry: automobiles.

German and Japanese automakers had the good fortune of being bombed in World War II. But Detroit grew bigger… more prosperous… and full of zombies.

Yes, dear reader, Detroit is another classic zombie story. Since 1971, almost all big stories have a zombie angle. Because the credit-based monetary system Richard Nixon put us in is a perfect habitat for zombies. The New York Times had the story:

Detroit, the cradle of America’s automobile industry and once the nation’s fourth-most-populous city, filed for bankruptcy on Thursday, the largest American city ever to take such a course.

Not everyone agrees how much Detroit owes, but Kevyn D. Orr, the emergency manager, has said the debt is likely to be $18 billion and perhaps as much as $20 billion.

For Detroit, the filing came as a painful reminder of a city’s rise and fall.

“It’s sad, but you could see the writing on the wall,” said Terence Tyson, a city worker who learned of the bankruptcy as he left his job at Detroit’s municipal building on Thursday evening. Like many there, he seemed to react with muted resignation and uncertainty about what lies ahead, but not surprise. “This has been coming for ages.”

Detroit expanded at a stunning rate in the first half of the 20th century with the arrival of the automobile industry, and then shrank away in recent decades at a similarly remarkable pace. A city of 1.8 million in 1950, it is now home to 700,000 people, as well as to tens of thousands of abandoned buildings, vacant lots and unlit streets.

Yes, the handwriting has been on the wall for a long time. But what did it say?

We’ll answer that without hesitation. It said: “Beware of Zombies.”

And here we offer a simple test so dear readers can tell which side they’re on.

Ask yourself: In the absence of government would people still willingly give you money to do what you do? If the answer is no, then you are probably a zombie.

Here’s how it works…

When people realize they can use the police power of the government to get other peoples’ money, they rarely hesitate. In the case of Motor City, unionized workers found that they could use government to back their demands. Gradually, wages and benefits rose…

After World War II, Germany and Japan built new auto industries, with factory workers who were willing and able to turn out better cars at lower prices.

Detroit, by contrast, let its machinery get old… and its workers get soft. Due to poor quality, out-of-date styles and high costs, the US auto businesses could barely make a go of it.

Light manufacturing was fleeing the country – to China, Southeast Asia and Mexico.

The heavy industry – car making, steel, mining – was a sitting duck. It couldn’t protect itself from zombies. The zombies soon got control over the government…. and then preyed upon fixed industries.

Only four years ago, the US federal government bailed out GM. Or rather, it bailed out its zombified labor unions – guaranteeing wages and benefits the company couldn’t afford to give.

What was happening in the motor business in general was happening even faster in Motor City.

As Detroit zombified, productive businesses and taxpayers moved out. Zombies were all that was left. People on welfare. People working for the government. People who were disabled. Crooks, malingerers, shysters – they were all there, getting money for nothing in the age-old zombie fashion.

Was there no way to turn Detroit around?

Of course there was. It was obvious how to do it. But who wanted to do it?

The more dysfunctional the city became, the more money the city’s sleaze-ball leaders got from the federal government. That’s how zombieism works: The worse things get, the better they are for the zombies…

Zombieism is like drug addiction. You rarely just “give it up.” Instead, you have to go all the way… and hit rock bottom.

Detroit may be hitting rock bottom now.

And how long will it be before Baltimore and Chicago go broke too?

It depends on how fast interest rates rise. The higher they go, the harder it is for these cities to keep up with their promises to the zombies. And since interest rates are probably embarking on a long-term secular rise… it is just a matter of time before they all go broke.

That is when the jig is up. Zombies fall. The credit-based money system collapses.

…Gold rises.

Regards,

Bill

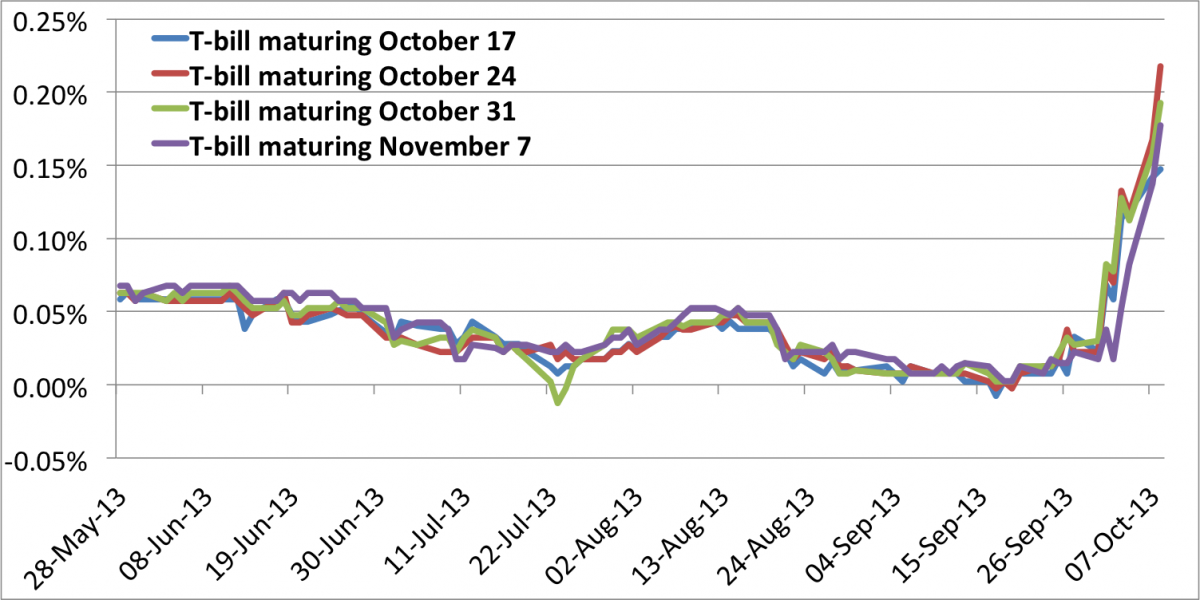

Short-Term Interest Rates Are Blowing Out Again This Morning As Debt Ceiling Tensions Get Worse.

Yields on the front end of the Treasury bill curve are blowing out this morning as markets price in higher odds that the disagreement in Congress over raising the debt ceiling will not be resolved in a timely manner.

….read & view more HERE

….also from ZeroHedge: JPY Jolts Stocks To Overnight Highs As T-Bill Yields Explode Higher

U.S. economic confidence plunged more in the past week than in any week since the collapse of Lehman Brothers on September 15, 2008 — the catalyst for the financial crisis and U.S. recession.

…..read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair