Bonds & Interest Rates

Signs Of The Times

“Fed’s Fisher: We Cannot Live in Fear of ‘Monetary Cocaine'”

– CNBC, June 5

“We increase our year-end target for the S&P to 1,730 (from 1,640) and introduce an end-2014 target of 1,900.”

– Credit Suisse, June 5

What are these guys tripping out on?

“Goldilocks: This Was the Perfect Job Report for The Market.”

– Business Insider, June, 7

Whatever it is, they seem to be smoking it as well.

Ed Note: Notice the name of one of the Cartoonist’s

In the madness of the “Roaring Twenties”, the head of the New York Fed, Ben Strong, wanted to give the stock market a boost. In 1927 he wished to impress a visiting central banker from France and used the term “coupe de whiskey”.

In the madness of the “Roaring Twenties”, the head of the New York Fed, Ben Strong, wanted to give the stock market a boost. In 1927 he wished to impress a visiting central banker from France and used the term “coupe de whiskey”.

Strange that similar boosts did not work during the collapse in the fall of 1929 and in the fall of 2008.

The last time we referred to the “Coupe” in earnest was in November of 2007. Some years ago, Paul McCulley, then at Pimco observed “When the Fed is the bartender, everybody drinks until they fall down.

Then there is the spoilsport:

“Obama: ‘We don’t want to tax all businesses out of business’.”

– CNS, June 10

With his ambition for unlimited government, this should be read as just the industries that interventionists like such as wind turbines and solar power.

Perspective

In the middle of April the scramble to buy risky bonds was another example of “reaching for yield”. That was one compulsion and it was backed up by “Confidence mounts that central banks will prop up debt markets through year end.”

Essentially the best for the bond future was set at the end of April and the best for lower- grade stuff was set in early May. As of this week, the initial whack has been severe enough that establishment is worrying about “disorderly”.

Oooops!

Our May 9th Pivot described the huge issuance of doubtful bonds as the “biggest Garbage Market in history”, and that what “central bankers propose and market forces dispose”.

Noted a number of times was that the bond frenzy was heading for a seasonal reversal in May. That governments were driving the action was discussed and compared to this time in 1998. That was the government tout that spreads in Europe would narrow. Backed by central bankers, LTCM bet the farm on “Convergence” and the crash was monumental. This disquieting event was also cited a few times.

On this spring’s mania, we noted that once the reversal was accomplished around May, lower-grade bond markets would crash in the fall. “Disorderly” is the polite term for a bond market crash.

There could be times when liquidity pressures will encompass long treasuries. Under such conditions most equities and commodities could suffer forced selling.

Indicators

The storm in the credit markets has been developing over the past few months. Perhaps a pause is due, but the turn is severe and points to a lot of forced liquidation in the fall.

On the stock market, the VIX rising though 19 would mark the breakout from complacency.

On currencies, the DX rising through the 84 level would do it. As a general indicator, the gold/silver ratio rising above 63 would be significant.

Precious Metals

Orthodox markets recorded enthusiasm, excitement and complacency only seen at important tops.

A four-year credit, business and stock market cycle is virtually complete.

In retrospect, the bear market for the precious metal sector started in the summer of 2011. The disaster in March-April created momentum and sentiment readings quite the opposite of the excesses recorded in 2011 and again last September.

That was a trip from one excess to the other. But beyond that it was a cyclical bear market for the sector as orthodox markets were accomplishing a cyclical bull market.

From time to time over the past year this page has wondered about when this opposite action would begin, Well, it was on, but we only noticed it earlier in the year.

Gold markets have recorded bearish sentiment and momentum numbers, gloom and dismay seen only at important bottoms.

The path to a cyclical bull market for this sector could still be difficult. Particularly when stocks and bonds are getting hit hard. At other times good advances are possible with eventually outstanding net gains being accomplished.

We would like to be more precise on this, but it is wild out there.

Mother Nature is seriously working to embarrass interventionist theories and practices – again.

The sector is worth buying on the bad days.

Link to June 15, 2013 ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2013/06/this-week-in-money-88/

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com

The QE Infinite parade officially ended yesterday when Bernanke hinted at tapering QE later this year or in mid-2014.

I first warned my clients about this in mid-May writing,

If Bernanke is going to step down (as hinted by his decision to skip out on the Jackson Hole meeting) he’s not going to want to leave with the Fed going at QE 3 and QE 4 full throttle.

Instead his best bet would be to take his foot off the gas a little bit, giving his replacement a little room to maneuver if things get ugly.

Source: Private Wealth Advisory

This is precisely what Bernanke is trying to do. However, there is another far larger issue at work here.

The primary driver of stocks for the last four years has been the hope of more Fed stimulus. This hope has put a floor under ALL asset prices as market participants KNEW the Fed was involved in the markets. As a result EVERYTHING (stocks, bond commodities, even currencies) has been artificially propped.

By calling for the end to QE 3 and QE 4, the Fed has begun to remove these market props. Which means that the markets are now going to start adjusting to where assets prices REALLY SHOULD BE.

Take a look at the spike in the 10-year Treasury yield:

This is just the start. I warned my subscribers in our most recent issue that higher rates were coming noting a collapse in bonds in Europe and the emerging market space.

This could easily become truly catastrophic. The world is in a massive debt bubble and the Central banks are now officially losing control. The stage is now set for a collapse that could make 2008 look like a joke.

If you are not preparing in advance for this, the time to get started is NOW.

For insights on how to prepare for a market collapse… including taking out portfolio “insurance” and which investments perform best during a crash…

http://gainspainscapital.com/protect-your-portfolio/

Best Regards

Graham Summers

The Central Bank announced Wednesday it has no plans to change its buying policy. In short Ben Bernanke’s Fed intends to Maintain Stimulus while it Voiced Increased Optimism on Economy.

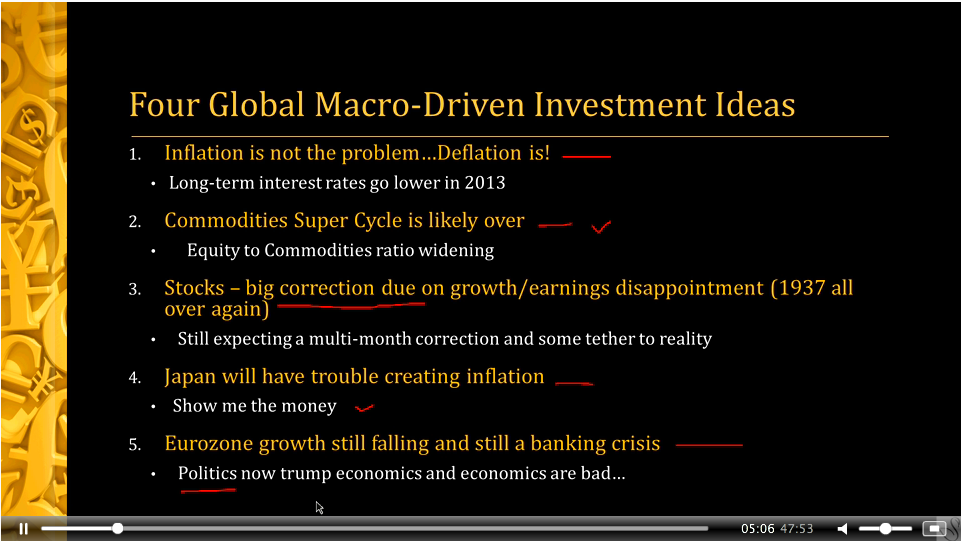

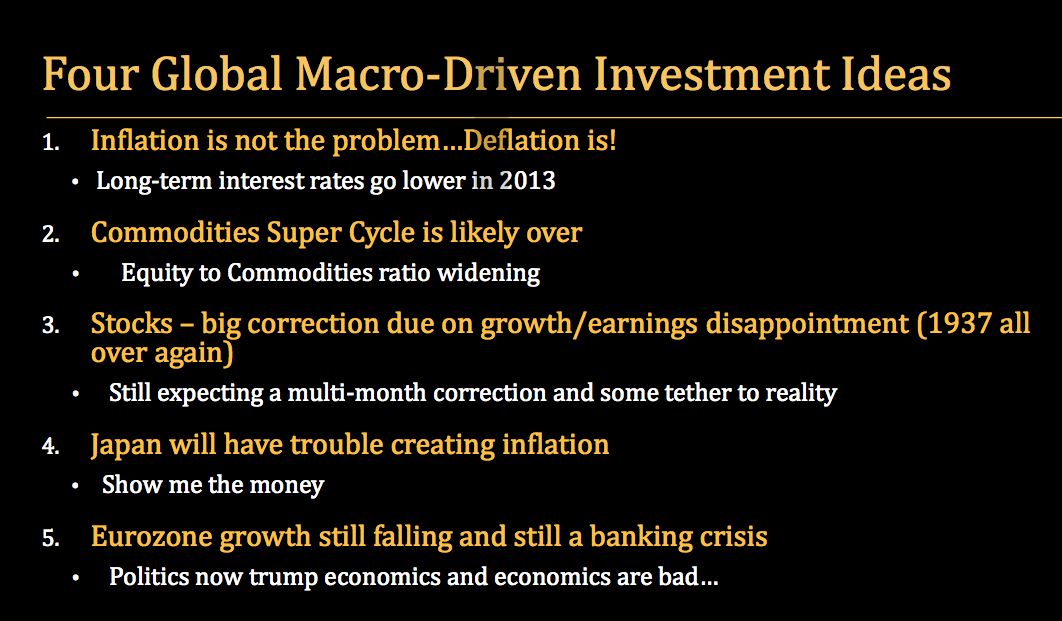

Below you have Jack Crooks Webinar Recording and PowerPoint commentary recorded after the19 June 2013 Federal Reserve Announcements.

Please click HERE or on the image video driectly below to hear the commentary while viewing the powerpoint slides.

The PowerPoint slides contained in the video above can be seen by themselves below.

Be sure to sign up for our FREE DAILY REPORT HERE

MEMBER SERVICES

-

BLACK SWAN FOREX

-

GLOBAL INVESTOR

Research, commentary, analysis and trading advice using ETFs covering global markets and asset classes … delivered each week.

-

THE BLACK SWAN STORY

BLACK SWAN CAPITAL, LLC

2161 SW Racquet Club Drive

Palm City, Florida 34990Email: info@blackswantrading.com” href=”mailto:info@blackswantrading.com” target=”_blank”>info@blackswantrading.com

Ph: 772-349-6883

Skype: blackswanfx

The most frequently asked question I seem to get, no matter the time period, is “Larry, don’t you see hyperinflation for the U.S. in the years ahead?”

So let me clarify my position, here and now. There was a time when I expected the U.S. economy would eventually experience hyperinflation.

But 21 months ago, when the price of gold failed to react to the Fed’s QE III announcement of virtually unlimited money-printing and the yellow metal entered an interim bear market, I knew something had radically changed.

So I further researched the known periods of hyperinflation in the world. And I found something that completely changed my view: There has never been a major core economy that has died at the hands of hyperinflation.

There was the Weimar Republic, of course, but it was not a core economy for the world. There are the hyperinflations of Zimbabwe, Brazil, Argentina and countless other small economies that were never at the core of the global economy.

And upon further study, I found that even the Roman Empire, certainly a core economy during its reign, didn’t even die of hyperinflation.

It died largely because of abuse of power by politicians, which drove citizens away from the Empire; by rapidly rising taxation, which had the same effect; and by a corrupt Treasury and justice system that tracked down and confiscated citizens’ wealth, largely to fund increased military campaigns, which were hoped to revive the Roman economy. Sound familiar?

Was there high inflation in Rome before it fell? Yes, but nothing of the sort of hyperinflation like we subsequently saw in Weimar Germany or any of the countries I mention above.

So, then, what does the U.S. economy face? Further disinflation, eventual reflation or something else?

My view, and I am not hedging my answer or talking out of both sides of my mouth: We face a combination of further disinflation in the short-term, followed by a rather large jump in inflation a few months from now and heading into the future for at least three years.

How high will inflation eventually go? Hard to say, but I wouldn’t be surprised if, say, three years from now, we see 20% or even 25% inflation.

But I highly doubt we will ever see inflation in the thousands or even millions of percent. It’s just not possible in a core economy. For many different reasons.

Whether we have deflation or inflation is also the wrong way to think about the U.S. economy these days. The reason? Ever since we abandoned the gold standard, inflation and deflation have become two sides of the same coin.

In other words, they are both present in the economy at the same time. You can have certain goods and services and even asset classes deflating, while others are inflating. It’s as simple as that.

For instance, the price of LED TVs has crashed in the past year or so, as have the prices of laptop computers and many other goods. Not to mention real estate prices since their peak in 2007.

Meanwhile, other items have experienced inflation. Food prices, legal and health-care services, and more.

So it’s not a matter of one or the other, it’s a matter of what sector is inflating and why, versus which sectors are deflating and why.

Nevertheless, there’s another important underlying force that you need to understand, another one that resulted from the abolishment of the gold standard.

A certain level of general, system-wide inflation is always baked into the cake. It’s due, again, to the fact that we no longer have a gold standard, but it’s also due to many other forces, such as population growth, limited availability of natural resources, the constant desire for people to improve their lives and more.

And it’s also why investing in gold ? just after it experiences a short-term disinflationary trend ? is an ideal strategy to jump on.This is important to understand, because it’s the chief reason prices will be higher a year from now, five years from now and even 10 years from now … no matter what the U.S. or global economy does.

And it’s also why investing in gold ? just after it experiences a short-term disinflationary trend ? is an ideal strategy to jump on.This is important to understand, because it’s the chief reason prices will be higher a year from now, five years from now and even 10 years from now … no matter what the U.S. or global economy does.

For instance, $5,000 in cash squirreled away in a bank in 1913, when the Federal Reserve was created, is now worth only 4.37 cents. That’s right: 4.37 cents.

Put another way, it would take $114,396.56 of today’s money to buy what $5,000 would have bought in 1913.

Want more recent examples? Consider the following …

It now takes $6,210.11 to buy what $5,000 bought just 10 years ago … $29,161.44 to buy what $5,000 bought in 1970 … $47,047.46 to buy what $5,000 bought in 1950.

Even a McDonald’s Big Mac, which cost a mere 57 cents in 1959, now costs about $4.37, an increase of 665%, for an average annual increase of just over 12% per year.

Now let’s look at gold. Even though we had a general level of price inflation from 1980 on, as we always do, the price of gold plunged from a high of $850 in 1980 to a low of $255 in 2000.

In other words, it deflated as the stock market inflated wildly during that time.

And, now, gold has some catching up to do. Just to regain its 1980 high, it needs to shoot to $2,331.75. And it most assuredly will.

Keep in mind the above figures are based on the government’s conservative, politically manipulated Consumer Price Index. As we all know, it vastly understates inflation.

The bottom line: There are several.

First, yes, we have, and pretty much always will have, a base level of inflation in our economy. It’s the natural state of things.

Second, inflation will at some point in the future move even higher. But don’t expect hyperinflation.

Third, and perhaps most importantly, gold does not need any further inflation to move higher. It’s undervalued right now. And it will probably fall even a bit further.

That’s how markets work. They go from overbought and overvalued, to underbought and undervalued.

Thing is, the more undervalued an asset becomes, the greater the profit potential. That’s precisely why I am more interested in gold now than I’ve been since my initial “buy” signal way back in 2000. The profit potential is simply enormous.

Best wishes,

Larry

– See more at: http://www.swingtradingdaily.com/2013/06/17/the-truth-about-inflation/#sthash.POVscBdf.dpuf

Good morning. Here’s what you need to know.

Good morning. Here’s what you need to know.

– Markets in Asia were higher in overnight trading. The Japanese Nikkei 225 rose 2.7% and the Hong Kong Hang Seng advanced 1.2%. European markets are higher across the board, led by France, up 1.7%. In the United States, futures point to a positive open.

– The big story for markets this week will be the Federal Reserve’s FOMC monetary policy meeting, which concludes Wednesday and is followed by an afternoon press conference with Chairman Ben Bernanke. Many expect the FOMC to strike a dovish tone after bonds have sold off aggressively due to fears over tapering back of monetary stimulus.

…….read 2-10 HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair