Bonds & Interest Rates

The Mayans were right. They never predicted the end of the world on 12/21/12. Those predictions were the antics of doomsayers and others hell bent on frightening you.

The Mayans predicted a turn in the major cycles impacting the world, and the beginning of a new era. And to that degree, I think they were spot on.

I say this because my work on economic cycles tells me the same thing;namely that we are now about to pass through the eye of the hurricane of what will be the biggest and nastiest financial storm of all time … and the back wall of that hurricane is about to hit in 2013.

I’ve studied the K-wave in detail … the Juglar economic cycle … the Kitchen cycle … the Kuznets cycle … and even the War cycles …

And all of them start ramping up in 2013, and will exert their influence for years to come, converging upon the economy in a way that hasn’t been seen since the period from 1841 to 1896, a period in U.S. history …

– That was characterized by 14 distinct recessions and SEVEN major financial panics.

– Included the longest and steepest depression in U.S. history, from 1873 to 1896. And …

– Where three of the ten deadliest wars in U.S. history occurred: The Civil War, the Spanish-American Wars, and U.S. Indian wars.

So fasten your seatbelts. The relative calm you’ve seen in the markets over the last 12 to 18 months is nearly over and the next phase of the financial crisis is just about here.

I can’t cover it all in this column today. But I will be making a major presentation of my forecasts at the Weiss Wealth Summit in Florida on January 18, where I’ll reveal all the details, including the strategies you will need to survive the second half of the financial crisis.

Right now though, I want to tell you about one market that stands out from all the rest, and it’s not gold.

It’s none other than the U.S. Treasury bond market and interest rates.

And I’ll put it very bluntly: If you own Treasury bonds, get the heck out of them NOW. Holding Treasury bonds is a recipe for financial suicide, no matter how much credence you give to Mr. Bernanke and the Federal Reserve.

Look, we all know interest rates are going to go up. So there’s nothing new there. The only things that matter then is the timing, when are interest rates going to go up, and then, how rapidly will they go up.

Again, I would not bet on the Fed being successful keeping rates low to 2015 or until unemployment hits 6.5%, as they have recently promised. Rates are going to start going up — and bond prices will fall — starting almost immediately.

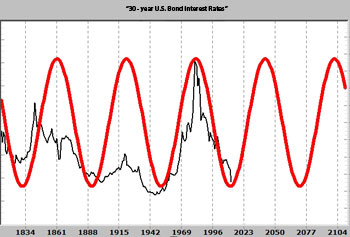

All you have to do is look at the well-established 64-year cycle in interest rates. It’s here in a chart for you.

All you have to do is look at the well-established 64-year cycle in interest rates. It’s here in a chart for you.

As you can clearly see, interest rates peaked right on cue in 1980, then fell for 32-years into their record lows this year.

And now take a look at where the next half-cycle, or 32-years is pointing. Much, much higher for interest rates. Till the year 2044!

Put another way, we are at the very, very bottom of the cycle for interest rates, hovering just above record low interest rates, and there’s virtually nowhere for interest rates to go but up, and starting almost immediately.

Personally, I believe that U.S. Treasury bonds will be the worst investment you can possibly make in the years ahead, destined for dramatic losses.

Moreover, the picture that chart tells you speaks a thousand words …

– The U.S. federal debt and budget deficit will likely get worse, not better, as a result of rising interest expenditures and Washington’s increased trouble selling new debt.

– As interest rates rise, we are likely to see a renewed bear market in the dollar. Rates will not be defending the dollar in this cycle, but instead, will be a reflection of investors, especially foreign investors, cashing in their holdings of our bonds.

– It will also reflect a dramatic increase in inflation.

– And to many analysts and investors, it will also signal renewed bull markets in many asset markets, especially commodities, but also in the shares of cream of the crop multinational companies.

What about other bonds? Shorter-term Treasuries, corporate bonds, municipals, junk bonds?

Based on my work, their prices all headed lower. I repeat: Owning them is a recipe for disaster.

The only interest rate investments I would buy today are sovereign notes and bonds of the emerging economies in Asia. Period. And even there, I would be very selective.

I hope you had a wonderful Christmas, and I wish you a very healthy and happy New Year. Be safe, and be ready to make a boatload of money in 2013.

Best wishes,

Larry

P.S. URGENT DEADLINE TODAY — $6,670 AT STAKE! Today’s your last day to get FREE access to every monthly newsletter published by Weiss Research.

If you haven’t already accepted your invitation to join The Weiss Elite, I strongly urge you to do itnow.

This special opportunity to access EVERY monthly newsletter we publish for a lifetime — a value of more than $6,670 …

PLUS every NEW monthly service we introduce in the future as long as we publish it — and NEVER a renewal fee …

IS ABOUT TO EXPIRE! Click this link for details and activate your membership in The Weiss Elitebefore it’s too late!

Think about one of those movie scenes when the leading man does all he can to defeat the big, bad enemy — punches, kicks, slams, stabs, shoots — but the bad guy just won’t go down. In fact he doesn’t even look fazed.

Follow us: @elliottwaveintl on Twitter | ElliottWaveInternational on Facebook

Economic policymakers aren’t lacking in intelligence – so why are their ideas so bad…?

Economic policymakers aren’t lacking in intelligence – so why are their ideas so bad…?

The question has haunted savants, wives and bartenders throughout the ages. But at least we have a hypothesis.

A guy gets a PhD in physics. You ask him a simple question. He comes up with one of the dumbest answers you ever heard.

Another guy becomes a world chess champion. The next thing you know he’s promoting a cause you know is moronic.

And what about Warren Buffett? There’s a smart guy. He must be smart; he’s made a lot of money.

The French admire intellectuals. The English admire people who can hold their tongues. The Australians admire people who can hold their liquor. But Americans admire people who make money.

A man who can make money is assumed to have qualities of judgment, brains and energy that set him apart from his fellows. Let drop the news that you have made a few million and the local paper will want to ask your opinion on the Egyptian politics or global warming.

And so someone must have asked Mr. Buffett what he thought about taxes.Bloomberg reports:

‘Billionaire investors Warren Buffett and George Soros are calling on Congress to increase the estate tax as lawmakers near a decision on tax policies that expire Dec. 31.

‘In a joint statement today, Buffett, Soros and more than 20 other wealthy individuals asked Congress to lower the estate tax’s per-person exemption to $2 million from $5.12 million and raise the top rate to more than 45 percent from 35 percent.

‘Obama has used Buffett’s call for higher taxes on capital gains to promote the “Buffett rule”, which would require a minimum tax rate for top earners.

‘Soros, 82, is chairman and founder of Soros Fund Management LLC. He is worth $21.6 billion, placing him at 24th on the Bloomberg Billionaires Index. He has donated more than $3 million to Democrats and has financed groups such as the American Civil Liberties Union.

OK. So two rich dudes want to increase taxes. Do they really believe that federal bureaucrats and elected politicians will do a better job of allocating scarce resources than the rightful owners of it?

The story continues:

‘Other signers of the statement include Bill Gates Sr., father of the Microsoft chairman; Richard Rockefeller, chairman of Rockefeller Brothers Fund Inc.; and Leo Hindery, managing partner of InterMedia Partners LP.’

Wait, Leo Hindery? The name rings a bell. Oh yes, is this the same Leo Hindery writing in the Financial Times and proving our point. Mr Hindery must be a smart guy. But what has gone wrong with his brain?

In his FT article on Wednesday of last week, Mr Hindery is as sharp as a baseball bat, bluntly pounding through dull ideas and leaving one hell of a mess behind him. He recites the facts as he sees them: unemployment is high; wages are stagnant and so forth.

And then he moves, like Custer to the Little Big Horn, onto the ground where meddlers cause disasters. In his simpleminded way, he imagines a world where results follow intentions, like marriage follows love. He sees no need for a pre-nup.

No need for second guesses or arrières pensées. It will work out. Why? Because he has thought it out thoroughly! He has used his large brain.

What is his solution to high unemployment and low wage growth? Government! No kidding:

‘The creation of a department of business would be a reflection of enlightened political and corporate leadership,’ says he.

What would this new bureaucracy do? It would, yes… you guessed it, be responsible for a new ‘manufacturing and industrial policy…’ Central planning, in other words. He endorses President Obama’s ‘one-stop shop reform of the commerce-side of the executive branch’. And he rejects the ‘discredited libertarian canard that government has no meaningful role to play in the nation’s commerce’.

The man is a deep thinker. Deeeep.

In the itals beneath his article we get his credentials. As might be anticipated, he is ‘chair’ of one worthy group and ‘co-chair’ of another. On the board of numerous trusts, non-profits, and other organizations, he is a smooth operator. The man is a fast-talking zombie, in other words.

He was brought in briefly to run Global Crossing. When he took the job, the stock was $61. A month later, it was $25. Later, after Hindery was removed, the company went bankrupt. Hindery probably had no idea what was going on.

And then…what about the geniuses at the central banks? A report in the Wall Street Journal tells us that a small group of central bankers all went to MIT… all believe they can engineer an economy, almost as if it were a jet engine.

Bernanke, Draghi at the ECB, King at the BoE, Fischer at the Israeli central bank – all are MIT men. Together, they and colleagues, have added $10trn to the world’s monetary footings in the last four years. None has any experience with this sort of thing – it’s never been done before. All admit that they really don’t know what they’re doing.

‘There’s a lot we just don’t know,’ says former Fed man, Donald Kuhn.

And yet, they plunge on…forward…confident that the will figure it out as they go.

Hindery, Buffett, Soros, Bernanke… to say nothing of Nobel Prize winners Krugman and Stiglitz – they’re all such smart guys. What’s wrong with them? Are they so good at getting their names in the paper…or making money… or whatever it is that Mr. Hindery does…that they have no brainpower left for common sense?

Or, are their smarts the real source of the problem. They are capable of remembering, manipulating and connecting ideas…does this give them the confidence to want to manipulate the entire world and create a better one?

A strong man trusts brute force. A wily man thinks he will win by his cunning. A man with a silver tongue expects to seduce and persuade his listeners.

And the smart man? He thinks he can figure things out…and use his brain to create the kind of world he wants.

Why can’t he? Because no matter how smart you are… the world is far more complex and far more nuanced than you will ever understand. Trying to control it always leads to disaster.

Accordingly, one of the great questions on everyones mind is simply – what are the consequences going to be of Central Bankers being so involved in the marketplace?

Accordingly, one of the great questions on everyones mind is simply – what are the consequences going to be of Central Bankers being so involved in the marketplace?

Quotable

“One of the elementary rules of foreign policy is when you are in a hole, stop digging. But judging by their recent behavior, Beijing’s foreign policy mandarins and national security establishment are clearly in violation of this rule.”- The Bullies of Beijing: China’s Image Problem, The Diplomat

Commentary & Analysis

Italian 10-yr benchmark yield at 4.56%; is the bottom in place?

European periphery country bond yields have plunged, after peaking in late November 2011. The catalyst seems two-fold: 1) the success of the European Central Bank’s (ECB) long-term refinancing operations (LTRO), which force-fed money into European banks to better match ongoing liabilities, and 2) the edict by the ECB that it would do all to save the euro and that includes “unlimited” bond buying if necessary.

Italian 10-year yields peaked at around 7.3% back in November 2011 and now sit comfortably at 4.56% today, after hitting a low of 4.4% on December 4th . December 4th was when Italy’s Economy Minister Vittorio Grilli said Italy was on track to hit its deficit targets for 2013 and 2014, Reuters reported. On Sunday, Italy’s central bank Governor, Ignazio Visco, said the country doesn’t need the ECB to handle market tensions now that market access has been restored.

In short, these are quite optimistic statements from Italy’s economics team given the Eurozone recession is still in full swing and likely deepening (S&P warned Italy’s rating could be cut if the recession continues). Plus, there is potential for a leadership crisis to rear its ugly head in Italy now that Mr. Monti has stepped down, and Mr. Berlusconi, in some form or fashion, has stepped up.

A whole lot of money has been made by those gutsy enough (and deep-pocket enough) to have bought Italian bonds early this year and held on tight for a wild ride. The question we always ask: Is everyone that wants to be in this trade already positioned or are there good reasons why it makes sense for more money to flow into Italian bonds?

Technically, there seems a little bit for both sides to support their respective fundamental view (there usually always is):

10-year Benchmark Italian Yield Daily: 1) An A-B-C correction is almost complete; or 2) a classic head and shoulders setup that suggest a test of those old lows at 3.6%?

Traders will likely be focusing on the Dec. 4th, 4.4% low. They rarely make this stuff easy so stay tuned.

Black Swan Forex Service:

We would be happy to provide samples of our forex trading service upon request. And if you have further interest, you are welcome to a free trial of the service. It is not a service for the novice, but if you are a serious trader looking for ideas, or another view to bounce against your own, I believe you will enjoy Currency Currents Professional.

Black Swan Global Macro Service:

Monthly global macro analysis and longer term trading ideas using ETFs. We are still seeking subscribers who prefer a dose of crowd skepticism delivered with their analysis. At only $99 per year this thing is a real bargain. If you would like to see a sample, please let us know.

Jack Crooks

Black Swan www.blackswantrading.com info@blackswantrading.com

Black Swan Capital’s Currency Currents is strictly an informational publication and does not provide personalized or individualized investment or trading advice. Commodity futures and forex trading involves substantial risk of loss and may not be suitable for you. The money you allocate to futures or forex trading should be money that you can afford to lose. Please carefully read Black Swan’s full disclaimer, which is available at http://www.blackswantrading.com/disclaimer

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair