Bonds & Interest Rates

The new easing steps the Federal Reserve announced Wednesday have some virtue, but they carry a lot of danger, too, says Pimco CEO Mohamed El-Erian.

The new easing steps the Federal Reserve announced Wednesday have some virtue, but they carry a lot of danger, too, says Pimco CEO Mohamed El-Erian.

“We should all welcome the greater policy emphasis being placed on unemployment,” he writes in Fortune. “This national jobs crisis has enormous human costs. . . . And the longer it persists, the harder it is to solve.”

The Fed plans to keep short-term rates near zero until the unemployment rate falls to 6.5 percent.

But, “the bad news is that the institution, with its imperfect tools for the challenge at hand and with other federal government entities essentially MIA, may be taking on an unsustainable burden,” El-Erian says.

“As recognized by [Fed Chairman Ben] Bernanke, the outcome of the Fed’s unusual activism is neither predictable nor costless.” There’s no guarantee that expected benefits will materialize, and there could be unpleasant, unintended consequences, El-Erian maintains.

“Second, the Fed’s growing involvement is ultimately inconsistent with the proper efficient functioning of a market economy,” he writes.

The central bank’s Treasury and mortgage-backed security purchases will mean it is “heavily involved in markets as both a referee and player.”

El-Erian’s Pimco colleague Bill Gross, co-chief investment officer, sees potential problems too.

The Fed’s decision to keep interest rates as low as possible “means the Treasury is issuing debt for free,” he tells Bloomberg. “There are complications. Inflation is one of the complications.”

For the next 10 years, I predict there will be little to no gain in the broader market. Instead, I think something else will account for ALL of the market’s return for the next decade.

My Stunning Prediction For The Next Decade

In just a moment, I’m going to show you a chart that every investor needs to see.

Every analyst already knows about it. Most experienced investors know it too. But it seems like no one is willing to admit exactly what it means.

Frankly, I don’t think most investors are prepared for what I’m about to tell you. I want to make sure you aren’t one of them.

I think dividends will account for ALL of the market’s return for the next decade.

Sound impossible? Not only is it possible, but it’s already happened before… and it’s happening right now.

Since 1931, dividends have accounted for 40% of the market’s total return, according to bond-king PIMCO. That means for every $100 returned by the stock market, $40 of that amount was paid in dividends. (Given that, it’s amazing how many investors still ignore dividends.)

And since that time, two entire decades — the 1930s and the 2000s — have seen ALL of their returns come from dividends.

Just look at the market’s recent history. The S&P 500 has lost 4% in capital gains during the past five years. But when you add in the dividends paid during that time, investors actually gained 7%.

In other words, we’re already in the middle of another “dividend decade” and yet you barely hear a word about it.

Let me show you why I’m convinced we’ll be stuck in this pattern for years to come. It all starts with that chart I mentioned at the start of today’s article…

The past three decades have been the absolute best time in history to invest — and that’s despite the ’87 crash, the popping tech bubble, the housing crash, the United States’ credit downgrade and dozens of other negative events. Just $10,000 invested in the S&P in 1982 would be worth $259,000 today.

But all those gains come with a dirty little secret… debt.

Debt is like jet fuel for economic growth. And never in the history of mankind has a group of people taken on more debt than Americans have in the past three decades.

In the mid-1980s, America’s household debt (just household debt, not government debt) stood at a little more than $2 trillion. Today, it’s $12 trillion — six times as much.

That debt binge has been the most important factor in the unprecedented returns in the stock market for nearly three decades. Debt has fueled purchases of everything from homes to cars to televisions to iPads. It’s helped millions of families live beyond their means… to the benefit of thousands of companies.

The chart below shows the direct relationship between soaring household debt and the rise of the stock market:

This chart also shows why the United States can’t escape the recent downturn, despite trillions of dollars in stimulus and record-low interest rates.

Consumer spending is 70% of the United States’ economy. Debt has fueled increased spending for decades. Now we’ve reached a point where the average American can’t easily take on any more debt. In fact, since the recession, the trend among U.S. households has been toward reducing debt. The bill is coming due on the largest segment of the American economy.

Keep in mind that everything I’ve just told you has nothing to do with government debt. The government has added trillions in debt to bail out banks and carmakers, fund stimulus projects, and backstop government enterprises like Fannie Mae. (It’s largely responsible for the market’s surge in the past few years, despite falling household debt.)

Government debt has risen from 50% of GDP three decades ago to 100% today.

But just like the rise in consumer debt, government debt can’t rise forever either.

On top of all of this, the United States economy faces the law of large numbers. The U.S. is a large, extremely developed market. Our GDP sits at $16 trillion annually. In 1982, GDP was $3.2 trillion (in today’s dollars). During the “debt boom” of the past 30 years, GDP increased 400%.

Say we saw the same 400% growth for the next 30 years. That means in three decades U.S. GDP would measure $80 trillion — more than the entire planet’s GDP today. It doesn’t take an economist to understand that’s highly unlikely, especially given that we can’t continue tapping into debt to fuel that growth.

We’re already seeing signs of a slowdown. From 1983 through 2000 — a period of 18 years — U.S. annual GDP grew at 4% or better nine times.

Fast forward to today, and the U.S. economy hasn’t grown at a rate of 4% or better for 12 straight years. At its current size, squeezing out growth of more than a few percent from our giant economy is a monumental task.

So does all this mean the stock market will crash and you’re better off stuffing your money under a mattress?

Absolutely not.

My point is this: For decades the U.S. economy has been the economic engine of the entire world. Never in history has so much wealth been created. During that time the stock market has soared, but dividends have still made up an enormous percentage of total returns.

Now we are almost sure to see slower growth for years… or even decades to come. In this type of environment, it’s obvious that dividends will account for an even larger share of the market’s returns.

Again, over the last 80 years dividends have accounted for 40% of the stock market’s returns. But going forward, I predict they’ll account for 100% — literally ALL — of the market’s returns. That’s exactly what we’ve seen for the past decade, and I expect that trend to continue throughout the next decade.

In this new environment, there is still an enormous opportunity to make money. You just have to position your portfolio to take advantage of this new reality.

[Note: As I mentioned earlier, the “dividend decade” isn’t just a myth… It’s already becoming a reality. In my recent report, The Top Ten Stocks For 2013, I’ve identified 10 stocks that are already benefiting from this new trend, and could continue to do so if my prediction proves to be true. One of these stocks has returned 137% in three years — more than triple the S&P’s 39% gain. Another has raised its dividend 463% since 2004… and another has over $9.21 per share in cash (49% of its share price).

To learn more about these top picks for the coming year — and possibly the decade — visit this link here.]

All the best,

Paul Tracy

StreetAuthority Co-founder, Chief Investment Strategist — Top 10 Stocks

P.S. — Don’t miss a single issue! Add our address, Research@DividendOpportunities.com, to your Address Book or Safe List. For instructions, go here.

Disclosure: In accordance with company policies, StreetAuthority always provides readers with at least 48 hours advance notice before buying or selling any securities in any “real money” model portfolio. Members of our staff are restricted from buying or selling any securities for two weeks after being featured in our advisories or on our website, as monitored by our compliance officer.

His Total Return Fund gained 11.7 percent over the past year, beating 94 percent of its peers, according to data compiled by Bloomberg. The fund has returned 8.5 percent over five years, outperforming 97 percent of competitors.

His Total Return Fund gained 11.7 percent over the past year, beating 94 percent of its peers, according to data compiled by Bloomberg. The fund has returned 8.5 percent over five years, outperforming 97 percent of competitors.

Pacific Investment Management Co.’s Bill Gross, manager of the world’s biggest bond fund, said the investment company may reduce its risk profile in 2013 after posting higher-than-average returns this year.

With interest rates so low and corporate spreads so tight, “you have to be leery of prices going the other way,” Gross said in a radio interview on “Bloomberg Surveillance” with Tom Keene.

Gross wrote in his monthly investment outlook released this week that structural headwinds may reduce real economic growth below 2 percent in the U.S. and other developed nations. With globalization, technological and demographic changes restricting growth, investors should seek returns from commodities such as oil and gas, U.S. inflation-protected bonds, high-quality municipal debt and non-dollar emerging market stocks, Gross said, reiterating earlier recommendations.

Long maturity developed country bonds in the U.S., U.K. and Germany should be avoided, as well as high-yield debt and financial stocks of banks and insurance companies, Gross wrote.

Investors should anticipate annual returns of 3 percent to 4 percent from bonds at best and equity returns only a few percentage points higher, Gross wrote.

Gross, the founder of Pimco, raised the proportion of U.S. government and Treasury debt in his flagship $285 billion Total Return Fund to 24 percent of assets in October, the first increase since April, as investors speculated the Federal Reserve would add to stimulus measures through more asset purchases, according to the latest available company data. Mortgages remained the fund’s largest holding at 47 percent.

The Total Return Fund gained 11.7 percent over the past year, beating 94 percent of its peers, according to data compiled by Bloomberg. The fund has returned 8.5 percent over five years, outperforming 97 percent of competitors.

The government bond bubble will burst, warns Charles Biderman, CEO of TrimTabs Investment Research.

The main buyers of government bonds have been large global banks that have to keep buying the bonds because if they don’t, both they and the government will go broke, he maintains.

….read more HERE

TrimTabs’ Biderman: Government-Bond Ponzi Bubble Has to Burst

The government bond bubble will burst, warns Charles Biderman, CEO of TrimTabs Investment Research.

The main buyers of government bonds have been large global banks that have to keep buying the bonds because if they don’t, both they and the government will go broke, he maintains.

The banks buying government bonds were the same institutions that central banks rescued by purchasing their bad loans.

…read more HERE

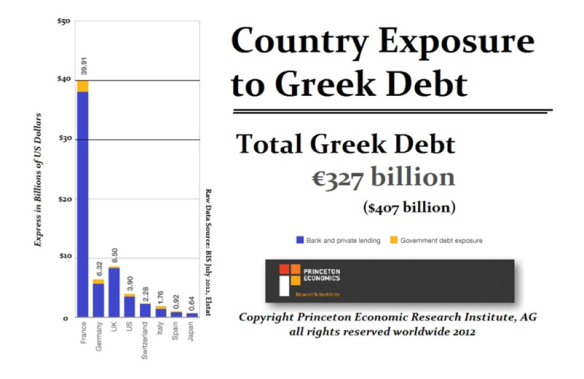

The Sovereign Debt Crisis is leading to authoritarian governments all over the world. Because government have to pay the bondholders and are scared to death of what happens if they cannot, we must lose all our liberties. It is not just the USA. It is everyone.

The Sovereign Debt Crisis is of profound importance. What is grossly being overlooked is both the exposure of banks to sovereign debt in Europe as well as Japan. In the case of the former, France is more or less ignoring the global trend and is putting peddle to the medal. As if they were driving straight off a cliff, they have simply sped up the process. On Wednesday the French government approved a measure that will lower the retirement age to 60 from 62 for a narrow group of workers, reversing the unpopular pension reforms made by former President Nicolas Sarkozy. They are also in Britain hunting down its citizens with new tax investigations. If the Greeks do not blow up the Euro, don’t worry, the French will.

The French banks are in serious shape and now the Government will not back off of its insane socialistic policies. Just where is this money supposed to come from nobody knows.

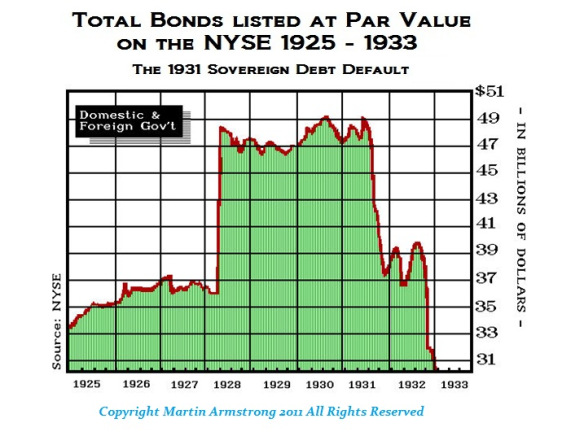

In Japan, the same problem exists. The Japanese debt is going to crash and burn in 2013. This will be the first opportunity for a major low in Japan. It will be 23 years down. Expect the JGBs to crash, the yen to decline, and the Nikkei to finally rally after it makes new record lows in 2013. The Japanese bank exposure to Japanese debt is monumental. The slightest uptick in interest rates in 2013 will wipe out bond investors like we saw in 1931. This will push the dollar higher as capital flees and parks in the dollar. Eventually that will flip and the dollar will drop with the Sovereign Debt Crisis eventually migrating to the USA.

As far as where to put your money, well that will be good solid equities. Gold of course will provide the underground economy. So those buying gold, make sure it is in coin form not in banks nor in bar form. Gold is not headed for nonsense of $30,000 and ounce. If that ever happened, the troops would be hunting down gold door to door in the USA.

The Sovereign Debt Crisis defines everything. Just remember what happened to bonds in 1931. Here is a vivid chart because this data is usually suppressed.

The government are all about self-interest. If you really think anything will change for the positive, think again.

About Martin Armstrong of Armstrong Economics

“Armstrong is the developer of the Armstrong Economic Confidence Model, best known for calling the crash of 1987 to the very day. The model pegged June 13-June 14, 2011 as the start of a long-term upward trend in the market; the market obliged by notching its first weekly rise since April 29.”. … Pi suggested some future turning points which Armstrong watched carefully as they approached. Among them was December, 1989, which marked the Nikkei’s peak before it crashed. This call earned him the New Yorker magazine’s Equity’s award as the top North American economist, and a big following in Japan, where the idea of cycles, a tenet of Eastern belief, did not seem so far-fetched. He presided over conferences in the ballroom of the Imperial Hotel in Tokyo and began investing billions of dollars on behalf of Japanese clients. He boasted that the Japanese called him Mr. Yen. Another big pi date was July 20, 1998, which turned out to mark the high point in the S. & P. just before a Russian default broke the giant hedge fund Long Term Capital Management and nearly wrecked the financial system. Armstrong by now was running a couple of hedge funds, and the Magnum Hedge Fund Reporter named him Fund Manager of the Year.

“In Armstrong’s view of the world where boom-bust cycles occur like clockwork every 8.6 years, what matters is his record as a forecaster. … He called Russia’s financial collapse in 1998, using a model that also pointed to a peak just before the Japanese stock market crashed in 1989. These days, as the European sovereign-debt crisis roils markets worldwide, he reminds readers of his October 1997 prediction that the creation of the euro “will merely transform currency speculation into bond speculation,” leading to the system’s eventual collapse.”

Investing to beat the coming blow up in the bond markets and you are not going to get a warning first!

It’s instructive to read that legendary bond investor Jeffrey Gundlach is predicting a blow up in global bond markets in a lengthy interview on Bloomberg this weekend (click here).

You don’t need to be a genius to spot the greatest boom of several centuries in bonds. Interest rates paid on bonds are at an all-time low, so that means the value of the bonds that pay them is at an all-time high.

Gundlach, who correctly predicted the subprime mortgage disaster, has a proven record as a prognosticator — and the performance numbers to go with it. At his former firm, TCW Group Inc., his Total Return Bond Fund earned an annual average of 7.9 percent in the decade ended in November 2009, according to data compiled by Bloomberg.

His flagship $35.8 billion DoubleLine Total Return Bond Fund (DBLTX) gained an annual average of 13.2 percent from its inception in April 2010 through Nov. 28, topping the performance of Gundlach’s more famous neighbor to the south, Bill Gross.

The Bond Bubble

….read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair