Bonds & Interest Rates

The Fed released a hawkish statement on Wednesday, but it’s doubtful the central bank will ultimately be able to reach its goal, Bill Gross told CNBC.

The Fed released a hawkish statement on Wednesday, but it’s doubtful the central bank will ultimately be able to reach its goal, Bill Gross told CNBC.- The Fed is maintaining its projection for a federal funds rate at 2.1 percent in 2018, according to the chart that has become known as the “dot plot.”

- He thinks the fed funds rate can go no higher than 1.5 to 1.75 percent over time given current economic conditions.

The Federal Reserve released a hawkish statement on Wednesday, but it’s doubtful the central bank will ultimately be able to reach its goal, noted bond investor Bill Gross told CNBC on Wednesday.

…also from Bill:

Bill Gross warns U.S. market risk is at highest since 2008 crisis

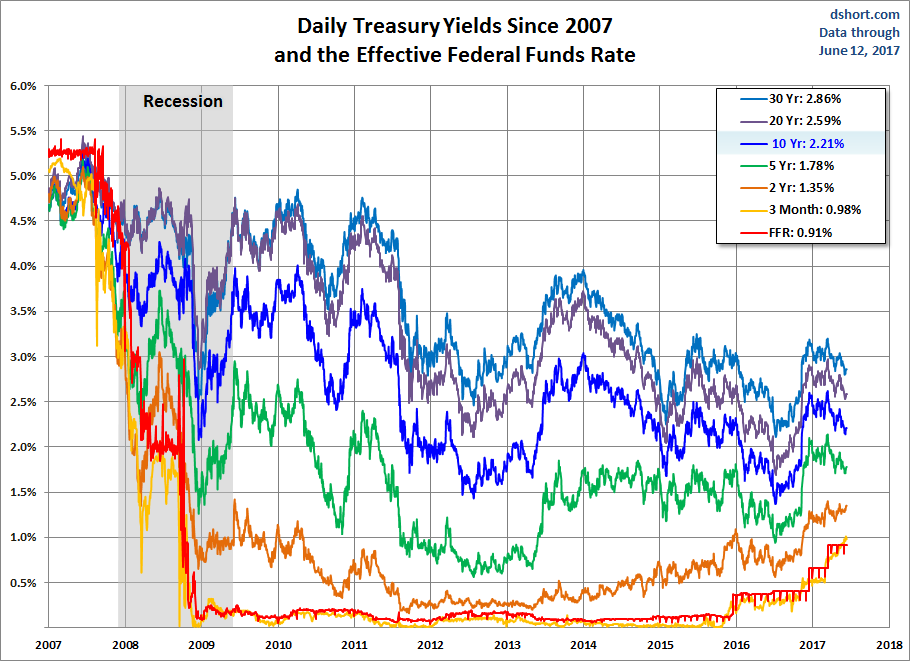

Let’s take a closer look at recent activity in US Treasuries. The yield on the 10-year note ended the day at 2.21% and the 30-year bond closed at 2.86%, well off their interim highs.

Here is a table showing the yields highs and lows and the FFR since 2007 as of today’s close.

The 2-10 yield spread is now at 0.86%.

The chart below shows the daily performance of several Treasuries and the Fed Funds Rate (FFR) since the pre-recession days of equity market peaks in 2007.

A Long-Term Look at the 10-Year Note Yield

A log-scale snapshot of the 10-year yield offers a more accurate view of the relative change over time. Here is a long look since 1965, starting well before the 1973 Oil Embargo that triggered the era of “stagflation” (economic stagnation with inflation). The trendline (the red one) connects the interim highs following those stagflationary years. The red line starts with the 1987 closing high on the Friday before the notorious Black Monday market crash. The S&P 500 fell 5.16% that Friday and 20.47% on Black Monday.

…continue HERE to view chart & commentary

Dr. Michael Berry is the go-to guest when it comes to parsing the tea leaves of the central banks, the US Federal Reserve which has singularly the largest impact on interest rates, stock markets & commodity pricing.

….also: When People Pay No Price For Being Wrong

While the Fed may be raising rates, there is still a flight to quality underway that is giving a bid to US Treasury issues. Low Treasury yields may remain the norm even if the Federal Reserve raises rates again. At about 2.25%, 10-year yields have dropped to 2017 lows, even with the central bank signaling an imminent rate hike. Many still see the stock market crash and that also supplies a bit of an underlying bid right now. However, The Fed has also made it clear it will maintain a gradual approach to shrinking its massive bond portfolio thereby reversing the Quantitative Easing. We are in never-never-land where the Fed tightening will not yet have a direct impact upon the bonds on a one-for-one relationship.

….continue reading and view 3 more charts

….related from Martin:

US Pension Crisis Picking Up Full Speed

Trump’s economic agenda has become further delayed by what seems like daily leaks from the White House. This may finally bring about the long-awaited equity market pullback of at least 5 percent. However, what will prove to be far more troubling than Trump’s ongoing feuds with the DOJ and the press, is the upcoming market collapse due to the removal of the bids from global central banks.

Trump’s economic agenda has become further delayed by what seems like daily leaks from the White House. This may finally bring about the long-awaited equity market pullback of at least 5 percent. However, what will prove to be far more troubling than Trump’s ongoing feuds with the DOJ and the press, is the upcoming market collapse due to the removal of the bids from global central banks.

The markets have been feeding off artificial interest rates from our Federal Reserve and that of the European Central Bank and the Bank of Japan for years. In addition, the global economy has been stimulated further by a tremendous amount of new debt generated from China that was underwritten by the PBOC. After it reached the saturation point of empty cities, China is now building out its “Belt and Road Initiative” that could add trillions of dollars to the debt-fueled stimulus scheme that has been spewed out over the world-wide economy.

Adding to this, the NY Fed just informed us that households are spending like its 2008. In fact, Americans are now in more debt than they were at the height of the 2008 credit bubble – a new high of $12.7 trillion – exceeding debt loads right before the entire financial system fell apart. In fact, Total U.S. debt has now reached 350 percent of GDP.

The perma-bulls on Wall Street argue this willingness to take on debt demonstrates optimism among banks and consumers about economic growth. But the truth is the bull market in equities has been fueled by a record breaking pace of Central Bank money printing and an unsustainable accumulation of global debt that has reached $230 trillion, or 300 percent of GDP.

Right now, the daily leaks out of the White House are sucking all the oxygen out of the room. But worse, they are delaying what Wall Street really needs to sustain the illusion of economic viability–a massive corporate tax cut that is not offset by eliminating deductions or reduced spending. After all, the market is in a desperate need of a reason to justify these valuations now that the Fed has abandoned Wall Street—at least for the time being.

But the truth is this extremely complacent and overvalued market has been susceptible to a correction for a very long time. But just like Trump, it has so far behaved like it is coated in Teflon. North Korean Atomic bomb tests, Russia election interference, Trump’s alleged obstruction of justice, an earnings recession, GDP with a zero handle; who cares? As long as a tax cut could be on the way and global central banks keep printing money at a record pace, what could go wrong?

It is still unclear if the latest Trump scandal provides an opportunity to yet again overlook these salient facts and simply view this sell off as just another buying opportunity. However, in the longer term we believe that the inevitable exodus of Central Bank manipulation of interest rates is going to bring chaos to the major averages, as it blows up the asset bubbles that have been underwritten by the mountain of new debt purchased by these same banks.

The Fed has ended its QE programs, for now, and is marching down the dangerous path of interest rate normalization. And the ECB will be forced to follow shortly. It is then that these bankers will realize that the record amount of debt they sponsored requires a record low level of debt service payments to keep the solvency illusion afloat. Once this bond bubble pops it will prove devastating for those investors that have been inculcated by central banks for decades that every single down tick in stocks is a buying opportunity, along with the mistaken and dangerous belief that active investing should have gone extinct long ago.

By Michael Pento, President and Founder of Pento Portfolio Strategies

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair