Bonds & Interest Rates

Rosengren & Carney

Draghi Heckled

Treasury Hat Trick

Stop Drinking Now

A Brief Commercial

Orlando, Washington DC, St. Thomas, and SIC 2017

Basic economics tells us all resources are scarce, but our demand for them is not. Hence we need methods to allocate the limited supply of each resource. A significant part of economics is the study of those methods.

One exception to the rule, though, has developed in the last few years: The amount of information available to us is practically unlimited. Open your internet browser, and most of that information is just a few clicks way. But if media industry profits (or lack of them) are any indication, demand for that information is anything but infinite.

One problem with information is that much of it is biased. I know, for instance, that when I read a certain economist commenting on recent data, he is going to put a spin on it that reflects the particular economic soapbox he prefers to stand upon. And while I will occasionally take time to read such people, just to kind of keep up on “influencers,” they often don’t really add much to the conversation.

Then there are those who are always delivering fascinating surprises. They do enormously deep dives into arcane data and tease out insights of real importance – connections to other ideas or solutions to challenging problems – they come up with new and different way of looking at the world. I don’t know what you call them, but “seekers of truth” is how I label them. They are just as curious as I am about how the Grand Puzzle all fits together, and they are describing the pieces as viewed from the another side of the table. I value these thinkers. (Sitting here thinking about it, I realize that I need to put a list together of some of my best resources. Some of them are expensive to access; but, surprisingly, more and more of them are either cheap or free. I will get around to that project and make it available to you one day.)

Back to the main plot line. What is scarce isn’t information itself (we’re all nearly drowning in it) but the ability to process it into something useful. All of us, including me, are still figuring out that part. And the creation of really valuable information takes time. I have had a vivid demonstration of that fact myself these last few weeks as I try to launch a new business andprepare for the upcoming Strategic Investment Conference. You cannot believe how much personal preparation goes into talking with every one of the speakers and figuring out how to blend their ideas so that something coherent emerges from our shared experiences at the conference.

And then there are the challenges of keeping up with my regular writing and research andputting in the many hours it takes to be a dad and granddad, always in the middle of a crisis or two. Life is what actually happens after you make careful plans.

My own particular approach to drinking from the enormous information firehose has a couple of key features.

First, be a connoisseur of good information sources. I hope that for you I am a trusted and reliable source. I do my best to deserve the precious time that you devote to me.

Second, depend on trusted colleagues and associates to pre-process information for you. Let me give you an example. It’s just one out of what could be dozens, but I think it’s a good illustrative choice. High among the sources who keep me reliably up to date and surfing (rather than drowning in) a flood of information is Peter Boockvar, a man whose ability to process raw financial data and quickly transmute it into intelligible, digestible pieces is superhuman. I honestly don’t know how Peter does what he does, but it’s awe-inspiring and very, very helpful.

Today I’m going to share a small sample of Peter’s daily output. Below are three articles he published on one day – Thursday, May 11, 2017. And he does this every day, week and month and year in and out. He never fails to make cogent, interesting points about the day’s events. Think about the brainpower it takes to generate this sort of creative output every working day.

Then, if you’re at SIC, shake Peter’s hand and tell him “Thank you for keeping John sane.” You might even share a drink with him and soak up a little wisdom. I work hard to encourage all my speakers to make themselves available to the attendees at the conference. Take advantage of that.

Here are Peter’s three pieces for May 11. I’ll be back afterward with a few more thoughts.

Rosengren’s 180, Mark Carney Boxed In

United States

In case you missed his comments yesterday, Boston Fed President Eric Rosengren, a currently non voting member, has really done a 180. I always considered him a card carrying bleeding heart dove and now he is one of the most hawkish members of the Fed. It’s the reverse of ex member Narayana Kocherlakota who went the exact opposite route and embraced zero rates and was jealous of the Europeans who went negative.

Rosengren yesterday said he wants to hike rates three more times this year and start tapering after the June meeting. He fears the economy is overheating which is ironic after a 0.7% Q1 GDP print but his point is more on the labor side as he realizes the hole they are now in with the labor market continuing to tighten, the unemployment rate continuing to fall and the Fed is sitting there with its benchmark rate of just 0.875% at the same time their balance sheet is still at emergency levels. Also highlighting the tug of war I’ve talked about all year between hoped for fiscal reform and its tailwind vs the headwind of monetary tightening, Rosengren said the more fiscal stimulus we see, the more monetary tightening we will get as well.

Bottom line, of course this is just his opinion and he doesn’t vote and it only matters what the troika thinks but if his line of thinking, coming from an ex dove, starts to permeate, watch out. That said, I don’t expect Yellen to adopt Rosengren’s stance as it’s just not her nature. We’ll most likely get two more hikes and a December announcement on quantitative tightening. In fact, Bill Dudley today essentially told Rosengren to reign it in as he said “there is no great urgency for Fed to tighten aggressively” and he used that word ‘gradual’ again. He also said that they’ll look at QT later this year or in early 2018. Another noteworthy comment from Dudley was after taking its balance sheet from under $1T to $4.5T he said there is “a lot of uncertainty over how much QE depressed rates.” Funny.

The UK

After the BoE left policy unchanged they hinted at a possible rate hike and warned markets not to be so nonchalant about current policy staying the same. As it was sort of a lame warning, the pound is down and gilt yields are little changed. They also raised their 2017 CPI forecast to 2.7% from 2.4%. What’s keeping the BoE from at least taking away the emergency rate cut after Brexit? They said that their economic forecasts “rely on pickup in wages that had yet to materialize.” I argue they have it backwards. If they cared more about controlling inflation and the plunge in the pound, we’d by definition see a pick up in real wages. Mark Carney in his press conference said “it will be a more challenging time for households.” Well, he’s partly responsible for that with his emergency monetary policy that is crushing wage earners, savers and pensioners while inflation flares. With a straight face he also said that “BoE stimulus isn’t excessive, it’s appropriate.” Appropriate for what? Armageddon? Their balance sheet has never been bigger, they’ve partly nationalized the corporate bond market and their benchmark rate sits at .25% with 10 year inflation expectations at 3.10%, actual consumer price inflation approaching 3% and wholesale input prices seeing near 20% growth.

Evidence that Mark Carney is getting stuck in a stagflationary type environment, March industrial production in the UK fell .5% m/o/m after an .8% drop in February. The estimate was down .4% and the y/o/y gain slowed to 1.4% and was driven by a slowdown in manufacturing.

Continuing Claims/Inflation/Draghi Heckled

United States

Initial jobless claims totaled 236k, 9k less than expected and compares with 238k last week. As a 234k print dropped out, the 4 week average was little changed at 244k. Continuing claims, delayed by a week, fell another 61k to the lowest level since 1988. See chart. Based on this visual, we historically have had only one way to go from here and it also highlights how far behind the 8 ball the Fed is and how much they missed this rate hike cycle. Employers continue to be reluctant to fire employees as its tougher to find good ones and they have high hopes for a tax and regulatory driven acceleration in growth.

Producer prices rose more than expected at all levels. The headline gain was .5% m/o/m, more than double the estimate of up .2%. The core level was higher by .4%, twice the estimate and also taking out trade saw prices spike by .7% vs the .2% forecast. The y/o/y gains for all three was 2.5%, 1.9% and 2.1% respectively. It was mostly the services side of the equation that drove the upside as the BLS said it contributed to 2/3 of the rise. Within this they said that 25% was “attributable to prices for securities brokerage, dealing, investment advice and related services which increased 6.6%.” I thought those prices are falling but whatever. They also cited higher prices for “guestroom rental, loan services, machinery equipment, parts, and supplies wholesaling, portfolio management, and airline passenger services.” On the goods side, cigarette prices was a main driver as they rose 2.2% while prices for food, natural gas and pharma products rose as well.

Bottom line, the demise of the inflation trade is a bit premature. To highlight in the commodity space, the Journal of Commerce index which I continuously refer to is down just 4.5% from its February high which comes after rising by 18% y/o/y. Also, services inflation is sticky and doesn’t just fade away. This said, the markets care more about CPI which we will see tomorrow. Rent growth is slowing and might keep a lid on it as housing makes up 40% of the index. The US 10 yr yield is unchanged on the day but up 1-2 bps from just before the number came out. European sovereign yields also moved higher.

Europe

One last thing, in case you missed it, Mario Draghi was basically heckled in the Dutch Parliament yesterday as they view the evils of monetary extremism similar to the Germans. He was accused of “raiding Dutch pensioners’ wealth” according to the FT. The FT also reported that “at one point following the ringing of bells in the Tweede Kamer, the lower House of the Dutch Parliament, one MP called out that the sound was the ‘end of your QE policies.’

Also the FT reported, and this is a good one, “MP’s finished the session with a gift of a solar powered tulip, to remind Mr. Draghi of the country’s famous asset price bubble and financial crisis in the mid 17th century. ‘We want you to look at this tulip before your meetings,’ said Pieter Duisenberg, the head of the MP’s committee, and son of Wim Duisenberg, the ECB’s first president.”

[JM here: I love people who can give me snippets of information that really illuminate the context of the politics central banks find themselves immersed in. I must confess that even though I have a subscription to the Financial Times, I simply don’t have enough time to read it all. I keep my subscription because people send me links and tell me that I should read this or that article. And I have a few friends who are FT junkies and who keep me up on all the important pieces.]

A Hat Trick of Weak Treasury Auctions

We have a hat trick of weak Treasury auctions this week as the 30 year bond offering was soft. The yield at 3.05% was about 1.5 bps above the when issued. The bid to cover of 2.19 was below the one year average of 2.30 and dealers got stuck with almost 36% of the auction vs the 12 month average of 29%. Prices and yields are not responding as it’s likely explained because the supply is now done for the week and prices adjusted all week. The 30 yr yield today stands at 3.05% vs 2.98% last Friday. The 10 yr yield is up by 5 bps and the 2 yr is higher by 3 bps on the week.

With insurance companies and pension funds typically heavy buyers of 30 yr paper, it’s not as an effective measuring stick of market sentiment compared to the 10 yr and the short end auctions. The recent uptick in yields seems more in response to the rise in Europe post French vote than any positive feel on US economic data. The US Citi Surprise index sits today at -19.2 from -18.2 last Friday.

John here again. All that was just ones day’s output for The Boock Report. But it’s not simply the length – these are relatively short articles. It’s more the density. You could spend hours teasing out all the implications of Peter’s analysis.

Spending hours on this sort of analysis is exactly what most people shouldn’t do, of course. Certainly not every day. It tends to have a kind of paralyzing effect. With Peter’s help I can spend 5–10 minutes and understand all the key data flow that’s happening on a given day. And he does this every day. And has been doing it for years. He has an encyclopedic knowledge of the detail behind every bit of data that comes out.

What makes me particularly lucky is that I have at least a dozen Peters in my life. I have become friends with most of them over the years, and they are my “distillers” of information.

Then there are another dozen or so writers that I read for their thoughtful insights. They too have a keen understanding of how data translates into real-world developments. There is a lot of knowledge available out there, but wisdom – really good thinking – is a rare commodity.

And then, too, the project of researching and writing a book on what the world will look like in 20 years has been an enormous help for my thinking. The project has become something of a fetish for me. I really am compelled to get a grasp on how things are changing. Let me tell you, my views on how the future will develop have changed over the last five years, and not all for the better. I’m increasingly concerned about what I’m calling the Great Reset.

I see my role, as it has developed over the years, as a processor of information who shares an in-depth and hopefully authentic view of “what it all means.” And by authenticity I mean that I’m trying not to spin the data or use it to promote some particular worldview. I do, of course, have my own evolving worldview, and it does show up here and there in these letters, but I try to make sure that I’m reading and talking and thinking on as many sides of the issues as possible.

I try to take all the information that comes at me from the firehose and intuit how it’s all connected. I often have friends tell me that one of the things they like most about my writing is how I pull together so many sources and introduce them to so many new ideas and people.

In addition to the sources I’ve mentioned above, there are perhaps another half dozen people whom I have come to respect over the years as connoisseurs and conduits of information. When they send me something to read, I pay attention. Can I always get around to reading what they send? No, but I try hard. Because the world is getting more and more complicated, and finding that wisdom, that sensible path forward, seems to be getting harder. My job is to try to make it easier for you.

Yes, “drinking from a firehose” is a pretty good metaphor to describe the information flows hitting investors today. Get an inch too close and the pressure will blow your head off. But here’s the thing: You really, really need a firehose in certain situations. Most houses, most of the time, are not going up in flames. But if yours is, you want a firehose on the scene as fast as possible.

By analogy, most days in the financial markets don’t require any action from most investors. But once in a while things burst into flames and you need a firehose. In those situations, Peter Boockvar has a pretty good one. You should visit his website and get a free trial. Then subscribe if it fits your needs – or come back later when you smell smoke.

The Strategic Investment Conference is again sold out, although there are a few spots that always turn up at the last minute . If you can make it, we’ll be glad to see you.

As noted above, Peter will be speaking at SIC, along with two dozen or so equally talented financial and geopolitical experts. SIC is itself a kind of firehose, delivering widsom in controlled bursts. It’s a chance to escape from the daily headlines and refocus on larger trends. And we have a lot of fun, too.

SIC equips you to take advantage of the massive shifts that are destabilizing our world. Change brings risk – but also opportunity for those who know where and how to look.

I really wish every single one of my readers could be with us in Orlando. If you can’t, the next best thing is our SIC Virtual Pass. If you order now at the early-bird price, you’ll get…

• 22 hours of audio sessions packed with insights and recommendations from world-renowned experts

• All the slide presentations from SIC 2017, brimming with actionable investment ideas

• The SIC 2017 highlights video

• Transcripts of every speech, presentation, and on-stage discussion at SIC 2017

I find the written transcripts particularly useful. We have actual humans listen to the sessions and type them out verbatim for you, with a little editing for clarity. It takes a few days extra to prepare these, but then you can browse through them at your leisure.

The Virtual Pass is only $350 if you pre-order before the conference. The price will go up afterward, so now – with SIC just a week away – is the time to move on this. Click here for more information and to place your order.

Orlando, Washington DC, St. Thomas, and SIC 2017

My next trip will be to the Strategic Investment Conference, May 22–25 in Orlando. On the 26th, Shane and I fly up to Washington DC to be with Neil Howe and bride Gisela at their wedding. And in late June Shane and I will fly to St. Thomas for a special occasion and a week of vacation.

I was reminded this week just how critically important it is to make sure you’re surrounded with good people. My teams at both Mauldin Economics and Mauldin Solutions really did jump into the breach this week and pick up the slack when I needed them to. I have an amazing group of people who work with me, and I’m totally grateful for all they do. In a world where business is changing so fast, my teams not only adapt to the changes but also respond to those special situations that crop up from time to time. It seems that one of my really lucky gifts is to be able to pick great partners to work with.

My twin daughters, Amanda and Abigail, are coming in later tonight from Tulsa, and then some of the kids will be coming over even later to all just hang out. And with that I think I’ll hit the send button.

Your thinking I’ll turn off the firehose tomorrow (at least for a day) analyst,

John Mauldin

John Mauldin

subscribers@MauldinEconomics.com

Let’s take a closer look at recent activity in US Treasuries. The yield on the 10-year note ended the day at 2.39% and the 30-year bond closed at 3.02%, well off their interim highs.

Here is a table showing the yields highs and lows and the FFR since 2007 as of today’s close.

The 2-10 yield spread is now at 1.06%.

The chart below shows the daily performance of several Treasuries and the Fed Funds Rate (FFR) since the pre-recession days of equity market peaks in 2007.

Many people don’t recognize the true value of an individual’s contribution to society until he or she is gone.

Many people don’t recognize the true value of an individual’s contribution to society until he or she is gone.

That’s not quite the case with our colleague, Larry Edelson. He did have a large, loyal following before he passed away. But it still applies to him in this sense: The Edelson Institute he founded now has an even larger group of devoted fans than he had.

I’m among them. And as I dig more deeply into his big-picture forecasts, I uncover even stronger evidence that supports them.

A classic example: Larry’s prediction of the coming sovereign debt crisis. Repeatedly and consistently, he told us how it would strike in three distinct phases — first hitting the European Union, then Japan, and finally the United States.

He explained how it would corrode society, corrupt politics, and raise the risk of war. Plus, he predicted what’s widely known today as the global money tsunami, the tidal wave of flight capital flowing into U.S. markets.

Now, the Edelson scenario is unfolding in aces and spades.

That’s why two weeks ago, I gave you the answers to five critical war questions, including the names of three defense giants that stand to benefit the most. It’s why last week, I showed you how the crisis is unfolding in the European Union (New, Bigger Shockwaves in Europe). Plus, it’s also why today’s the day to look ahead to the next big phase …

A Volcanic Sovereign Debt Crisis in Japan

Most people seem to have forgotten how massive Japan’s economy still is. Its GDP is double that of the United Kingdom, India and France. It’s three-times larger than Canada’s. Moreover, with nine of its banks among the 100 largest in the world (compared to ten in the United States), its banking sector remains among the most powerful in the world.

Yes, China’s economy has surpassed Japan’s in terms of sheer size. But compared to China, Japan is far more integrated into the global financial system and it will impact it more directly, especially during a sovereign debt crisis.

The big elephant in the room: Japan’s government debts are off the charts!

I witnessed this phenomenon firsthand. I was there in 1980 when the debt problem first emerged in a big way. I launched and edited Japan’s first newsletter on global bond markets. And I talked to virtually everyone who understood how serious the problem could become.

|

Even back in 1980, many feared that Japan’s giant government debts could strangle its economy, sink the stock market, or worse.

They didn’t want to talk about it publicly, themselves, but they implored me to write about it in the strongest possible terms.

“If we complain too loudly,” they said, “it could damage our relations with the Ministry of Finance and the Bank of Japan. But as a gaijin, you’re kind of expected to be more outspoken. So don’t pull any punches!”

Here’s the irony: In those days, Japan’s government debts were only 50% of GDP. Now, they’ve soared to 239% of GDP, or nearly FIVE times more. (See chart.)

That’s far bigger than the debt load weighing down on Greece (close to 160%) or Italy (about 130%). Plus, it’s nearly double the debt burden of the U.S. government and its agencies.

“Wait just a minute,” I said to Larry when he first made this argument years ago. “Japan and the United States are not directly comparable because Japan’s households save a huge portion of their income, which helps finance their deficit. America’s households save far less.”

True? When Larry and I first talked about it, yes. Now, absolutely not!

Over the years, Japan’s household savings rate has plunged from 20.4% of disposable income to a meager 2.4%. (See red line in chart.)

|

In contrast, the U.S. savings rate has declined gradually from 13.3% to 6.2% (blue line). In other words …

- Japan’s savings rate used to be close to double America’s.

- Now, in a radical reversal, it’s less than HALF of America’s.

Sound alarming? It should. Because if you multiply the risks illustrated in the two charts, you’ll see that the danger in Japan is far greater than most analysts think.

Risk #1 comes from the sheer size of the debt problem, which is 1.7-times worse than the United States (239% versus 138% of GDP).

Risk #2 comes from the scarcity of domestic savings to finance the deficit, which is over twice as bad as in the United States.

Result: All else being equal, their sovereign debt crisis could be about four-times worse! (And ours won’t be a piece of cake either; America’s government debt load is, itself, the worst of all time.)

How could that impact U.S. investors? For an answer, just remember that bond markets around the world are closely linked: When bond prices collapse in Japan, that crisis can easily spread like a contagion to U.S bonds as well.

Everywhere in the world, heavily indebted governments will have to …

- Pay a lot more to borrow money from the public, driving all interest rates higher, or …

- Raise taxes and cut spending dramatically, a big blow to their already-sagging economies, or …

- Some combination of both.

Bad for bonds. Bad for stocks. And bad for investors who are overcommitted to either.

Just don’t assume that this is going to happen all at once. The crisis could ramp up slowly at first and then erupt when least expected.

To make sure you’re prepared, stay tuned to the free updates provided by The Edelson Institute.

Good luck and God bless!

Martin

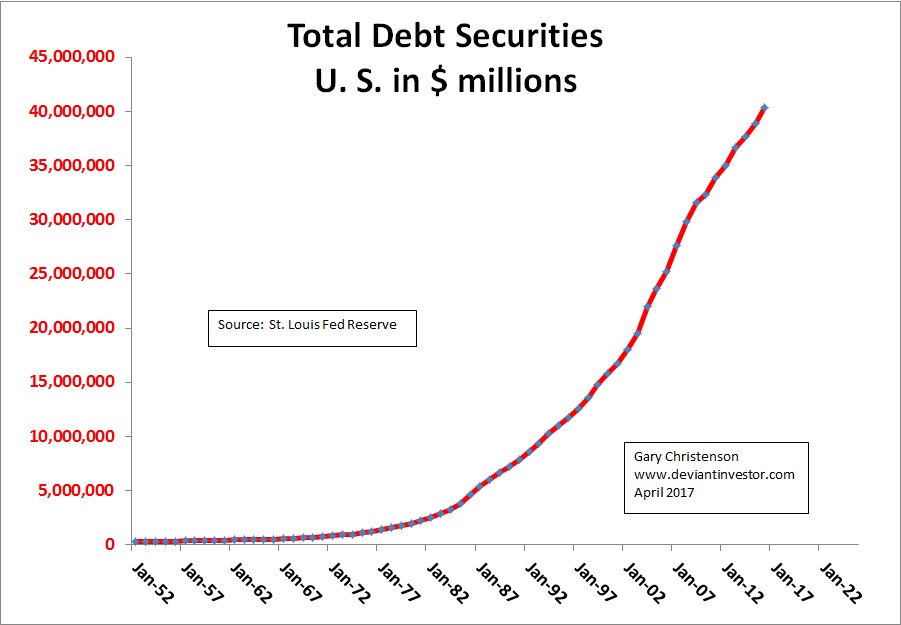

Examine the picture below. The global economy thrives on debt and credit. We purchase essential products using debt/credit. The U.S. dollar bill is a debt of the Federal Reserve. All debt based assets have counter-party risk.

The St. Louis Federal Reserve publishes data on “Total Debt Securities” in $ millions. Note the rapid rise since 1971 after President Nixon encouraged rapid devaluation of the dollar.

Yes, the total U.S. increases debt rapidly – about 9% per year on average since 1971. A graph of U.S. national debt looks similar and shows about the same rate of increase.

Gold bullion and coins are NOT debt and have no counter-party risk, in contrast to debt based assets. But who cares about gold?

- Central banks profess little interest in gold, although they own a substantial quantity.

- Wall Street makes little profit from gold – no interest there.

- The middle class struggles to pay debts and shows little awareness of gold. (A change in attitude is coming!)

How does increasing debt affect us?

- Rapidly increasing total debt means more dollars in circulation and higher consumer prices.

- Increasing debt service for the masses. How much do you owe for mortgage debt, auto loan debt, student loan debt, credit card debt? How much interest do you pay each year?

- More profits for Wall Street.

- Debt increases every day – globally.

- Zimbabwe, Venezuela, Greece, and many more in the near future.

From 1934 Montgomery Ward Catalog:

Debt and Gold:

On the log scale you can see:

- Total debt increased rapidly until about 2008, but the rate of increase has slowed since then. Regardless, debt is growing more rapidly than the economy which forces prices higher.

- How much debt can the economy carry? Is “peak debt” or “debt saturation” the reason why central banks in the EU, Japan and the US have pushed interest rates to near and below zero? Can this end well?

- Gold rose more rapidly than debt until 1980, fell for 20 years, and has increased since 2001.

- On average gold increases along with debt.

- Expect much higher prices for gold as the dollar and all fiat currencies are devalued.

Thought Experiment:

- Which government expects to spend less and reduce debt each year?

- Will military and Medicare expenditures decrease in the next 10 years?

- Name the congressmen who want to spend less and balance the budget each year?

- Does Wall Street support a reduction in spending, debt, and their profits?

- Does the Federal Reserve want to reduce the profits of big banks?

- Do Social Security recipients want their benefits reduced?

- Do “Big Pharma” and the “Health Care Cartel” want their revenue and profits reduced?

- Will the multi-decade trend of increasing debt and increasing prices reverse except as a consequence of a disastrous collapse?

Do you expect total debt to decrease in the next decade?

CONCLUSIONS:

Option A: More debt, more expenses, higher prices. Expect the same failed fiscal and monetary policies, more wars, increasingly fragile economies, accelerating consumer price inflation and an excess of “happy talk” from leaders. Gold and silver prices will rise.

Option B: Catastrophic collapse possible, global depression, nuclear war or expanded conventional war and much trauma for most people of the western world. In this hopefully unlikely collapse scenario, should you own gold and silver with no counter-party risk, or debt based paper that might be worth much less in purchasing power, or could become utterly worthless?

Given the debt policies of the western financial world, the following makes far more sense!

Gary Christenson

The Deviant Investor

After two years of recurring warnings (both on this website and elsewhere) that Canada’s largest alternative (i.e., non-bank) mortgage lender is fundamentally insolvent, kept alive only courtesy of the Canadian housing bubble which until last week had managed to lift all boats, Home Capital Group suffered a spectacular spectacular implosion last week when its stock price crashed by the most on record after HCG revealed that it had taken out an emergency $2 billion line of credit from an unnamed counterparty with an effective rate as high as 22.5%, indicative of a business model on the verge of collapse .

Or, as we put it, Canada just experienced its very own “New Century” moment.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair