Bonds & Interest Rates

The Federal Reserve has raised a key interest rate in response to a solid US economy and expectations of higher inflation, and it foresees three rate hikes in 2017.

The Federal Reserve has raised a key interest rate in response to a solid US economy and expectations of higher inflation, and it foresees three rate hikes in 2017.

Key points:

- The US Federal Reserve raises the interest rate from 0.5 per cent to 0.75 per cent

- It is the first time in a year that the interest rate has been raised, and the second time since the GFC

- Analysts predict a faster pace of increases in 2017 as the Trump Administration takes over

The Fed’s action will mean modestly higher rates on some loans.

The central bank announced after its latest policy meeting that it is increasing its benchmark rate by a modest quarter-point to a still-low range of 0.5 per cent to 0.75 per cent.

The Fed last raised the rate in December 2015 from a record low near zero set during the 2008 financial crisis.

The Fed’s move, only the second rate hike in the past decade, came on a unanimous 10-0 vote.

It also released an updated economic forecast that showed modest changes to its outlook for economic growth, unemployment and inflation, mainly to take account of stronger growth and a drop in the unemployment rate for November to a nine-year low of 4.6 per cent.

Its new projection has the unemployment rate dipping to 4.5 per cent by the end of 2017 and remaining at that level in 2018.

The Fed foresees economic growth reaching 1.9 per cent this year, slightly above its forecast in September, and 2.1 per cent in 2017. The new prediction is slightly more optimistic than it projected in September.

The Fed kept its long-term estimate for economic growth at 1.8 per cent, far below the 4 per cent pace that President-elect Donald Trump has said he can achieve with his program of deregulation, tax cuts and increased spending on infrastructure.

The Fed’s estimate that it will raise rates three more times in 2017 is up from an estimate of two increases at the September meeting.

Its policy statement showed only modest changes in wording from the previous meeting. It said “economic activity has been expanding at a moderate pace since mid-year” helped along by solid job growth.

Mr Trump’s plans for tax cuts and infrastructure spending have led investors to expect that inflation will pick up in coming months.

Pick-up fuels hopes economy will keep rising ….continue, reading view video HERE

…related from Larry Edelson: The Two Biggest Debt Caverns in the World

…related: Can we expect as many as six rate hikes?

No, it’s not the so-called massive government debt problem in China. Like the stories of the ghost cities there, China’s debt problems are largely a myth, in the sense that it’s still largely a closed economy and monetary system. A communist economy where it’s largely the state owing the state … debts can be extinguished by the stroke of a pen.

I’m talking about the brewing U.S. pension crisis and Washington’s sovereign debt crisis, which is now here in spades.

I have been ramping up the warnings in these columns and in my new E-wave columns that now publish every Monday, Wednesday and Friday afternoons.

You know about the U.S. sovereign debt crisis. Washington is officially in debt to the tune of $20 trillion PLUS as much as another $200 trillion in “unofficial debts and IOUs.”

Things like raided Medicare accounts, Social Security Trust Funds, and more.

It’s so bad already that the 30-year U.S. Treasury has already had its worst decline in 26 years, shedding as much as 19% of its value in just the past five months, with the yield soaring from 2.099 to 3.16, a huge 50.5% jump in the same time period.

It’s so bad already that the 30-year U.S. Treasury has already had its worst decline in 26 years, shedding as much as 19% of its value in just the past five months, with the yield soaring from 2.099 to 3.16, a huge 50.5% jump in the same time period.

So much pain is coming in the sovereign debt markets of Europe, Japan and the U.S. …

It will be like a nuclear holocaust wipeout of tens of trillions of wealth.

But there’s also the more personal hit of watching y our state and municipal pensions get gutted.

Currently in deficit by at least $1.3 trillion, the state and local pensions deficits are headed into their deathbeds and it will take nothing short of a miracle to turn them around.

Based on assumptions of achieving returns of roughly 6% to 8% for years on end now, they’ve been returning less than 1% in reality. The “gap” between those figures is bleeding pensions to death and will soon cause a massive coronary heart attack that will reverberate through state and local pensions …

Wiping out police retirements, teacher retirements, public service retirements of all kinds.

Want a sneak peek at what it’s going to look like and cause? Simply look at the ongoing Greek labor unions and their protests over wages, pension and labor agreements which are now ramping up again big time.

Or look at California and Illinois where withdrawals from pensions and employees exiting the system are taking what money they can get now and heading for the hills and in record numbers.

Is it any wonder Americans have gotten angry? Is it any wonder Europeans are doing the same?

I don’t think so, and if I were you I would do everything in my power to protect whatever funds I have in a state or local — and even corporate pension.

And I certainly would not rely on Social Security and Medicare. It’s not going to be there for you. Those programs will start breaking down late next year.

My view: Use the power of large macro-economic cycles that can foretell of these events well ahead of time.

Just like they did for those who profited enormously by correctly timing the Great Depression. They were, yes, in the minority — but it doesn’t have to be that way.

Stay safe and best wishes, as always …

Larry

Larry makes an offer HERE

…related article: Violent Bond Selloff: An Eye-Opening Perspective

The U.S. Federal Reserve gets ready for the final monetary policy meeting of the year, and just like last year there is a high probability of a rate hike announcement. The U.S. Federal Reserve will publish the Federal Open Market Committee (FOMC) statement on Wednesday, Dec. 14 at 2:00 pm EST. Fed Chair Janet Yellen will then host a press conference where she will read a prepared statement and open the floor for questions from the financial press at 2:30 pm EST.

The U.S. Federal Reserve gets ready for the final monetary policy meeting of the year, and just like last year there is a high probability of a rate hike announcement. The U.S. Federal Reserve will publish the Federal Open Market Committee (FOMC) statement on Wednesday, Dec. 14 at 2:00 pm EST. Fed Chair Janet Yellen will then host a press conference where she will read a prepared statement and open the floor for questions from the financial press at 2:30 pm EST.

The Fed is expected to raise the benchmark funds rate by 25 basis points. The eyes of the market will be focused on the economic projections from the central bank to get some insights on next year’s policy moves.

The Bank of England (BoE) will release the Monetary Policy Summary on Thursday, Dec. 15 at 7:00 am EST. The central bank is expected to keep rates on hold with the majority if not all the votes in favor of keeping rates on hold. There is no press conference scheduled following the publication of the statement but the BoE releases the minutes of the meeting immediately after to offer transparency to markets.

The Euro/U.S. dollar (EUR/USD) currency pair tumbled 1.232% in the last week. The single currency is trading at 1.0541 after the European Central Bank (ECB) surprised markets with a reduction in the quantitative easing program, while at the same time extending the deadline until the end of the year and allowing the purchase of bonds with yields below the deposit rate. ECB President Mario Draghi was careful to avoid any comparison of the central bank’s move to be confused with “tapering” as it is slowing down the pace of bond purchases. The euro depreciated after the announcement and press release and is looking to the Fed to announce a 25 basis point hike to its benchmark rate on Dec. 14.

The ECB will face a difficult 2017 as the anti-Union movement across Europe has grown and triggered a surge in political risk. Elections in the Netherlands, France, Germany and Italy will all have a direct impact on the task at hand for the central bank. The ECB has enjoyed the backing of the Union during the worst times of the crisis, but now the European experiment is under threat complicating how fast and conclusive it can respond.

The EUR/USD could be heading toward parity if both the Fed and the ECB continue on a divergent path. The Fed underperformed against its own forecast at the beginning of the year as it has yet to deliver a single rate hike. Post election rallies in the United States have the dollar gaining traction with the promise of higher inflation as a result of new infrastructure projects that could keep the American central bank raising interest rates to keep up.

The Fed will deliver its economic projections on Wednesday and this is where the market will look for guidance into next year. There was plenty of optimism this time last year as the Fed had no way to know of the multiple setback that lay waiting the global economy, this time around after the United States itself has opened a can of political risk going into 2017 and a politically charged environment it remains to be seen if they will be more cautious in their predictions. Banks have been forecasting as many as six rate hikes if the growth rate and inflation expectations are met, while at the lower end a more conservative two could also feature if there are cuts to growth forecasts.

In Elliott wave terms, bond investors have transitioned from extreme optimism to extreme pessimism

[Ed Note: The text version of the story is below.]

What a rout in the bond market in November (Bloomberg, Dec. 1):

Global Bonds Suffer Worst Monthly Meltdown as $1.7 Trillion Lost

The price of U.S. Treasuries nosedived as 10-year yields – a.k.a., interest rates, which move inversely to bond prices — saw their steepest climb since November 2009.

Bloomberg (Dec. 1) provides another perspective:

The 30-year-old bull market in bonds looks to be ending with a bang. The Bloomberg Barclays Global Aggregate Total Return Index lost 4 percent in November, the deepest slump since the gauge’s inception in 1990. Treasuries extended declines Dec. 1.

Elliott Wave International subscribers were prepared well ahead of time.

On June 17, well before the rout, The Elliott Wave Theorist showed this chart and said:

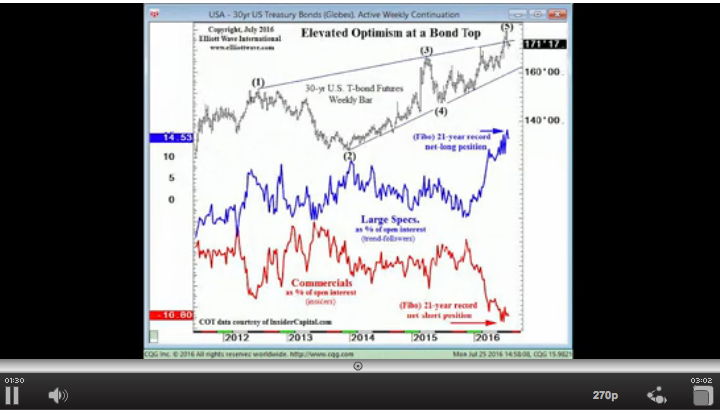

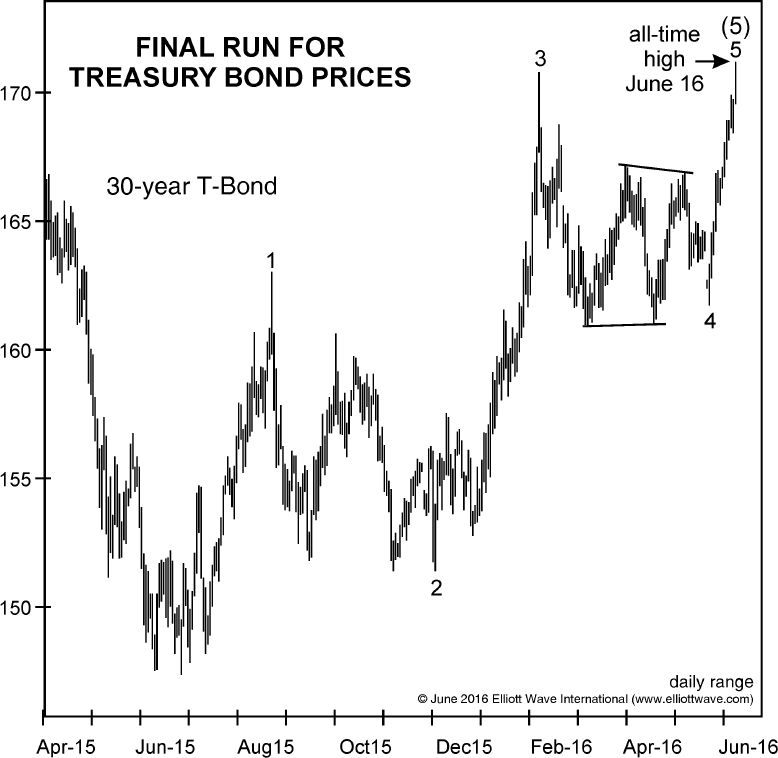

The 30-year Treasury bond made a new all-time high on June 16. The triangle is indicative of a fourth wave, making the recent thrust a fifth wave.

This wave count is terminal. Bonds are on their last leg.

But, at the time, most speculators disagreed. Even so, bond prices topped less than a month later. Said our U.S. Short Term Update on July 25:

The wave structure of the rally ended at the 177^11.0 high on July 11. Sentiment remains historically optimistic. The most recent tally of the Commitment of Traders data shows that Large Speculators (trend-followers) remains a tad off a 21-year record net long extreme in the percentage (of open interest) of bond futures and options contracts they hold. With Commercials taking the opposite side of this trade, the sentiment set up is in place for a continued bond price decline .

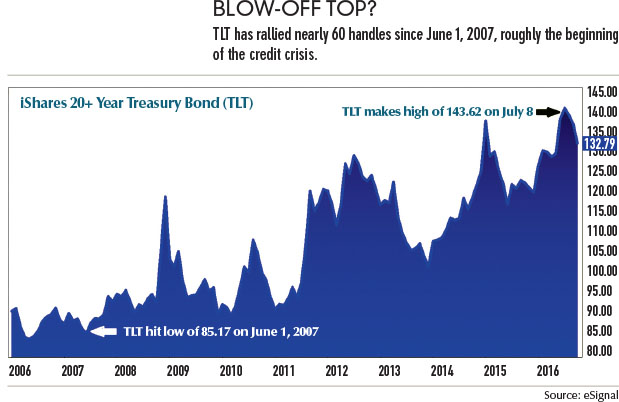

Despite the historic optimism, Treasury bond prices continued to decline.

This week, as of Dec. 1, the 30-year yield rose to as high as 3.15%. That’s a 51% climb since the July low of 2.085%.

In other words, in the short term, the market sentiment in bonds has transitioned from a highly elevated optimism four months ago to a deep pessimism we see this week. In fact, the 30-day bond Daily Sentiment Index (trade-futures.com), which our U.S. Short Term Update quotes quite often, is at its lowest level since September 2013 – a contrarian indicator.

Investor psychology could grow even more negative toward bonds. But, keep in mind that countertrend moves in financial markets usually occur when sentiment reaches an extreme like the one we’re seeing now.

Put differently, the 30-year Treasury bond’s price pattern is again looking highly interesting — although, again, in the opposite way most investors expect.

What to do if/when interest rates start rising? Buy an out-of-the- money put butterfly.

In 2008, the U.S. economy hit its roughest patch since the Great Depression nearly eighty years earlier. Only the inflationary spiral of the late 1970s followed by the sharp recession of the early 1980s can compete with it. In reaction to that inflation, the Federal Reserve, led by then newly appointed chairman Paul Volcker, raised the Fed Funds rate as high as 20% in March of 1980 and January of 1981. The Fed Funds Rate is the rate that depository institutions lend out to other depository institutions overnight, with funds that are maintained at the Fed. The higher the rate charged by the Fed the more painful it is to borrow. During inflationary times, when the rate is raised money turns over more slowly and inflation then cools off, or so goes the plan.

….related: Look what’s happening to Treasuries: Most Oversold in 43 Years

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair