Bonds & Interest Rates

-

Global government debt due in decade or more swells by record

Global government debt due in decade or more swells by record -

Duration buildup creates vulnerability to interest-rate shock

The hottest craze in fixed income is at risk of overheating.

A headlong rush into higher-yielding, long-term bonds in recent years has created one of the most crowded trades in financial markets. Investors seeking relief from central banks’ zero-interest-rate policies have poured into government debt due in a decade or more, swelling the amount worldwide by a record $733 billion this year. It’s more than doubled since 2009 to about $6 trillion, data compiled by Bloomberg and Bank of America Corp. show.

Now money managers overseeing more than $1 trillion say..…continue reading HERE

….related: Bank of America: Investors are getting worried that a bond market crash is coming

Across asset classes, investors are worried about a bond market crash, according to a survey of fund managers around the world conducted by Bank of America Merrill Lynch.

Across asset classes, investors are worried about a bond market crash, according to a survey of fund managers around the world conducted by Bank of America Merrill Lynch.

They think that bond prices are frothy, showing signs of being in a bubble — meaning that prices are much higher than what bonds are actually worth.

Bond prices rose and pushed yields lower as investor demand grew and central banks, in Europe for example, bought bonds to lift inflation and fire up their economies.

…related:

Central bankers are able to put off the day of reckoning for years

The jobs number came in light at 156,000. This benefits the incumbent party because the number wasn’t good enough to invoke interest rate hike fears. It wasn’t bad enough for the market to tank. But all the other factors are still out there, including Deutsche Bank and now the rhetoric concerning a conflict with Russia is heating up.

So, my view has not changed. The markets are asleep and continue to sleepwalk in complacency and there are still too many possibilities for a black swan now only a month out to the election. I’ve heard different reports at this moment that are not confirmed, but we do know the Russians have instituted a no fly zone in Syria. What I can say is the rhetoric coming from both sides is nothing like I’ve ever seen and I was only two years old for the Cuban missile crisis.

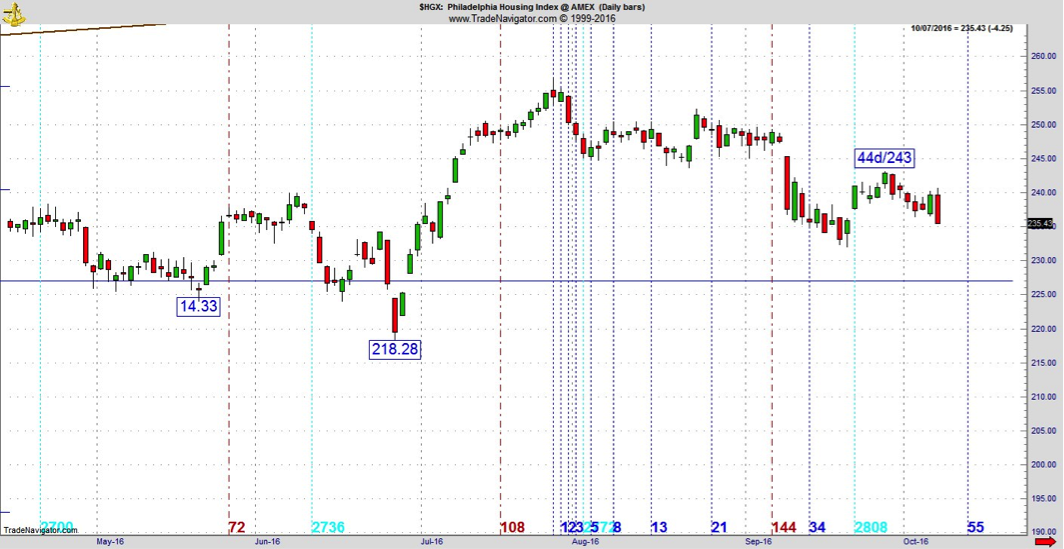

Coming into the week, there is a real shot oil could be peaking right here. Other sectors that could get into trouble are Transports and biotech, which gapped down and extended losses last week. Here’s some interesting symmetry for housing which may finally be losing it. There is a secondary high (second one off top) at 44 days off the top and a matching price at 243. This wouldn’t mean much without Friday’s candle, which was a bearish engulfing to the day before.

This one looks like it’s going to be tough to get back and if we lose housing, we are going to lose the market. It’s not a matter of “if,” but “when.” It could be right now as there will never be a better time in the entire calendar year. As you read this on Monday, note the date was right near the 2007 top and also the 2002 bottom. So this specific time of year has a history of important market turns. With everything swirling around, risk remains very high for an acceleration.

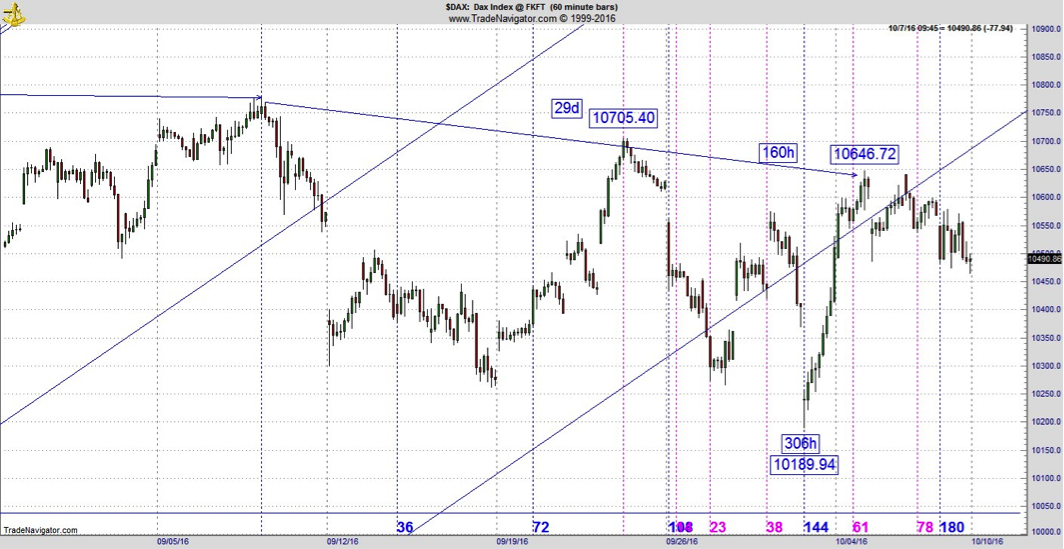

Of course, we know a lot of the trouble starts in Europe, especially Germany. The week didn’t end well there. So here’s a look at what could potentially lead down this week. First of all, the DAX turned lower on a 160 hour high to high sequence while the CAC stalled at 169 hours after a 4569 high. To start the week, the bears have an edge even as the initial Monday action in Europe was good for bulls. It might be small, but it still is an edge. But that’s only Europe, we have a divergence working.

In Part One of this article I addressed the deceit of Hillary Clinton and politicians of all stripes as they promise goodies they can never pay for, in order to buy votes and expand their power and control over our lives.

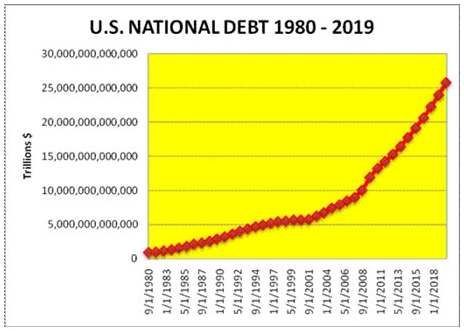

I created the chart below for an article I wrote in 2011 when the national debt stood at $14.8 trillion, with my projection of its growth over the next eight years. I predicted the national debt would reach $20 trillion in 2016 and was ridiculed by arrogant Keynesians who guaranteed their “stimulus” (aka pork) would supercharge the economy and result in huge tax inflows and drastically reduced deficits. As of today, the national debt stands at $19.7 trillion and is poised to reach $20 trillion by the time “The Hope & Change Savior” leaves office on January 20, 2017. I guess I wasn’t really a crazed pessimist after all. I guarantee the debt will reach $25 trillion by the end of the next presidential term, unless the Ponzi scheme collapses into financial depression and World War 3 (a strong probability).

There Is No Economic Recovery!

The FED and the Corporate World understand that there is NO economic recovery. They need to keep feeding this ‘bull market’ with plenty of accommodative easing or this ‘bull’ will die. The FED will do whatever it takes to maintain this by cutting rates to near zero and below so asto spruce up the economy. However, these conventional policies that are being applied, by the FED, will not work seeing as the ‘deflationary forces’ have gained momentum. Global economies cannot sustain rate hikes. They will continue to use ‘expansionary monetary policy’, indefinitely: (https://finance.yahoo.com/news/trump-says-fed-chief-yellen-114816250.html).

The FED will no longer remain the ‘lone wolf’ Central Bank of and by keeping interest rates from going negative. The New Zealand Central Bank went through this same cycle, last year, at which time the economy could not sustain a rate hike, thus resulting in a quick cycle of rate cuts.

The ‘herd mentality’ is now at the stage where they must accept this as the ‘new norm’. They want to keep this illusion alive and do not want to deal with the reality.

When the FED does implement negative interest rates, the stock markets are going to soar so high that it will probably even shock the ‘bulls’. Thus, this is the reasoning that the market will not currently crash, but will experience sharp corrections. In this current market environment, I now recommend putting your money into precious metals.

This is one of the most detested ‘bull markets’ in history. The FED has provided this market with the ingredients that it needs to take it to the ‘bubble level’. The masses will embrace this market in the same manner as the corporate world has done so for the past eight years.

The main trigger for the financial crisis of 2008 was the issuance of mortgages that did not require down payments. The ease at which one could get mortgages, in the past, is what drove housing prices into unsustainable levels.

Currently, Barclays has launched the “Family Springboard Mortgage” which allows homebuyers the opportunity to purchase a property with a mere 5% deposit. In order to acquire this 5% deal, one will need guarantors to put up the cash, which, in turn, will be lost if one fails to repay the mortgage.

Ones’ family/guarantor must place savings which are equal to 10% of the purchase price into a Barclays Helpful Start savings account. No withdrawals are allowed for three years. The Helpful Start savings account pays the Bank of England’s’ base rate plus 1.5%, which currently means getting 2% interest, before taxes. This is not a lot of interest considering the lengthy period of time: (http://www.barclays.co.uk/mortgages/family-springboard-mortgage).

When the FED starts purchasing private assets, this will negatively impact economic growth and consumers’ well-being. This reasoning is that the FED will use this power to keep failing companies alive and thus preventing the companies’ assets from being used to produce goods or services which are more highly valued by consumers.

The Reality:

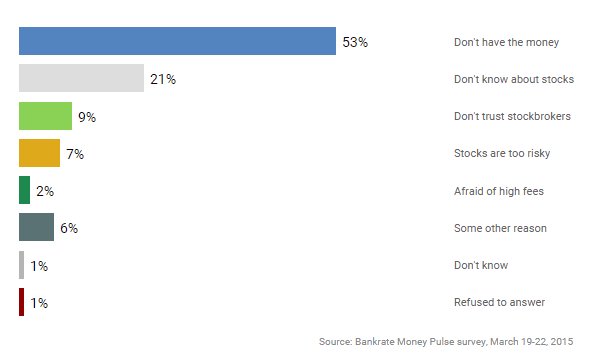

Over 50% of Americans do not have enough money to invest in stocks. The U.S., unfortunately, is currently appearing to be closer to that of a third world nation. Americans appear to be living hand to mouth thus making it more and more difficult for the average person to focus on his/her financial security. One in every seven Americans currently depend on food stamps in addition to using Food Banks, despite this ‘so-called economic recovery’.

The chart below from Banktrate.com illustrates that a total of 74% of individuals either do not have enough money to invest in the stock market or they do not know anything about stocks.

Random tests have already shown that the monkeys with darts fare better than most of these experts would.

The severe economic contractions which I have been speaking of, over the last couple of years, should now be evident to all of us, today. Productivity has now fallen to a negative rate. Investment has stalled and individuals have turned against globalization. Without productivity growth, capitalism becomes unpopular, globalization becomes unpopular and politicians, in turn, become unpopular.

Conclusion:

Gold and silver should be viewed as a form of insurance against the impending future financial disaster. We will also experience another disaster, sooner or later. I am not advocating that you should load up on bullion seeing as the precious metals sector has put in a bottom. I am referring to one obtaining insurance against another financial crisis that has the potential to be larger than the 2008 financial crisis was.

Every crisis also brings with it an opportunity, hence, one should make the best use of this opportunity before the price of gold and silver jump and value. It is better to invest now and see one’s investments multiply rather than waiting for the crisis to commence and pay a premium for insurance later.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair