Bonds & Interest Rates

Bond Sentiment will lead to a Cycle Turn

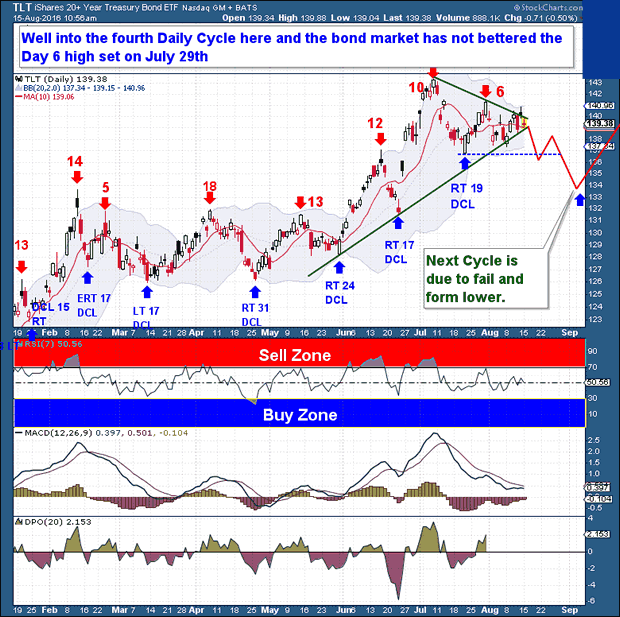

The Bond market has obviously been in a strong rally since the April Investor Cycle Low (ICL). History teaches, however, that even during solid bull market moves, corrections into major Cycle Lows are a normal part of the Cycle flow process.

And this is where we find Bonds today. The Commitment of Traders report shows a massive Long speculative position, while overall Bond Sentiment remains sky-high. Weekly Cycle timing is well into its topping range, and the 4th Daily Cycle (shown below) is beginning to struggle. I would never count Bonds out, at least until we see a failed Daily Cycle, but I am starting to believe that a new down leg in Bonds is almost upon us.

A technical caution – if price were to move higher and exceed the current day 6 high, a bullish continuation is possible. For the bulls, loss of the 10-day moving average would be extremely negative, as it would signal a potential downturn and Left Translated Daily Cycle.

The Financial Tap – Premium

The Financial Tap publishes two member reports per week, a weekly premium report and a midweek market update report. The reports cover the movements and trading opportunities of the Gold, S&P, Oil, $USD, US Bond’s, and Natural Gas Cycles. Along with these reports, members enjoy access to two different portfolios and trade alerts. Both portfolios trade on varying time-frames (from days, weeks, to months), there is a portfolio to suit all member preferences. NOTE: special offer SIGN UP PAGE!

….related: Big Hitters Warn Of Market Meltdowns

What is the true value of the Italian banking system?

We have heard a lot of different opinions concerning the European and, in particular, the Italian banking system, both positive and negative, depending upon the source: let’s try to make things clear.

The Italian premier, Matteo Renzi, told the American Cnbc that the stress tests, led by the EBA (European Banking Authority), showed Italian banks are not the main problem of the European banking system: definitely true since 8 credit institutions failed and only Monte dei Paschi di Siena and Unicredit are Italian.

The list includes the German Commerzbank, the Irish AIB, the British Barclays, the Austrian Raiffeisen Landesbanken and the Spanish Banco Popular; those banks recorded a capital level below the 7.5% limit in case of a negative scenario.

We cannot avoid mentioning the embarrassing -2.4% of Monte dei Paschi di Siena: the only one with a bankruptcy risk in case of adverse situations.

7% is usually considered to be the level triggering the devaluation of bonds and the Italian banking system, with an average of 7.6% of the capital, Italy has been among the weakest in the European area, after Ireland and Austria.

On the other hand, Italy also has the best bank with Intesa San Paolo which scored an outstanding result.

Now we need to look deeper inside Mps and Unicredit to understand the real situation and what the Italian government and the bank’s management are planning to do in order to safeguard customers’ savings.

Mps presents a critical situation due to financial debts which are five times higher than its equity in 2015 and strong losses from 2011 to 2014 as you can see in the picture below which shows the main data and the related growth.

Click on the image below to enlarge it

Unicredit is in a different situation since they have less net losses at the end of the last 5 years than Mps with some positive results, yet the same situation when we compare financial debts with total equity. This is even one of the largest credit institutions in Europe and the biggest in Italy with one of the highest capitalizations: too big to fail? no, it isn’t. We have already heard these words but we can say the situation is still under control.

The market’s reaction after the stress tests results has been strong with peaks of -16% for Mps and -7% for Unicredit.

Other Italian banking titles have maintained the same trend for years and we strongly believe that this is the right moment to buy them after an accurate technical and fundamental analysis.

Basically it is true that there is a problem of uncollectible receivables inside the banking system, but not as serious as described by the mass media all around the world. The international speculation has done much to lower stock prices so that foreign investors are able to purchase Italian companies at discounted prices

We analyze balances every day and their Fair Values are all higher than current prices. For example, we take a look at the Banca Popolare di Milano’s Fair value and, as displayed in the picture below, the current price is strongly inside the buy range.

We analyze balances every day and their Fair Values are all higher than current prices. For example, we take a look at the Banca Popolare di Milano’s Fair value and, as displayed in the picture below, the current price is strongly inside the buy range.

Brought to you by

As rates on government bonds have gone negative in Europe and Japan, the above companies have been big buyers of US Treasury bonds, which still (for some reason) continue to offer positive yields. But according to a Bloomberg analysis published today, Treasuries’ positive yield has recently evaporated when the cost of hedging currency fluctuations is included. Here’s an excerpt: ….related: ‘Soon’ And ‘Really, Really Crazy’: Starting Up The Helicopters

There are four stages of fiat money printing that have been used by central banks throughout their horrific history of usurping the market-based value of money and borrowing costs. It is a destructive path that began with going off the gold standard and historically ends in hyperinflation and economic chaos. Stage one is the most benign of the four, but it sets the stage for the baneful effects of the remaining three. The first level of monetary credit creation uses the central banks’ artificial savings to set short-term interest rates through the buying and selling of short-duration government debt. This stage appears innocuous to most at first but is insidiously destructive because it prevents the market from determining the cost of money. This is crucially important because all assets are priced off of the so called “risk-free” rate of return. A gold standard keeps the monetary base from rising more than a few percentage points per annum and thus restrains bank lending. However, having a fiat currency also means a nation has a fiat monetary base. This leads to unfettered bank lending and the creation of asset bubbles. The second stage of monetary madness has been around for decades but is now commonly known as Quantitative Easing (QE). After several cycles of lower and lower short-term interest rates that are intended to bring the economy out of successive recessions, the central bank (CB) ends up pegging rates at zero percent or below. Once CBs run out of room on the downside of short-term rates they go out along the yield curve and begin to artificially push down borrowing costs for long-term debt. It is important to note that at this stage CBs only purchase assets on private banks’ balance sheets and at least pretend they will someday liquidate these holdings. also from Marc Faber: also from Marc:

“Central banks are now talking about helicopter money. The Federal Reserve will also introduce QE 4 (another round of quantitative easing),” also from Marc:

Negative interest rates are an existential threat for insurance companies, pension funds and other financial entities that need positive investment returns to survive.

Negative interest rates are an existential threat for insurance companies, pension funds and other financial entities that need positive investment returns to survive.

I think money printing in the one or the other form will continue. Now increasingly central banks and fund managers and treasury departments are talking about helicopter money. Helicopter money you don’t just buy securities that are traded in the public market like treasuries or sovereign bonds and equities, but you essentially distribute money to each individual. Distributing money is like a tax cut but whereas the tax cut only flows to people that actually pay tax, pay federal tax in the US and roughly half of Americans do not pay Federal tax. So, that tax cut is not taxing everybody but if I send a cheque to every man, woman and child for USD 10000 then he gets that money and he can then go and spend that money, for a month or two that obviously boosts economic activity unquestionably but then comes the question, who finances this? So, what can happen in this helicopter money is that the treasury issues bonds that investors would buy or the treasury just gets the money from the Federal Reserve, so that is another form of money printing.

I think money printing in the one or the other form will continue. Now increasingly central banks and fund managers and treasury departments are talking about helicopter money. Helicopter money you don’t just buy securities that are traded in the public market like treasuries or sovereign bonds and equities, but you essentially distribute money to each individual. Distributing money is like a tax cut but whereas the tax cut only flows to people that actually pay tax, pay federal tax in the US and roughly half of Americans do not pay Federal tax. So, that tax cut is not taxing everybody but if I send a cheque to every man, woman and child for USD 10000 then he gets that money and he can then go and spend that money, for a month or two that obviously boosts economic activity unquestionably but then comes the question, who finances this? So, what can happen in this helicopter money is that the treasury issues bonds that investors would buy or the treasury just gets the money from the Federal Reserve, so that is another form of money printing.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair