Bonds & Interest Rates

We’re going to talk about bonds today but before we get to that, I want to briefly point out why the Brexit event is impacting US markets so heavily.

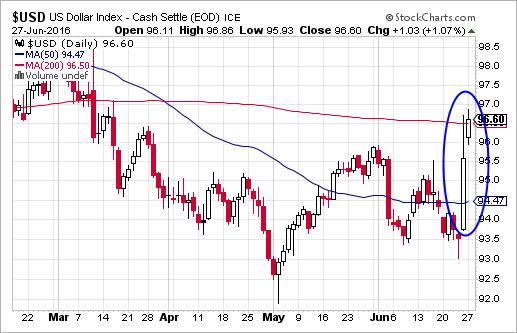

As we’ve discussed many times here at DTL, the strength of the US dollar dictates the cost of US goods to our trading partners. When the dollar goes down, our goods go on sale; when the dollar goes up, it’s equivalent to a price hike across the board. And it goes without saying that higher prices stifle demand, which means less revenue, profits, etc.

With Europe thrown back into turmoil, investors are flocking to the US dollar for safety. This is how the dollar reacted on Friday and Monday.

related:

Be sure to read Martin Armstrong’s work:

Another down day for the Dow on Friday left it in the red for the week.

Barron’s, in a lather, says it is facing the “Two Horsemen of the Apocalypse.”

Huh?

Supposedly, the so-called Brexit – the vote in Britain this Thursday on whether to leave or remain in the European Union (EU) – and uncertainty over where the Fed will take U.S. interest rates are cutting down stocks faster than a Z-turn mower.

Doomsday Device

But Brexit is a side show.

As our contacts in London explained in last week’s issue of Bonner & Partners Inner Circle, Britain will do just fine outside of the EU. It will even thrive. [Inner Circle members can catch up here.]

As for the Fed’s fumbling, it is a consequence, not a cause, of falling stock prices.

As for the Fed’s fumbling, it is a consequence, not a cause, of falling stock prices.

The real threat to this market is more basic… more dangerous… and completely unavoidable. It is a “doomsday device” – hidden in plain view – in the feds’ fiat money system.

It took us a long time to understand how this works. For many years, we referred to the Fed’s EZ money policies as “printing money.” Finally, we realized that this metaphoric description of the Fed’s role probably hides more than it reveals.

The Fed is not printing money. If it were printing money, we’d have more money around… and higher consumer prices.

Instead, when the feds went to a “paper” money system in 1971, they did it very cleverly.

Yes, their new system is totally fraudulent and absolutely ruinous – just like an old fashioned money-printing scheme. But the fraud takes much longer to uncover… and the ruin is only obvious at the end.

It is a “bezzle”… where you only become aware that you’ve been had when it blows up.

Unlimited Credit

Here’s the deal…

Instead of printing money itself, the Fed allows banks to create an almost unlimited amount of credit (providing they meet certain capital requirements).

Contrary to popular belief, banks don’t act as “warehouses” – taking in deposits and then lending them out again. Instead, banks create new deposits (aka money) when they make a loan.

All it takes is a few strokes on a keyboard, and account balances – along with the money supply – go up.

At first, this new credit-money acts much like printing-press money: It gives people money to spend that nobody ever earned. Everybody is happy.

But if you keep on creating more and more paper money, the fraud is soon obvious. Prices rise. People realize that they have no more purchasing power than they had before.

In the meantime, businesses and consumers have all made bad decisions, based on the apparent increase in “demand.”

After a while, all those mistakes have to be flushed out… in a recession or a depression.

Problem Postponed

By setting up this credit-money system, on the other hand, the feds avoided that problem… or at least, postponed it.

Between 1980 and 2016, for example, Americans spent $32 trillion in net, excess credit. That’s credit (and debt) above and beyond the historic relationship between GDP and debt.

That, too, would have increased consumer prices dramatically, but the Japanese… and then the Chinese… were busily making things much more cheaply.

This offset consumer price increases. And more important, much of the increase in credit-money went directly into Wall Street, instead of the Main Street, economy.

In a credit-money system, the sectors of the economy that are most creditworthy get most of the new money.

Who’s most creditworthy?

The rich. Big business. Government.

Prices soared, all right. But they were the kinds of prices people wanted to go up. Houses… businesses… commercial real estate… collectibles – talk about inflation; these things went through the roof.

Everything that can be financialized – priced and traded – became incredibly expensive. But the price of labor went nowhere.

The Rich Get Richer

Almost unbelievably, according to the Pew Research Center, today’s average hourly wage has roughly the same buying power as it did in 1973 – more than 40 years ago.

The system hasn’t done much for the common man, but it has helped the rich get richer. And now we know that the Deep State controls the U.S. government (and indirectly, the Fed and the financial system). So nobody really cares about the voters anyway.

What a system!

The banks are allowed to create money. They lend it to consumers until the household sector can’t take anymore. (This is what happened in 2008). Then they lend to corporations and the government.

One by one, each sector takes on too much debt and ceases to be creditworthy. Finally, only government can borrow… because it is the only sector that can print money!

We’re approaching that already in Japan, where the central bank buys about 100% of new Japanese government debt issuance.

Recession Warning

If the feds had handed out paper money, prices would have gone up. But even in a recession, or a debt deflation, the cash would still be there. Printing-press money raises prices, permanently.

But a credit-money system is very different. Every new dollar that comes into the system is also another dollar of debt.

Now, American consumers, businesses, and government all drag behind them about $60 trillion in debt. It slows them down. It depresses economic growth. And most important, it is subject to the credit cycle… and to the “doomsday device” built into system.

A recession is coming in the U.S.

If it hasn’t already begun, it will probably set in within six months. When that happens, stock prices will fall.

This will have a similar effect as the 2008 crisis… when houses plunged. Ultimately, a company’s earnings potential and stock market equity provide the collateral for its debt. When the stock market falls, lenders disappear.

Then, the debt market tightens and the doomsday device explodes.

Debt is just the flip side of credit. As debt goes bad, credit disappears. And then the system that created so much credit-money will go into reverse, destroying the nation’s money supply.

The money supply (actually, the supply of ready credit) will shrink – suddenly and dramatically. And what should have been a minor, routine pullback in the economy will become a catastrophic panic.

Don’t go away!

Regards,

Bill

related: The Fed Just Lost All Credibility

The central banks have risked it all and lost. They have reached the point of no return. The Fed decided not to raise rates, which are desperately needed to prevent a collapse in pensions and insurance companies, and merely froze like a deer in headlights. The superficial analysts who think lower rates are good for the stock market are blinded by their own stupidity. The theory that low rates will encourage people to buy stocks is brain-dead and demonstrates that these people are incapable of comprehending how the economy functions.

We have taken simple correlations of interest rates and the stock market and discovered something in plain sight. The market has NEVER peaked with the same level of interest rates in history. WHY? It is not the empirical level of interest rates that matters, rather it is the rate of interest that is a factor of expected inflation. Therefore, if the expectation of gain is greater than the rate of interest, there is profit in borrowing. If the expectation is below the rate of interest, then the rate must decline. Consequently, assuming that simply raising or lowering rates will reverse the trend is primitive and lacks any analysis whatsoever.

The central banks have gone way too far and are now trapped. They do not have the ability to influence the economy anymore for they are loaded with government debt that will default. They have converted government bonds into one of the riskiest asset classes of all time.

More and more of our institutional clients (pensions & insurance) are bailing out of government bonds and switching to corporate. Why? No major corporate debt becomes worthless. One was audited by S&P and they remarked that they were taking on more risk. They conducted their own studies to verify what we have been saying and found no corporate defaults, but countless government defaults and partial defaults. In the few rare cases of a default, you receive a payout after liquidation. In the case of government debt, you have something to frame and that is all. Government debt is unsecured and since they have the guns and the armies, you cannot force them to pay anything.

Some insurance companies have come out and stated publicly that they are selling government debt and moving to corporate. Swiss Re AG moved more of its investments into corporate debt as conceded by its chief investment officer who said, “If you’re looking for a bubble, here you go…With government bonds, you’re not adequately compensated for the risk you’re taking.”

We have been in meetings with pension funds. Here too, we find the same response. They are starting to shift. Government debt has become a time bomb. A simple 1% rate hike will be devastating to bond values and blow the budgets of government sky-high.

The European Central Bank has created a total mess of the European banking system. Negative interest rates have been devastating. Now in the Middle East, the National Bank of Abu Dhabi and First Gulf Bank PJSC are exploring a potential merger to create the largest lender in the Middle East. But forget the fluff — banks do not merge unless there is a problem. Rumors behind the curtain say First Gulf Bank PJSC is in trouble.

Negative interest rates have destroyed much of the economy. The rise in regulations and taxes have combined to create the weakest recovery in the United States post-Great Depression. This is not going to end nicely. It is only a matter of time before the general public begins to see the real crisis, and then everything will explode in their faces.

More from Martin: Retail Sales of US Equities (Domestic & Foreign) Reaching Historical Low

Fed officials try to understand why they cannot keep raising rates

FOUR times a year the meeting of the Federal Open Market Committee, the Federal Reserve board that sets monetary policy, concludes with a special flourish: a press conference, and the publication of the members’ economic projections. The latter includes a “dot plot” which shows how members think rates will unfold over the next few years. When the new dots were released at the end of the June meeting, on the 15th, it quickly became clear that one was not like the others. FOMC members overwhelmingly see the Fed’s main interest rate rising to between 1% and 2% in 2017, then on to between 2% and 3% in 2018: all of them, that is, except one. That oddball member projected the interest rate would stay right about where it is now over the next two years. When the projections dropped, Fed watchers immediately speculated about just which member had turned super-dovish (or super pessimistic).

Two days later, all was revealed....continue reading HERE

related: The Fed Just Lost All Credibility

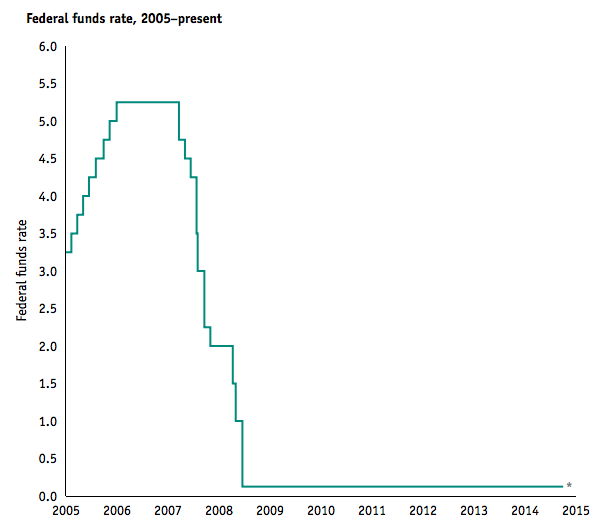

Yesterday the Fed failed to raise rates… again.

It’s pretty incredible if you step back and think about it. Here were are, seven years into a supposed recovery, and the Fed’s actions tell us the economy cannot handle rates higher than 0.5% (the overnight benchmark rate fluctuates between 0.25% and 0.5%).

Rates of 0.5% (and lower) and the word “recovery” do not belong together. The Fed is currently maintaining rates at levels usually reserved for dealing with Crises, NOT recoveries. Heck, the Fed kept rates higher than current levels during the recession following the TECH BUST.

Put another way, seven years into this “recovery” the Fed views the economy as weaker than it was after the Tech Bubble burst in 2002.

At this point, after seven years of ZIRP and $3.5 trillion in QE, shouldn’t we consider alternatives? Maybe we might want to let some other people try running the economy for a change?

After all, if you spent $3.5 trillion and the best you can garner is a recovery that is weaker than the 2001 recession… maybe you’re not cut out for the job of “fixing” the economy.

Moreover, at what point do we start questioning the Fed’s data?

Back in 2012, the Fed claimed it would start to raise rates when unemployment fell to 6.5%. We hit that target over two years ago in April 2014.

The Fed also claimed it would raise rates when inflation hit 2%. Core inflation has been above that level for five months now.

Now the Fed claims that it is concerned about Brexit or China or who knows what, as an excuse not to hike rates.

But the Fed didn’t just fail to hike rates. It also lowered its rate hike forecast to just one rate hike this year (down from two) and possibly three rate hikes next year (down from four).

Despite these dovish developments, stocks cratered. It if weren’t for the usual desperate PPT manipulation, we’d probably have had a mini-Crash.

We may have reached the point at which the Fed has lost all credibility.

The markets are in a massive bubble. The S&P 500 is sporting an EV/EBITDA of over 10. There is simply no way on earth this is not a bubble. Indeed, this reading is even higher than the S&P 500’s EV/EBITDA in 2007: a period that everyone agrees was a bubble.

Earnings are at levels not seen since 2012. Meanwhile stocks are 70% higher than they were during that time.

Meanwhile, bonds or the “smart money” are not buying this rally in stocks at all.

We are heading for a crisis that will be exponentially worse than 2008. The global Central Banks have literally bet the financial system that their theories will work. They haven’t. All they’ve done is set the stage for an even worse crisis in which entire countries will go bankrupt.

Best Regards

Graham Summers

Note: For a 21-page investment report titled the Stock Market Crash Survival Guide Phoenix Capital Research is giving away just 1,000 copies of this report for FREE to the public. If there are any left pick up yours at: https://www.phoenixcapitalmarketing.com/stockmarketcrash.html

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair