Bonds & Interest Rates

One of the oddest things in this increasingly odd world is the spread of negative interest rates everywhere but here. Why, when the dollar is generally seen as the premier safe haven currency, would Japan and much of Europe have government bonds — and some corporate bonds — trading with negative yields while arguably-safer US Treasuries are positive across the entire yield curve?

One answer is that the Bank of Japan and the European Central Bank are buying up all the high-quality (and increasing amounts of low-quality) debt in their territories, thus forcing down rates, while the US Fed has stopped its own bond buying program. So the supply of Treasury paper dwarfs that of German or Japanese sovereign debt. Greater supply equals lower price, and lower price equals higher yield.

The other answer is that this is just one of those periodic anomalies that persist for a while and then get arbitraged away. And Brexit might be the catalyst for that phase change.

It’s not clear that the UK leaving the EU will cause any real near-term problems. But the fact that it might happen at all is setting off a “who’s next?” contagion in which the viability of the EU itself is called into question. From earlier this week:

Biggest Brexit fear is really end of European Union as we know it

(CNBC)- European Council President Donald Tusk became the latest official to voice those concerns. In an interview with German newspaper Bild, Tusk said a Brexit vote to leave would be a boost for anti-European interests who would be “drinking champagne.”

“As a historian, I fear that Brexit could be the beginning of the destruction of not only the EU but also of western political civilization in its entirety,” he said in the interview. Tusk said the long term consequences are difficult to see but that every nation in the EU would be hurt economically, particularly the U.K.

This is the kind of sentiment that leads to extreme risk-aversion. And what, in the financial world, is safer then Treasury bonds when “Western political civilization” is in jeopardy? So a torrent of terrified global capital might soon be pouring into the US, pushing bond prices up and interest rates down. US Treasury yields, as a result, might behave the way German rates have since Brexit became conceivable:

Treasuries are already trending in that direction. From today’s Wall Street Journal:

U.S. 10-Year Government Bond Yield Falls to Lowest Since 2012

The yield on the benchmark U.S. government note closed at the lowest level since December 2012 on Tuesday as the yield on Germany’s 10-year debt fell below zero for the first time on record.

Tuesday’s move extends the record declines in high-grade global government bond yields, reflecting investors’ consistent concerns over sluggish global economic growth and the limit major central banks are facing in boosting growth via their unconventional monetary stimulus.

“It’s amazing. I never thought I’d see the day where 10y German rates would go negative,” said Anthony Cronin, a Treasury bond trader at Societe Generale SA. “It is difficult to say what is next but it seems safe to expect money to continue to flow into U.S. Treasurys.”

Traders say investors need to buckle up for higher market volatility. The VIX, a key measure of volatility in the U.S. stock market, hit the highest level on Tuesday since February. As investors cut risk appetites, it stokes demand for haven debt.

The yield on the benchmark 10-year Treasury note fell for a sixth consecutive day and settled at 1.611%, compared with 1.616% Monday. It fell to as low as 1.569% during Tuesday’s trading. Yields fall as bond prices rise.

The yield’s record closing low was 1.404% set in July 2012. Some analysts and money managers say they expect the yield to breach that level in the months ahead.

Our ability to accept crazy new things and incorporate them into “normal” life is truly amazing. Negative rates, as the initial surprise wears off, do indeed seem to be merging into the background, becoming simply part of the financial environment.

But they shouldn’t. Some things — for instance gay marriage or drug legalization — seem revolutionary but are on balance either harmless or beneficial. But negative interest rates are indeed revolutionary in the sense that they turn the operation of capitalism on its head. In a negative interest rate world, debt generates a profit and saving shrinks capital. Governments and corporations are paid to rack up ever greater obligations and thus have no incentive to control their natural hubris. To re-purpose some of John Maynard Keynes’ words, fair becomes foul and foul becomes fair, because foul is profitable and fair is not.

This is a world, in short, where all the old limits on our worst natures are removed and anything, no matter how long-term destructive or contrary to the laws of economics, becomes permissible. And where the only possible outcome is a crisis as epic in scale as the mistakes that will bring it about.

If gold-bugs circa 2000 were asked to sit down and design an environment in which owning precious metals is an absolute no-brainer, they’d produce the following: Unrestrained government spending leading to overwhelming debts leading to debt monetization leading to universal negative interest rates. A highly-unlikely wish list that is on the verge of coming true.

related: Don’t Bank On Rate Hikes!

It was fun playing Masters of the Universe when expectations were low.

Ah, the good old days, when a simple, completely empty promise to do whatever it takes could move the world. It was fun being a central banker back in the good old days–back then playing Master of the Universe was wondrously good fun.

Now–not so fun. Now that interest rates are drifting below zero, there’s not much room for fun left in that sandbox.

As for mortgage rates: they’re so low, some countries are effectively paying people to take out a mortgage, and the resulting bubbles and market distortions are no fun.

also:

The problem is that the FED, including other Central Banks, have waited too long and gone too far in their ‘zero interest rate’ policies and ‘quantitative easing’ programs so….. Don’t Bank On Rate Hikes!

This past Friday, June 3rd, 2016, The Bureau of Labor Statistics released their most recent report regarding new employment data and nonfarm payroll employment which indicates that during May of 2016, it was the smallest increase seen in 28 months.

During May of 2016, there were 144,592,000 payroll jobs within the US, which was up by 1.6 percent, or equivalent to 2.3 million jobs, from May of 2015 (These are all not-seasonally-adjusted numbers).

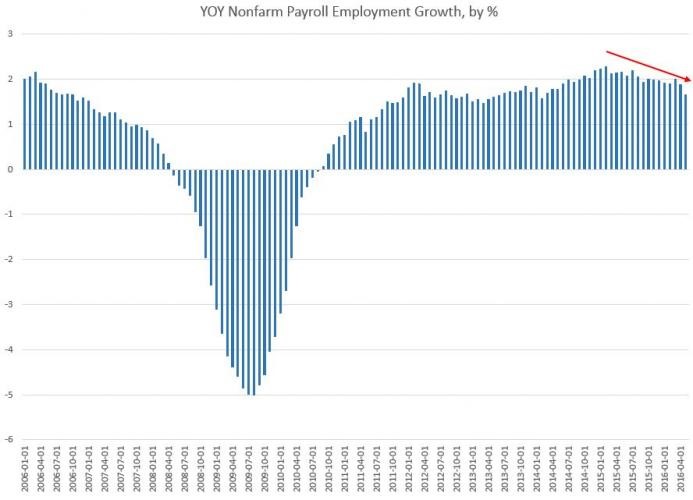

That represents the smallest year-over-year increase that has been reported since February of 2014, at which time payroll jobs increased by 1.57 percent. The largest year-over-year increase, in recent years, was reported during July of 2015, when it was up by 2.18 percent:

Since July of 2015, the general trend in growth has been down. This 1.6 percent remains well below where growth was during most of the 1990’s.

I am not fond of using the seasonally adjusted numbers, since they add an additional layer of ‘needless manipulation’. I do prefer to compare job growth, from the same time of year, over several years.

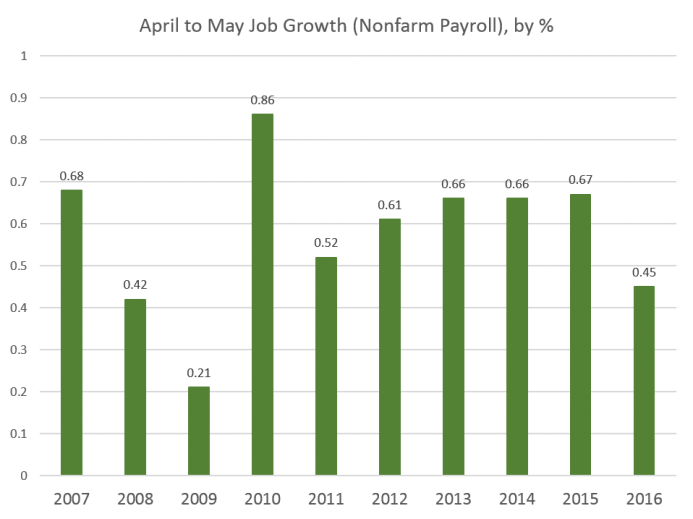

When I do this, I find that the job growth from April to May of 2016, was the lowest April-May growth total since 2009:

From April to May of 2016, there were 651,000 new jobs added, which is a significant drop from that same period of time, last year when 947,000 jobs had been added. Over the past decade, this current year of 2016, in this measure, beats out only 2008 and 2009, both of which were years of ‘economic decline’. Therefore, May of 2016 was the weakest May on record, for job growth, in eight years.

The Secretary of Labor, Tom Perez attempted to blame everything on the Verizon strike. That is a nice “spin”, however, the strike does not explain the obvious ‘decline’ in the year-over-year numbers! The strike might explain why the May numbers dropped off as much as they did, however, it cannot explain the ‘trend’. It is a bit of a stretch to blame this drop from April-May of 2015 to April-May of 2016 on the Verizon strike.

Mr. Perez, however, attempted some other, even less convincing, claims as well, stating that the U.S.’s insufficient mandates on paid family leave means that fewer women are entering the work force, and therefore pushing down the jobs totals. Is this IMPORTANT? The answer is NO! These bad numbers merely reflect our current poor economic situation, today!

In any case, the overall trend should not be a big surprise, as it has always has been weak. It has been dependent on the FED and their low interest rates. In recent quarters, the FED has finally been backed into a corner and has become hawkish. Realizing that more rate cuts are unlikely to occur any time soon, the economy is not receiving the usual FED-manufactured stimulus which investors and companies have both become accustomed to. With the FED talking about the need to raise ‘rates’, who can be surprised that the “recovery” is nonexistent?

The financial news, of the past few weeks, had its cadre of regional FED Presidents attempting to sway markets into believing that the Central Bank was sure to ‘hike’ interest rates during this current month of June 2016.

The jobs report sent ‘shock waves’ throughout the entire financial system. The report printed a jobs number of just 38,000 new employees, which is the lowest single month since the height of the “Great Recession”.

What is even more ludicrous than this, is the fact that the unemployment rate fell to 4.7 percent seeing as 664,000 workers are no longer being counted and included, by the government, within the labor force.

The FED relies heavily on these ‘manipulated’ government jobs numbers, the idea of “data dependency” being used to determine when to ‘hike’ or ‘drop’ interest rates shows the incompetency of a body that supposedly employs hundreds of economists who are dedicated to discover the true state of the economy and of its’ economic data. This in turn, should provide Americans with the reality that not only does the Central Bank have any idea what they are doing, but, more often than not their policy decisions are based on ‘incorrect’ and ‘outdated’ models which have only served to make matters worse, since the “Credit Crisis of 2008”.

The majority of jobs created were either part-time or low-wage service sector oriented. You can bank on the fact that the FED is now more likely to lower ‘rates’ than they are to raise them, going forward!

Today, it is both unlikely and irrational for the FED to raise interest rates either now or in the near future, despite the Central Banks’ recent “moral suasion” on mass media, of a potential rate ‘hike’ occurring as early as this month or possibly next month. The FED continues to create policies in an attempt to protect the economy and stock markets through November of 2016 so as to “spin” the election in favor of Hillary Clinton. This is due to the uncertainty from the presumptive Republican candidate, Donald Trump, who may force the Central Bank into ending its’ mission to fuel ‘stock and housing bubbles’. I, myself, as well as many economists, are seeing the ‘Summer of 2016’ as a dangerous period of time where and when a financial, economic, or monetary ‘collapse’ could take place from any number of ‘flashpoints’. The actions that are now taking place, in the equity markets, are an indication that these ‘fears’ may very well be arriving much sooner than most analysts expect.

The economy is still performing ‘significantly’ below its’ potential:

The problem is that the FED, including other Central Banks, have waited too long and gone too far in their ‘zero interest rate’ policies and ‘quantitative easing’ programs. With all of this nonsensical talk coming from the FED, the debt default levels, especially for credit default swaps on the 10-year Treasury are NOW at their highest level since the FED raised rates by a quarter of a point, back in December of 2015.

The probability of a U.S. default of its’ debt has hit its’ highest point since the FED has hiked rates in December of 2015. This is indicated by the recent dynamics in credit-default swap (CDS) agreements. The expectations that the Central Bank may raise borrowing costs still further, in the coming months, will set off this ‘time bomb’. Since the FED has turned increasingly hawkish of their policy outlook since late April 2016, market volatility has increased, with stocks swinging between gains and losses and U.S. Treasuries sliding along slide with the dollar. “Systemic risks” stemming from the CDS transactions are rising amidst the unfavorable global financial environment. This is not only true in the U.S., but its’ counterparts are also subject to greater turmoil in the coming months, as possible FED hikes, “Brexit” concerns, U.S. elections and faltering global growth are all interconnected factors thereby contributing to the recent spikes in U.S. CDS spreads.

If things follow the FED script, I imagine that next months’ payrolls will exceed ‘tapered down’ expectations and consequently, there will be an upward revision of Mays’ numbers. Will this continue sending the market into exuberance? NO! However, the FED officials will then restart the rate ‘hike’ talks with just enough offsetting uncertainties to mislead everyone while trying to keep the market ‘bubble’ from ‘bursting’.

The financial system is like a giant game of poker with all the major player holding a seven and two off suite (worst hand you can have), yet they are all-in with their chips (money & policies) trying to bluff their way out of this mess.

Things are going to be very crazy over the next 6-12 months and beyond, but until the US large cap stocks breakdown and start a bear market expect tough trading and investing.

Chris Vermeulen

related:

Canada’s Monetary Policy Stuck Between a Rock and a Hard Place

“The Fed seems to be constantly changing its focus from one meeting to the next. They seem to regularly promise hikes, only to back off at the last second. Fed statements often seem stale, reflecting where the economy and markets were a couple months ago, rather than current conditions. They say their 2% inflation target is not a ceiling, and yet they only plan to bring inflation back to 2%. They argue that the risks to the outlook are very asymmetric—with rates near zero they have limited anti-recession ammunition—and yet their inflation target is symmetric. This is policy transparency?”

….read more from ZeroHedge HERE

….read more from ZeroHedge HERE

related:

Canada’s Monetary Policy Stuck Between a Rock and a Hard Place

The U.S. economy created the fewest number of jobs in more than 5-1/2-years in May as manufacturing and construction employment fell sharply, suggesting slippage in the labour market that could make it harder for the Federal Reserve to raise interest rates… CLICK to read the complete article

The U.S. economy created the fewest number of jobs in more than 5-1/2-years in May as manufacturing and construction employment fell sharply, suggesting slippage in the labour market that could make it harder for the Federal Reserve to raise interest rates… CLICK to read the complete article

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair