Bonds & Interest Rates

“Crises refine life. In them, you discover what you are.” ~ Allan K. Chalmers

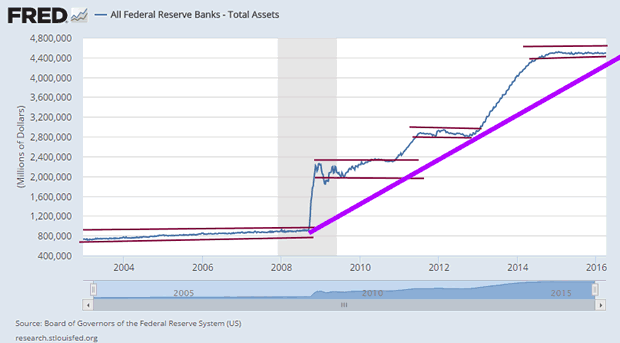

What strikes one immediately is that the Fed has been creating money hand over fist; one hand they create money, with the other hand they buy assets and put it on their books, all looks well until you realize this is something called monetization of debt. Paper buying more paper and in most nations this leads to hyperinflation and a currency collapse. However as the Dollar is the world reserve currency. The Fed can magically create money out of thin air and use this newly created money to pay bills and or prop up markets as is currently the case.

Look at how the total assets of the Fed have skyrocketed since 2004. You will also notice that we have nice channel formations where nothing happens for awhile and then suddenly the Fed’s assets explode. One hand starts to print while the other hand uses this newly created money to buy treasuries, etc.; it’s nothing but one big Ponzi scheme. It has not collapsed because the masses are still asleep and show no signs of waking up so it will go on for a significantly longer period. Translation, the markets will not be allowed to stay down for the count for too long. In other words, strong corrections should be viewed as buying opportunities.

Look how CNBC aired in 2009: in this video one of the members openly describes what is essentially a Ponzi scheme, but the CNBC host goes on to say, well we have a better term for that it’s called “debt monetization” but that is just a nice word for outright robbery and theft.

The market is going to trend higher in such an environment; sure it’s going to be a volatile ride up, but the markets will be spending more time to the upside than to the downside. Hence, all strong corrections/pullbacks have to be viewed through a bullish lens. Lastly, it would be prudent to allocate some money to Gold bullion; look at it as a form of insurance against an unforeseen event.

“Man is not imprisoned by habit. Great changes in him can be wrought by crisis — once that crisis can be recognized and understood.” ~ Norman Cousins

related:by Martin Armstrong: Full Blown Panic at the Fed?

Someone seems to have hit the emergency button at the Fed, as even though the central bank said that everything was just fine with the American economy just a few weeks and months ago, the situation has currently escalated into a full-blown panic mode.

Someone seems to have hit the emergency button at the Fed, as even though the central bank said that everything was just fine with the American economy just a few weeks and months ago, the situation has currently escalated into a full-blown panic mode.

On Thursday, the Board of Governors of the Federal Reserve has called an ‘emergency’ meeting for Monday, April 11.

related:

Martin Armstrong: ECB Losing Control

“Earnings don’t move the overall market… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.” Stanley Druckenmiller

Global liquidity conditions, as measured by BofA Merrill Lynch’s Global Liquidity Tracker, are still firmly in negative territory since mid-2015 (bottom panel). The most recent data shows a steep drop related to Japan, with three of the four components (Japan, Euro Area, and Emerging Markets) now below zero. Though the US is fractionally positive at 0.75, the continual tightening of liquidity conditions abroad is the greatest risk currently, aligning with Yellen’s cautious remarks on raising rates.

“We may well at present be seeing the first stirrings of an increase in the inflation rate.”

—Stanley Fischer, Vice-Chairman, Federal Reserve

There should be an “immediate increase in rates.”

—John Williams, President, Federal Reserve Bank of San Francisco

“I think the evidence indicates that inflation expectations remain well anchored. I am reasonably confident that, barring subsequent shocks, inflation will move back to the FOMC’s 2% objective.”

— Jeffrey Lacker, President, Federal Reserve Bank of Richmond

Are interest rates headed higher?

If you believe Janet Yellen’s ad nauseam promises that the Federal Reserve’s decision to increase interest rates is totally “data dependent,” then you should expect interest rates to move higher.

I say that because of the line of data points pointing toward an uncomfortable increase in inflation.

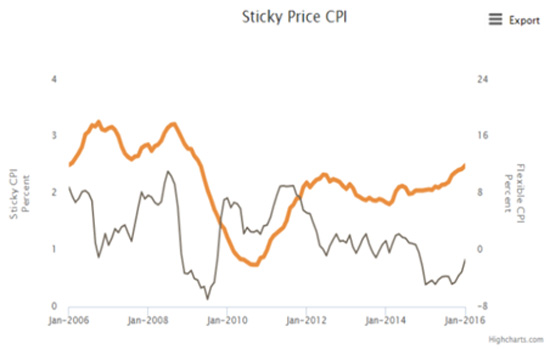

The Atlanta Fed’s measurement of what it calls “sticky price” inflation jumped to a post-Financial Crisis high of 3% in February. This index is a measure of core inflation.

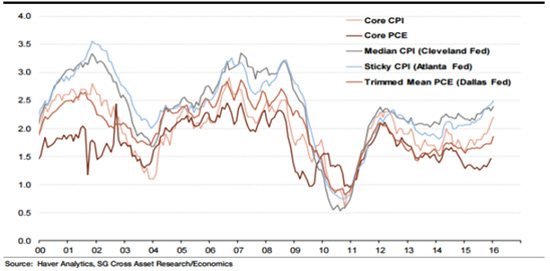

What’s more, the Cleveland Fed reported that its CPI index jumped to 2.9%—largely from big price increases in medical services, housing rents, car insurance, restaurants, hotels, and women’s clothing.

Inflation was nowhere to be found for years, but the evidence is mounting that we are at an inflation inflection point.

Our economy is already fragile, but I want you to remember that economic expansions seldom die of old age. Instead, they are killed by idiot central bankers. In fact, every major US recession since World War I has been caused by the Federal Reserve attempting to kill off inflation.

I have no reason to think that Janet Yellen and her Fed buddies are any smarter than our previous central bankers, so my expectation is for them to screw things up like their predecessors always have.

When that happens, income investors with a big weighting of long-term bonds are going to get clobbered. Fortunately, there is a new breed of ETFs designed to prosper when interest rates are rising:

iShares US Treasury Inflation Protected Securities ETF (TIP): This ETF invests in US government bonds whose value adjusts with inflation.

ProShares Investment Grade—Interest Rate Hedged ETF (IGHG): This ETF invests in investment-grade bonds while adopting short positions in US Treasury bonds of approximately the same duration. This ETF seeks to achieve an overall duration of zero.

SPDR Citi International Government Inflation-Protected Bond ETF (WIP): This ETF buys inflation-protected bonds issued by foreign governments, such as the UK, France, Italy, Sweden, Brazil, Turkey, Australia, Canada, and Mexico.

Sit Rising Rate ETF (RISE) is an ETF designed to profit from increases in short-term interest rates. This ETF shorts the shorter end of the yield curve, which are the bonds most affected by Federal Reserve rate hikes.

As always, timing is everything, so I’m not suggesting you rush out and buy any of these ETFs tomorrow morning. But if you’re worried about a return of inflationary pressures and Fed rate hikes, the above ETFs are worth your consideration.

Also, check out my monthly newsletter Yield Shark where I recommend the best dividend-paying stocks with inflation-beating yields and great upside.

Tony Sagami![]()

30-year market expert Tony Sagami leads the Yield Shark and Rational Bear advisories at Mauldin Economics. To learn more about Yield Shark and how it helps you maximize dividend income, click here. To learn more about Rational Bear and how you can use it to benefit from falling stocks and sectors, click here.

Hindsight is 20/20. That being said, 2015 saw a bull run in the US dollar that was forecast by many credible analysts. The year also saw commodities tumble and other assets that are negatively correlated to the US dollar show weakness, particularly the Canadian dollar. Now, looking ahead to 2016, the Bank of Canada is no longer viewed or anticipated to be more accommodative. The federal government has planned stimulus spending to ‘invest’ in the Canadian economy. And surprisingly, we have seen somewhat strong economic indicators in the first few months of 2016 despite heightened levels of uncertainty from the global economy over same time period.

Hindsight is 20/20. That being said, 2015 saw a bull run in the US dollar that was forecast by many credible analysts. The year also saw commodities tumble and other assets that are negatively correlated to the US dollar show weakness, particularly the Canadian dollar. Now, looking ahead to 2016, the Bank of Canada is no longer viewed or anticipated to be more accommodative. The federal government has planned stimulus spending to ‘invest’ in the Canadian economy. And surprisingly, we have seen somewhat strong economic indicators in the first few months of 2016 despite heightened levels of uncertainty from the global economy over same time period.

It’s worth reconsidering what factors drove the loonie and oil prices to the levels they are today. A major contributor to sharp movements in the global currency markets was the US Federal Reserve out in front in terms of tightening monetary conditions. With steadied and continued improvement in the US labour market, the Fed prepared to gradually raise their key policy interest rates. And, with regards to commodities markets, the world economy faced both weakening demand, particularly from China and the emerging economies and an oil supply glut that focused heavily on shale production in the US.

The reason it’s worth revisiting those two aforementioned factors that caused such disruption for global markets, is because they currently remain at the forefront of what’s driving investment markets. Janet Yellen was speaking at the Economics Club of New York this past week, and seemed to do a course change on how the Fed views international developments. What was previously not a concern of the US Federal Reserve and just a mere acknowledgment in their prior policy statements suddenly became a focal point of Ms. Yellen’s speech. Following the Fed’s initial rate hike in December, anticipation was for four additional quarter point moves this year. Now the question is whether there will even be two.

Regarding commodities, there is still clouded uncertainty over whether OPEC members will come together to cut production levels and assist in putting a floor under the oil market. This question will have greater clarity by the middle of this month when OPEC and Non-OPEC producers meet, but at this time oil prices are a factor that continues to weigh on commodity markets, as the possibility of lower prices is continuously debated.

This in essence represents Yellen’s paradox, and it seems she is willing to delay and shift back to a wait and see approach. Her enigma is heightened by the fact that a strong US dollar stemming from central bank policy in tandem with a supply glut in commodities led to dogged market volatility. Many of her fellow Fed members have been vocal these past few weeks, and appeared ready to continue to hike rates. Other members, including Yellen, have seen how a strong US dollar has challenged the US economy with the expectation of a Fed rate anticipated with a vibrant US labour market. While waiting, however, the Fed risks their credibility of being able to raise interest rates as they had previously guided investors to believe.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair