Bonds & Interest Rates

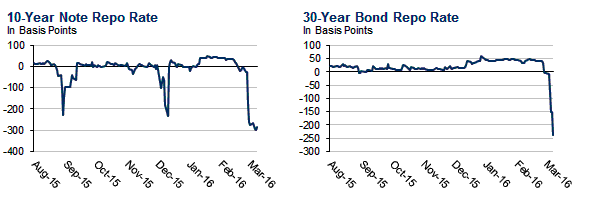

Earlier this week, when looking at the rapidly fraying dynamics in the all-important Treasury repo market, we explained that as a result of the unprecedented, record shortage of underlying paper, the repo rate for the 10Y has plunged to the lowest on record (and even surpassing it on occasion), the -3.00% “fails” rate, an unstable, broken state characterized by a surge in failures to deliver and receive, when one party fails to deliver a U.S. Treasury to another party by the date previously agreed by the parties. Think of it as a margin call issued on a stock in which the responsible party refuses to comply, and is instead slapped with a token penalty, or “fails” fee.

This is precisely what has been going on with the Treasury market for over a week, ever since last Friday when we first pointed out the precarious collapse in the repo rate on the 10Y – traditionally the best indicator of stress in lending markets.

There was some expectation that after this week’s 10Y and 30Y auctions, that the shortage would moderate, however so far that has not happened, and now the last possible renormalization date is when these auctions settle early next week.

For now, however, things are going from bad to worse, and as Stone McCarthy shows in the following two charts, it is no longer just the 10Y which is in trouble: so is the 30Y, which as of this morning is trading near the fails range, or -2.40% in repo.

The S&P 500 may yield just 2.2% today – but if you smartly invest in stocks that specialize in profitable niches, you can collect 6-11% yields right now. With double-digit price upside to boot!

Real Estate Investment Trusts (REITs) are some of my favorite vehicles for specialization and yield. REITs must have 75% of their assets in actual real estate and earn 75% of their income from those assets. These dividend machines are legally required to pass along at least 90% of their earnings to shareholders.

This is actually the best time to buy REITs this decade. The Vanguard REIT Index ETF (VNQ) pays 3.9% today – just about its highest since 2009. You’ll bank easy double-digit gains buying high quality REITs when their yields are high.

Of course, we must make sure the dividends are well funded, and preferably growing. Which is why I love REITs that specialize. The more unique the focus, the better. It means less competition, and higher rents.

Last week I shared my favorite office REITs – good plays on a quietly booming job market. Today I’ve got 4 unique niche REITs to share with you. They all have natural competitive moats and rising rents powering their big yields.

Four Specialized REITs With Yields Up To 11%

There is money to be made so the game must be played… It’s always “ShowTime” in the financial markets. What is the game plan?

Levitate the bond market. See chart below. Keep those interest rates dropping so the bond market continues its 35 year climb. Oops – $7 Trillion in bonds with negative interest rates, at last count, with more from Japan this week. Have we reached a limit? Probably not, but what could go wrong lending money to insolvent governments who guarantee they will return less than they borrowed in 10 years?

Currencies must retain some purchasing power. No Argentina or Zimbabwe devaluations will be allowed. When the dollars/euros/yen/pounds barely buy groceries the crowds will get restless and that must be avoided. So keep the currencies strong – which is code for devalue them slowly enough that people don’t riot. Remember when you could deliver a baby in a hospital in the U.S. for under $100? Really! It was a long time ago and the dollar has devalued considerably since then.

Increase debt exponentially. The bubbles must not implode and that requires continual inflating and massively more debt each year. What could go wrong with exponential debt increases? Hint: One penny invested at 6% per year for 1,000 years exponentially grows to $200,000,000,000,000,000,000,000. (Yes, really!) Exponential growth of debt mathematically cannot continue forever.

Allow gold to increase in price slowly, BECAUSE IT MUST, but fight it every step of the way. They own the media, the markets, and the High-Frequency-Traders so they use them to discourage gold purchases and promote paper debt, paper stocks, paper bonds, and digital bank accounts. Sell the paper story – HARD!

Keep the churn in play. Take your slice of every transaction, every credit card charge, every debit card transaction, and bring in the “big guns” to sell the “war on cash” so all those unbacked fiat currencies remain in digital form in a bank – easy access you know …….

The next crisis will be funded by depositors. Yup, that means us. But it can’t happen in my country …… Don’t be naïve!

Distractions are critical. Elect a president every four years, as if it matters. How about a war in Syria? A terrorist attack in some major city? Zika virus? A Kardashian scandal? Russia on the move? Chinese market crash? Don’t forget to blame someone else, and keep the money churning!

Play your own game, exit the “digital money churn,” and reduce your “financial paper footprint.”

Watch Tom Cloud’s latest market commentary – a short video.

Stack gold and silver. You can buy from Tom Cloud and Why Not Gold.

Gary Christenson

The Deviant Investor

Moody’s lowered its outlook on China’s credit rating stable to negative. We have been warning that our models on China indicate that the bottom in the economy does not appear likely until 2020. This should be a 13-year contraction. So far, that forecast appears to be on target.

Moody’s lowered its outlook on China’s credit rating stable to negative. We have been warning that our models on China indicate that the bottom in the economy does not appear likely until 2020. This should be a 13-year contraction. So far, that forecast appears to be on target.

« Australia Is Hunting for People Who Use Business Cars to Go to Sports Games

First, it was Kinder Morgan (KMI). Then, ConocoPhillips (COP). Which sacred dividend is going to get cut next?

Regular readers know that I believe big oil is a big avoid for now. But if you insist on speculating in the goo patch, stick with Exxon (XOM).

There are payout problems outside of energy, too. A quick look at Reality Shares’ DIVCON screen reveals seven 4% payers in “DIVCON 1” territory. This means they’re more likely to cut their dividend than raise it. Let’s discuss these, and a few more high yielding problem children.

1 Shaky Telecom

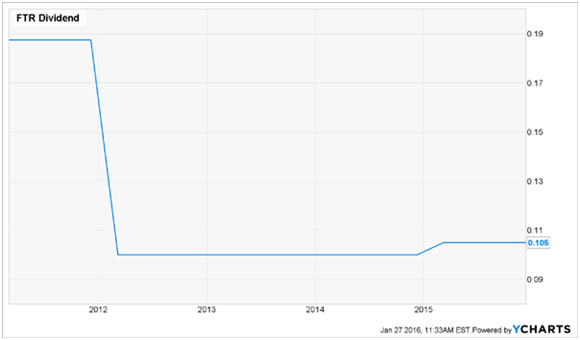

Frontier Communications Corp. (FTR) is a good example of a sky-high yield (8.8%) that should set off alarm bells. As for a low P/E, the “E” part of the equation is non-existent—the telco has posted losses in three of the last four quarters, and the Street forecasts a loss of $0.17 a share in 2016.

Add rising long-term debt (up 74% from a year ago as of the end of Q3) and a payout ratio that’s also headed in the wrong direction (81% of free cash flow, up from 67%) and you get a sense the dividend—which has barely budged since it was cut in 2011—is on borrowed time again.

FTR Hangs Up on Income-Seekers

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair