Bonds & Interest Rates

Seven years after ZIRP (then NIRP) was launched and central banks grew their balance sheets by $13 trillion, in the process inflating the biggest bubble the world has ever seen, sending risk prices to record highs and trillions in government debt to record negative yields, first the Fed admitted QE was a mistake, and now the investment banks – especially those who were bailed out and were the biggest beneficiaries of QE such as Citigroup – admit central bank quantitative easing failed.

Seven years after ZIRP (then NIRP) was launched and central banks grew their balance sheets by $13 trillion, in the process inflating the biggest bubble the world has ever seen, sending risk prices to record highs and trillions in government debt to record negative yields, first the Fed admitted QE was a mistake, and now the investment banks – especially those who were bailed out and were the biggest beneficiaries of QE such as Citigroup – admit central bank quantitative easing failed.

The reason for this failure? What we said from day one dooms all unconventional monetary policy – too much debt.

Here is Citi’s Willem Buiter, finally catching up to what we said in early 2009.

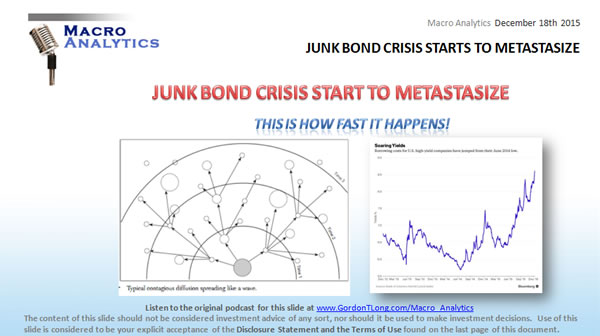

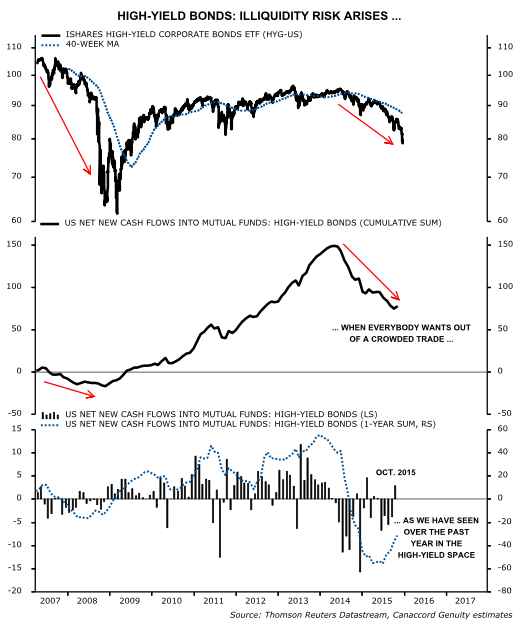

John Rubino and Gordon T Long discuss the alarming developments in the Junk (HY) Bond market. John was warning on his last appearance on Macro Analytics about the things he was seeing, while Gord was warning of a turn he was seeing in the Credit Cycle. Both previous observations have proven correct so John and Gordon postulate what to expect next. It isn’t pretty!

A Huge Potential Problem

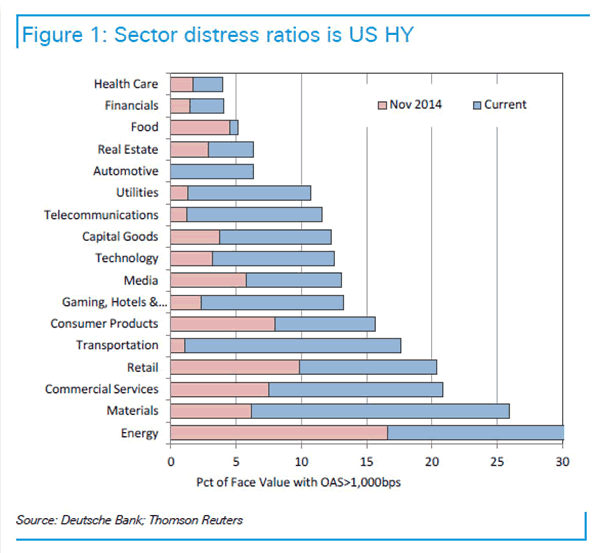

Since the Financial Crisis the US Federal Reserve has increased its balance sheet by approximately $3.5 Trillion. In this same period the Junk Bond (HY) issuers have issued $2.2T of debt which the markets have ‘gobbled’ up to achieve yield. The question is what happens if they start selling some of that debt to avoid capital losses. This problem is compounded by regulations since the financial crisis which has significantly curtailed banks making markets in these instruments. Many worry that Investment Grade (IG) bonds also issued over the same period will be “infected”, especially with a historic $1.3T being sold for the first time in 2015 to significantly fund stock buybacks and dividend payouts. This is a ‘witch’s brew’ for a potential disaster.

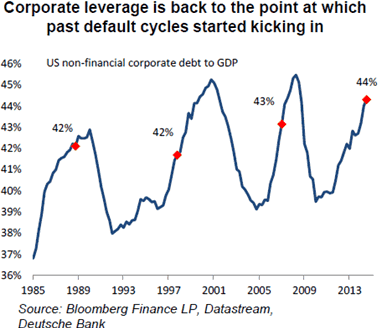

Corporate Leverage

Corporate Leverage

With Corporate Leverage back to the point at which past default cycles started kicking in, there are more reasons to worry, as corporate cash flow and EBITDA fall while the Federal Reserve raises rates.

Worsening cash flow to debt ratios normally force credit downgrades making credit more expensive and harder to get. This is coming at a time when major Junk Bond issuers in the Energy and Commodity sector are being hardest hit by falling pricing. They are trapped and investors know this and are now worried about junk bond liquidity.

A Slowing Global Economy

John and Gord both see a steadily deteriorating global economy which will bring further pressures to an already troubling situtation.

John lays out the torrent of bad news coming as the Fed begins raising rates:

Oil slump resumes on U.S. supply build, expected Fed rate hike

Why the current credit crisis might be 35 times worse than you thought

Freight Shipments Hammered by Inventory Glut, Weak Demand

Baltic Dry Crashes To New Record Low As China “Demand Is Collapsing”

US Markit flash manufacturing PMI slips to three-year low in December

US industrial output falls as manufacturing stays flat

Brazil’s currency sinks after Fitch cuts rating to junk status

The question is whether the Fed will be able to follow through with its stated policy direction.

Worry of Contagion

The problems in the Junk Bond market are not isolated to just the hard hit commodity and energy sectors. The protracted period of “easy money” created by Fed policy has sowed its seeds across all economic sectors.

A Critical 90-Day Window

The next 90 days are going to be both quite worrying to investors and highly volatile for the financial markets, as the Credit Cycle, Rate Cycle and Business Cycle all send confusing signals before the future economic direction becomes clear.

Let’s all hope that is not spelled: “Recession”.

…. there is much, much more in this comprehensive 31 minute video discussion.

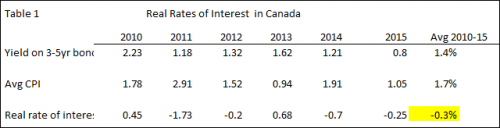

In his December 8th speech, the Governor of the Bank of Canada, Stephen Poloz introduced the possibility of negative interests as a policy tool. He was adamant that the Bank was not embarking upon this policy, rather it was exploring the implications of using such an unconventional policy instrument in times of economic shock or major dislocations. It was his view that “it’s prudent to be prepared for every eventuality.” (1)

Yet, his discussion went beyond just academic musings and into the practical realm of how negative interest rates would impact the Canadian financial markets. In 2009, the Bank looked at the application of negative interest rates, but rejected it as a possible tool. What has changed since that time that caused the Bank to come out in favor of such an unprecedented policy move?

When asked about why the Fed decided to raise rates now, Ms. Yellen responded by suggesting that the “odds were good” the economy would have ended up overshooting the Fed’s employment, growth and inflation goals had rates remained at low levels. She then went on to state that it was a “myth” that economic growth cycles die of “old age.”

While such an optimistic outlook for economic growth was certainly welcomed by the markets, both of her statements expose the challenges that lie ahead for the Fed.….more analysis and bigger charts HERE

Canadian lifecos (OW) vs. banks (MW): After successfully favouring lifecos over banks in 2015, CG analyst Gabriel Dechaine recently inversed the trade. From a quant/macro viewpoint, we cannot make the switch just yet. A key driver between lifecos and banks is relative forward EPS strength. As Figure 2 shows, lifecos’ forward EPS still outpace those of banks and the rising trend in relative pricing power (i.e., insurance premiums/financial services & mortgage interest costs) suggests further strength. Also, market-based variables have been supportive for lifecos’ EPS in the fourth quarter with bond yields and global equities rising while the CDN$ has fallen to multi-year lows (Figure 3). Last, lifecos trade at a 7% premium to banks on a forward PE basis but this is reasonable given the superior EPS growth rate projected next year (11% vs. 4%).

….read more with larger charts HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair