Bonds & Interest Rates

Lots of folks are throwing roses at Janet Yellen for her rate-hiking performance yesterday. They pulled it off without a hitch. Like the Ocean’s Eleven heist—everything had to go right, and it did.

Lots of folks are throwing roses at Janet Yellen for her rate-hiking performance yesterday. They pulled it off without a hitch. Like the Ocean’s Eleven heist—everything had to go right, and it did.

Stocks rallied hard, FX had it fully priced in, and the only thing that was down was oil. Even the junk bond market caught a break. You couldn’t have scripted a better ending.

Except this isn’t the ending, but the beginning.

Also, I’d like to reiterate that the Fed has been screwing around with this for over a year, to get the market used to the idea of a 25bp rate hike. I don’t call it a success when you need a year of jawboning to raise rates a quarter-point. I call that hopelessly inept.

Anyhow, I think the takeaway for investors here is how hawkish the Fed is and how rates might go higher, faster than we thought. Many people thought the directive was dovish. I didn’t think so at all.

-

The Fed talks a lot about labor utilization slack being taken up—that’s code for “If the unemployment rate goes down any more, we are going to look stupid for not having hiked rates.”

-

The Fed seems confident that inflation will rise to 2%. Why, I’m not sure.

-

The whole directive has a hawkish tone.

-

The Fed emphasizes that rate hikes will be “gradual,” but it’s still targeting 1.4% fed funds at the end of 2016, which would entail 3-4 rate hikes next year.

-

The Fed doesn’t seem to be at all concerned that it’s an election year.

Economists are focusing on the word “gradual,” taking that to mean that the Fed will be very cautious, but if you’re hiking four times in a year, you’re hiking pretty much every other meeting, and I don’t see any flashing lights in the directive that might indicate the January meeting is off limits.

Nothing seems to be off limits.

Having said all that, I do think the Fed will significantly undershoot its target for 2016 fed funds (it certainly won’t overshoot it), so there is still money to be made, but the big takeaway is that this is not a one-and-done Fed.

In my Street Freak letter and my premium publication, The Daily Dirtnap, I did correctly predict that the Fed would hike and that risk would rally, but I did not anticipate how hawkish the tone had turned within the Fed.

The Implications

Pretend that fed funds really do get to 1.4% at the end of 2016. Where do you think the following currency pairs will be?

EUR (rates -0.3%)

CAD (rates 0.5% and dropping, possibly going negative)

CHF (rates -0.75%)

JPY (rates 0%)

SEK (rates -0.35%)

Etc. This is like currency trading for dummies. The dollar is going higher.

And if the dollar goes higher…

…more pain for commodities and emerging markets.

In other words, back to the salt mines.

This could change, if the Fed dilly-dallies, or credit doesn’t cooperate, or something pushes back the rate hikes, but it is entirely possible that even more pain will be piled onto the enormous steaming pile of pain that has been heaped on commodities already.

On the other hand, gold didn’t get killed yesterday, which is a start.

Sage Words

Someone cited an old Buffett quote on Twitter yesterday, about how he never, ever took what the Fed was doing into account with his investment decisions.

And then you have Stan Druckenmiller in the Lost Tree Club speech, saying that the first thing he looks at when investing is what the Fed is doing and the liquidity situation.

Whom are you to believe?

I believe Mr. Druckenmiller—hands down. Especially in today’s environment, where central banks play a much more active role. Liquidity drives everything.

Getting back to what I was talking about earlier, the Fed is getting credit for hiking rates without upsetting the market.

I remember a time when the Fed didn’t give a crap if it upset the market. If you recall, we used to have surprise, intermeeting rate hikes. Oh Em Gee, can you imagine what would happen if they did that today? Pandemonium.

Greenspan started this whole transparency kick, and Bernanke expanded it even further. It is counterproductive. If you’re going to have a central bank with a monopoly on interest rates, have it operate in secret and drop bombs on people, like the Fed described in the book Secrets of the Temple.

Forward guidance is actually a trap for central bankers. You give the market expectations, you risk disappointing it later if you change your mind. The gnomes haven’t figured this out yet.

People think the Fed is “omnipotent” and controls the markets. Nothing could be further from the truth. Today’s Fed is held hostage by the markets. If it weren’t, it rightfully would have raised rates 18 months ago, and we’d be at 3% fed funds right now.

I asked rhetorically the other day—when was the last time the Fed hasn’t come to the rescue?

You have to go all the way back to Paul Volcker, who to this day is in Central Banking Cooperstown. History has a funny way of not looking kindly on the doves. That applies to any central bank in any country, throughout history. Toughness is a virtue.

A quick note before I leave: Right now, you can get Street Freak plus all of Mauldin’s other paid services for one low price if you become a Mauldin VIP. Click here for more.

Jared Dillian

Editor, The 10th Man![]()

Jared’s premium investment service, Street Freak, is available now. Click here for our introductory offer. Jared Dillian, former head of ETF Trading at one of the biggest Wall Street firms and author of the highly acclaimed book, Street Freak: Money and Madness at Lehman Brothers, shows you how to pick and trade trends, and master your inner instincts. Learn how to use “Angry Analytics” as a leading indicator of budding trends you can profit from… and how to view any market situation through the lens of a trader. Jared’s keen insight into market psychology combined with an edgy, provocative voice make Street Freakan investment advisory like no oth er. Follow Jared on Twitter at @dailydirtnap.

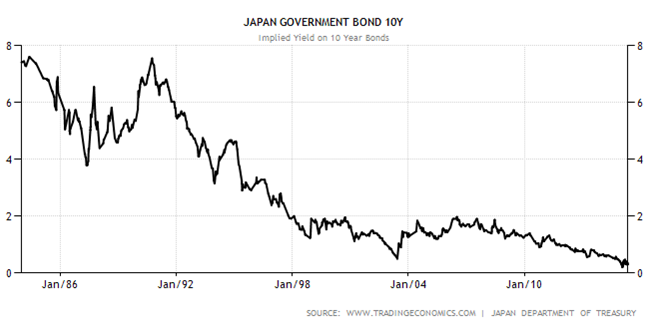

I remember how in 2003 the late legendary Barton Biggs, a strategist for Morgan Stanley, proclaimed in one of his Investment Perspectives that 10-year Japanese government bonds (JGBs) were “the short of the century.” Japan had just gone through 10 years of deflation and the 10-year JGB yields had gone from nearly 8% at the time of the all-time high in the Nikkei 225 benchmark index (at near 40,000 in December 1989) to a hair shy of 40 basis points (0.4%) in 2003.

The Japanese government bond market did sell off as deflation seemed to be abating and riskier asset classes like stocks were coming out of the 2000-2002 bear market, but the 10-year JGB yield in Japan never decisively crossed the 2% mark and again sank into deflationary territory to make yet another all-time low in January of this year at 20 basis points…..read full article and larger charts HERE

While everyone seems to place a huge question of will the Fed raise rates or not, the markets have factored in the rate rise already for sometime. The Fed was scheduled to raise rates in June, but the IMF turned to the press to criticize them to prevent rate hike. Then in September, the IMF, ECB and other governments all pleaded with the Fed not to raise rates.. The trend will change. The Fed has no choice and that seems to be what the pundits do not get. We can see that rates are BELOW the historic low of the Great Depression. But they are also at a 5000 year low in interest rates on a global scale as well….read more HERE

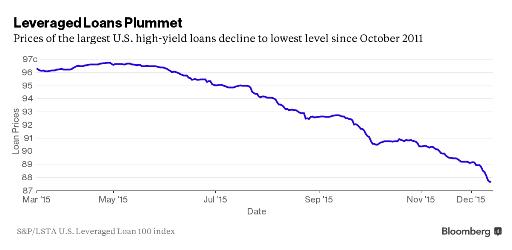

With junk bonds finally reverting to their intrinsic value, the question on everyone’s mind is “what blows up next?” Here’s the first in what might be a long, painful list:

CLOs Hammered as Energy Rout Plays Havoc With Other Markets

(Bloomberg) – The bust in commodities that’s roiling junk bonds is also taking its toll on funds that bundle corporate loans used to finance buyouts.

The riskiest slices of collateralized loan obligations raised after the financial crisis plunged 9 cents on the dollar since September to about 58 cents at the end of last month, down from 84 cents a year ago, according to JPMorgan Chase & Co. Intensifying price declines in recent months have led to one of the “more challenging years in recent memory,” JPMorgan analysts Rishad Ahluwalia and Jacob Kurosaki wrote in a Dec. 11 note to clients.

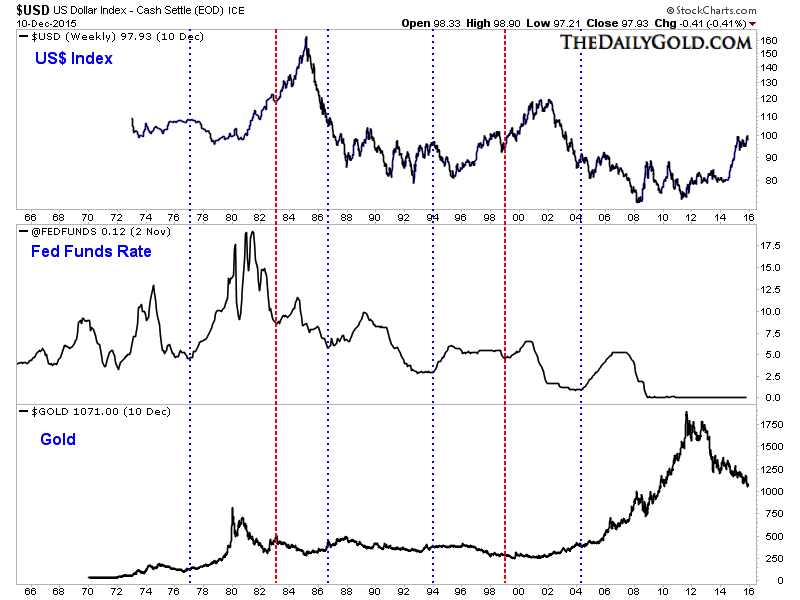

The markets have for the most part already priced in a Fed rate hike which is expected next week. Yesterday fed funds futures indicated an 80% chance of a rate hike. It would be the first hike in roughly 9 years. The Fed last began a new hiking cycle in 2004. We consult history to decipher the potential impact (of a rate hike) on the embattled precious metals sector.

The chart below plots the US$ index, the Fed Funds rate and Gold. We marked the points at which the Fed Funds rate began to increase. The red marks show the two points which are most comparable to today with respect to the US$ index. At those points (1983-1984 and 1999) an increase in the Fed Funds rate was preceded by a strong uptrend in the US$ index.

US$, Fed Funds Rate, Gold

The Fed Funds rate increases in 1983-1984 were preceded by US$ strength but also massive rebounds in Gold and gold stocks. From mid 1982 into early 1983 Gold rebounded by 73% and the Barron’s Gold Mining Index rebounded by 210%.

The Fed Funds rate increase in 1999 is most applicable to today because it was preceded by US$ strength and steep declines in Gold, gold stocks and Commodities. (It was also preceded by strength in US equities and major weakness in emerging markets).

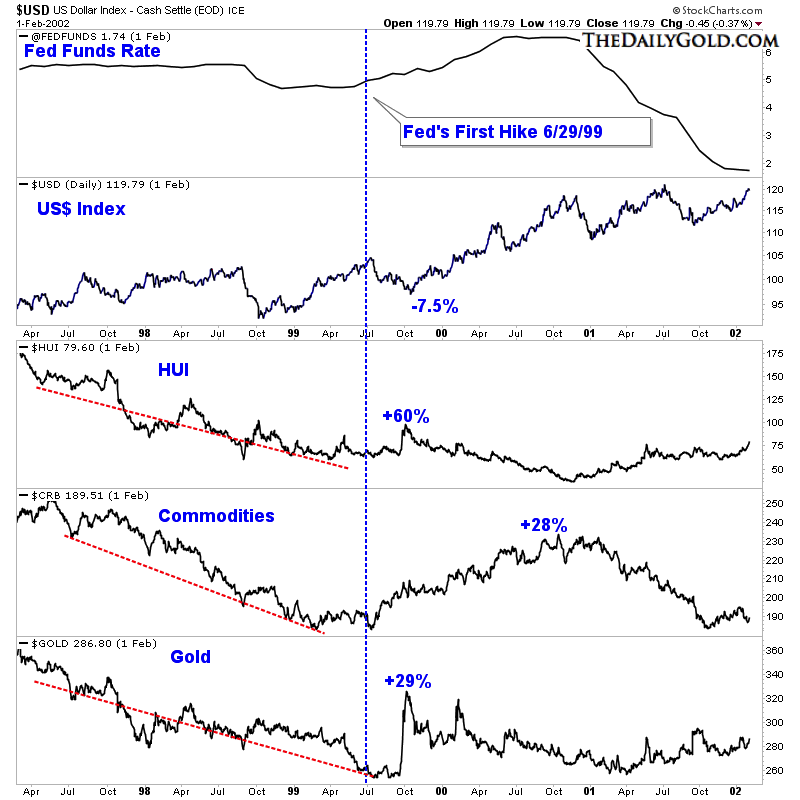

The chart below shows how various markets performed before and after the rate hike in summer 1999. The US$ index declined by 7.5% while Gold and gold miners surged higher. The counter-trend move lasted the longest in Commodities. Another similarity to note, albeit small, is the gold miners (HUI) did not make a new low before the hike as Gold did.

Fed Rate Hike in 1999

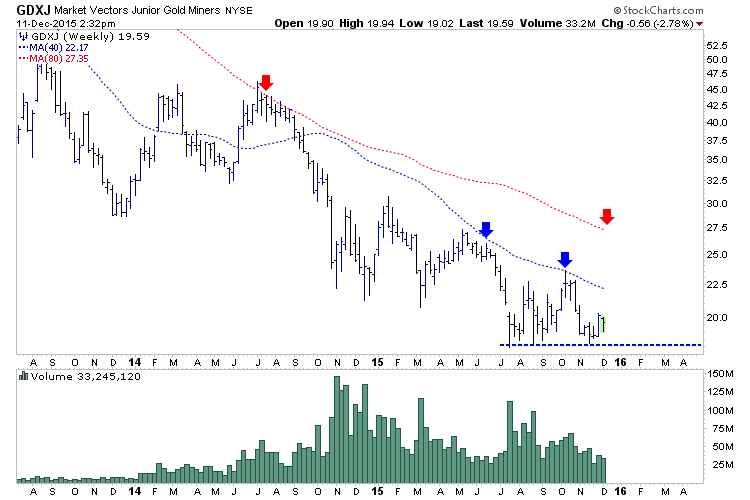

The gold mining indices (GDX, GDXJ, HUI) have essentially held support and built a base since July. GDXJ (shown below) figures to close the week in the mid $19s. If history repeats itself (with respect to Fed actions) then a rebound should begin after the hike and last for a few months. The initial target would be the 200-day moving average ($22) followed by the October high (mid $23) and the 400-day moving average ($27).

A Fed rate hike could be a catalyst for a decent rebound in hard assets and in gold stocks especially. However, the key word is rebound. History argues for a rebound in the weeks to come but a rebound followed by new highs in the US$ index and new lows in precious metals. This fits with our expectation that the US$ index could surge higher in 2016 and lead to capitulation and the end of the bear market in Gold and Silver.

Jordan Roy-Byrne, CMT

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair