Bonds & Interest Rates

PARIS – Yesterday, we got so much mail on our recent issue on Donald Trump we couldn’t read it all.

PARIS – Yesterday, we got so much mail on our recent issue on Donald Trump we couldn’t read it all.

Pro… con… off the wall – readers’ sentiments were all over the place.

But a clever reader mercifully brought the discussion to an end with this quote from fellow Baltimorean H.L. Mencken:

As democracy is perfected, the office of the President represents, more and more closely, the inner soul of the people. On some great and glorious day, the plain folks of the land will reach their heart’s desire at last and the White House will be occupied by a downright fool and complete narcissistic moron.

All over the world, elections allow the people to express their innermost thoughts and feelings.

This is a big day in Argentina, for example.

Outgoing president Cristina Kirchner is supposed to hand over power to her successor, Mauricio Macri. (If you’re a Bonner & Partners Inner Circle member, you can get the full story from our analysts on the ground in Buenos Aires here.)

But when we looked yesterday, there was dispute as to exactly what time the baton would be passed. And Cristina has let it be known she would not attend the inaugural and would generally make life as difficult for Mr. Macri as possible.

Deep State in Control

Elections are misunderstood.

On the surface they are contests between zombies and cronies. The zombies (leftists, socialists, Democrats) want lots of little handouts. The cronies (rightists, Wall Streeters, Republicans) want fewer but bigger ones.

All the loot comes from the voters – who willingly give up both their money and their liberty believing that, somehow, they are better off for it.

But the real winner is the Deep State. It usually controls the candidates… and continues to gain power and resources, no matter which side wins.

But the Deep State is not immune to setbacks. On the pampas, it must be worried that Macri may actually believe in free markets rather than markets controlled by cronies.

If so, it may be harder to work with him than they had hoped.

And in the U.S., poor Janet Yellen must be having trouble sleeping again. The Deep State, the zombies, the cronies – all turn their black hearts and beady eyes unto her.

Next Wednesday, she takes center stage again. And with the whole world watching, she’ll make a complete fool of herself.

The Trouble with the Future…

Yellen is supposed to announce a tiny increase in the Fed’s key lending rate… currently sitting at 0.25%.

Analysts will examine every word. Commentators will report, confuse, and misinterpret her remarks. And the economy and the markets will react.

But they may not react as the insiders hope…

Each generation has its market myths. Each decides what is important and what is not.

The generation of the 1970s and 1980s watched inflation rates and money supply figures.

Investors had been beaten up by the inflation of the 1970s. Then they learned from Milton Friedman at the Chicago School that inflation was “always and everywhere a monetary phenomenon.” So they began to watch the Fed’s M2 money supply figures like scouts looking for early warning of an enemy attack.

The attack never came. The rate of consumer price inflation fell from a high of about 15% in 1980 to its near-zero levels today.

Investors are always looking in the wrong direction. They have to be…

“I’m going home to the U.S. to die,” said an old friend the other day.

“If you know you’re going to die at home,” we asked, “why not stay in Paris?”

Likewise, if investors knew what the future held, it wouldn’t happen that way. They would sell their positions before the top was in, avoiding a crash. And they’d buy before stocks hit rock bottom, never allowing a bear market to fully express itself.

Surprises would be eliminated. Accidents avoided. If everyone knew where they would have a fender-bender, auto-body shops would be out of business!

That is the trouble with the future: It must come as a surprise.

Wrong Direction

We talk about borrowing as “taking from the future.”

But it’s not really possible. Because the future hasn’t happened yet. It’s just a metaphor for understanding what is going on.

Farmers – at least in the old days – saved some of their corn each year as “seed corn.” This is what they would plant the following year.

And if they ate it rather than saving it, they would have been “taking from the future.” Next year’s crop would be reduced as a result. More today but less tomorrow.

But it is always a risk to take from tomorrow. Centuries ago, fewer seeds – and perhaps less rainfall, or too much rainfall, or too much wind, or hail, or frost – might have meant starvation.

What might it mean today?

We don’t know. The future is always a surprise… especially to people with PhDs in economics.

And now we watch Ms. Yellen.

Acres of print will be devoted to speculating on how much of an increase she will announce… and how it will be followed up.

Guessing about the “pace of tightening” (that is, how soon will the first rate hike be followed by another) and positioning portfolios for tighter money – more dollars, less emerging market debt – are already growth businesses.

Could it be that investors are looking in the wrong direction? Has the future moved on… without Ms. Yellen?

Have stocks already topped out? Are sales already dropping? Is subprime student, energy, auto, corporate, and emerging market debt already sinking?

Have the trains already left their stations, headed to destinations that investors haven’t even thought of?

Could it be that the Deep State’s debt-based financing system is already in trouble? And, after 84 months of zero interest rates and roughly $4.5 trillion of central bank stimulus, can Ms. Yellen save it?

Regards,

Bill

Market Insight

“Thinking” computers are closer than you may realize…

This year has been a landmark year for artificial intelligence (AI) – one of the big themes editor Jeff Brown is tracking in our newest publication, Exponential Tech Investor.

As Jeff put it in his recent webinar about how to profit from the next wave of technology breakthroughs:

It won’t be long before your personal AI will be able to take care of the vast majority of menial tasks, such as scheduling meetings, reading and responding to routine emails… even buying and sending flowers on your behalf. I can’t wait for that day. It will free up so much of my time for more productive pursuits.

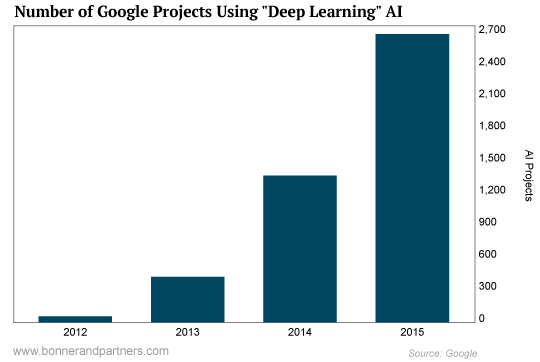

And as today’s chart reveals, growth in AI during 2015 has been huge.

From a couple hundred projects in 2012, tech maven Google… now called Alphabet (NASDAQ:GOOG)… is running almost 3,000 projects involving a type of AI called deep learning.

And it’s not the only tech big hitter betting on AI. Facebook (NASDAQ:FB), Apple (NASDAQ:AAPL), Microsoft (NASDAQ:MSFT), and Amazon (NASDAQ:AMZN) are also investing heavily in this technology.

As Jeff reveals in his latest investor presentation, breakthroughs in AI will transform the world around us. They will also create once-in-a-lifetime profit opportunities for investors who are properly positioned. Watch it here.

Further Reading: Bill has been warning about the coming collapse of the Deep State’s debt-based financing system. And in his latest presentation, he lays out the frightening details that those in control of the Deep State don’t want you to know. Watch it here now.

“these days, some 70% of market orders are generated by computers, and many of the rest by indexers. And computers do not think”

“these days, some 70% of market orders are generated by computers, and many of the rest by indexers. And computers do not think”

In some 40 years of watching financial markets, my dominant emotion has been a mixture of curiosity, amusement and despair. It seems the stock market must have been invented to make the maximum number of people miserable for the greatest possible amount of time. The bond market, meanwhile, has just one goal in life: to make economists’ forecasts for interest rates look even more silly than their other predictions.

Over the years I have often observed how most market participants are able to concentrate on only one set of information at a time. For example, in the 1970s, the only data release that mattered was the consumer price index. In the days leading up to the CPI’s publication, everybody dropped all other considerations to speculate feverishly about what the number might be. And then following the release, they would spend the next week or two commenting sagely on what the number actually had been. Eventually Milton Friedman convinced the Federal Reserve (and from there the markets) that there was some kind of relationship between the money supply and the CPI. So everyone stopped looking at the CPI, and instead started to focus on the publication every Thursday evening of M1 (or was it M2?). Inevitably each week would see an immediate rash of commentary on these arcane matters from the leading specialists at the time, Dr. Doom and Dr. Gloom.

This gave way to a period in which the US dollar went through the roof on the covering of short positions established during the era of the minister of silly walks in the 1970s. For a few years, the only thing that mattered was the spread between the three-month T-bill yield and the three-month rate on dollar deposits in London (an indication of the shortage of dollars outside the US). The beauty of this one was that the scribblers on Wall Street could comment on it twice a day or more, which of course had no discernible impact on reality, except for the destruction of the forests needed to print so much waffle.

That era came to an end in 1985 with the Plaza Accord. At that point the Fed, under the wise guidance of Paul Volcker—my favorite central banker of all time, probably because he was the only one without a PhD in economics, which may well explain his success—decided it was going to follow a type of Wicksellian rule-based policy under which short rates were kept closely in line with the rate of GDP growth. Of course, this meant the Fed paid little attention to the vagaries of the financial markets, so there was very little to comment on. The result of policymakers’ lack of interest in financial markets was that from 1985 to 2000 the US enjoyed a long period of rising economic growth, low inflation, low unemployment and high productivity; a period dubbed “the great moderation”. The trouble was that no one was able to make any money trading on inside information provided by the politicians and central bankers. As an advertisement for Sm ith Barney put it at the time: “We are making money the old way. We earn it.”

Naturally, that wouldn’t do at all. After nearly 20 years of economic success, the US budget was in surplus, the pension funds were over-funded, and the “consultants” in Washington were on the verge of bankruptcy, having nothing to say. Clearly something had to be done, and it was: policy shifted to accommodate Wall Street, with forward guidance, negative real rates, the privatization of money, and a lack of regulation. This allowed Wall Street to make money, but it created nightmares elsewhere through the ever-successful euthanasia of the dreadful rentier.

Still, the shift to an economy driven by the decisions of central bankers meant the market commentators were back in business in a big way. For the last 12 years, the only thing that has mattered has been to know whether or not the chairman of the Federal Reserve has had a good night’s sleep. Similarly in Europe, the dysfunctional euro, created by a bunch of incompetent politicians and Eurocrats, bred drama after drama. Since nobody wanted to admit it was a failure, the most important man in Europe became the president of the European Central Bank.

In the last week, we have reached what is surely the apex of this stupidity. A bunch of algo traders programmed their computers expecting “Derivative Draghi” to be extremely dovish, as any proper Italian central banker should be. I am not sure I understand why, but some traders obviously decided that he had not been dovish enough. European stock markets plunged by -4%, while the euro went up by roughly the same amount in the space of a few minutes. What that means is simple: value in the financial markets is no longer a function of the discounted cash flow of future income, but instead is determined by the amount of money the central bank is printing, and especially by how much it intends to print in the coming months. So we are in a world where I can postulate the following economic and financial law: variations in the value of assets are a function of the expected changes in the quantity of money printed by the central bank. To put it in a format that today’s economists understand:

Δ (VA) = x * Δ (M),

where VA is the value of assets and M is the monetary increase.

What we are seeing is in fact in one of the stupidest possible applications of the Cantillon effect, whereby those who are closest to the money-printing, i.e. the financial markets, are the biggest beneficiaries of that printing. This is exactly what happened in 1720 in France during the Mississippi Bubble inflated by John Law. The end results were not pretty (see “Of Central Bankers, Monkeys And John Law” [above]).

What I find most hilarious is that some serious commentators have been pontificating at considerable length about what the market’s participants think. These days, some 70% of market orders are generated by computers, and many of the rest by indexers. And computers do not think. They simply calculate at light speed, which allows them to react to short term movements in market prices as they were programmed to do. And since they are all programmed the same way, the result is some big short term market moves. In essence, these computers act as machines that allow market participants to stop thinking. As a result, I cannot remember a time when less thinking has ever been done in the financial markets, which is why I find today’s financial markets infinitely boring.

We are swimming in an ocean of ignorance, just like France in 1720. It seems all the painful economics lessons learned over the last 300 years have been forgotten. I suppose that means we will just have to wait for another Adam Smith to appear. La vie est un éternel recommencement…

Bank of Canada’s chief finally said what we had been patiently waiting for over the past several months: admission that Europe’s experiment with negative rates is about to cross the Atlantic. From Market News:

Bank of Canada’s chief finally said what we had been patiently waiting for over the past several months: admission that Europe’s experiment with negative rates is about to cross the Atlantic. From Market News:

- BOC POLOZ: NOW SEES EFFECTIVE LOWER BOUND FOR POLICY RATE AROUND -0.5%

- BOC POLOZ: CANADN FIN MKTS COULD FUNCTION IN A NEG INT RATE ENVRIONMNT

- BOC POLOZ: ‘SHOULD THE NEED ARISE’ FOR UNCONVENTIONAL MONETARY POLICY, ‘WE’LL BE READY’

That, as they say, is “forward guidance” of what is coming.

And what is coming, is also precisely what Keith Dicker from IceCap Asset Management said in his latest monthly letter, would happen in Canada in the very near future. To wit:

Related: Peter Schiff Warns: “The whole Economy Has Imploded….Collapse Is Coming” 12/07/2015

Related: Peter Schiff Warns: “The whole Economy Has Imploded….Collapse Is Coming” 12/07/2015

Fed’s Rocket Ship Turns Hoverboard

Over the past year, while the U.S. economy has continually missed expectations, Federal Reserve Chairwoman Janet Yellen has assured all who could stay awake during her press conferences that it was strong enough to withstand tighter monetary policy. In delivering months of mildly tough talk (with nothing in the way of action), Yellen began stressing that WHEN the Fed would finally raise rates (for the first time in almost a decade) was not nearly as important as how fast and how high the increases would be once they started. Not only did this blunt the criticism of those who felt that the delays were unnecessary, and in fact dangerous, but it also began laying the groundwork for the Fed to do nothing over a much longer time period. To the delight of investors, the Fed has telegraphed that it will adopt a “low and slow” trajectory for the foreseeable future and move, in the words of Larry Kudlow, like “an injured snail.”

To order your copy of Peter Schiff’s latest book, The Real Crash (Fully Revised and Updated): America’s Coming Bankruptcy – How to Save Yourself and Your Country, click here.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

Worried that rising rates are going to hurt some of the bonds you own? A 0.5% – 1% move would be plenty big to pancake many bonds.

As I write to you on this first Wednesday of December, traders are handicapping a 78% probability that the Fed will boost rates in two weeks. Overall they’re projecting a half-percent increase between now and June. And renowned government insider Goldman Sachs is a bit more aggressive – it’s projecting a full percentage point of tightening.

So if you’re worried that Goldman Sachs could be right, you’d better move some of your fixed-rate bond money into “floating-rate” issues.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair