Bonds & Interest Rates

This is a pickle wrapped in a conundrum surrounded by a puzzle, or something like that. The Fed declined to hike rates, which everyone thought was bullish, and then stocks got on the vomit comet. They’ve been going down on an elevator ever since.

I think what’s interesting here is how shamefully far behind the Fed is on this. Dudley is out there still talking rate hikes. Like, just the other day. He has gone right out of his tree. It’s almost as if he lost his B-Unit and can’t log into Bloomberg.

It was like this in the financial crisis, too. The Fed was very slow to act. It is a known fact that the Fed has never forecasted a recession (in spite of employing hundreds of nerd economists whose job it is to do precisely that). They don’t even react to them very well. I’m not certain we’ll get a recession, but the Magic 8 Ball says, “It is decidedly so.”

Like junk bonds, for example.

Credit spreads tend to be the best capital markets indicator of bad juju. The underlying bonds are even worse than the ETF. There are

bonds that are gapping 10 points lower at a time. There is no dealer participation. We are going to get hung bridge loans. Some of the larger deals are troubled. It is a mess.

My guess is that over the course of the next few weeks, the Fed is going to change their minds on rate hikes. Maybe they have already. It’s been my view that they won’t hike until 2017. I still believe that to be the case. I think you and I know what the Fed is going to do better than the Fed itself.

There are some people who think we’re FUBAR, that the Fed is out of ammo and we just have to get run over by the Mack truck because we can’t hike rates anymore, and what good is QE going to do, anyway?

Well, the one thing QE did was to raise asset prices, which happens to be the thing that currently ails us.

But remember, the Fed has all kinds of tools that haven’t even been explored yet.

- They can lower reserve requirements

- They can lower IOER (interest rate on excess reserves)

- They can do some magic stuff with the repo market that I don’t understand

- Helicopter money

The latter refers to when the central bank prints money and doesn’t buy bonds with it… it just mails out checks to everybody.

If I were a gold bear, I’d be nervous.

Let the Dollar Drop

The only way the Fed can get out of this is if they somehow manage to get the dollar to go the other way. To sell off.

That’s going to be hard. The strong dollar trade is the most relentless trend around.

This is the dollar over two years:

This is the dollar over a much longer timeframe:

Any technician would tell you that the dollar is consolidating, and the next move is higher.

But a move higher in the dollar would be brutal for global markets. EM is falling apart as it is.

If the Fed wants the dollar lower, it has to do one or more of those things in the itemized list.

An Austrian economist would say, screw it, let it go. There will be an adjustment period. And everything will be fine.

Even I am old enough to remember a time when the Fed didn’t feel compelled to intervene every time stocks went down 10%.

What People Are Saying

Pretty much every hedge fund guy I talk to is 100% bearish, this is the end of the world, etc. These are the guys responsible for the five-figure orders in HYG puts.

I would say the real money crowd is a little more sanguine. They are looking for value here.

The hedge fund guys are supposedly the smart money, but they tend to move as a pack. And they all tend to be wrong at the same time.

It’s getting ugly, but this isn’t the financial crisis and it’s not the dot-com bust. Stocks were overvalued, but not egregiously. Carl Icahn said there was a bubble in high yield, but there’s historical precedent for spreads to be this tight—they were tight throughout the duration of the Great Depression.

Biotech has sold off almost 30%, and big-cap biotech is trading with single-digit P/Es. Things can get worse—that’s what markets do—but this isn’t the end of the world.

I think the bigger danger is not how far the market goes down but how long it stays down. It will take a long time to reclaim the highs.

This is no-man’s land. If you’re thinking of selling here, you’re probably too late. If you’re thinking of buying, it’s probably too early.

I realize this is probably no help. Trust me, if I had conviction here, I would let you know.

Jared Dillian

Editor, The 10th Man![]()

Jared’s premium investment service, Bull’s Eye Investor, is available now. Click here for our introductory offer. For Jared, no asset class or type of investment is off limits. From an iconic sports outfitter to a particularly liquid frontier-market ETF—Jared picks the best vehicles for his subscribers to profit from tomorrow’s trends today. Put Jared’s ingenious mix of market analysis and trader’s intuition to work in your portfolio today. Follow Jared on Twitter at @dailydirtnap.

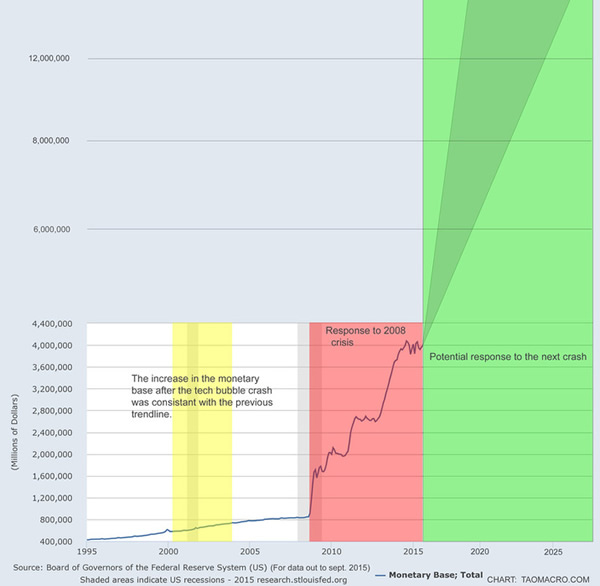

IS “HELICOPTER MONEY” COMING?

Since the start of June, global equity markets have lost over $13 trillion. This might be thought of as lost “collateral” for the mountains of pyramided global debt. This is frightening the Central Bankers!

(The last time global market dropped this much – Bernanke unleashed QE2)

As Zero Hedge spells out:

“world market capitalization has fallen back below $60 trillion for the first time since February 2014 as it appears the world’s central planners’ “print-or-die” policy to create wealth (and in some magical thinking – economic growth) has failed – and failed dramatically”.

Despite a steady diet of global rate cuts and balance sheet expansion around the world, the last 4 months have seen an 18% collapse – the largest since Lehman.

THE FED HAS BEEN BACKED INTO THE CORNER OF ONCE AGAIN INCREASING ITS BALANCE SHEET

HISTORICAL BEHAVIOR SUGGESTS THIS SHOULD SOON TO BE EXPECTED

WHAT ARE THE CENTRAL BANKERS’ OPTIONS?

Of course you never know for sure, but the general thinking is there are three likely central bank initiatives in our future. They may be rolled out or unleashed in a coordinated fashion to stem a potential economic crisis.

IT WIIL ONLY TAKE THE PERCEPTION OF A CRISIS TO UNLEASH A TORRENT LARGER THAN WE CAN CURRENTLY IMAGINE!

Let me be perfectly clear, non of this will work in the longer term! But when you are trying to keep your job, the longer term is the least of your concerns.

IT WILL LIKELY RESULT IN AN 9 MONTH RALLY AND MARGINALLY NEW HIGHS (OUR PREDICTED”M” TOP)

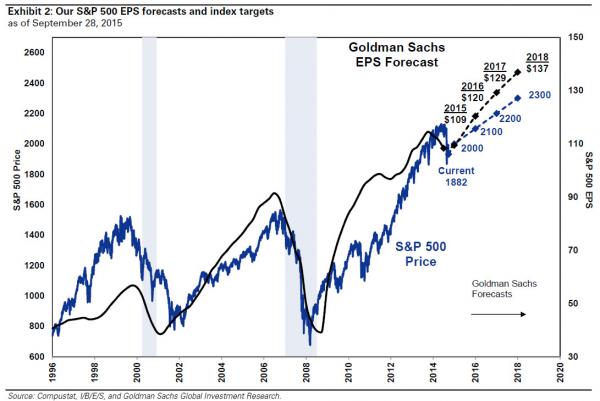

GOLDMAN SUPPORTS OUR ‘M” TOP – WITH BOGUS NUMBERS

POTENTIAL FED TRIGGER LEVELS

So how long will the Fed wait before acting? What might the FEd’s trigger points be?

A- BULL MARKET TREND CHANNEL SUPPORT

CHANNEL SUPPORT = 1860

B- TRADITIONAL FIBONACCI SUPPORT LEVELS

FIBONACCI 38.2% = 1837

FIBONACCI 50.0% = 1743

C- REGRESSIONS & TRADE WEIGHTED DOLLARS

Our longer term analysis on both the basis of linear regression and trade weighted dollars for the S&P 500 suggest ~1800needs to be held or matters could get quickly out of control for central bank policy initiatives.

D- SOME SEE THE FED “PUT” TO BE MUCH LOWER

I find the views of Nomura’s Bob Janjuah to very insightful and predictive. He sees the Fed “PUT” to be much lower than we do.

“Where is the Fed “put”, and what would such a “put” look like? It is very early in the process and lots will depend on global policy responses and data outcomes, but I am happy to declare my view: the next Fed “put” is not likely until the S&P 500 is trading in the 1500s at least (so more likely to be a Q1 2016 item rather than Q4 2015); and in terms of what the Fed could do, clearly QE4 has to be in the Fed’s toolkit. However, considering the failure of global QE to generate sustainable global growth and inflation, and considering the Fed’s starting point, 2016 could be the year when we see negative Fed Funds as a way of getting money velocity moving up rather than down.

… while I think a US recession is merely possible rather than probable, the evidence is growing in my view that a global recession is more probable than possible. Certainly the global trade data are pointing to meaningful global growth weakness, backed by weak data from EM and large parts of DM too. And a quick look at credit markets, in particular the HY markets in the US and Europe as well as the EM credit space support my view of a global growth recession being probable and not just possible. So if a global growth recession is more probable than possible, then it seems clear to me that neither risk assets nor core rates markets are accurately reflecting this at this time – instead, they reflect the “more possible” scenario rather than “more probable”. In other words, financial markets are NOT yet pricing for a recession, rather they are merely flirting with the idea. I suspect this largely reflects faith/hope in policymakers within market participants. The events of the past few weeks, both going into and after the most recent BOJ and FOMC meetings, should give those heavily invested in policymaker faith/hope a lot of food for thought.”

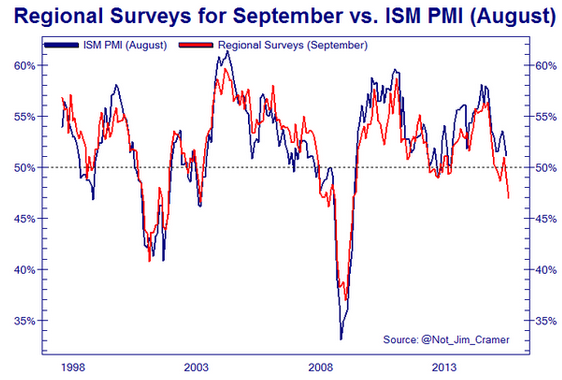

THE REVENUE RECESSION IS MOVING TOWARDS A ECONOMIC RECESSION SCARE

The Fed catalyst may not be a market level but rather the potential worry of an Economic Recession. A scare that may galvinize the Fed into action?

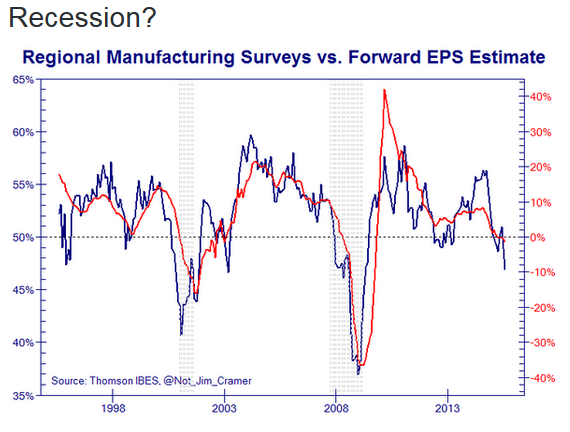

My research shows for the first time since 2009, all six major Fed regional activity surveys are in contraction territory.

Charts: Bloomberg

WHAT THE MAINSTREAM MEDIA IS NOT SHOWING – But the fed is acutely aware of!

EXPECT THE FED TO HIDE BEHIND THE COMING MARKET REALIZATION SCARE!

QE4, Helicopter Money (OMF), NIRP and Collateral Guarantees are coming soon!

Gordon T Long

Publisher & Editor

general@GordonTLong.com

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. While he believes his statements to be true, they always depend on the reliability of his own credible sources. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that you are encouraged to confirm the facts on your own before making important investment commitments.

© Copyright 2015 Gordon T Long. The information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. Please note that Mr. Long may already have invested or may from time to time invest in securities that are recommended or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or suggestions you receive from him.

We call on central banks to abolish their zero interest rate policy (ZIRP) framework before more harm is done. In our assessment, ZIRP is bad for all stakeholders and may even lead to war.

We call on central banks to abolish their zero interest rate policy (ZIRP) framework before more harm is done. In our assessment, ZIRP is bad for all stakeholders and may even lead to war.

ZIRP: Bad for Business?

At first blush, it may appear great for business to have access to cheap financing. But what may be good for any one business is not necessarily good for the economy. When interest rates are artificially depressed, it can subsidize struggling enterprises that might otherwise be driven out of business. As a result, productive capital can be locked into zombie enterprises. If ailing businesses were allowed to fail, those laid off would need to look for new jobs at firms that have a better chance of succeeding. As such, the core tenant of capitalism: creative destruction, may be undermined through ZIRP. In our assessment, the result is that an economy grows at substantially below its potential.

ZIRP: Bad for Investors?

Investors may have enjoyed the rush of rising asset prices as a result of ZIRP. However, this may well have been a Faustian bargain as the Federal Reserve (Fed) and other central banks have masked, but not eliminated, the risks that come with investing. Complacency has been rampant, as asset prices rose on the backdrop of low volatility. When volatility is low (more broadly speaking, we refer to “compressed risk premia”), rational investors tend to allocate more money to historically risky assets. While that may be exactly what central banks want – at least for the real economy – investors may bail out when volatility spikes, as they realize they didn’t sign up for this (“I didn’t know the markets were risky!”).

We believe that until early August this year, investors generally “bought the dips” out of concern of missing out on rallies. Now, they may be “selling the rallies” as they scramble to preserve their paper gains. This process is driven by the Fed’s desire to pursue an “exit.” For more details on this, please see our recent Merk Insight “Lowdown on Rate Hikes.”

But it’s not just bad because asset prices might crumble again after their meteoric rise; it’s bad because, in our analysis, ZIRP has driven fundamental analysts to the sideline. For anecdotal evidence, look no further than the decision by Barron’s Magazine to kick Fred Hickey (who may well be one of the best analysts of our era) out of the Barron’s Roundtable. Instead, money looks to be flocking towards investment strategies based on momentum investing, a strategy that works until it doesn’t. Again, ZIRP gives capitalism a bad name because we feel it disrupts efficient capital allocation.

ZIRP: Bad for Main Street?

Excessively low interest rates are also bad for Main Street. In our analysis, excessively low interest rates are a key driver of the growing wealth gap in the U.S. and abroad. Hedge funds and sophisticated investors seemed to thrive as they engaged in highly levered bets; at the other end of the spectrum are everyday people that may not get any interest on their savings, but are lured into taking out loans they may not be able to afford. We believe ever more people are vulnerable to “fall through the cracks” as they encounter financial shocks, such as the loss of a job or medical expenses; hardship may be exacerbated because people had been incentivized to load up on debt even before they encountered a financial emergency. Again, we believe ZIRP gives capitalism a bad name, although ZIRP has nothing to do with capitalism.

Low interest rates may not even be good for home buyers: it may sound attractive to have low financing cost, but the public appears to slowly wake up to the fact that when rates are low, prices are higher: be that the prices of college tuition or homes. It’s all great to have high home prices when you are a home owner, but it’s not so great when you are trying to buy your first home.

ZIRP: Bad for Price Stability?

While we believe inflation may ultimately be a problem if interest rates are kept too low for too long, ZIRP may temporarily suppress inflation. While this may sound counter-intuitive, it is precisely because of the aforementioned capital misallocation ZIRP may be fostering: when inefficient businesses are being subsidized, as we believe ZIRP does, inflation dynamics may not follow classical rulebooks. That’s because an economy with inefficient capital resource allocation experiences shifts in supply of goods and services that may not match demand leading to what may appear to be erratic price shifts. The most notable example may be commodity prices, where the extreme price moves in recent years are a symptom that not all is right.

ZIRP: Bad for Politics?

In our assessment, Congress has increasingly outsourced its duties to the Fed (the same applies to politicians and central bankers to many other parts of the world). The Fed now ought to look after inflation, employment, and financial stability. The Fed, in our humble opinion, is not only ill suited to tackle most of these, but invites political backlash as they step on fiscal turf. Let me explain: monetary policy focuses on the amount of credit available in the economy; in contrast, fiscal policy – through tax and regulatory policy – focuses on how this credit gets allocated. If the Fed now allocates money to a specific sector of the economy, say, the mortgage market by buying Mortgage Backed Securities (MBS), they meddle in politics. Calls to “audit the Fed” are likely a direct result of the Fed having overstepped their authority, increasingly blurring the lines between the Fed and Congress.

More importantly, the U.S., just like Europe and Japan, face important challenges that in our opinion can neither be outsourced, nor solved by central banks in general or ZIRP in particular.

ZIRP: Bad for Peace?

In 2008 and subsequent years, you likely heard the phrase, “Central banks can provide liquidity, but not solvency.” In essence, it means central banks can buy time. But what happens when central banks buy a lot of time and underlying problems are not fixed? In our assessment, it means that the public gets antsy, gets upset. When problems persist for many years the public demands new solutions. But because monetary policy is too abstract of an issue for most, they look for solutions elsewhere, providing fertile ground for populist politicians. Here are just a few prominent political figures that have thrived due to public frustration with the status quo: Presidential candidate Donald Trump; Senator and Presidential candidate Bernie Sanders; Greek Prime Minister Tsipras; Ukrainian Prime Minister Yatsenyuk; Japanese Prime Minister Abe; and most recently the new leader of UK’s Labor Party Jeremy Corbyn.

And what do just about all politicians – not just the ones mentioned above – have in common? They rarely ever blame themselves; instead, they seem to blame the wealthy, minorities or foreigners for any problems.

We believe the key problem many countries have is debt. I allege that if countries had their fiscal house in order, they would rarely see the rise of populist politicians. While there are exceptions to this simplified view, Ukraine may not be one of them: would Ukraine be in the situation it is in today if the country were able to balance its books?

Central banks are clearly not appointing populist politicians, but we allege ZIRP provides a key ingredient that allows such politicians to rise and thrive. ZIRP has allowed governments to carry what we believe are excessive debt burdens though ZIRPs cousin quantitative easing (“QE”). QE is essentially government debt monetization in our view. Take the Fed’s U.S. treasury buying QE program. Those Treasuries (or new Treasuries that the Fed rolls into) might be held indefinitely by the Fed (despite claims of balance sheet normalization) – meaning that US Government will never pay the principle, and the U.S. Government effectively pays zero interest on that debt because the profits of the Fed flow back to the US Treasury. ZIRP allows governments to engage on spending sprees, such as a boost of military spending Prime Minister Abe might pursue.

The Great Depression ultimately ended in World War II. I’m not suggesting that the policies of any one politician currently in office or running for office will lead to World War III. However, I am rather concerned that the longer we continue on the current path, the more political instability will be fostered that could ultimately lead to a major international conflict.

How to get out of this mess

It’s about time we embrace what we have been lobbying for since the onset of the financial crisis: the best short-term policy is a good long-term policy. We have to realize that when faced with a credit bust, there will be losers, and that printing money cannot change that. In that spirit, we must not be afraid of normalizing policy in fear of causing an economic setback. When rates rise, businesses that should have failed long ago, are likely to fail. Rather than merely rising rates, though, policy makers must provide a long-term vision of the principles that guides their long-term policy. In our humble opinion, “data dependency” is an inadequate principle, if it is one at all.

The Fed needs to have the guts to tell Congress that it is not their role to fix their problems. It requires guts because they must be willing to accept a recession in making their point.

To continue this discussion, please register to join us for our upcoming quarterly Webinar. If you haven’t already done so, ensure you don’t miss it by signing up to receive Merk Insights. If you believe this analysis might be of value to your friends, please share it with them.

###

Sep 29, 2015

Axel Merk

Contact Merk

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Merk Investments LLC makes no representation regarding the advisability of investing in the products herein. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice and is not intended as an endorsement of any specific investment. The information contained herein is general in nature and is provided solely for educational and informational purposes. The information provided does not constitute legal, financial or tax advice. You should obtain advice specific to your circumstances from your own legal, financial and tax advisors. Past performance is no guarantee of future results.

©2005-2015 Merk Investments LLC. All Rights Reserved.

“If you look at rentals in London where you live or in New York or in other cities in the U.S., they have of course been going up much more than the CPI [consumer price index] would suggest,” he explains. “Even the day before yesterday, Donald Trump was interviewed. He said, Obamacare is a disaster because the premiums have gone up close to 50% for some people.”

“If you look at rentals in London where you live or in New York or in other cities in the U.S., they have of course been going up much more than the CPI [consumer price index] would suggest,” he explains. “Even the day before yesterday, Donald Trump was interviewed. He said, Obamacare is a disaster because the premiums have gone up close to 50% for some people.”

“We have to define what inflation is,” Faber continues. “Inflation is basically the increase in the supply of money and credit. There are symptoms. You can have wage inflation. You can have commodity inflation.” — Marc Faber told CNBC, September 16, 2015

…more from Marc:

Marc Faber on Asia Turmoil – Marc discusses how a slowdown in Asia will affect global economies with Brian Sullivan.

Marc Faber is an international investor known for his uncanny predictions of the stock market and futures markets around the world.Dr. Doom also trades currencies and commodity futures like Gold and Oil.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair