Bonds & Interest Rates

It looks like the Federal Open Market Committee, in the Fed minutes, may have to change its target on raising rates as the global economic story continues to change minute by minute.

It looks like the Federal Open Market Committee, in the Fed minutes, may have to change its target on raising rates as the global economic story continues to change minute by minute.

The Fed, while saying that outlook for the rate hike still looked good, is possibly worried about China and Greece concerns that may cause the Fed to rethink that target. The concern is that plunging commodity prices may start to cement in a deflationary mood to the market. Also, it’s possible a rate-hike in the United States may cause even more harm to those Euro zone markets. Also, we could harm our markets–a possible capital flight could raise the dollar to dangerous levels.

Despite the turmoil in China, and Europe economic data out of Japan and Germany and an artificial rally in the Shanghai composite is giving crude oil some hope.

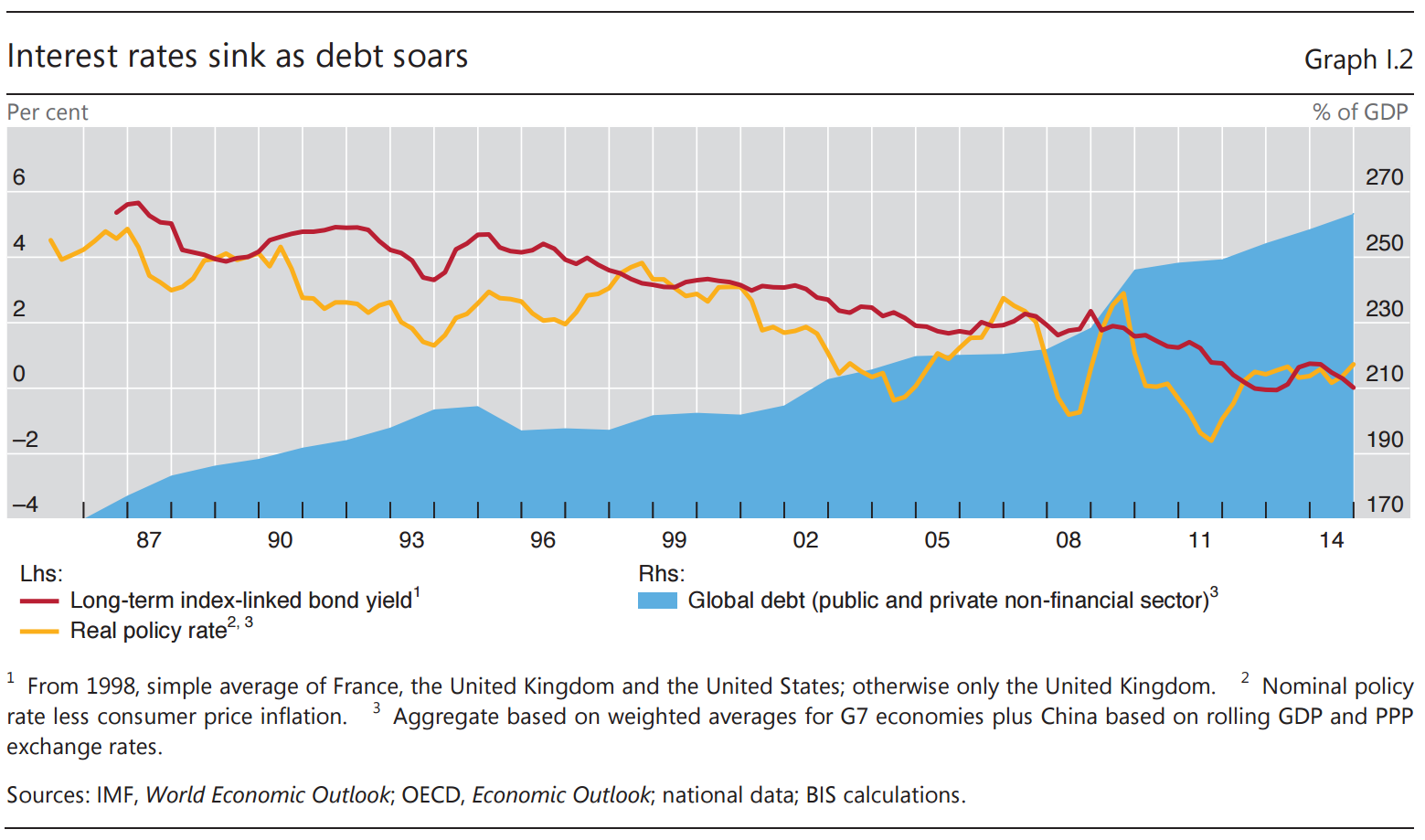

World’s oldest global finance organization thinks central banks could be causing a crisis all over again

“We argue that the current malaise may to a considerable extent reflect a failure to come to grips with how financial developments interact with output and inflation in a globalised economy. For some time now, policies have proved ineffective in preventing the build-up and collapse of hugely damaging financial imbalances, whether in advanced or in emerging market economies (EMEs). These have left long-lasting scars in the economic tissue, as they have sapped productivity and misallocated real resources across sectors and over time.” – From the Bank For International Settlements report:

$1.4 trillion of Chinese stocks have stopped trading. Greece is finally imploding. The US trade deficit is widening on falling exports.Copper just fell back to 2009 levels. And safe-haven capital flows are revving up again, with Swiss 10-year bonds once again trading with negative yields.

Yet somehow a majority of economists and money managers continue to believe that not only will the fed hike rates at its next meeting, but that it should do so.

The IMF isn’t normally the voice of reason on major financial issues, but in this case — perhaps because it has its hands full with Europe — its caution seems appropriate:

IMF Reiterates Call for Fed to Hold Off on Rate Rise Until 2016

WASHINGTON–The Federal Reserve risks stalling the U.S. economy by raising interest rates too early, the International Monetary Fund warned Tuesday as it detailed further its call for the central bank to delay a move until 2016.

The IMF’s push for a delayed rate increase is at odds with the current signals Fed officials are sending for a move later in 2015. Last week’s job numbers bolstered the Fed’s plans to increase short-term rates in the months ahead.

The IMF, which cut its growth forecast for the U.S. last month, said the Fed could be forced to reverse course next year if the central bank proves overly optimistic about the health of the American economy. IMF staff argue that, barring upside surprises, there is still too much uncertainty around inflation, employment and wage prospects for the Fed to pull the trigger in coming months.

“Raising rates too early could trigger a greater-than-expected tightening of financial conditions due to some combination of a further upward swing in the U.S. dollar, lower equity prices, and/or a repricing of risk premia and the yield curve,” the IMF said in its detailed annual analysis of the U.S. economy.

“There is a risk that the tightening impact on the economy could go well beyond the initial [0.25 percentage point] increase in the fed-funds rate, creating a risk that the economy stalls,” fund staff said.

A policy U-turn wouldn’t be without precedent. Both the European Central Bank and Sweden’s Riksbank were forced into rate reversals in 2011, and the Bank of Japan seesawed through rate moves in the 1990s and 2000, fund economists noted.

Such an about-face puts the Fed’s all-important credibility at stake, the IMF said.

The emergency lender also said the crises in Greece and Ukraine represent “unpredictable wild card” risks to the U.S. economy. So far, the impact in U.S. markets from the Greek crisis has been limited. The country has little direct exposure. But if it deteriorates further, it could hit broader European growth, which could weigh on the U.S. recovery.

Weaker global growth or a faster slowdown in China could also hit the U.S., sparking a selloff in equity markets, the IMF said.

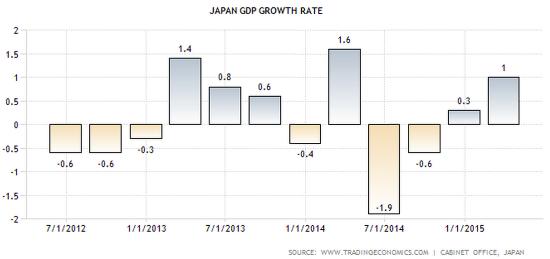

“Weaker global growth” indeed. The next two charts show GDP growth for Japan and Germany. Note that they’re both positive (barely) but are also lower than the previous year. So momentum was already slowing before Greece blew up and China’s stock bubble burst.

For the world’s biggest economy to respond to the above with steps to slow down its growth would be at best ill-mannered and at worst the kind of slap in the face that sets off global contagions. So yeah, it’s kind of hard to imagine.

Highlights:

- Throwing More Liquidity At Greece Is ‘Problematic’

- Situation In Greece Difficult To Forecast

- Liquidity Flight May Begin In Peripheral Countries

- Surprised By Muted Market Reaction To Greece

- We Are In’eye Of The Hurricane’ Situation Not Calm

- Germans Are ‘Disingenuous’ On Loans Considering History

- Germans Were Given Help After World War Ii

- Central Banks Throwing More Money To Restore Calm

- Says He Went Public On China Short Four Weeks Ago

- Says He’s ‘Rather Proud’ Of China Short Call

- Resolution Of Greek Crisis Lies Within Germany

- 70-80% Possibility Of Greek Exit From Euro

On whether he is surprised by the calm reaction of the markets, Gross said: “Yes, I am surprised…It appears that we’re in the eye of the hurricane. I do not believe that this situation really is calm.”

Apparently it can according to the author below – MT Ed

It’s not an overstatement to say that over the 6-year period beginning in September-2008, the US Federal Reserve went berserk with its Quantitative Easing (QE). The following chart shows that the US Monetary Base, an indicator of the net quantity of dollars directly created by the Fed*, had a gentle upward slope until around August of 2008, at which point it took off like a rocket. More specifically, the Monetary Base gained about 30% during the 6-year period leading up to September of 2008 and then quintupled (gained 400%) over the next 6 years. Is it therefore fair to say that the Fed has now ‘shot its load’ and will be unable to do much in reaction to the next financial crisis and/or recession?

Unfortunately, the answer is no. The sad truth is that the Fed is not only capable of doing a lot more, it will almost certainly pump a lot

more money into the economy the next time its senior management decides that the financial or economic wheels are falling off.

The Fed is capable of doing a lot more because it is not yet remotely close to running out of things to monetise. For example, the US Federal debt is presently about $18.1T and will probably top $20T within the next two years. This means that there is plenty of scope for the Fed to add to its current $2.5T stash of Treasury securities. Also, the Fed is not strictly limited in what it can monetise. Up until now it has been monetising Mortgage-Backed and Agency securities in addition to Treasury securities, but it could branch out into other asset-backed securities (those backed by auto loans or student debt, for instance), municipal bonds, investment-grade corporate bonds, and equity ETFs. If the situation were perceived to be sufficiently dire it could even change the rules to allow itself to monetise commercial and residential real-estate.

And the Fed almost certainly will do a lot more on the money-pumping front in the face of future economic and/or stock market weakness, because it has not only failed to learn the right lessons from the events of the past 15 years, it has learned exactly the wrong lessons. Rather than learning that injecting more money into the economy in an effort to mitigate the fallout from a busted bubble leads to a bigger bubble, a bigger bust, greater hardship and structural economic weakness, its senior management is convinced that the QE and interest-rate-suppression programs provided a substantial net benefit to the overall economy. Given this conviction in the righteousness of its previous actions, why wouldn’t the Fed do more of the same if the perceived need were to arise in the future? The answer, of course, is that it would. And it will.

In conclusion, those who think that the Fed is incapable of further monetary expansion do not have a good understanding of the situation, and those who believe that the Fed could do more, but will choose not to as the result of newfound financial prudence or concern for the well-being of savers, are naive.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair