Bonds & Interest Rates

The unorthodox specificity found in the International Monetary Fund’s latest forecasts for the US economy reintroduces a level of confusion and uncertainty for investors surrounding when the Federal Reserve will raise interest rates. News out of Washington last Thursday threw an absolute curveball at the Fed’s escape plan from zero interest rate policy. As a topic that was previously over-discussed and framed by the financial media, the IMF as the de facto global monetary policy authority has entered the discussion. Previous statements from the US Fed and their Federal Open Market Committee (FOMC) ensured for investors that the data dependency of the US Fed would dictate when we would see higher interest rates. The plea from the IMF Thursday could reshape this debate.

The unorthodox specificity found in the International Monetary Fund’s latest forecasts for the US economy reintroduces a level of confusion and uncertainty for investors surrounding when the Federal Reserve will raise interest rates. News out of Washington last Thursday threw an absolute curveball at the Fed’s escape plan from zero interest rate policy. As a topic that was previously over-discussed and framed by the financial media, the IMF as the de facto global monetary policy authority has entered the discussion. Previous statements from the US Fed and their Federal Open Market Committee (FOMC) ensured for investors that the data dependency of the US Fed would dictate when we would see higher interest rates. The plea from the IMF Thursday could reshape this debate.

Ultimately, the typical investor has to question whether the Fed raising rates in the second half of 2015 or the beginning

of 2016 would really make any material difference. And the assumption is a very likely, no. But it is important to discuss the motivation behind the IMF speaking out in this nature and entering an arena they typically stay absent from, which is imposing their view on US monetary policy. Furthermore, what are the risks they are implying, which really centres on the uncertainties in the global economy at present time?

PIMCO founder Bill Gross made the strongest argument for why the IMF made this recommendation to Chair Yellen and the FOMC. Gross suggests that in a post gold standard world where the US dollar is the world’s reserve currency, the global economy looks to it for stability. Thus, the IMF makes their case to the US Fed to remember to move slowly because as we see liquidity taken away from the global markets, US policy shocks have far reaching effects as witnessed over the last 8 years.

The problem this creates for the US Federal Reserve is their mandate to the US congress is to make policy decisions based on domestic employment and inflation. Global financial stability, which is arguably in their realm of interest, doesn’t dictate when they should raise rates. And as many economists have argued this week, waiting until 2016 with the jobless rate trending lower and expected to be below 5 per cent, is waiting too long to raise rates. As St. Louis Fed President Jim Bullard discussed last week, the Fed will be proactive in raising rates, not reactionary.

One could argue in many instances the Fed’s policy is aligned with the interests of the global economy, but this decoupling notion (of US and global growth) that was introduced in September of last year is once again exhibiting its challenges. If the Fed were to wait, they are giving credence to the IMF’s implied concerns.

It circles back to the earlier question of does it really make a difference when the Fed raises rates? No, not when. It’s clearer, however, a reputable institution doesn’t so much see trouble with when the Fed acts, but the effects of raising rates. It’s a liquidity issue for markets that risk the readjustments, like a 40 basis point swing in US treasuries in a moment’s time which we saw in October, 2014, or the German 10 year bund yield moving from one twentieth of a per cent to eight tenths of a percent in less than week.

The IMF has warned. Now we wait and see.

ECB chief said investors should get used to volatility

ECB chief said investors should get used to volatility

The bond move is really significant and that is sending huge shock waves through the market and driving investors to reduce their exposure to any risk,” said Philip Lawlor, a partner at London-based Smith & Williamson Investment Management LLP.

He said ECB President Mario Draghi had “injected a huge amount of uncertainty into markets and that is still having a major impact.”

…read the rest of this Wall Street Journal article posted and updated at June 4, 2015 9:40 a.m. ET HERE – M/T Ed

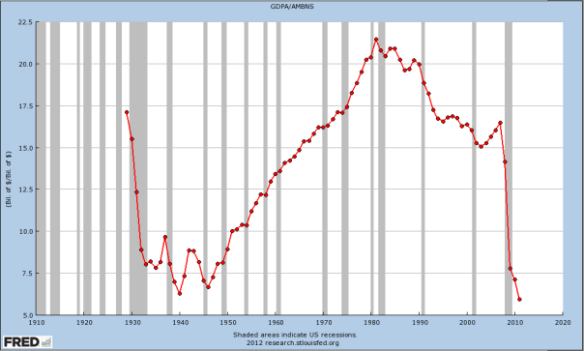

“The collapse in the VELOCITY of money illustrates the collapse in liquidity in the markets which will erupt in higher volatility we have not seen before. The VELOCITY of money declines as HOARDING rises. This is how empires, nations, and city states decline and fall.’

The New York banks have destroyed banking when Robert Rubin of Goldman Sachs managed to get the Clinton Administration to repeal Glass Steagall, Even Mario Draghi, head of the ECB, who is taking interest rates negative, was a vice chairman and managing director of Goldman Sachs International and a member of the firm-wide management committee (2002–2005). So the tentacles of NY spread wide and far.

That corruption in New York controlling Congress, the Justice Department, and the courts, has allowed the NY bankers to rise to the top of the world from a power elite perspective. They even control much of the media and Hollywood. This power which has transformed banking has been emulated by other banks around the world insofar as Transactional Banking has displaced Relationship Banking as the “new” way to make money.

But the banks outside the USA do not control their governments as fully as they do in the USA. Who does Hillary run to for money – the NY bankers. Yet, the battle over the banking industry’s reputation is emerging everywhere but New York. It intensified last Friday in Australia as two of Australia’s top regulators took a simultaneous shot at the “culture” at the heart of the nation’s largest financial institutions.

The banking industry suffers from Narcissistic Personality Disorder (NPD) which typically only affects 1% of the population but they all seem to be working at the top of the banks. NPD is when someone has unrealistic fantasies of success, power and intelligence. That seems to be a qualification to be on the board of the major New York Banks.

Ever since the repeal of Glass Steagall by Bill Clinton in 1999, this “new” way of making money transforming banking from Relationship to Transactional Banking has destroyed the economy in ways we are soon to discover. The VELOCITY of money has fallen to BELOW Great Depression levels. This is the destruction of Capitalism and I fear the response against the banks on the next downturn will lead to authoritarianism.

Taking interest rates NEGATIVE will not reverse this trend – it will accelerate the trend. This is all part of Big Bang. We seriously need to understand the nature of the problem or we will lose all rights and freedom because of what the bankers have set in motion. Transactional Banking only benefits the banks and fails to create a foundation for economic growth. This is not about Fractional Banking, this is all about the destruction of Relationship Banking that creates small businesses and employment.

The collapse in the VELOCITY of money illustrates the collapse in liquidity in the markets which will erupt in higher volatility we have not seen before. The VELOCITY of money declines as HOARDING rises. This is how empires, nations, and city states decline and fall.

Summary

Summary

- An analysis of past, present and potential future dividend income stream can serve as an excellent barometer of fair value.

- Dividends are a reliable fundamental metric.

- Stock prices are fickle, unpredictable and unreliable.

Introduction

In today’s low interest rate environment, prudent long-term investors, especially those in retirement, are best served by putting maximum weight and focus on dividends. There are important reasons why I support this position, and those reasons will be the focal point of this article. However, putting maximum weight and focus on dividends is not to the exclusion of other important fundamental metrics.

Prudent long-term investors, especially those in retirement, should also be…..continue reading HERE

Zürich, Switzerland

Zürich, Switzerland

Today… what we learned over dinner from a surprisingly smart central banker.

But first, to the markets…

The Dow shot up 121 Dow points yesterday, recovering most of Tuesday’s slide.

In a series of business meetings Tuesday and Wednesday, we explained why nobody but us is rooting for a depression.

Yes, there’s no point in hiding it. We would like to see a depression. Short, swift, and decisive – a quick and sharp end to the biggest credit expansion in all of history.

As secretary of the Treasury Andrew Mellon said after the 1929 stock market crash:

Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate. It will purge the rottenness out of the system.

High costs of living and high living will come down. People will work harder, live a more moral life. Values will be adjusted, and enterprising people will pick up the wrecks from less competent people.

Credit Cannot Increase Forever

“It’s unbelievable,” said colleague Merryn Somerset Webb. Merryn is the editor ofMoneyWeek magazine in London.

“London property prices just keep going up and up. It’s so expensive our writers can’t afford to live here anymore. I’m thinking of moving the business to Edinburgh.”

You can’t build a solid economy on the jelly of unaffordable housing, unpayable debts, and unsustainable asset prices. But that’s what we’ve got.

The only way to get down to something more reliable… more real… and healthier… is to wash away the financial glop and goo that has accumulated during the last 30 years.

One way or another, the credit expansion that began after War World II must come to an end. About that we have no doubt. Contrary to the evidence of the last half-century, credit cannot increase faster than income forever.

It is mathematically, economically, and financially impossible.

But when will it stop?

“The trouble with you guys,” says a loyal reader (or words to this effect), “is that you are generally right… but you are always early.” Early?

Certainly. In the case of the credit bubble, we were nearly 40 years ahead of the curve.

We saw the handwriting on the wall back in the 1970s! We thought it said, “The End Is Nigh for the Paper Money System.”

After all, no paper money ever lasted for very long.

Not All Central Bankers Are Idiots…

But we misread the graffiti…

We don’t know where “nigh” is, but we’re pretty sure the end wasn’t close to it. Because, here we are four decades later, and the paper money system is still going strong.

And guess what?

We are still sure that it is headed for a debacle.

But when?

“It could take another two or three decades.”

That was the answer we got from a top central banker. We had the rare treat of dining with one last night.

We’ll keep his identity to ourselves, to protect his job and the reputation of the central bank. But he was a breath of fresh air. And a relief. Now, we can say with confidence: Not all central bankers are idiots.

Here’s what he told us:

It is doomed, of course. But not necessarily soon. As long as the major tendency of the economy is toward deflation, central banks can print money without causing consumer price inflation. They can buy bonds and keep buying them.

When they buy bonds, they tend to lower interest rates. They also finance government deficits. And, from Japan’s example, it looks as though they can do it almost indefinitely.

That’s right: They can keep this gig going… until they can’t. When it ends is anybody’s guess.

It is in the future, where no man goeth with GPS or map in hand…

Who Wants a Depression?

And we goeth there only in hopes of discovering a depression. Everyone else hopes to discover many more years of asset price inflation, boom, bubble, and central bank management. This distinction is an important one.

At least WE think so.

Everyone in government, industry, commerce, and academia has an unspoken prejudice for the bubble.

Wall Street wants to sell you stocks and bonds. Industry and commerce have products to unload… not to mention mergers and acquisitions to finance.

And governments all over the planet are running deficits and counting on low interest rates to pay for their zombie wars and crony programs.

Who speaks for the future? Who stands up for a healthy, sane, and real economy?

Who champions the cause of the little guy… the small investor… the small businessman… the ordinary working stiff?

Who wants a depression?

Tune in tomorrow!

Regards,

Bill

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair