Bonds & Interest Rates

Get ready for a disastrous year for U.S. government bonds. That’s the message forecasters on Wall Street are sending.

Get ready for a disastrous year for U.S. government bonds. That’s the message forecasters on Wall Street are sending.

With Federal Reserve Chair Janet Yellen poised to raise interest rates in 2015 for the first time in almost a decade, prognosticators are convinced Treasury yields have nowhere to go except up. Their calls for higher yields next year are the most aggressive since 2009, when U.S. debt securities suffered record losses, according to data compiled by Bloomberg….

Last week we learned that the key to a strong economy is not increased production, lower unemployment, or a sound monetary unit. Rather, economic prosperity depends on the type of language used by the central bank in its monetary policy statements. All it took was one word in the Federal Reserve Bank’s press release — that the Fed would be “patient” in raising interest rates to normal levels — and stock markets went wild. The S&P 500 and the Dow Jones Industrial Average had their best gains in years, with the Dow gaining nearly 800 points from Wednesday to Friday and the S&P gaining almost 100 points to close within a few points of its all-time high.

Last week we learned that the key to a strong economy is not increased production, lower unemployment, or a sound monetary unit. Rather, economic prosperity depends on the type of language used by the central bank in its monetary policy statements. All it took was one word in the Federal Reserve Bank’s press release — that the Fed would be “patient” in raising interest rates to normal levels — and stock markets went wild. The S&P 500 and the Dow Jones Industrial Average had their best gains in years, with the Dow gaining nearly 800 points from Wednesday to Friday and the S&P gaining almost 100 points to close within a few points of its all-time high.

Just think of how many trillions of dollars of financial activity that occurred solely because of that one new phrase in the Fed’s statement. That so much in our economy hangs on one word uttered by one institution demonstrates not only that far too much power is given to the Federal Reserve, but also how unbalanced the American economy really is.

While the real economy continues to sputter, financial markets reach record highs, thanks in no small part to the Fed’s easy money policies. After six years of zero interest rates, Wall Street has become addicted to easy money. Even the slightest mention of tightening monetary policy, and Wall Street reacts like a heroin addict forced to sober up cold turkey.

While much of the media paid attention to how long interest rates would remain at zero, what they largely ignored is that the Fed is, “maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities.” Look at the Fed’s balance sheet and you’ll see that it has purchased $25 billion in mortgage-backed securities since the end of QE3. Annualized, that is $200 billion a year. That may not be as large as QE2 or QE3, but quantitative easing, or as the Fed likes to say “accommodative monetary policy” is far from over.

What gets lost in all the reporting about stock market numbers, unemployment rate figures, and other economic data is the understanding that real wealth results from production of real goods, not from the creation of money out of thin air. The Fed can rig the numbers for a while by turning the monetary spigot on full blast, but the reality is that this is only papering over severe economic problems. Six years after the crisis of 2008, the economy still has not fully recovered, and in many respects is not much better than it was at the turn of the century.

Since 2001, the United States has grown by 38 million people and the working-age population has grown by 23 million people. Yet the economy has only added eight million jobs. Millions of Americans are still unemployed or underemployed, living from paycheck to paycheck, and having to rely on food stamps and other government aid. The Fed’s easy money has produced great profits for Wall Street but it has not helped — and cannot help — Main Street.

An economy that holds its breath every six weeks, looking to parse every single word coming out of Fed Chairman Janet Yellen’s mouth for indications of whether to buy or sell, is an economy that is fundamentally unsound. The Fed needs to stop creating trillions of dollars out of thin air, let Wall Street take its medicine, and allow the corrections that should have taken place in 2001 and 2008 to liquidate the bad debts and malinvestments that permeate the economy. Only then will we see a real economic recovery.

This analysis is assembled to paint a picture of the current Global Financial condition. The first article “These Are Astonishing Figures, Evidence Of A 1930s-Style Depression” can be found HERE or click the chart below – Editor Money Talks

….then there is this:

The Case for Gold in One Chart

The purpose of this paper is not to make the case for investing in precious metals (plenty has already been written on this topic), but rather to lay out the options available to the investors who has made up his mind to do so.

Before going into any great detail, let’s pause for a moment to take a helicopter view of our financial system in order to better understand gold’s position in it. Most people are well aware that gold is a scarce resource but are usually not aware of the sheer volume of other financial products which currently exist. The following chart provides an overview of our financial system and lays the case for gold quite succinctly.

A financial meltdown would see the upper layers of the pyramid being liquidated in a panic that would likely involve the opaque over-the-counter derivatives markets. A few of the world’s largest banks hold the bulk of all derivative contracts, which have notional amounts in the 10s of times their assets and 100s of times their market capitalizations.

A financial meltdown would see the upper layers of the pyramid being liquidated in a panic that would likely involve the opaque over-the-counter derivatives markets. A few of the world’s largest banks hold the bulk of all derivative contracts, which have notional amounts in the 10s of times their assets and 100s of times their market capitalizations.

Whilst the upper layers evaporate as the market for most IOUs simply stops existing, capital will seek refuge in the “most marketable good” or the most liquid asset further down the pyramid. Many people holding assets located at the top of the pyramid will lose parts of their capital on the way down in the flight to liquid and to less-risky assets. After most of their wealth literally has evaporated, they will finally come to the conclusion that gold is the ultimate store of value.

A look at recent history reminds us of the intrinsic value of paper money, which is the paper that it is printed on. One picture in support of this case is certainly worth a thousand words.

“Paper money eventually returns to its intrinsic value – zero.” ~ Voltaire

Download the complete paper: ![]() How to Own Precious Metals

How to Own Precious Metals

The Bond Market Bubble is Reaching Epic Proportions

The Bond Market Bubble is Reaching Epic Proportions

Too Much Cheap Money Sloshing Around Financial Markets

Low Gasoline Prices are Inflationary in the Big Picture

Wages Starting to Spike

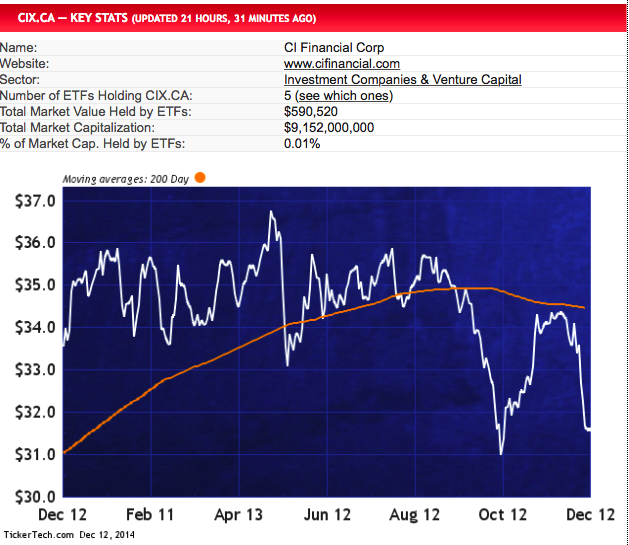

#10. CI Financial Corp (TSE:CIX.CA) — 4.0% YIELD

At #10, CI Financial is engaged in the management, marketing, distribution and administration of mutual funds, segregated funds, structured products and other fee-earning investment products for Canadian investors. Co. operates two reportable segments: Asset Management and Asset Administration. The asset management segment provides the management of mutual, segregated, pooled and closed-end funds, structured products and discretionary accounts. The asset administration segment involves the sale of mutual funds and other financial products, and ongoing service to clients and capital market activities.

![]()

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair