Bonds & Interest Rates

Also Faber on The Swiss Gold Referendum “It is about time that the power of central banks is contained and regulated. The Swiss gold initiative, while not ideal, would be a starting point,”

Also Faber on The Swiss Gold Referendum “It is about time that the power of central banks is contained and regulated. The Swiss gold initiative, while not ideal, would be a starting point,”

TRISH REGAN: Bond investor Bill Gross is saying deflation is a “growing possibility” as governments worldwide struggle to create inflation and to stimulate growth. In his second investment outlook since joining Janus Capital, Mr. Gross writes, “The real economy needs money printing, yes, but money spending more so. Until then, deflation remains a growing possibility, not the kind that creates prosperity but the kind that’s trouble for prosperity.”

Well is Mr. Gross right and should investors bid good bye to double-digit returns in this new normal? Joining me here to discuss via Skype, Marc Faber, editor and publisher of Gloom, Boom and Doom. Hello, Marc. Always good to see you. What do you think here about what Bill Gross is saying? Do you think in fact deflation is a real possibility for the United States?

MARC FABER: Well, I think the concept of inflation and deflation is frequently misunderstood because in some sectors of the economy you can have inflation and in some sectors deflation. But if the investment implication of Bill Gross is that – and he’s a friend of mine. I have high regard for him. If the implication is that one should be long US treasuries, to some extent I agree. The return on 10-year notes will be miserable, 2.35 percent for the next 10 years if you hold them to maturity in each of the next 10 years.

However, if you compare that to French government bonds yielding today 1.21 percent, I think that’s quite a good deal, or Japanese bonds, a country that is engaged in a Ponzi scheme, bankrupt, they have government bond yields yielding 0.43 percent.

…related:

Marc Faber Warning : Soon I will soon be proven right about The Market Crash

Sooner or Later The Market Forces will Reverse

Market Buzz – China’s Central Bank

Market Buzz – China’s Central Bank

China’s central bank succumbed to political and market pressure and cut interest rates for the first time in more than two years, in a sign that the country’s leadership is leaning toward more sweeping measures to bolster flagging economic growth.

China’s cut helped oil prices rise on Friday for crudes first weekly gain in two months with benchmark Brent crude returning to above US$80 a barrel after a rally triggered by China’s interest rate cut and speculation of an OPEC output cut. China is the largest net importer of petroleum and metals, and the rate cut sent most commodity prices higher, albeit from beat down levels.

Brent oil rose US$1.03 to settle at US$80.36 a barrel. It had risen as much as US$2.28 earlier to a session high of US$81.61. WTI or U.S. crude finished up US$0.66 at US$76.51, after an intraday peak at US$77.83.

The surprise move by the People’s Bank of China late Friday comes after a series of piecemeal easing measures that failed to encourage banks to lend and companies to borrow. Several economic indicators—from investment growth to factory production to retail sales—showed weakness last month. A number of pundits are not in the camp that China could miss its annual growth target—set at about 7.5% for 2014—for the first time since the 1998 Asian financial crisis. We question whether or not the numbers are accurate in the first place, but the trend in terms of slower growth is something to pay attention to.

Expectations of a production cut from the Organization of the Petroleum Exporting Countries (OPEC) at its November 27th meeting also fed the rally, although profit-taking emerged later, along with selling by those expecting another tumble next week.

KeyStone’s Latest Reports Section

11/21/2014

CASH RICH BASE METAL PRODUCER POST SOLID Q4, SHARES JUMP AMID TAKEOVER SPECULATION – HOLD

Words are important. This is not just a headline, it is a reality…

Words are important. This is not just a headline, it is a reality…

Draghi says ECB will ‘do what it must’ on asset buying to lift inflation

Not ‘do what it thinks would be the best course for the European economy’, not ‘choose the path of least resistance in guiding the financial system to recovery’… the ECB will DO WHAT IT MUST.

As I have written til I’m blue in the face for the last 10 years, we are in the age of ‘Inflation onDemand‘©, 24/7 and 365. “…do what it must”… let that sink in for a moment.

Japan is trying to kill the Yen, China is dropping interest rates and the world over we have a rolling inflationary operation that is little more than a game of Whack-a-Mole. BoJ popped up a couple weeks ago and now this one…

US Situation

Transitioning to the country and policy making establishment that has truly shown ‘em how it’s done over the last 6 years, we view the S&P 500 with its eternal attendant, ZIRP and add a view of the CPI as well. One message that can be interpreted from this chart is that stock markets have been used (controlled) as a mechanism for asset owners to keep up with the reported effects of inflation (CPI). Saving has been disallowed, legislated by policy right out of the equation. Everybody into the pool, if you’ve got the bankroll to play.

We have maintained since the post 2012 lift off of the most intense phase of the inflated stock bull market that there is and has been no bubble in stocks (though they have become over valued* even by traditional metrics) but rather, a massive and ongoing bubble in global policy making.

First Alan Greenspan laid the groundwork and the initial blueprint (asset inflation), then his inflation operation was liquidated with extreme decisiveness and now, from the ashes we have a new global asset inflationary operation born not of good intention or rationally sound strategy. It is pure and simple desperation. The ECB will “do what it must”. The US Federal Reserve has done “what it must” since instituting ZIRP nearly 6 full years ago and through QE’s 1-3.

Straw Man

It sure looks like the whole debate about 2015’s coming interest rate hikes are another Straw Man stood up to manage market expectations (see Deflationary Straw Man), to give the impression that Policy Central is still in control and that they have decisions to make. There is no decision folks. The inflationary operation, now gone global, is an all-in, all-or-nothing’ proposition.

It sure looks like the whole debate about 2015’s coming interest rate hikes are another Straw Man stood up to manage market expectations (see Deflationary Straw Man), to give the impression that Policy Central is still in control and that they have decisions to make. There is no decision folks. The inflationary operation, now gone global, is an all-in, all-or-nothing’ proposition.

Greenspan’s inflation ended up being less than nothing. It was resolved in a sea of debits that assigned negative value to the system. The ongoing effects of inflation feel good to some people now (especially those who get to lap up the silver spoon’s gifts that keep on giving first and foremost as opposed to those savers and paycheck-to-paycheckers who just get to suck on ZIRP-eternity) but inflation is never a lasting benefactor. It is a subtractor over the years and decades as savings and productivity are replaced by money printing.

We will clip this post here and go on managing the market as always, taking what it gives, managing against what it is one day going to take and keep the big picture view in place at all times. That view very simply is that 6 years on from the US financial crisis (ongoing, though that is an unpopular notion at this time) a global  cadre of policy makers are playing a transparent game of Whack-a-Mole trying to one-up each other until the whole thing flushes once again.

cadre of policy makers are playing a transparent game of Whack-a-Mole trying to one-up each other until the whole thing flushes once again.

* Although it is worth asking the question ‘what is value today, anyway?’ when considering the constant inputs and distortions inflicted by policy makers. Anyone care to take a guess on that one?

As Japanese Prime Minster Shinzo Abe has turned his country into a petri dish of Keynesian ideas, the trajectory of Japan’s economy has much to teach us about the wisdom of those policies. And although the warning sirens are blasting at the highest volumes imaginable, few economists can hear the alarm. (A longer version of this article can be found in Euro Pacific Capital’s Global Investor Newsletter.)

As Japanese Prime Minster Shinzo Abe has turned his country into a petri dish of Keynesian ideas, the trajectory of Japan’s economy has much to teach us about the wisdom of those policies. And although the warning sirens are blasting at the highest volumes imaginable, few economists can hear the alarm. (A longer version of this article can be found in Euro Pacific Capital’s Global Investor Newsletter.)Although the Japanese economy has been in paralysis for more than 20 years, things have gotten worse since December 2012 when Abe began his radical surgery.. From the start, his primary goal has been to weaken the yen and create inflation. On that front, he has been a success. The yen has fallen 23% against the dollar and core inflation, which was running slightly negative in 2012, has now been “successfully” pushed up to 3.1% according to the Statistics Bureau of Japan.

But there is no great mystery or difficulty in creating inflation or cheapening currency. All that is needed is the ability to debase coined currency, print paper money or, as is the case of our modern age, create credit electronically. These “successes” should not come as a surprise when one considers the relative size of Abe’s QE program. For much of the past two years the Bank of Japan (BoJ) has purchased about 7 trillion yen per month of Japanese government bonds, which is the equivalent of about $65 billion U.S. [Forbes 9/24/14, Charles Sizemore] While this is smaller than the $85 billion per month that the Federal Reserve purchased during the 12-month peak of our QE program, it is much larger in relative terms.

The U.S. has roughly 2.5 times more people than Japan. Based on this multiplier, the Japanese QE program equates to $162.5 billion, or 91% larger than the Fed’s program at its height. But, according to IMF estimates, the U.S. GDP is 3.3 times larger than Japan. Based on that multiplier, Japanese QE equates to $214.5 billion per month, or 152% larger. And unlike the Federal Reserve, the Bank of Japan hasn’t even paid any lip service to the idea that its QE program will be scaled back any time soon, let alone wound down.

In fact, Abe’s promises to do more were spectacularly realized in a surprise move on October 31 when the BoJ, claiming “a critical moment” in its fight against deflation, announced a major expansion of its stimulus campaign. (The fact that official inflation is currently north of 3% – a multi-year high, seems to not matter at all.)

At the same time the BoJ also announced its intention to roughly triple its pace of its equity and property purchases on Japan’s stock market. According to Nikkei’s Asian Review (9/23/14), the BoJ now holds an estimated 7 trillion yen portfolio of Japanese stock and real estate ETFs. Even Janet Yellen has yet to cross that Rubicon.

And what has this financial shock and awe actually achieved, other than 3% inflation, a weaker yen, a stock market rally, and continued international praise for Abe? Well, unfortunately nothing other than a bona fide recession and a growing threat of stagflation.

The weaker yen was supposed to help Japan’s trade balance by boosting exports. That didn’t happen. In September, the country reported a trade deficit of 958 billion yen ($9 billion), the 27th consecutive month of trade deficits. The deterioration occurred despite the fact that import prices rose steeply, which should have reduced imports and boosted exports. And while some large Japanese exporters credited the weak yen for easier sales overseas, small and mid-sized Japanese businesses that primarily sell domestically have seen flat sales against rising fuel and material costs.

But price inflation is not pushing up wages as the Keynesians would have expected. In August, Japan reported real wages (adjusted for inflation) fell 2.6% from the year earlier, the 14th straight monthly decline. This simply means that Japanese consumers can buy far less than what they could have before Abenomics. This is not a recipe for happy citizens.

Japanese consumers must also deal with Abe’s highly unpopular increase of the national consumption tax from 5% to 8% (with a planned increase to 10% next year). The sales tax was largely put in place to keep the government’s debt from spiraling out of control as a result of the fiscal stimulus baked into Abenomics. And while economists agree nearly universally that the price increases that have resulted from the sales tax have caused a sharp drop in consumer spending, they fail to apply the same logic that price increases due to inflation will deliver the same result.

A bedrock Keynesian belief is that falling prices create recession by inspiring consumers to delay purchases until prices fall further. According to the theory, even a 1% annual drop in prices could be sufficient to decimate consumers’ willingness to spend. Conversely, they believe rising prices, otherwise known as inflation, will spur spending, and growth, as it inspires people to buy now before prices rise further. But if consumers have clearly been put off by rising prices due to taxation, why would they be encouraged if they were to rise for monetary reasons? Don’t look for an explanation, there isn’t any. In reality, as any store owner will tell you, shoppers shop when prices are low and stay at home when prices are high.

Despite the bleak prospects for Japan, Abe continues to bask in the love of western economists and investors. In an October 6 interview with the The Daily Princetonian, Paul Krugman, who has emerged as Abe’s chief champion and apologist, responded to a question about the European economic crisis by saying “Europe need something like Abenomics only Abenomics, I think, is falling short, so they need something really aggressive in Europe.” A Bloomberg article ran on November 18 under the headline “Abe’s $1 Trillion Gift to Stock Market Shields Recession Gloom.” So according to Bloomberg, Abenomics is not responsible for the country’s fall back into recession, which hurts everyone, but it is responsible for the surging stock market, which primarily benefits the wealthy.

One wonders how much more bad news must come out of the Japanese experiment in mega-stimulus before the Keynesians reassess their assumptions? Oh wait…I’m sorry, for a second there I thought they were susceptible to logic. But those who are not blinded by left-wing dogma should take a good look at where the road of permanent stimulus ultimately leads.

Subscribe to Euro Pacific’s Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

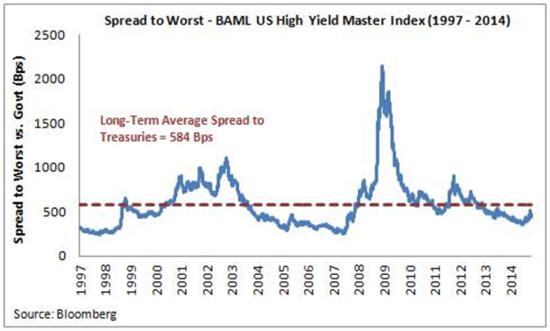

One of the surest signs that a bubble is about to burst is junk bonds behaving like respectable paper. That is, their yields drop to mid-single digits, they start appearing with liberal loan covenants that display a high degree of trust in the issuer, and they start reporting really low default rates that lead the gullible to view them as “safe”. So everyone from pension funds to retirees start loading up in the expectation of banking an extra few points of yield with minimal risk.

This pretty much sums up today’s fixed income world. And if past is prologue, soon to come will be a brutally rude awakening. Most of the following charts are from a long, very well-done cautionary article by Nottingham Advisors’ Lawrence Whistler:

Junk yield premiums over US Treasuries are back down to housing bubble levels:

…continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair