Bonds & Interest Rates

There is a popular American military term called a “last stand”, which is meant to describe a situation where a combat force attempts to hold a defensive position in the face of overwhelming odds. The defensive force usually sustains very heavy casualties or is completely destroyed, as happened at Custer’s Last Stand. General Custer, misreading his enemy’s size and ability, fought his final and fatal battle of Little Bighorn; leading to complete annihilation of both himself and his troops.

There is a popular American military term called a “last stand”, which is meant to describe a situation where a combat force attempts to hold a defensive position in the face of overwhelming odds. The defensive force usually sustains very heavy casualties or is completely destroyed, as happened at Custer’s Last Stand. General Custer, misreading his enemy’s size and ability, fought his final and fatal battle of Little Bighorn; leading to complete annihilation of both himself and his troops.

The Japanese government is now partaking in a truly incredulous measure to expand its QE program in a desperate attempt to de-value its currency and re-inflate asset bubbles around the world. In other words, Japan is constructing its own version of a “last stand”.

In a final attempt to grow the economy and increase inflation, Japan announced a plan to escalate its QE pace

to $700 billion per year. In addition to this, Japan’s state pension fund (the GPIF), intends to dump massive amounts of Japanese government bonds (JCB’s) and to double its investment in domestic and international stocks. All this in a foolish attempt to increase inflation, which Japan mistakenly believes will spur on economic growth. But these failed policies have now caused Japan to enter into an official recession once again, as GDP fell 1.6% in Q3 after falling 7.1% in the previous quarter.

Japan is now guaranteed to be successful in the total destruction of its currency, the complete destruction of its economy and the collapse of the markets it is attempting to manipulate around the world. To fully understand its misguided reasoning, we have to explore how Japan got here in the first place.

Coming out of WW II, Japan enjoyed a three-decade period referred to as its “Economic Miracle”. This “miracle” was instigated by a booming post-war export economy helped by prudent fiscal policies, which was meant to encourage household savings. Japan’s standard of living soared among the highest in the world. Japan sailed into the 1980’s on the wave of robust economic growth. However, if we have learned one thing after all these years, it’s Government’s insatiable need to meddle with the free market, even when they don’t need to. Accordingly, the 1985 Plaza Accord was sought to weaken the U.S. dollar and German Deutsche Mark against the yen. The Bank of Japan, in an attempt to offset the rising yen, drastically reduced interest rates. The BOJ’s loose monetary policy in the mid-to-late 1980s led to aggressive speculation in domestic stocks and real estate, pushing the prices of these assets to astonishing levels. From 1985 to 1989, Japan’s Nikkei stock index tripled to 39,000 and accounted for more than one third of the world’s stock market capitalization.

By the late 1980s, Japan had transitioned from a “miracle” economy to its infamous bubble economy, in which stock and real estate prices soared to stratospheric heights driven by a speculative mania. Japan’s Nikkei stock market hit an all-time high in 1989, then crashed, leading to a severe financial crisis and long period of economic stagnation that Japan is still entrenched in. It has now become known as Japan’s “Lost Decades.”

Shortly after the bubble burst, Japan embarked on a series of stimulus packages totaling more than $100 trillion yen–leaving an economy that was once built on savings to eventually be saddled with a debt to GDP ratio that now exceeds 240%–the highest in the industrialized world. Making matters worse, the BOJ has more recently engaged in an enormous campaign to completely vanquish deflation, despite the fact that the money supply has been in a steady uptrend for decades. At the end of 2012, we were introduced to Abenomics, which is Premier Shinzo Abe’s plan to put government spending and central-bank money printing on steroids. His strategy is crushing real household incomes (down 6%) and caused GDP to contract 7.1% in Q2.

With the rumored delay of its sales tax, Japan is clearly making no legitimate attempt to pay down its onerous debt levels. Therefore, one has to assume this huge addition to their QE is an attempt to reduce debt through devaluation and achieve growth by creating asset bubbles larger than the ones previously responsible for Japan’s multiple lost decades. This will not return Japan back to the days of its “economic miracle”, where the economy grew on a foundation of savings, investment and production.

The sad reality is that Japan is quickly surpassing the bubble economy achieved during the late 1980’s. Its equity and bond markets have become more disconnected from reality than at any other time in its history. The nation now faces a complete collapse of the yen and all assets denominated in that currency.

This is clearly Japan’s last stand and there is no real exit strategy except to explicitly default on its debt. But an economic collapse and a sovereign debt default on the world’s third largest economy will contain massive economic ramifications on a global scale. Japan should be the first nation to face such a collapse. Unfortunately; China, Europe and the U.S. will also soon face the consequences that arise when a nation’s insolvent condition is coupled with the complete abrogation of free markets by government intervention.

“It’s called a “credit cycle” for a reason. Rising rates come around sooner or later – often ferociously – after a long period of apparent stability, over-optimism, overpriced equities and artificially suppressed yields.”

“It’s called a “credit cycle” for a reason. Rising rates come around sooner or later – often ferociously – after a long period of apparent stability, over-optimism, overpriced equities and artificially suppressed yields.”

We’ve been meaning to write about what hasn’t happened yet.

Not that we claim any knowledge of tomorrow or the day after. But we can look at the present. And here’s a guess about where it might lead.

The middle classes – aka “the voters” – expressed themselves last week. They have been sorely used and they know it.

The biggest money-fabricating program of all time – the Fed’s QE – has done nothing for them. Instead, it has made their lot worse.

Investment in new business output has gone down. Their meager savings produce no revenue. And “breadwinning jobs” are scarce.

For all the talk of an “improving labor market,” there is no sign of it in wages. The typical household has $5,000 less income than it had when the 21st century began.

Cold, Dark and Desperate

Meanwhile, Europe and Japan grow cold, dark and desperate. Last week, ECB chief Mario Draghi announced the central bank would buy another €1 trillion of bonds to try to light a fire under the euro-zone economy.

And Bank of Japan governor Haruhiko Kuroda got out his matches the week before, claiming potentially unlimited tinder.

Can the US resist the worldwide slump?

Our view is it’s just a matter of time before either the US economy or US stock market begins to wobble.

We could see the Dow fall 1,000 points or more… or we could hear GDP growth has gone negative… or both.

Then what?

It’s a good bet that the Yellen Fed would intervene again – hoping to keep a small problem from becoming a bigger one.

Ever since the 1930s, central bankers have learned that they will scarcely ever be criticized for overreacting. But if they sit on their hands, they will be damned to hell.

And ever since Alan Greenspan’s 1987 “put,” the Fed has backed up the stock market with whatever policy it deemed appropriate.

Lower rates? QE? It’ll do “whatever it takes.”

Janet Yellen is aware that the two previous Fed chairmen were hailed for having saved the economy from destruction. She won’t want to be the first to let it fail.

While we are guessing, we’ll suppose each rescue effort will be more costly and less effective than the one that preceded it.

That’s the way “stimulus” works. Like looking at naughty pictures, the first are exciting and titillating. Later, they are just boring and sordid.

Still, a vigorous new response from the Fed would probably produce another rise in financial asset prices. But then what?

Coaxing Stocks Higher

Central bank activism – stimulating credit creation with artificially low interest rates – only works when people see little risk of default or rising rates. But that risk cannot be ignored forever.

It’s called a “credit cycle” for a reason. Rising rates come around sooner or later – often ferociously – after a long period of apparent stability, over-optimism, overpriced equities and artificially suppressed yields.

When that happens, the central banks lose their ability to coax stocks higher with lower rates.

The Fed has been interfering with the credit cycle for the last 20 years. But when it believes it can overturn the cycle for good… that is when it becomes a big loser.

At that point, and it could be months – or years – ahead, we are likely to see central banks become more creative.

What else can they do?

They will still be fully committed to “saving” the economy. When their policy tools fail, they will have to come up with something different.

What? We see three things:

1) Central banks will buy stocks. Japan, as usual, is ahead of the curve.

2) Governments will bring out large fiscal stimulus packages aimed at infrastructure “investments” that are supposed to pay for themselves.

3) Some form of Direct Monetary Funding from central banks will finance these stimulus packages. Central banks will simply “print” the needed funds.

All of these measures are either already in service or much discussed in the leading financial journals.

What will they mean to stocks? Bonds? The dollar?

Stay tuned…

Regards,

Bill Bonner

Whatever about the future effects of monetary stimulus, it cannot be said that past efforts have been good for inflation-sensitive commodities.

In fact, the opposite is true.

As Bill alludes to, commodities are plunging as the exchange value of the dollar rises versus foreign currencies.

As you can see below, the iShares S&P GSCI Commodity-Indexed Trust (GSG) – which tracks a broad basket of commonly traded commodities – is down 32% from its 2011 peak. And it recently took out the low it set in June 2012.

This decline happened under the Fed’s QE.

And gold – the finite yardstick against which infinite currencies are supposed to be measured – has also come under huge selling pressure.

The chart below, going back two years, shows that not only has gold been in a downtrend, but also it has taken out its June and December 2013 lows at around $1,200 an ounce.

Again, most of this decline happened under the Fed’s QE.

This does not mean you should rush out and sell your gold. Gold is not a speculation. It is an insurance policy against monetary disaster. And if Bill’s thesis is right, owning some gold is prudent.

But judging from the charts above, there could be a lot more price falls to come before that policy pays out.

Saudi Arabia is barging ahead with a reckless plan to try and curb American oil production by dropping the global price. But, the news is in and America is not stopping its quest for energy independence any time soon. Continued strong American production will bolster these three companies while they keep piping profits to their shareholders through big dividends.

The drop in the price of crude has negatively affected master limited partnerships (MLP) values almost across the board. The decline in MLP prices has driven some very high quality partnerships to what I view as a very attractive 5+10 investment potential. By this I mean a 5% current yield combined with 10% annual distribution growth. That is a combination which will make any income focused investor very happy over a multi-year holding period. Before I give my list of three high quality MLPs to pick up now, a little discussion on the somewhat secret energy war.

The cause of the recent drop in the price of WTI crude oil from the mid $90′s to below $80 can be laid at the doorstep of Saudi Arabia. Historically, the Saudis have been willing to curtail production to help prop up oil prices for all of the OPEC members. However, this time around it is the emergence of the U.S. as one of the top oil producers that has caused the Saudis to change their tactics. The belief is that Saudi Arabia has allowed the price of crude to decline to force U.S. energy companies to curtail their drilling efforts and reduce production.

Saudia Arabia has even offered its oil at discounted rates to U.S. buyers.

The U.S. energy companies know this is going on and have vowed to continue drilling and driving the U.S. closer to energy independence. In the more productive plays, energy exploration and production companies have stated that they can remain profitable down to as low as $40 per barrel. This is a war that the U.S. energy sector will win and Saudi Arabia needs to find different markets for its oil.

The midstream MLPs provide the services that the oil and gas drillers need to get their products from the wellhead to the end users. Energy production growth requires continued expansion of the midstream infrastructure. Midstream assets include gathering and processing facilities in the energy plays, oil and gas pipelines, other transportation assets, and storage facilities. The larger midstream MLPs have long term plans to continue their growth records, the financial strength to weather short term adversity, and established positions in the best energy plays and at the major energy processing locations. As I noted above, the combination of a 5% yield plus an outlook for 10% distribution growth is a sweet spot to generate an attractive and growing income stream in this sector. Here are three MLPs that will power your portfolio as the energy sector works through the current energy price disruption.

Enable Midstream Partners LP (NYSE: ENBL) went public with an April 2014 IPO, but is already one of the largest midstream MLPs. Enable was spun off by two large natural gas public utility companies. It provides the full range of midstream services. With a $10 billion market cap, ENBL yields 5.02% and is forecast to grow its distribution by 11% per year.

EnLink Midstream Partners LP (NYSE: ENLK) is a $6.9 billion market cap MLP formed in early 2014 by the combining of the Crosstex Energy MLP and the Devon Energy (NYSE: DVN) midstream assets. EnLink has a four pronged approach to generate growth, allowing the company flexibility in the pursuit of its growth goals. ENLK currently yields 4.9% and management has stated a growth target of about 10%. This one is a sleeper with the potential to perform better than the forecast.

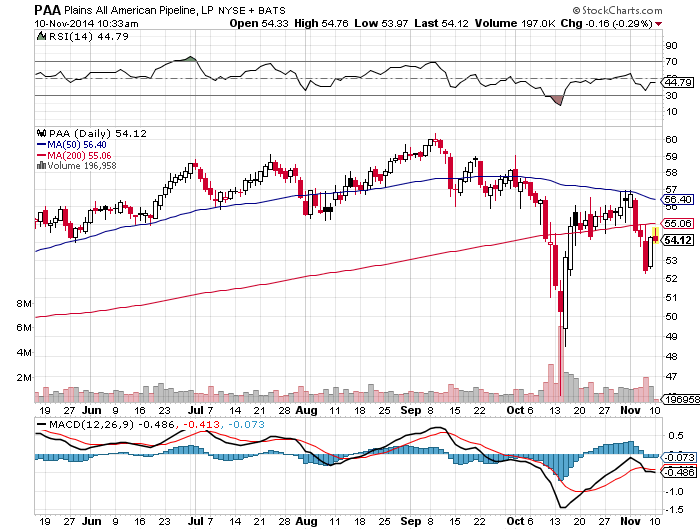

Plains All American Pipeline, LP (NYSE: PAA) primarily provides crude oil and refined products pipeline, rail transport, and storage services. Plains offers the combination of one of the best asset portfolios in the midstream sector and a very conservative management philosophy. The PAA distribution has grown by an 8.5% compound annual growth rate for the last 10 1/2 years, and has put up 10% growth over the last three years. The current 4.9% yield is well above the sub-4.5% average PAA has carried for the last year.

MLPs are an integral part of the income strategy with my newsletter, The Dividend Hunter. And there are currently several of them in my Monthly Paycheck Dividend Calendar.

The Monthly Dividend Paycheck Calendar is set up to make sure you’re getting 2, 3, even 5 dividend paychecks per month from stable, reliable stocks with high yields. And that you’re getting payments every month, not just once a quarter like some investors.

The Calendar tells you when you need to own the stock, when to expect your next payout, and how much you could make from stable, low risk stocks paying upwards of 8%, 10%, even 11%. I’ve done all the research and hard work, you just have to pick the stocks and how much you want to get paid.

The next critical date this month comes on Friday, November 7th, so you’ll want to take action today to make sure you don’t miss out. Click here to find out more about this unique, easy way of collecting monthly dividends.

There is a saying: “The rich just keep getting richer”. And by all accounts, since the 2008 financial crisis, they have. Unfortunately, for the struggling poor and middle class, wealthy asset holders have been the only beneficiary of six years of Federal Reserve easy-money policies. Under the tutelage of Ben Bernanke, the Fed introduced QE in March of 2009 with the hope it would save the economy from economic collapse. The goal was to create a new vibrant market for borrowing to replace the former vibrant market for borrowing that had just blown up, taking the economy with it. I am sure Ben Bernanke began this ruse with good intentions and the misplaced belief that real economic prosperity could be manufactured from creating new money.

There is a saying: “The rich just keep getting richer”. And by all accounts, since the 2008 financial crisis, they have. Unfortunately, for the struggling poor and middle class, wealthy asset holders have been the only beneficiary of six years of Federal Reserve easy-money policies. Under the tutelage of Ben Bernanke, the Fed introduced QE in March of 2009 with the hope it would save the economy from economic collapse. The goal was to create a new vibrant market for borrowing to replace the former vibrant market for borrowing that had just blown up, taking the economy with it. I am sure Ben Bernanke began this ruse with good intentions and the misplaced belief that real economic prosperity could be manufactured from creating new money.

But as they say, hind sight is 20-20, and here we sit six years and 3.5 trillion dollars later with the realization this money printing scheme did not work as planned. Don’t just take my word for it. According to Wall Street Journal, Former Fed Chairman Alan Greenspan said the QE program had failed to achieve its primary goals. As a means of boosting consumer demand, the asset purchase program, he said, “has not worked,” though it did a good job of increasing asset prices.

Bond king Bill Gross agrees, noting that the roughly $7 trillion pumped into the financial system since the financial crisis by the world’s three biggest central banks has succeeded mostly in lifting asset prices rather than workers’ wages: “Prices go up, but not the right prices.”

And Hedge fund manager Paul Singer recently noted “The inflation that has infected asset prices is not to be ignored just because the middle-class spending bucket is not rising in price at the same rates as high-end real estate, stocks, bonds, art and other things that benefit from quantitative easing.”

Why QE Hasn’t Worked

The U.S. Government has done a splendid job of continuing its borrowing spree, as Federal debt has increased from $9.2 to $17.9 trillion. But if we learned any lessons from these last few years, it should be that government borrowing and spending in the form of transfer payments (such as food stamps) doesn’t grow an economy.

The Fed hoped that printing $3.5 trillion would encourage private companies to borrow money and grow their business by investing in property, plant and equipment. Unfortunately, growth doesn’t happen in a vacuum. With the consumer tapped out, business was more realistic about demand. The idea that low interest rates and available credit would spur growth similar to what we saw in the 1990’s with the technology boom did not manifest. Therefore, instead of borrowing at low rates to grow their businesses, many companies just took on cheap debt and bought back stock–growing their EPS but not the economy. This kept the “beat the expectation” crowd on Wall Street happy but did nothing to encourage sustainable growth.

Central banks have failed to realize that lasting economic growth only comes from real savings and investment, which leads to an increase in labor hours and productivity. The government’s borrowing and printing scheme left the banking system intact, but did nothing to help the average consumer. While the Fed was frantically printing money to re-inflate asset prices, the majority of American’s incomes have decreased, as real after tax income has actually fallen by -5.9%. In fact, in this recent election, we learned 65% of Americans are still primarily concerned with the economy, and nearly the same amount believe they are worse off since the great recession began. This is despite manipulated data from the Federal Government meant to persuade them otherwise.

With the prospect of viable economic growth pushed further out of reach and the Federal Reserve out of the QE game, deflationary forces should prevail and equity prices should be falling. But, if there is one thing Central Banks are famous for, it’s not learning from past mistakes. Fittingly, taking a page from the hyperinflationary playbook, Japan has gone on a kamikaze mission to destroy its currency; announcing an escalation of its bond purchase rate to $750 billion per year. In addition to this, Japan’s state pension fund (the GPIF), intends to dump massive amounts of Japanese government bonds (JCB’s) and double it allocation to equities, raising its investment in domestic and international stocks to 24% each. The BOJ is also planning on tripling its annual purchase of ETFs and other equity securities. Japan has taken the baton from Yellen and will run with it until the nation achieves runaway inflation and its currency is completely destroyed.

Central bankers across the globe have succeeded in hallowing out the middle classes, but have failed miserably in achieving viable growth. This game will continue until the inevitable currency collapse unfolds and investors lose faith in government-manipulated asset prices. The tsunami resulting from currency, sovereign debt and equity market destruction will soon begin rolling in Japan. The problem is that Japan isn’t some isolated banana republic — it is the world’s third largest economy. When its currency collapses it will wipeout worldwide markets and economies as well. And then, hopefully, investors will insist on putting their faith and wealth in money that can’t be destroyed by a handful of unelected and unaccountable government hacks.

I think the concept of inflation and deflation is frequently misunderstood because in some sectors of the economy you can have inflation and in some sectors deflation. But if the investment implication of Bill Gross is that – and he’s a friend of mine. I have high regard for him. If the implication is that one should be long US treasuries, to some extent I agree. The return on 10-year notes will be miserable, 2.35 percent for the next 10 years if you hold them to maturity in each of the next 10 years.

I think the concept of inflation and deflation is frequently misunderstood because in some sectors of the economy you can have inflation and in some sectors deflation. But if the investment implication of Bill Gross is that – and he’s a friend of mine. I have high regard for him. If the implication is that one should be long US treasuries, to some extent I agree. The return on 10-year notes will be miserable, 2.35 percent for the next 10 years if you hold them to maturity in each of the next 10 years.

However, if you compare that to French government bonds yielding today 1.21 percent, I think that’s quite a good deal, or Japanese bonds, a country that is engaged in a Ponzi scheme, bankrupt, they have government bond yields yielding 0.43 percent. So –

REGAN: You say Japan is engaged – go ahead.

MARC FABER: Well I think they’re engaged in a Ponzi scheme in the sense that all the government bonds that the Treasury issues are being bought by the Bank of Japan.

REGAN: So Japan’s engaged in a Ponzi scheme. What about the US? We’ve done our share of money printing. We’ve had record low interest rates for six years.

MARC FABER: I think the good news is – for Japan is that most countries are engaged in a Ponzi scheme and it will not end well. But as Carlo Ponzi proved, it can take a long time until the whole system collapses.

REGAN: So all this QE in your view is a form of a Ponzi scheme. It’s going to take some while before it catches up with us, and yet, Marc, you look at the jobs numbers coming out of the US. You look at the GD print (ph). All this has actually been pretty good lately. So isn’t there a case to be made for some economic growth here?

MARC FABER: I really have to laugh when I look at the economic statistics because they are published by the Obama administration, and there I would be very careful to take every figure for granted. The fact is simply that first-time home buyers in the US are now at the 30-year low. What does it tell you? That people don’t want to live in homes anymore? No. They can’t afford to live in homes anymore. That is the problem. And the whole exercise with quantitative easing has been to boost asset prices, but the bigger problem is the affordability. A lot of people are being squeezed very badly because the costs of living are rising more than their salaries and wages.

Marc Faber is an international investor known for his uncanny predictions of the stock market and futures markets around the world.Dr. Doom also trades currencies and commodity futures like Gold and Oil.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair