Bonds & Interest Rates

It’s a challenge to put a finger on what was the most significant event that took place in financial markets this past week. It might have been the price of crude oil further deteriorating to touch below 80 dollars a barrel for a brief instance on Wednesday, or the volatility index, the VIX coming within a hair of a 30 print. For certain, the most revealing of all markets was for US Treasury bonds as investors in a herd fashion reached for the safe haven and saw yields dip below the 2 handle and touch a low of 1.85 per cent. It is uncertainty that continues to be the theme that casts a shadow over economic growth prospects, but as commentators noted this week, investor complacency amongst the masses leading to excessive risk taking is what is fundamentally shifting these markets.

It’s a challenge to put a finger on what was the most significant event that took place in financial markets this past week. It might have been the price of crude oil further deteriorating to touch below 80 dollars a barrel for a brief instance on Wednesday, or the volatility index, the VIX coming within a hair of a 30 print. For certain, the most revealing of all markets was for US Treasury bonds as investors in a herd fashion reached for the safe haven and saw yields dip below the 2 handle and touch a low of 1.85 per cent. It is uncertainty that continues to be the theme that casts a shadow over economic growth prospects, but as commentators noted this week, investor complacency amongst the masses leading to excessive risk taking is what is fundamentally shifting these markets.

This correction we are witnessing in the equity markets almost seemed long overdue, and the supply glut in the global oil market was perhaps the catalyst that acted to push these markets over the edge. The S&P500 moving over 1000 trading sessions without seeing that down move of 10 per cent or greater has left behind a number of investors waiting to participate in the rebound of US equity markets, and as the buying that took place on Thursday and Friday of this week, and the speedy rebound (for the time being) highlighted how welcomed this correction was.

But perhaps there was another factor contributing to the turnaround we saw towards the end of the week, and it was

inspired by comments from St. Louis Fed President James Bullard. Bullard made the point that the FOMC should remain adaptive to when they choose to end their bond purchase program, and even hinted that an end to Quantitative Easing, expected to be announced at the end of this month, could only be temporary as they stand ready to support financial markets and continue to artificially boost asset prices. Bring on the speculation for QE4.

Former PIMCO CEO, Mohammed El-Erian comments that investors should be careful what they wish for. One of Ben Bernanke’s famous quotes when justifying the Fed’s accommodative policy was that the benefits were always outweighing the costs and risks. If the Fed was to embark on QE4, it would become incrementally harder for their policy committee to justify whether the benefits would outweigh the increasing costs and risks.

The US economy continues to experience record low interest rates. Falling oil prices will ultimately create yet another significant boost to an economy that is 70 per cent consumer driven and now sees gasoline prices 25 percent off their summer highs. And employment as a whole continues to see strong and stable growth above 220 thousand new positions a month. The takeaway though is not what’s driving the US economy via Fed policy. It’s how Fed policy is impacting financial markets, and that’s the reason for concern.

As has always been, the single biggest risk of the Fed’s accommodative policy is how investors have become dependent on their asset purchases in order to see risk assets trade higher. Thursday and Friday are further evidence of this. A sobering reminder comes with this, which is how overcrowded consensus trades have become, and really a question about how deep the liquidity or support in these markets really is when the majority of investors with the same mentality are all selling.

“the European Central Bank will soon unleash its own QE program; which will effectively pass on the baton to Mr. Draghi & Co.”

Passing on The Baton

BIG PICTURE – The first round of QE began in March 2009 and after 5½ years, the Federal Reserve’s bond buying program is coming to an end. Since the QE program boosted confidence, combated deflationary forces and sparked an epic bull market on Wall Street; it is hardly surprising that its end has brought about some turbulence in the stock market.

There can be no denying the fact that over the past few years, the QE program significantly assisted the stock market by tackling the deflationary forces within the economy. You will recall that when QE1 and QE2 were ending, the stock market abruptly reversed course and the major indices started to face intense selling pressure. Thereafter, when the Federal Reserve unleashed its next bout of bond purchases, buyers returned in earnest and piled into common stocks.

Today, the QE initiative has run its course and the big question is whether the US economy is strong enough to stand on its own feet; or if the withdrawal of the punch bowl will bring about deflation?

At this stage, nobody can guarantee how this will play out; however, we suspect that the US economy will continue to muddle through and avoid an outright recession. Although there may be some near-term weakness in business activity, the economy is likely to continue its expansion.

Turning to the stock market, we suspect that although a mean reversion to the 200-day moving average cannot be ruled out (Figure 1), Wall Street will not enter a prolonged bear-market for the following reasons:

(i) The Fed Funds Rate is at a historic low and the yield curve remains steep

(ii) For the foreseeable future, the Federal Reserve will maintain an accommodative monetary policy

(iii) Last but not least, the European Central Bank will soon unleash its own QE program; which will effectively pass on the baton to Mr. Draghi & Co.

Figure 1: S&P 500 Index – pullback is underway

Source: www.stockcharts.com

It is interesting to note that all year; the European Central Bank faced growing pressure from various governments, the

mainstream academics and the International Monetary Fund to embark on a large scale government bond buying program. And all year, the European Central Bank resisted, arguing repeatedly that quantitative easing would yield little benefit in the Eurozone’s structurally challenged economy. Furthermore, Mr. Draghi also warned of the political and moral hazard that would arise as a result of exposing the European Central Bank’s balance-sheet directly to sovereign credit risk.

Yet last month, Mr. Draghi threw those concerns aside, pushing through a decision by the bank’s governing council to cut interest rates and to embark on a program of large-scale bond purchases.

For now, although the European Central Bank will buy only asset-backed securities and covered bonds, the market may soon realise that a taboo has been broken. Put simply, Mr. Draghi’s objective of restoring the European Central Bank’s balance sheet to its size as of early 2012 will equate to a possible US$1.26 trillion expansion and show that the central bank has shifted its focus to money-creation.

When the European Central Bank unleashes its QE program, the stock markets of the developed world will resume their northbound journey and the single currency will accelerate its slide.

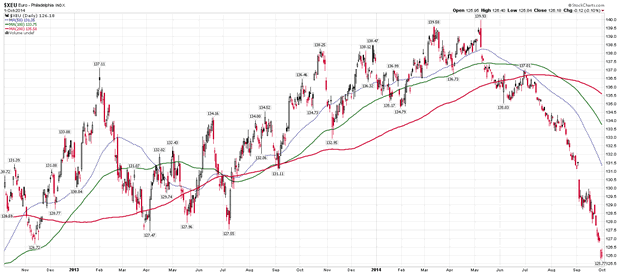

If you review Figure 2, you will observe that the Euro topped out in spring and since then, it has depreciated significantly against the US Dollar. In our opinion, when Mr. Draghi announces QE, the Euro will decline further and it may soon trade at a multi-year low.

Figure 2: Euro – more downside ahead?

Source: www.stockcharts.com

Similar to the US, we do not think that Mr. Draghi’s QE program will bring about an economic boom in the Eurozone. Nonetheless, we suspect that it will restore confidence, thwart deflationary forces and revive interest in the stock market.

If our assessment is correct, European Central Bank’s ‘stimulus’ will end the ongoing pullback in the stock market and it will set the stage for a multi-month rally. Furthermore, we suspect that bond purchases within the Eurozone will primarily benefit the stock markets of the developed world i.e. Europe, Japan and the US.

Remember, since April 2011, the stock markets of the developed world have outperformed the emerging nations by a wide margin and this trend will probably continue for the next 2-3 years. Accordingly, we have over-weighted our managed portfolios to Europe, Japan the US.

As far as sector analysis is concerned, airlines, asset managers, banks, biotechnology, broker dealers, defence, healthcare, insurance, semiconductors, railways and travel related stocks are showing strength. Conversely, agriculture, consumer staples, energy, materials, industrials and precious metals stocks remain weak and these should be avoided for now.

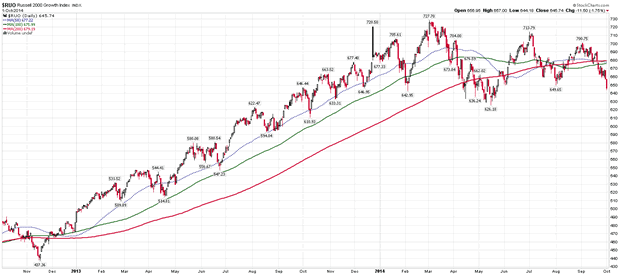

Although the widely followed major indices such as the Dow Jones and the S&P500 Index are holding up relatively well, some cracks have appeared in the market’s internals and these are worth monitoring. For instance, only 43% of the NYSE stocks are currently trading above the 200-day moving average. Furthermore, the small-cap counters as well as the growth stocks are struggling and the Russell 2000 Growth Index has now slipped below the key moving averages (Figure 3).

Figure 3: Russell 2000 Growth Index

Source: www.stockcharts.com

Elsewhere, the number of 52-week lows on the NYSE has now surpassed the number of 52-week highs on the NYSE and even the high yield bond ETF is trading beneath the 200-day moving average. Last but not least, the Volatility Index (VIX) is rising and this is another bearish omen for the market’s near-term outlook.

Over in the international markets, it is noteworthy that our preferred nations (India and Japan) are doing well and it appears as though additional gains are likely over the following months.

As far as India is concerned, much is expected from the new Prime Minister – Mr. Modi and if he delivers, the Bombay SENSEX will probably embark on an impressive rally. Consequently, we are maintaining our modest position in Indian equities.

Over in Japan, it appears as though the lengthy consolidation phase in its stock market is now complete and a new advance is underway. Currently, the Tokyo NIKKEI Average is taking a breather beneath last spring’s high but we suspect it should soon surpass that level. Make no mistake, the rally in Japanese stocks is primarily due to the weakening Yen and on that front, it is notable that after a lengthy consolidation, the currency has resumed its downtrend. Given our optimistic outlook, we have allocated some capital to Japanese stocks.

In summary, although the world’s stock markets are currently undergoing a pullback; we believe that this weakness will not morph into a prolonged bear market. After all, short-term interest rates are at historic lows, the majority of central banks remain accommodative and the European Central Bank is about to embark on its own QE initiative. Under these circumstances, we believe that the ongoing pullback will give way to a multi-month advance which will probably continue until spring. Accordingly, we are staying fully invested in our preferred investment themes.

COMMODITIES – The world’s reserve currency is strengthening; consequently, commodities (which are denominated in US Dollars) are automatically depreciating in value. Furthermore, the weak aggregate demand for commodities is not helping their cause either.

Due to these two factors, commodities remain trapped in a primary downtrend and it appears as though the weakness is likely to persist for the foreseeable future.

If you review Figure 4, you will observe that the Reuters-CRB Index (CCI) topped out in April 2011 and since then, the prices of natural resources have drifted lower. Furthermore, whereas in 2012 and 2013, the CCI Index found support around the 500 level (blue line on the chart), it has recently breached that key support level. By doing so, the CCI has reasserted its downtrend and opened up the possibility of a vicious decline.

Figure 4: Reuters-CRB Index (weekly chart)

Source: www.stockcharts.com

At this stage, nobody can guarantee how this will play out, but if the US Dollar appreciates sharply, commodities could experience a waterfall decline. Accordingly, we currently have no exposure to the physical commodities or the related stocks.

Although we do not possess a crystal ball, we believe that the primary downtrend in commodities will continue for at another 3-4 years. In fact, for the bear market to end, aggregate demand for ‘things’ will need to rise and that is not likely to happen in the near-term.

Remember, when it comes to commodities, China is the critical factor since the world’s most populous nation remains the largest consumer of natural resources. Unfortunately, China is currently dealing with its own problems, not least of which is the grossly overinflated property market.

Whether you like it or not, China’s real-estate sector is extremely overstretched and the value of its residential property stock now exceeds 400% of GDP! To put this in some perspective, it is worth noting that at the height of the Japanese real-estate boom in 1989-1990, its residential property stock also topped out at around 400% of GDP!

Apart from these two instances, never before in history has property become so expensive relative to the size of an economy; and we all know how the Japanese party ended. So, unless ‘this time is different’, you can be pretty sure that China’s property bubble will also pop and when it does, the shockwaves will be felt throughout the commodities universe.

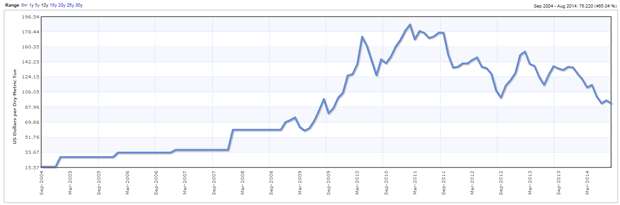

Even though China’s property boom is still intact, it is noteworthy that the prices of most base metals have declined significantly and the price of iron ore is currently trading at a 5-year low (Figure 5). In our view, these markets are discounting the looming troubles in China’s construction sector and when the inevitable bust arrives, things could get pretty ugly!

Figure 5: Iron Ore price – US$ per dry metric ton

Source: www.indexmundi.com

Elsewhere, the price of copper is also struggling and it is barely holding above the US$3 per pound level. If you review copper’s weekly chart, you will note that the metal has carved out a series of lower highs and this is typical bear market price action. From our perspective, the price of copper is extremely vulnerable and a decisive close beneath US$3 per pound may trigger a sharp decline.

In the agriculture complex, with the exception of coffee, prices are heading lower and this is a terrible time to be a farmer! Once again, the strengthening US Dollar is suppressing food prices, which is good for the consumer but unfavourable for the agricultural industry.

Last but not least, the price of energy is also coming under pressure and sellers are firmly in control of this market. Turning to specifics, it is notable that the price of crude has declined to a 52-week low and it is currently trading beneath the key moving averages. Elsewhere, the price of natural gas has also sliced through the key moving averages and the price of uranium is at a multi-year low.

Given the fact that the prices of various commodities remain in a primary downtrend, the related stocks are also struggling and this is not the time to be exposed to these securities.

Although the energy stocks performed well up until the summer months, the Oil Index (XOI) has broken down badly and it is now trading below the 200-day moving average. Moreover, the oil services and pipeline stocks have now also joined the downtrend, so our readers should consider liquidating their positions in this sector.

In summary, commodities are passing through a lean patch and the primary downtrend is likely to persist for several years. Therefore, we currently have no positions in the physical commodities or the related stocks.

In an article in the UK’s Telegraph on October 10, veteran economic correspondent Ambrose Evans-Pritchard laid bare the essential truth of the nearly universal current embrace of inflation as an economic panacea. While politicians, CEOs and economists talk about demand stimulus and the avoidance of a deflationary trap, Evans-Pritchard reminds us that inflation is all, and always, about debt management.

In an article in the UK’s Telegraph on October 10, veteran economic correspondent Ambrose Evans-Pritchard laid bare the essential truth of the nearly universal current embrace of inflation as an economic panacea. While politicians, CEOs and economists talk about demand stimulus and the avoidance of a deflationary trap, Evans-Pritchard reminds us that inflation is all, and always, about debt management.

Every year the levels of government debt as a percentage of GDP, for both emerging market and developed economies, continue to go higher and higher. As the ratios push out into uncharted territories, particularly in Europe’s southern tier, the ability to “inflate away” debt through monetization remains the only means available to postpone default. Evans-Pritchard quotes a Bank of America analyst as saying that even “low inflation” (not to mention actual deflation) is the “biggest threat to the dynamics of public debt.” IMF Managing Director Christine Lagarde ramped up the rhetoric further when she recently told the Washington Press Club that “deflation is the ogre that must be fought decisively.” In other words, governments need inflation to remain viable. It’s the drug they just can’t do without.

But as this simple truth is just too embarrassing to admit, politicians and central bankers (and their academic, journalistic, and financial apologists) have concocted a variety of tortured theories as to why inflation is not just good for overly indebted governments, but an essential economic good for all. In a propaganda victory that even Goebbels would envy, it is now widely accepted that purchasing power must decrease for an economy to grow.

Despite centuries of economic evidence to the contrary,they argue that if prices do not rise by at least 2% per year consumers will not spend, business will not hire, and economies will slip into an intractable deflationary death spiral. To prevent this, they recommend governments spend without raising taxes. Not only would such a move involve a direct stimulus by increased government spending, but the money printed by the central bank to finance the deficit will push up prices, which they argue is very healthy for the economy. As the Church Lady used to say, “How convenient.”

Offering voters something for nothing is the Holy Grail of politics. But as a matter of reality, voters should know that a free lunch always comes with a cost. This isn’t even economics, its physics.

When increased government spending is paid for with higher taxes, workers notice that their paychecks have been reduced. This provides clear evidence that government spending comes with a cost. But this bright line is much more difficult to see when the spending is paid for by inflation (printing money). But the net impact on consumers is the same.

Inflation does not reduce the nominal amount of one’s paycheck. But rising prices reduce the amount of goods and services it can buy. So when governments run deficits, workers will be stuck with the bill. Whether they pay though higher taxes or inflation, their standard of living will be diminished. The main difference is that workers know to blame government for higher taxes, which explains why politicians prefer inflation.

To give cover to this tendency, economists have come up with the bizarre concept that falling, or even stable, prices squelch demand and deter consumption. The idea is that if consumers know that something will cost less in the future (even if it’s just 2% less) they will defer their purchases indefinitely, perhaps waiting for the cost of their desired product or service to approach zero. They argue that this can push an economy into a deflationary spiral of falling prices and diminished demand which may be impossible to escape.

But this idea ignores the time value of a product or service (people will tend to pay more for something they can enjoy sooner rather than later) and the economic law that shows how demand goes up as the price falls. But common sense has absolutely nothing to do with the current practice of economics. Instead, the dominant argument is that inflation is needed to seed the economy with demand.

However, this argument is merely a smoke screen. The only thing that inflation can do is to help governments spend. Economies do just fine with low inflation. In fact during the late 19th century, in the Great Sag, the United States experienced sustained deflation while creating much faster economic growth than we have seen in the last few generations. As recently as during the early 1960s the U.S. experienced consistently low inflation (barely 2%) and strong economic growth based on government figures. But in their call for more inflation, modern economists tend to forget or downplay those periods.

But inflation is actually more economically harmful than taxation. By blurring the link between higher government spending and reduced purchasing power, the public is less likely to oppose government expansion. And therein lies the truth. Inflation is not needed to grow economies but to grow governments.

The problem is particularly acute in Europe where countries of radically different fiscal characteristics have been locked into a politically unworkable monetary union. On one side are countries like Italy, Spain, and France whose governments have been notorious for offering generous benefits for which they can’t pay. Before adopting the euro, these countries had currencies that were not known for their bankability. Germany, on the other hand, had built its reputation on balanced budgets and a strong Deutsche Mark. But given the strict monetary restrictions that were needed to grease the skids toward union, the European Central Bank has not been able to create inflation as freely as the U.S. or Japan. As a result, the debt crisis there has been placed in particularly sharp focus, as the problem is perceived to be much larger than in other developed countries that can print at will.

The calls for more inflation in Europe should be raising hackles on the streets of the Continent. But Keynesian economists have provided cover for politicians for years, and true to form, they have again risen to the occasion. While it is understandable that governments are motivated to champion inflation, it is harder to see why professional economists are similarly inspired. Perhaps they believe modern economics has the magic ability to create something from nothing. But the idea that a properly applied macroeconomic formula can somehow circumvent the laws of supply and demand is ludicrous and dangerous.

Of course, the idea that governments can hold inflation to just 2% per annum is preposterous. Once it breaches that level, governments will be powerless to contain it. The endgame will be hyperinflation. That is because escalating levels of debt will prevent them from raising interest rates high enough to break the inflationary spiral. The last time that inflation really got out of hand was back in the early 1980s when a boldly inspired Federal Reserve was able to put the genie back in the bottle by hiking interest rates all the way up to 18%. The economy not only survived that harsh medicine, but it prospered as a result. Does anyone seriously believe that we could survive even a quarter of that dosage today?

Since the central banks are now destined to forever remain behind the inflation curve, it will continue to accelerate until the real threat of hyperinflation looms much larger than did the contrived threat of deflation.

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on Youtube

Market Psychology began to go “risk off” the first week of September as capital retreated from the periphery to the center…but the Big Cap stock indices continued higher until September 19…the day of the Alibaba debut…and then the major American stock indices, the bond market and several lesser markets all registered a Key Turn Date (KTD.) Since September 19th “risk off” psychology has intensified across markets…we anticipate more to come. (Note: This blog was written Oct 11/12 but all charts below were created Oct 13 as posting was delayed by the Canadian Holiday.)

Stocks: The DJIA is down nearly 900 points (~5%) from its September 19th All Time High (ATH) and is negative YTD. The TSE has fallen nearly 1500 points (~9.5%) from its September 2nd ATH…the German DAX is down ~11% from Sept 19…while the Emerging Markets index is down ~12%.

We have been skeptical of the stock market for most of 2104…preferring to trade it from the short side…while respecting the huge upside momentum created by 5 years of global money printing (and corporate share buy backs!) We bought S+P puts on Sept 19 as the market broke from ATH but covered them (too early!) after 2 weeks on the expectation of another “buy the dip” rally…which never really came…unless you count last Wednesday when the DJIA soared nearly 350 points on the Fed minutes. We did not expect the stock market to “turn on a dime” at ATH…rather we expected “topping” price action…which would include price breaks and recovery rallies…but no new highs…to eventually “break the spirit” of bullish Market Psychology.

Volatility: We had ultra-low volatility across asset classes this summer…that has changed dramatically since the Sept 19 KTD with the VIX hitting 2 year highs last week…almost a double from the Sept 19 lows.

Credit markets: Top quality bond yields have dropped like a stone since the Sept 19 KTD with US 10 year Treasury yields near 2.25%…their lowest in over a year…while junk bond yields have risen to their HIGHEST in over a year as credit spreads have widen dramatically. Euro Area Sovereign bond yields have dropped to new All Time Record lows…German 5 year bunds are now on par with Japanese 5 year bonds.

The falling stock markets are the lead story on the nightly news…but the changes in the credit markets may be much more important as weaker borrowers suddenly find it harder to raise money after years of feasting on capital provided by “yield hungry” investors.

Currencies: We’ve been relentlessly bullish the US Dollar for months…but we thought it was overdone in late September (up 12 weeks in a row) and we stood aside the currency markets looking for a correction to re-establish long US Dollar positions. We do NOT want to be short the US Dollar. The Dollar Index closed lower last week for the first time since early July.

The Russian Rouble closed last week at All Time Lows…down ~20% since June (a huge move in FX)…tracking almost perfectly with the 20% tumble in crude oil.

Crude Oil: WTI has fallen ~20% from its June highs…registering its lowest weekly close in 2 years. WTI is down ~11% in just the last 2 weeks! Western Canada Select (the Canadian Benchmark) traded just above $70 last week as global energy markets struggle with rising supply and falling demand. Crude looks extremely over-sold short term…skyrocketing volatility has us considering short puts.

Commodity Indices: The CRB commodity index is down ~30% from its 2011 ATH…now at 4 year lows. Slow global growth, disinflationary pressures and a strong US Dollar have been “bad news” for commodity prices after a decade long surge…when Market Psychology assumed that China would buy everything that wasn’t nailed down…

It’s a deflationary world: The Fed is concerned that slow global growth and a strong dollar will make it harder for them to reach their goal of 2% domestic inflation. (US Import prices have fallen in each of the last 3 months.) The Fed is expected to end their current “Q” program…and had been expected to start raising interest rates early next year…especially given the improvement in their “employment” mandate…but…if inflation stays stubbornly low…because it’s a deflationary world outside the USA…the Fed may drag their feet on raising interest rates. (Treasury Secretary Lew has also spoken out against countries using currency devaluation for competitive advantage…however…we maintain our macro view that capital will “come to America” seeking safety and opportunity.)

Short term trading: Markets were not prepared for the Fed’s concern about slow global growth and a strong Dollar. The DJIA rallied ~350 points and the US Dollar tumbled as Market Psychology suddenly shifted to thinking (hoping) that the Fed might delay raising interest rates…BUT…the fact that there was absolutely no follow-through to Wednesday’s stock market rally highlights the intensity of the prevailing “risk off” tone. We look for lower prices ahead.

We had a good run with our bullish US Dollar positions then stood aside…waiting for a correction to re-establish long positions. We are still waiting. We bought S+P puts on September 19…but in hindsight we exited that position WAY too early! We are currently flat in our short term trading accounts…looking for opportunities…and VERY aware that trading is not a “game of perfect”!

Leon Cooperman Cooperman said the risk in financial markets rests “unequivocally” with bond investors right now.

Cooperman said US government bonds usually move in connection with nominal GDP, which is a combination of real GDP and inflation.

Cooperman said that if we get real GDP of about 2% to 3% and inflation of about 2% to 3%, then nominal GDP comes to about 4% to 6%.

To Cooperman, this means it wouldn’t be unreasonable to expect that US 10-year Treasuries could rise to 4%, 5%, or 6%, and Cooperman said that if this happens, bond investors would see capital losses.

On Thursday morning, the yield on the US 10-year Treasury bond fell to 2.27%.

Leon Cooperman also spoke on Apple, as he was on live on CNBC as Carl Icahn’s open letter to Apple CEO Tim Cook crossed the wires, with Cooperman saying that Apple shares were currently 20% undervalued.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair