Bonds & Interest Rates

Last month, an Advanced Micro Devices (NYSE: AMD) bond delivered investors 66% more annually than they were expecting in just 14 months.

The same performance can’t be said of its stock. It’s had a rough ride since the advent of tablets and what most believed was the death of the PC market.

From its glory days in the early 2000s, Advanced Micro Devices has dropped from more than $40 to about $4.40 a share.

So how does a company dealing with such horrible market conditions pay its bondholders 66% more than it has to?

It’s called a tender offer.

Unconventional Advice

A tender offer is when a company offers to buy back a bond before maturity. It does this to reduce its interest costs. It is no different than refinancing your mortgage to reduce your costs.

Most brokers will tell you tenders are bad deals because you can make a higher total return by collecting all the interest payments to maturity than what can be made on a tender offer.

In some cases, the brokers are correct… but not usually. In my 30 years of experience, I have taken almost all tender offers. Call me crazy, but if my annual return is 66% higher than what I expected to earn, I take the money and run.

Here’s how the numbers worked out for this cash giveaway.

A 66% Increase in Expected Return

In January 2013, I alerted my Oxford Bond Advantagesubscribers to purchase an Advanced Micro Devices bond at about 93.5, or $935 per bond. The coupon, or the amount the bond holder is paid annually in interest, was 8.125%, or $81.25 per bond per year.

If they held this bond to maturity, they would have received 10 interest payments of $40.62 every June and December until maturity on December 15, 2017, for a total of $406.20.

Since bonds have to pay $1,000 at maturity, and my subscribers only paid 93.5, $935 per bond, they would pocket another $65 per bond as a capital gain.

The annual return to maturity would have been about 10.2%.

(Here’s the math: 10 payments x $40.62 interest + $65 capital gain / $935 cost / 59 months to maturity x 12 months = 10.2% annually.)

But, and this is where its gets good, Advanced Micro Devices just made a tender offer to buy back the bond at 104.58, or $1,045.80.

My subscribers paid $935, and the tender offer will pay them $1,048 per bond now, instead of $1,000 at maturity in three years. Plus, subscribers will also get $115 in earned interest for buying the bond back in January 2013.

(Here’s the calculation for the tender offer: $115 interest + $110.80 capital gain / $935 cost / 17-month holding period x 12 months = 17.05%.)

All told, the annual return on this bond is now 17.05% compared to 10.2% a year.

There is no question here for me. Take the money and run.

A Positive Signal

You may be asking why anyone would buy a bond in a company that has had as many problems in the past few years as Advanced Micro Devices. You’d be right to do so. It does not look like something a conservative income investor would hold.

But remember this… When a bond owner is looking at a potential investment, he or she is only concerned with whether the company will be able to pay its bills until the bond matures.

That’s it. We don’t need the company to grow or even do well. We just need it to keep its head above water and meet its minimum obligations.

Advanced Micro Devices did that and a lot more. That’s why the bond shot up in price.

And even though many brokers will disagree with me, calls, tenders and sales before maturity can make bonds one of the biggest and most consistent payers.

A Note From the Editorial Director: Steve’s bond commentary is an integral part of each monthly issue ofThe Oxford Income Letter, where he updates readers on the latest opportunities in the bond market. Right now, subscribers are buzzing about a brand-new – and entirely unique – opportunity. It’s something we call the Presidents’ Private Stock Market… and it could send your income 2,114% higher than the average investor. To get all the details, click here.

End result is shocking, 4 times more Debt when it is added properly .

Apparently the Debt is 70 Trillion, significantly higher than the 16 trillion the US Government says it is in debt according to new figures. Jim Rogers comments in the first 2:30 of the following video – Money Talks Editor

Venture Capital, Katie Pilbeam talks about the worrying new estimations on US debt figures with Jim Rogers, a legendary investor author of Street Smarts: Adventures on the Road and in the Markets.

The artist formerly known as Prince once sang that he was gonna party like it’s 1999. After all, when it’s “two thousand zero zero, party over, oops out of time!”

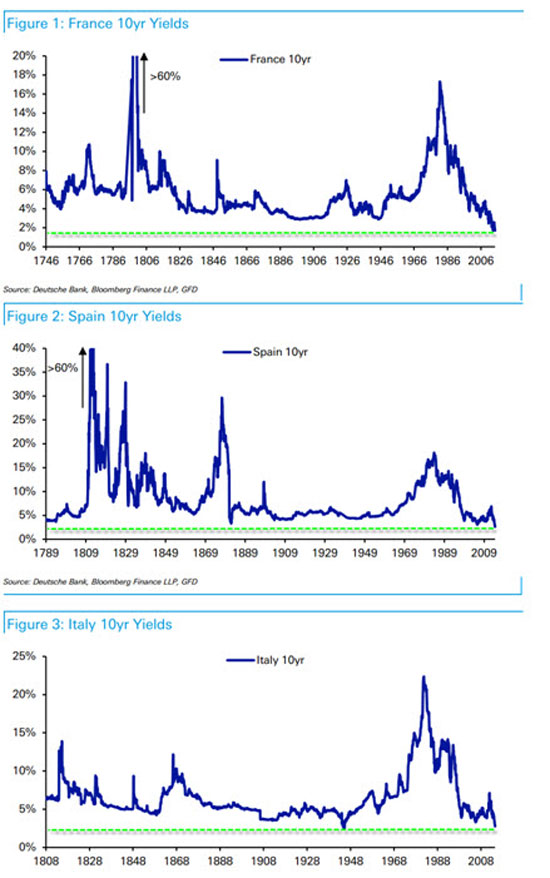

But today’s bond holders are much more ambitious. They’re partying like it’s 1746! As in, more than two and a half centuries ago.

I say that because in the wake of the European Central Bank’s latest policy gambit, yields on the benchmark French 10-year government bond just fell to 1.65 percent. That is the lowest level since 1746, according to new research from Deutsche Bank.

In Italy, 10-year government bond yields just sank to 2.76 percent — the lowest level since early 1945. Except for that one brief period, yields are the lowest since at least 1808.

And Spain? The country that almost went broke a couple years ago … that still faces record-high unemployment and incredibly anemic growth … and that is still mired in a housing slump that mirrored the one we suffered here?

Well, naturally amid all that risk … its benchmark 10-year yield just sank to 2.6 percent. Not only is thatbelow the benchmark sovereign yield on U.S. Treasuries, it’s also the lowest since at least 1789. You know 1789 don’t you? That was when George Washington became the first president of the U.S., and when the French Revolution began.

Look, I’ve seen a lot of market swings and a lot of strange things in my 17 years of following the capital markets closely. My mentor, Dr. Martin D. Weiss, has seen even more over the decades he’s been tracking interest rates and government bonds.

James (Jim) Grant, founder and publisher of Grant’s Interest Rate Observer newsletter, sat down with Forbes Magazine and talked about Central Bank moves, history as well as some individual opportunities – Editor Money Talks

Listen to the video or read the transcript HERE

For all those analysts (including this one) who thought the debt binge of the previous decade marked end of the Age of Leverage, well, not so fast. It turns out that memories are short and government printing presses are powerful, and this combination has turned the “Great Deleveraging” into a minor speed bump on the road to something even more extreme. As the following chart illustrates, the growth in total US debt flattened in 2009 and 2010, with government borrowing more-or-less offsetting a decrease in consumer and business loans. But now the trend is once again onward and upward across the board.

Prudent Bear’s Doug Noland publishes a quarterly analysis of the Fed’s Z.1 report of US credit market activity. This is always a must-read, but last Friday’s was truly extraordinary. Among other big, ominous trends, Noland notes the following:

• Total (financial and non-financial) Credit jumped $484bn during Q1 to a record $59.399 TN, or 347% of GDP.

• Total Non-Financial Debt (NFD) expanded at a 5.0% rate.

• Corporate borrowings grew at a robust 9.3% pace

• Federal government debt mounted at a 7.1% rate

• Consumer credit rose at a 6.6% rate

• Household net worth surged $7.98 TN, or 10.8%, over the past year.

• Over the past four years, household holdings of financial assets have surged $22.0 TN, or 49%, to a record $67.2 TN.

What’s happening? The short answer is that zero interest rates have finally begun to work their magic. Corporations, for instance, are using the proceeds from low-rate bonds to buy back stock on a vast scale. See Zero Hedge’s Here’s the mystery and completely indiscriminate buyer of stocks in the First Quarter.

And now cheap credit is leading consumers to start buying cars and using plastic. Here’s an excerpt from a Financial Sense article asking how US consumer spending could be rising while incomes are not:

“One of the questions discussed was “how is this increased spending financed?”. It’s a fair question, given the painfully slow wage growth in the US.

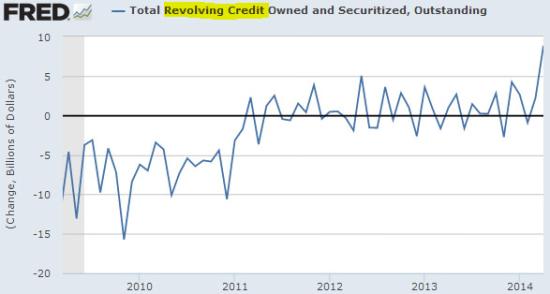

On Friday we got our answer. US consumer credit outstanding spiked way above expectations. While the media focused on the jobs report, this was the key news item:

Source: Investing.com

Unlike in previous Fed reports that showed consumer credit growth driven by student loans and to a lesser extent auto finance, we saw something new this time around. The increase was caused by a jump in revolving credit. Americans are warming up to using plastic again.

Source: Investing.com

This is certainly a positive signal because it shows that household confidence is improving sufficiently to send consumers shopping. Unfortunately a great deal of what Americans bought came from abroad, causing the US trade deficit to jump unexpectedly. The effect on GDP growth from this jump in consumer spending will therefore be relatively muted.

Some thoughts

It was just six years ago that soaring consumer spending, massive trade deficits and generally excessive debt caused the biggest crisis since the Great Depression, and here we are back at it. The details are slightly different but the net effect is the same: inflated asset prices, growing instability and rising risk of a systemic failure capable of pulling down pretty much the whole show.

All of which creates a fascinating economic landscape in which families are making no more money than they did last year but are borrowing to buy things they don’t need, while corporations sell bonds to pump up their stock prices and by implication their executives’ year-end bonuses. It is, in short, another debt-fueled orgy in which the most vulnerable individuals are being suckered by governments and corporations into mortgaging their futures in order to transfer wealth to the “smart money.” Recall the Z.1 Report finding that household holdings of financial assets have surged by $22 trillion in just four years.

This is sad in one sense because the people being hurt are, as always, not the architects of this latest bubble. But it’s also exasperating because the same thing happened JUST SIX YEARS AGO and should still be fresh in the memories of the adults doing the borrowing and spending. Unless all those food additives and pesticides are impairing the average person’s cognitive functioning (which is a subject for another day) the people using credit cards to buy Chinese-made junk really have no excuse.

For now, the bubble is the story, and the fact that it’s hitting its stride with stocks and bonds already at record levels is a new twist. Just about the only thing that can be said with near-certainty is that the next few years will be more volatile than the last few.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair