Currency

USDCAD Overnight Range 1.2307-1.2377

The Greek PM cries referendum, the Eurozone Finance ministers cry no extension and Greek citizens just cry. News that the Greek government implemented capital controls and shuttered banks until July 7th spooked FX markets in early Asian trading. A bout of risk aversion in a thin market saw EURUSD plunge to 1.0955 from Friday’s close at 1.1170. USDJPY also gapped lower, dropping to 122.20 from 123.80. EURUSD recovered almost all of its losses in Europe while USDJPY has not.

Lost in the tossed salad that was Greek, was news of a 0.25 bp rate cut in China. The one year benchmark deposit rate is now 2.00% while the lending rate fell to 4.85%.

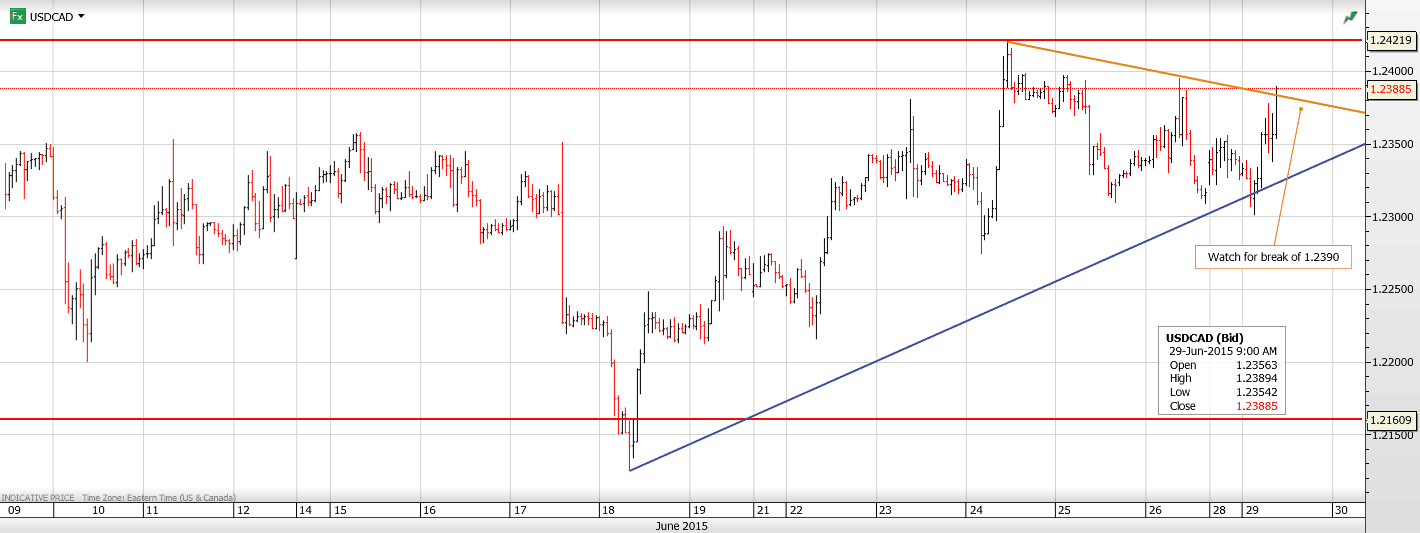

USDCAD has been trading water since the start of trading in New York. An initial foray towards resistance in the 1.2390-05 area failed in part due to an improvement in domestic data. The May Industrial Product Price Index came in at 0.5%, as expected but way better than the previous month’s decline of 0.9%. The Raw Materials Price Index rose 4.4% vs.4.0% the previous month. It also helped that the US dollar strength seen overnight, abated somewhat.

Looking ahead until tomorrow, Greece issues and the risk of default plus the expiry of the Iran nuclear talks will keep fingers on the trigger for risk aversion trades while month end portfolio flows will make for choppy FX markets.

USDCAD technical outlook

The intraday USDCAD technicals are bullish while trading above 1.2310 and attempting to test resistance at 1.2395-1.2405 which represents the downtrend line from the June peak. A move above here will set up a test of the 1.2450-60 March peak, downtrend line. For today, USD support is at 1.2340, 1.2305 and 1.2280. Resistance is at 1.2390, 1.2420 and 1.2450.

Today’s Range 1.2320-1.2405

Chart: USDCAD daily with moving averages Larger Chart

The Chinese central bank is backing its Yuan with GOLD. This may set the Yuan as a “New Reserve Currency.”

The Chinese central bank is backing its Yuan with GOLD. This may set the Yuan as a “New Reserve Currency.”

If this happens, a new order in global currencies will appear. This would attract new foreign capital. The rest of the world will view the Yuan as a real currency rather than a fiat currency. Creating the Yuan with a gold standard will surely make China more powerful and become a more influential world power.

The United States Dollar will no longer be the only “Reserve Currency” in the World anymore.

China will most likely become the world’s largest economy catapulting over the United States. They already have close ties to the world’s largest energy nation (Russia), and consumer based BRICS (acronym for the combined economies of Brazil, Russia, India, China, and South America). It is only a matter of time before a large portion of the world systematically rejects the Dollar.

The world will seek stability in a much different type of financial construct. The BRICS nations have already started making alternatives to the World Bank, IMF, and the SWIFT system. We will be facing a hard choice: Either remain steadfast to the old regime or shift to the “New Paradigm.” In shifting to the “New Paradigm”, we will set up the Yuan as the next global reserve currency.

Russia and China are in the works to create a new alternative to the long-standing SWIFT system. SWIFT stands for the Society for Worldwide Interbank Financial Telecommunications. It is a messaging network. Financial institutions use it to securely transmit information and instructions with a standardized system of codes.

An alternative to SWIFT could end the US Dollar as the sole reserve currency in the global financial system. The Russians would then turn away from the SWIFT system and have a new alternative. They would thus avoid any serious economic sanctions now or in the future.

Russia is expected to join forces with China and create their own “Union Pay”. The People’s Bank of China started “Union Pay” in 2002. It is now the second-largest payment networking system behind Visa. Union Pay is now preparing for a full-scale collaboration with Russia.

It has developed the foundation needed to be very successful in this venture. This would replace the SWIFT system. Then Russia and China could avoid any interference by a Western superpower imposing economic sanctions on them. To this end, they have decided to end the Dollar as the global reserve currency.

They are now creating another choice everyone can pick and use as they like. I would call this a “Game Changer”. There will be two reserve currencies as Petro-Yuan joins Petro-Dollar.

Chris Vermeulen

Also:

If You Have Money in a US Bank Account Be Aware!

Trade Signals: Gold, Silver, and Miners – Resource Stock Alerts

USDCAD Overnight Range 1.2327-1.2395

FX volumes are down across the board in Europe as the weekend looms and another EU/Greece meeting is on the agenda. The US dollar has had a pretty good week. As of 7:00 am it has gained against the entire G-10 spectrum. The RBNZ contributed to the US dollar’s rise, claiming that NZD is at “unjustifiable and unsustainable levels”, which some interpret as “Bank-speak” for “FX intervention ahead”.

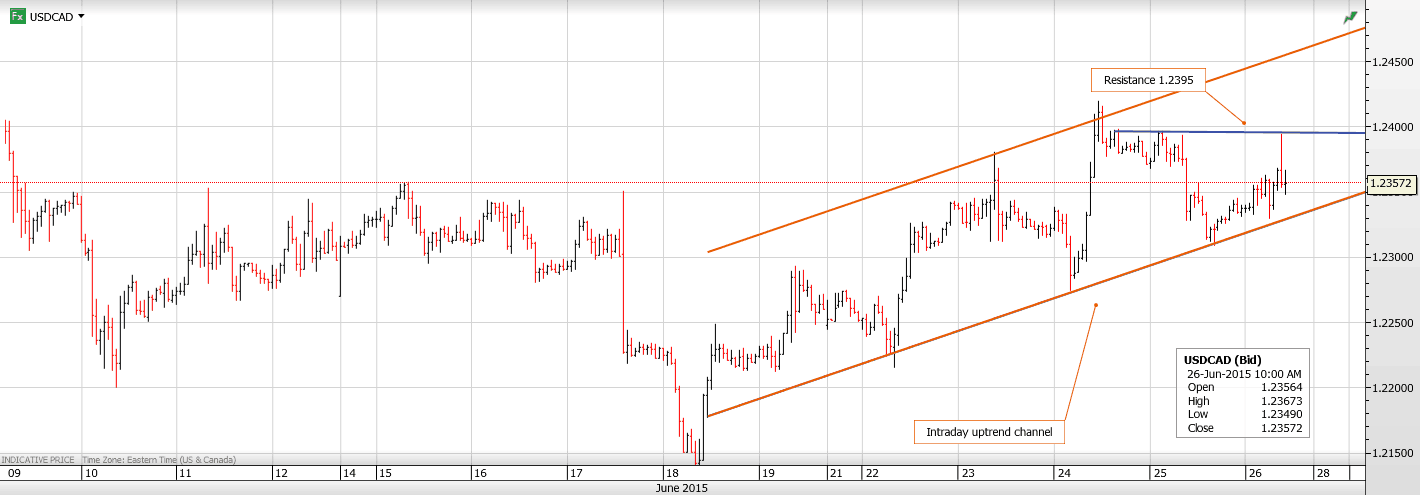

USDCAD started the day in New York with a modestly bid tone and managed to grind all the way to 1.2395 from 1.2355 before reversing and drifting back to its opening levels. Friday’s movement is merely a reflection of a “quote and cover” market rather than one with any direction.

It will be an eventful and volatile week coming up, with the bulk of the USDCAD action occurring on Tuesday. That is the day that Greece needs to pay the IMF. It is also the day Canadian GDP gets released and it is month end, quarter end and half-year end for portfolio managers.

USDCAD technical outlook

The intraday USDCAD technicals are bullish and in a modest uptrend channel since June 18. The bottom of the channel is currently 1.2325 and the top is at 1.2450. However there is “multi-top “resistance at 1.2390-00 which has capped short term rallies. A break above this resistance will extend gains to 1.2420 and then 1.2450. A break below 1.2325 may lead to a test of 1.2260. Meanwhile the 2 week range of 1.2155-1.2420 remains intact. For today, USD support is at 1.2325, 1.2305 and 1.2280. Resistance is at 1.2395 and 1.2420.

Today’s Range 1.2325-1.2395

Chart: USDCAD hourly with uptrend channel

Quotable

“In response to a question posed at a forum by The International Economy magazine in its Spring 2015 issue: Will America Soon Have an Inflation Problem?

“Not a chance. Fed policy since 2008 has been to tilt against powerful deflationary forces that have yet to abate. How powerful are those forces? Consider this: from September 2008 to date, the monetary base has increased by 336%, from $0.94 trillion to $4.1 trillion, yet the annual CPI growth declined from 5% in September 2008 to a negative -0.1% in February 2015. So, we are talking about quite powerful underlying deflationary forces that will not go away.

–Criton Zoakos

Commentary and Analysis

Thinking Swissie! By far the most overvalued currency on a cycle low to high scale

Swiss Bank Chairman Thomas Jordan said today the Swiss franc is “considerably overvalued” and was concerned there may be a rush of funds into the franc if Greece were to leave the single currency regime. I believe Mr. Jordan is correct on both counts. If you measure relative Swiss valuation to the other major pairs in terms of what I define as cycle low to high, you get a better sense of the love investors have had for Swissie during the last dollar bear market cycle.

First the definition of cycle low to high: It is that period measure from early 2000 to early 2008 which represented the eight year dollar bear market (which was a roughly eight year bull market in the Swiss franc and other major pairs).

I have summarized the major pairs’ cycle low-high prices and dates in the table below. Prices are in dollar terms for consistency.

Using Swissie (CHFUSD) for example, the chart shows the cycle low in Swiss-USD was on 10/25/2000 at a price of 0.5489; the cycle high was made on 8/9/2001 at 1.3827; and the last trade was 1.0671 today.

1. From cycle low to cycle high (during the Swiss bull market, i.e. dollar bear market) Swissie appreciated a whopping 151.9%; a far greater than any other major currency. The Australian dollar was in second place with an appreciation of 131.8% during its low-high cycle.

2. Despite such whopping gains; Swissie has depreciated the least from its cycle high based on today’s prices, down 22.8%.

3. And the point to this analysis (if we can call it that) is Swissie is still perched a whopping 94.4% above its cycle low even though we are into year five of the US dollar bull market. Again, the next most overvalued currency on this cycle low/high scale is the Aussie; it is still 61.6% above its cycle high.

Granted, there is no guarantee the dollar bull market continues. And if it does, there is no guarantee the US dollar will reach its last cycle high at 121.02 in early July 2001 (meaning the major pairs may not reach their cycle lows).

But, it is interesting to think about. Why did Swiss appreciate so much and why is it still holding up so well? I would suspect the answer on both counts is a currency name the euro.

Using this simple measure of relative appreciation/depreciation of the major pairs against the US dollar, it helps justify Mr. Jordan’s concerns and helps explain why Swiss rates are in negative territory and likely to remain there for a while. Swiss has institutional value beyond hot money flows based on yield differentials alone. [Though there was reputational damaged given the poor handling of the de-pegging from the euro. And of course the Orwellian-named US Justice Department snoopers can now see peek into Swiss accounts.]

The question is what needs to happen for Swiss to start trading more in line with the other pairs i.e. for some of that relative overvaluation to be shaken out of the franc? The answer again likely points back to the euro. If we get through this Greek crisis period, and there is some market normalization, maybe Swiss negative yields will start to play a bigger role. And if the Fed does start a campaign of rate hikes in September, the Swiss franc could be the horse to ride for a change.

Free Three-Week Trial to Black Swan Capital currency services: Click Here

Jack Crooks

President, Black Swan Capital

Quotable

“And what would you do, … if you could rule the world for a day? I suppose I would have no choice but to abolish reality.”

― Robert Musil, The Man Without Qualities Vol. 1

Commentary & Analysis

Vulnerable Aussie – Chinese stocks and the Reserve Bank of Australia

The Australian dollar has fallen a long way from its high against the US dollar. And from a technical perspective may have done enough; at least it may be poised to “correct” higher in the near- to medium-term. But an examination of the fundamental factors suggests there could be more room to fall—maybe a lot more room.

Two considerations come to mind:

1. The Chinese connection. Over the last few years, when speaking at conferences and peening these missives to Currency Currents readers, I have suggested Australia has become a satellite country of China. A bit of hyperbole? Yes indeed. But used in an effort to make the point Australia’s economy is closely linked with China’s; especially in regards to China’s demand for raw materials.

China’s economy is slowing, most of us know that. But most of us likely don’t give much thought to just how far and how fast economic growth in China has fallen.

From the Financial Times 6/23/15:

20 per cent to less than 6 per cent in the first quarter, which is a much more dramatic slowdown that many people realise,” said Chen Long, China economist at Gavekal Dragonomics in Beijing.

• Revenue growth for companies listed in mainland China, which excludes volatile energy and financial stocks, closely matches the trend in nominal growth rate

From the Financial Times 6/23/15:

- “A lot of the arguments over whether China’s official growth rate of 7 per cent is real or not actually miss the point that the nominal GDP growth rate has fallen from more than 20 per cent to less than 6 per cent in the first quarter, which is a much more dramatic slowdown that many people realise,” said Chen Long, China economist at Gavekal Dragonomics in Beijing.

- Revenue growth for companies listed in mainland China, which excludes volatile energy and financial stocks, closely matches the trend in nominal growth rates over the last decade.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair