Currency

As the saying goes, you can know a person by the quality of his or her enemies. This is also true of societies, where moral evolution can be traced by simply listing the things on which they declare war. Not so long ago, for instance, the world’s good guys — the US, Europe’s democracies and a few others — fought existential battles against fascism and communism. Then they went after poverty and discrimination. They were, at least in terms of their ideals, on the side of personal freedom and opportunity and against institutionalized control.

As the saying goes, you can know a person by the quality of his or her enemies. This is also true of societies, where moral evolution can be traced by simply listing the things on which they declare war. Not so long ago, for instance, the world’s good guys — the US, Europe’s democracies and a few others — fought existential battles against fascism and communism. Then they went after poverty and discrimination. They were, at least in terms of their ideals, on the side of personal freedom and opportunity and against institutionalized control.

But then came the war on drugs, in which the US imprisoned millions of non-violent people guilty only of voluntary transaction. Not long after that we declared war on “terror,” using the enemies created by our own incompetent foreign policy as an excuse for a vast expansion of surveillance and police militarization.

And now, seemingly out of nowhere, comes a new enemy: cash. Around the world, governments and banks are making it harder to save and transact with paper and coin. The ultimate goal seems to be the elimination of private tools of commerce, in favor of transparent (to governments and banks) plastic, checks and online payment systems. The following excerpts are from longer articles that should be read in their entirety:

The Death of Cash

(Bloomberg) – Could negative interest rates create an existential crisis for money itself?

JPMorgan Chase recently sent a letter to some of its large depositors telling them it didn’t want their stinking money anymore. Well, not in those words. The bank coined a euphemism: Beginning on May 1, it said, it will charge certain customers a “balance sheet utilization fee” of 1 percent a year on deposits in excess of the money they need for their operations. That amounts to a negative interest rate on deposits. The targeted customers—mostly other financial institutions—are already snatching their money out of the bank. Which is exactly what Chief Executive Officer Jamie Dimon wants. The goal is to shed $100 billion in deposits, and he’s about 20 percent of the way there so far.

Pause for a second and marvel at how strange this is. Banks have always paid interest to depositors. We’ve entered a new era of surplus in which banks—some, anyway—are deigning to accept money only if customers are willing to pay for the privilege. Nick Bunker, a policy analyst at the Washington Center for Equitable Growth, was so dazzled by interest rates’ falling into negative territory that he headlined his analysis after a Doors song, Break on Through (to the Other Side).

Now comes the interesting part. There are signs of an innovation war over negative interest rates. There’s a surge of creativity around ways to drive interest rates deeper into negative territory, possibly by abolishing cash or making it depreciable. And there’s a countersurge around how to prevent rates from going more deeply negative, by making cash even more central and useful than it is now. As this new world takes shape, cash becomes pivotal.

The idea of abolishing or even constraining physical bank notes is anathema to a lot of people. If there’s one thing that militias and Tea Partiers hate more than “fiat money” that’s not backed by gold, it’s fiat money that exists only in electronic form, where it can be easily tracked and controlled by the government. “The anonymity of paper money is liberating,” says Stephen Cecchetti, a professor at Brandeis International Business School and former economic adviser to the Bank for International Settlements in Basel, Switzerland. “The bottom line is, you have to decide how you want to run your society.”

As long as paper money is available as an alternative for customers who want to withdraw their deposits, there’s a limit to how low central banks can push rates. At some point it becomes cost-effective to rent a warehouse for your billions in cash and hire armed guards to protect it. We may be seeing glimmerings of that in Switzerland, which has a 1,000 Swiss franc note ($1,040) that’s useful for large transactions. The number of the big bills in circulation usually peaks at yearend and then shrinks about 6 percent in the first two months of the new year, but this year, with negative rates a reality, the number instead rose 1 percent through February, according to data released on April 21.

Bank notes, as an alternate storehouse of value, are a constraint on central banks’ power. “We view this constraint as undesirable,” Citigroup Global Chief Economist Willem Buiter and a colleague, economist Ebrahim Rahbari, wrote in an April 8 research piece. They laid out three ways that central banks could foil cash hoarders: One, abolish paper money. Two, tax paper money. Three, sever the link between paper money and central bank reserves.

Abolishing paper money and forcing people to use electronic accounts could free central banks to lower interest rates as much as they feel necessary while crimping the underground economy, Buiter and Rahbari write: “In our view, the net benefit to society from giving up the anonymity of currency holdings is likely to be positive (including for tax compliance).” Taxing cash, an idea that goes back to German economist Silvio Gesell in 1916, is probably unworkable, the economists conclude: You’d have to stamp bills to show tax had been paid on them. The third idea involves declaring that all wages and prices are set in terms of the official reserve currency—and that paper money is a depreciating asset, almost like a weak foreign currency. That approach, the Citi economists write, “is both practical and likely to be effective.” Last year, Harvard University economist Kenneth Rogoff wrote a paper favoring exploration of “a more proactive strategy for phasing out the use of paper currency.”

Pushing back against the cash-abolition camp is a group of people who want to make cash more convenient, even for large transactions. Cecchetti and co-author Kermit Schoenholtz, of New York University’s Stern School of Business, suggest a “cash reserve account” that would keep people from having to pay for things by sending cash in armored trucks. During the day, funds in the account would be payable just like money in a checking account. But every night they’d be swept into cash held in a vault, sparing the money from the negative interest rate that would apply to money in an ordinary checking account. In a way, physical cash would take on a role similar to that played by gold in an earlier era of banking.

The “War on Cash” Migrates to Switzerland

(Acting Man’s Pater Tenebrarum) – The war on cash is proliferating globally. It appears that the private members of the world’s banking cartels are increasingly joining the fun, even if it means trampling on the rights of their customers.

We just come across a small article in the local European press (courtesy of Dan Popescu), in which a Swiss pension fund manager discusses his plight with the SNB’s bizarre negative interest rate policy. In Switzerland this policy has long ago led to negative deposit rates at the commercial banks as well. The difference to other jurisdictions is however that negative interest rates have become so pronounced, that it is by now worth it to simply withdraw one’s cash and put it into an insured vault.

Having realized this, said pension fund manager, after calculating that he would save at least 25,000 CHF per year on every CHF 10 m. deposit by putting the cash into a vault, told his bank that he was about to make a rather big withdrawal very soon. After all, as a pension fund manager he has a fiduciary duty to his clients, and if he can save money based on a technicality, he has to do it.

A Legally Murky Situation – but Collectivism Wins Out

What happened next is truly stunning. Surely everybody is aware that Switzerland regularly makes it to the top three on the list of countries with the highest degree of economic freedom. At the same time, it has a central bank whose board members are wedded to Keynesian nostrums similar to those of other central banks. This is no wonder, as nowadays, economists are trained in an academic environment that is dripping with the most vicious statism imaginable. As a result, withdrawing one’s cash is evidently regarded as “interference with the SNB’s monetary policy goals”.One large Swiss bank recently responded to a pension fund’s withdrawal request with a letter stating: “We are sorry, that within the time period specified, no solution corresponding to your expectations could be found.”

Although we all know that fractionally reserved banks literally don’t have the money their customers hold in demand deposits, the contract states clearly that customers may withdraw their funds at any time on demand. The maturity of sight deposits is precisely zero.

Some thoughts

- A well-run economy operating without cash would require a trustworthy government. That is, the people who know where we are and what we’re buying and selling 24/7 would have to be decent, competent and honest. Otherwise we’re giving near-absolute power to folks who might use it for their own enrichment at our expense. Which is of course to state the blindingly obvious. The fact that power both corrupts and attracts the already corrupt means that the more power we hand the government, the further we push it towards absolute evil. A cashless society would pretty much guarantee a dictatorship in a single generation.

- If a cashless society is a means to the end of total government control of interest rates, i.e., the price of money, then the resulting deeply-negative rates would distort the pricing signals that make capitalism work. The system would devolve into a centrally-planned malinvestment-fest resembling bigger, more chaotic versions of the past century’s collectivist experiments, all of which crashed and burned in short order.

- An environment in which cash is illegal and interest rates are negative would be both insanely good and catastrophically bad for gold. Good because the removal of cash leaves only gold and silver as historically-trusted private stores of value. Terrified capital would pour into bullion, sending its relative price through the roof. But then of course it would become an overt (rather than a covert) target of the same forces that made cash illegal. When “the war on gold” begins, the world as we knew it will have already ended.

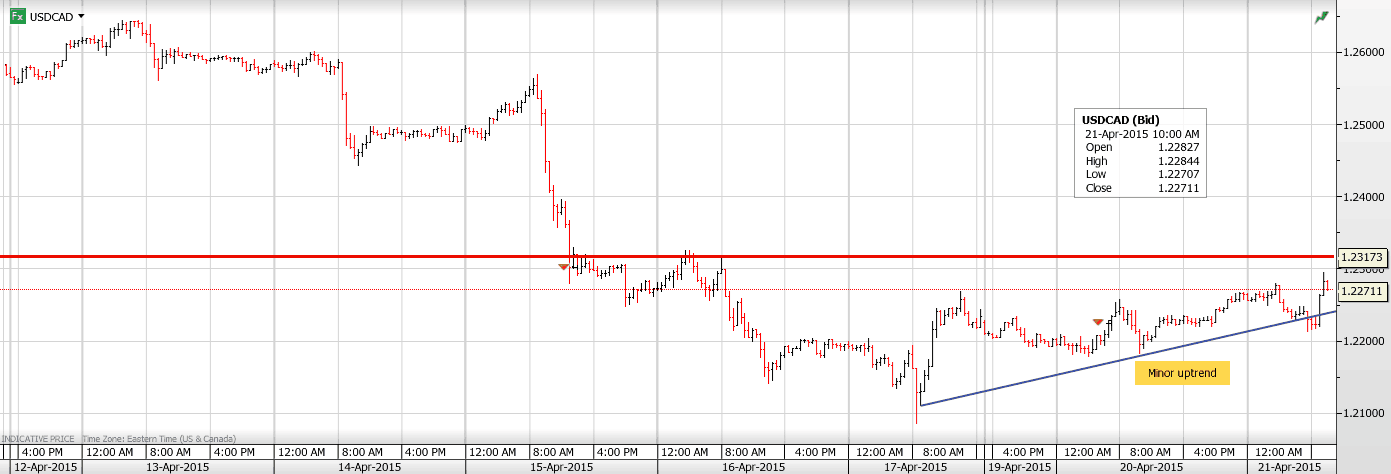

USDCAD Overnight Range 1.2218-1.2294

The US dollar has caught a bit of a bid in NY after being mostly offered overnight.EURUSD has dropped from 1.0710 to 1.0660 while USDJPY popped up from 119.25 to 119.75. There hasn’t been any real catalyst for the moves and USDCAD has been rising in sympathy with the US dollar gains. Today’s weak Wholesale Prices data didn’t help, but that data series is usually ignored anyway.

In Asia, USDCAD climbed steadily, continuing the NYC afternoon trend on the back of both profit-taking and AUDUSD weakness. That move reversed itself when Europe came in.AUDUSD was sold on verbal intervention by the RBA governor, yesterday, in NYC, and by doveish RBA minutes that led to a May rate cut conclusion.Further debate ensued and in Europe, AUDUSD recovered all of its losses, post RBA minutes. News that the ECB was studying ways to reduce Emergency Liquidity Assistance (ELA) to Greek banks sent EURUSD tumbling.

USDCAD is in consolidative mode. For the moment, the pause in the oil price rally and general US dollar strength has offset bearish USDCAD technicals and a new and more neutral BoC. However, the move below the 1.2340-60 area was significant and likely to cap any USDCAD rallies.

USDCAD technical outlook

The intraday USDCAD technicals are modestly bullish while trading above 1.2230 looking for a break above 1.2280 to extend gains to 1.2310 and then 1.2330. A move below 1.2230, targets 1.2210 and 1.2160. The longer term technicals are bearish while trading below 1.2340 looking for a retest of 1.2050.

Today’s Range 1.2240-1.2310

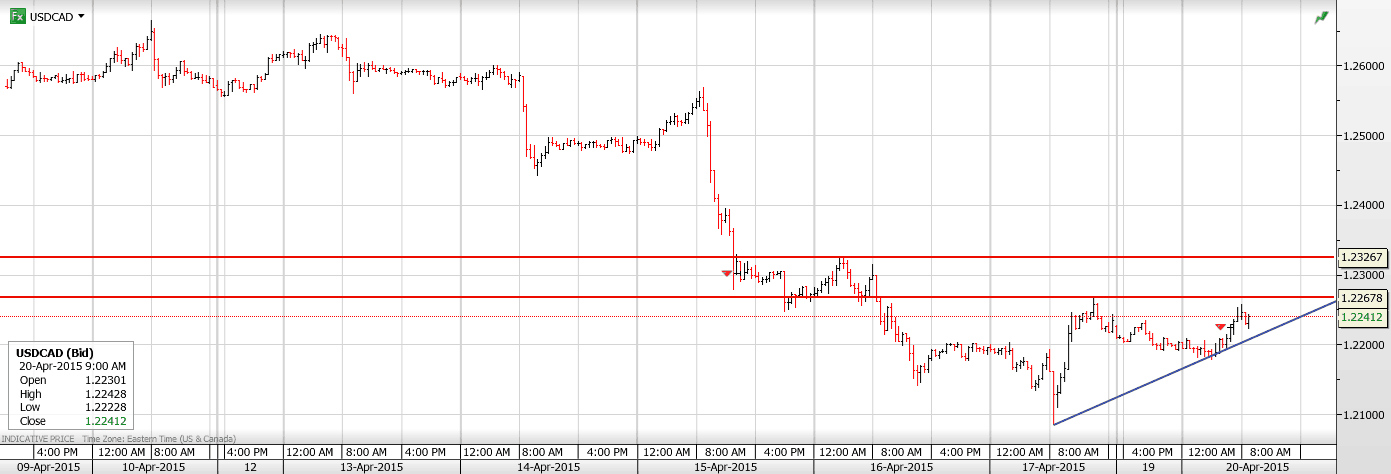

USDCAD Overnight Range 1.2183-1.2255

USDCAD was largely sidelined overnight and remains well off of Friday’s lows as it currently probes resistance in the 1.2250 area. The fundamental outlook for the Loonie has taken a turn for the good on the back of a rosier economic outlook by the Bank of Canada and better than expected economic data last Friday. Higher oil prices are also supporting the Canadian dollar.

China kicked off the FX week when the PBoC announced a 100 point cut in the Reserve Requirement Ration (RRR), hoping to boost bank lending. The news lifted AUD and NZD but that only lasted a short while and both currencies quickly returned to Friday’s lows during the European session. EURUSD trading will be governed by Greece news while the pound will be pounded by UK election headlines.

The BoC governor, Stephen Poloz, will be speaking in New York this morning and traders will be looking for additional bullish CAD remarks. Tomorrow’s Federal budget should be a non-event although forecasts for balanced budgets may help the currency.

USDCAD technical outlook

The intraday USDCAD technicals are modestly bullish while trading above 1.2210 looking for a break of resistance at 1.2260 to extend gains to 1.2320. A move below 1.2210 argues for a retest of the Friday low of 1.2089. For today, USDCAD support is at 1.2210 and 1.2160. Resistance is at 1.2250-60, 1.2290 and 1.2320

Today’s Range 1.2180-1.2260

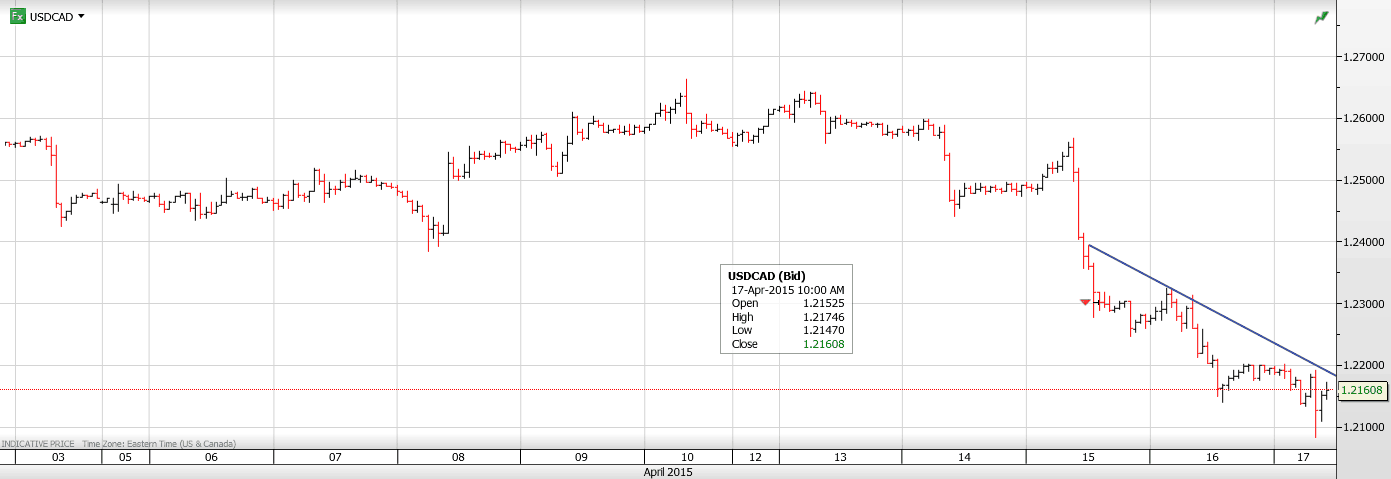

USDCAD Overnight Range 1.2093-1.2200

The Canadian dollar gained 3.5% against its US counterpart and outperformed against the rest of the G-7 currencies thanks to a less dovish Bank of Canada outlook, strong domestic data, higher oil prices and a generally soft US dollar.

Today’s Canadian CPI data (Actual 0.7% vs forecast of 0.5%) combined with a big jump in Retail Sales appears to have validated the slightly rosier outlook in the BoC’s Monetary Policy Report. The news led to additional demand for the Canadian dollar which managed to touch 1.2092 but has since bounced on the back of profit taking and a rise in the Michigan Consumer Confidence Index.

Overnight, the US dollar lost even more ground continuing the trend that started earlier this week when a series of weak economic reports crushed rate hike hopes for June and seriously debased the September call as well.

The Asian session was relatively tame but that wasn’t the case in Europe where the shifting outlook for US rates fueled EURUSD demand. A stronger than expected UK employment report put additional selling pressure on the US dollar and GBPUSD powered above 1.5000.

The outlook for the balance of the day will be one of consolidation. The US dollar should recoup some lost ground against the majors on profit taking ahead of the weekend.

USDCAD technical outlook

The intraday USDCAD technicals are bearish while trading below 1.2210.A break of minor support at 1.2140 and 1.2090 will extend losses to 1.2050. (61.8% Fibo of 2015 range). A move above 1.2210 will lead to a test of 1.2250. The 38.2% Fibo retracement of the July 14-March/15 range comes in at 1.1980.

Today’s Range 1.2140-1.2210

I can’t even count the number of analysts who believe Europe’s financial crisis is over.

I can’t even count the number of analysts who believe Europe’s financial crisis is over.

They claim that the massive 25 percent-plus decline in the euro is starting to stoke inflation … that economic indicators are starting to turn positive … that the recent record highs in Germany’s DAX are proof positive the crisis is over … and more.

But based on all of my research and trading models, nothing could be further from the truth.

First, the annual inflation rate in the euro zone was -0.1 percent in March. While a tad better than February, one month’s numbers don’t make a trend, and as far as I’m concerned, -0.1 percent is still deflation.

First, the annual inflation rate in the euro zone was -0.1 percent in March. While a tad better than February, one month’s numbers don’t make a trend, and as far as I’m concerned, -0.1 percent is still deflation.

Moreover, that figure is skewed due to the size of Germany’s economy. Actual deflation in most of the euro zone is far worse. Greece is running at -1.9 percent, and France is seeing prices fall at an annual average of -0.3 percent.

Prices in Spain are falling at a -0.7 percent rate, Cyprus at -1.88 and Poland at -1.6 percent. Hardly the stuff of strong economic growth and normalized inflation.

Second, unemployment remains high at 11.3 percent. Yes, that’s a slight improvement from February, but again, not enough to claim a trend reversal is underway.

And here too, the numbers are skewed due to Germany’s low unemployment of 4.8 percent. Greece is still seeing unemployment at 26 percent, Spain at 23.2 percent, Ireland 9.9 percent, Cyprus 16.3 percent, Croatia at 18.5 percent.

Youth unemployment, meanwhile, is still off the charts. 4.85 million Europeans under the age of 25 are unemployed, an amazing 21.1 percent. Again, it understates the problem. Greece has 51.2 percent youth unemployment, Spain, 50.7 percent, and Italy, an amazing 42.6 percent.

Third, severe austerity measures continue to this day and they are hollowing out Europe’s economic growth. The proof is in the numbers. Before the Greek crisis flared up,debt-to-GDP in Greece stood at 113 percent. Today — according to the most recent data and even after all the write-offs — Greece’s debt-to-GDP stands at a whopping 174 percent.

In Spain, pre-crisis debt stood at 40 percent of GDP. Today it’s 97.7 percent.

In Italy, debt-to-GDP is hovering near 132 percent while France is running at 92.2 percent … Ireland, 123.3 percent … Greece, 174.90 percent.

Clearly, all the austerity measures that Europe has implemented have done nothing to reduce debt levels. Instead, they are further hurting the people of Europe, causing economic growth to crater even more.

In short, there is ZERO evidence Europe’s economy is improving. And anyone who takes an uptick in one or even two or three months’ worth of economic numbers to make such claims is a fool. And unfortunately, there are a lot of them out there.

It’s kind of like saying gold has bottomed just because it rallied five or 10 dollars.

Most importantly, the long-term chart of the euro currency couldn’t be more bearish. Follow along with me by referring to the numbers on the chart below.

1) As you can clearly see, the major trend for the euro is now down. Solidly down. Virtually any rally in the euro is a counter trend move that should be sold.

2) As you can clearly see from this long-term uptrend line, it’s recently been broken. Another confirmation the long-term trend has changed to the downside.

3) Minor cyclical support is declining, a bearish sign too. That support currently stands at the 0.94800 level, well below the market, and declines all the way down to the 0.74 percent level by 2020, when I expect the final bottom in the euro, which will signal the collapse and breakup of the European Union.

4) This is what I call a projection line, a type of line I developed many moons ago that aids in determining where major lows can form (or conversely, highs in a bull market).

It acts as a kind of magnet for price moves, and it’s a leading technical indicator in the sense that it melds both time and price.

As you can clearly see, the slope of this projection line is seriously negative, a sign of just how bearish the euro is.

{kind=link}

Moreover, it points to as low as 0.36 for the euro by the next major cyclical target for the euro currency in 2019/2020.

I don’t think the currency will go that low, since there will be complete chaos in Europe once the currency falls back to its 2001 low of roughly 0.82.

But as noted above, I have no doubt the euro will plunge to at least the 0.74 level, by 2020 at the latest, and probably much sooner than that.

Bottom line: Based on the long-term chart of the euro, there is virtually no way Europe is recovering, not in any way, shape or form.

So don’t buy into all the analysts who take an uptick or two in economic stats and say otherwise.

Instead, the smart thing to do is …

A. Recognize the long-term trend, the European Union is decaying and the grand experiment of a single currency and a United States of Europe is failing.

B. Steer clear of European sovereign debt. Period. It’s a disaster in the making.

C. If you’re a speculator, sell short the euro on rallies, either in the forex markets, in futures, or by purchasing an inverse ETF, such as ProShares UltraShort Euro, symbol EUO.

D. If your business is vulnerable to a decline in the euro, consider hedging your exposure via similar methods.

E. If you’re looking to invest in Europe, either its stock markets or via buying a business or real estate — I say be patient. You’ll be able to buy those assets 40 percent cheaper than they currently are, if not cheaper, a few years from now.

In the meantime, there are better things to do with your money.

Best wishes, as always …

Larry

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair