Currency

Strengths

- Deutsche Bank said that after seven consecutive days of gains in the gold market, it has become increasingly difficult to dismiss the rally as merely a function of the recent weakness in the U.S. dollar. Additionally, Saudi Arabia-led bombings in Yemen this week boosted demand for safe-haven assets. The Saudi government pledged to continue the strikes against Shiite rebels to prop up the allied government.

- Bank of America believes the euro/dollar squeeze is not over, meaning the dollar should continue to correct lower. Given this outlook, BofA recommended buying any dips in the gold price and set a target of $1,307 per ounce.

- Shanghai Gold Exchange withdrawal volume through March 13 was 51.5 metric tons (mt). If this pace continues, withdrawals this year would exceed last year’s 2,102 mt.

Weaknesses

- JPMorgan Chase, Barclays, Goldman Sachs, HSBC, Bank of Nova Scotia, SocGen and UBS will be the participant banks in setting the LBMA Gold Price benchmark. Several of these banks have been involved in commodities price-fixing scandals. China, now a major player in the global gold trade, was not granted representation. Commentators have speculated that had Chinese banks been included, there would be less room for manipulation.

- Reports have been circulated speculating that Nevsun’s Bisha mine had been bombed by the Ethiopian Air Force, in retaliation to an Ethiopian helicopter being held by Eritrea, earlier in the week. So far Nevsun has only reported an “act of vandalism” at the mine which caused no significant damage, affecting only the base of a tailings thickener.

- Platinum non-commercial Nymex shorts have more than doubled since the beginning of February and last week rose another 13.2 percent to their fourth successive all-time high. Several factors have weighed on the metal recently including an ongoing weak demand outlook due to constrained diesel auto catalyst consumption in Europe, poor jewelry demand for platinum in China, and South African supply recovering much more quickly than expected after last year’s five-month-long strikes.

Opportunities

- HSBC analysts, some of the earliest adopters of a bullish view on the U.S. dollar back in 2013, now believe the dollar rally may be at or nearing its end. The analysts point out that past dollar rallies of this type have mostly seen a dollar appreciation of around 20 percent and lasted from under a year, meaning the current rally is already extended. Furthermore, they pointed out that disappointing U.S. economic data is mounting and being largely ignored. Valuations suggest that the U.S. dollar may now be the world’s most overvalued currency, only being overshadowed by the strength in the Swiss franc since its tie to the euro was cut.

- The Philadelphia Gold and Silver Index, made up of the largest gold stocks, is at around a 73 percent discount to the bullion price, with the index more than 60 percent lower than the start of 2008. Gold, on the other hand, is still more than 40 percent higher. The index’s total price/cash flow has almost halved from 2008, to around 7.5x from 14.3x even though it is expected to post its first positive operating income this year since 2012.

- TD Securities published a precious metals outlook in which the firm questions the sustainability of the supply/demand balance in the gold market due to declining reserves. 2014 marked the third straight year of reserve declines, with exploration spending being reduced as miners focused on capital preservation. Total reserves for the large-cap producers are down around 24 percent from the 2011 peak. The decline highlights that existing exploration budgets are not sufficient to keep pace with current mining depletion. In contrast, Integra Gold announced it recently intersected 14.8 grams per tonne (g/t) gold over 10 meters and 11.5 g/t gold over 8 meters in a step-out drilling up to 330 meters from triangle. Discoveries like Integra could make it of interest as a takeover target.

Threats

- Analysts at SocGen published a report in which they forecast that the gold price, having given away all its early year gains, is headed sharply lower, as they see a continuation in the dollar’s strength. They see the price of gold falling to an average of $925 per ounce between 2016 and 2019. The timing of the report was perhaps unfortunate in that it predated the events of the past few days, which has seen the reverse, occur.

- CPM Group sees gold falling for a third straight year in 2015 as concern eases that global economies will falter, curbing demand for the metal as a haven. CPM Group forecast gold will average $1,208 per ounce in 2015.

- Under the auspices of fighting terrorism, France’s Minister of Finance has rolled out a series of eight new restrictions aimed specifically at minimizing the use of cash. In reality, these are capital controls designed to keep individuals’ savings trapped in the banking system. Many banks in Europe have already dropped their deposit rates into negative territory and as interest rates become even more negative, more people will realize that they’re better off holding physical cash instead of paying their banker to hold it for them.

“Just a little patience, yeah…”

– Guns N’ Roses

Lastweek the FOMC essentially removed forward guidance and placed all options back on the table, and at the end of the day they’ve opened the door for further tightening. As Yellen recently explained in advance, the removal of the word patience from the Fed’s guidance amounts to fair warning to the rest of the world’s central banks: an interest rate hike is on the horizon. Govern your actions accordingly. (My personal guess, for those interested, is September, with the Fed proceeding exceedingly slowly and cautiously thereafter.)

Lastweek the FOMC essentially removed forward guidance and placed all options back on the table, and at the end of the day they’ve opened the door for further tightening. As Yellen recently explained in advance, the removal of the word patience from the Fed’s guidance amounts to fair warning to the rest of the world’s central banks: an interest rate hike is on the horizon. Govern your actions accordingly. (My personal guess, for those interested, is September, with the Fed proceeding exceedingly slowly and cautiously thereafter.)

The bigger story here is the sustained strength of the US dollar, which has traded wildly in the FOMC’s wake. A correction to the one-way trading prior to the meeting was well overdue and could last some time, but then the dollar strength will resume. (Euro) Parity or Bust! My young colleague Worth Wray and I have been writing for some time about the risks this trend poses, to emerging markets in particular, and now it seems that nightmare could happen sooner rather than later.

We’re already seeing profound FX pressures on countries like Russia, Brazil, Turkey, and South Africa, among many others; but, while clearly exacerbated by the strong dollar and/or weak commodity prices, recent stress in various emerging markets appears to have more to do with internal troubles than external shocks. Nevertheless, the dollar’s strength has not been fully absorbed by EM economies, so a BIG, broad-based, dollar-driven adjustment may be yet to come.

Until this Wednesday’s FOMC press conference with Janet Yellen, the growing consensus was that an eventual interest rate hike would lead to an even stronger USD. Now it seems most observers, including our own Jared Dillian, are doubting that a rate hike will come this summer… or anytime soon.

Worth and I have a different view. We believe that Federal Reserve Vice Chair Stanley Fischer has carefully laid out a framework for interpreting the FOMC’s opaque communications as the committee moves closer to a rate hike. In a speech last October, Fischer made it clear that the Fed would “recognize the effect of (its) actions abroad and … minimize the negative spillovers (those actions will likely have) on the global economy” by clearly communicating its policy intentions in advance. If you read between the lines, the only way the Fed can give foreign central banks the opportunity to prepare for the likely FX shock that would follow a rate hike is to send the message in a way that the market does not immediately understand as overtly hawkish. This week’s announcement makes perfect sense when looked at through that lens.

Translation: while the FOMC’s decision to hike interest rates remains data-dependent, the Fed has opened the door for further tightening as soon as June 2015. That could be terrible news for a number of emerging markets, but none of those countries can credibly complain that the Fed is responsible as capital flees their economies in search of safety and more-attractive risk-adjusted rates. Emerging markets are not a homogenous group, but even the best positioned countries like the Philippines are at risk in the event of a broad-based contagion. We’ve seen that dynamic play out repeatedly in the 1980s, the 1990s, and the 2000s. It may be time for another hurricane.

With our expectations on the table, Worth and I still have to ask… what if we’re wrong? What if the dollar doesn’t strengthen? We’ll consider that scenario in today’s OTB.

It’s a real pleasure for me to introduce today’s author, because this OTB is also the perfect opportunity for an announcement I’ve been wanting to make for some time: Jawad Mian has brought his excellent research service, Stray Reflections, to Mauldin Economics. You can learn more about his service here. His “transparent hedge fund” approach to investment research is unique, well-reasoned, and decidedly non-consensus. And his prose is unrivaled.

Today’s OTB is taken from Jawad’s top 10 investment themes. These are the themes around which he builds his portfolio. I agree with many of his ideas, but I offer up this particular piece as an example of one where I remain unconvinced, if not in outright disagreement. Yet… Jawad makes such a strong argument for the dollar’s weakening. We have exchanged emails and dueling notes of late (but in a very collegial fashion).

I have to admit, I am NEVER comfortable when this much of the crowd agrees with my view, as they seem to now. A serious correction of the recent trend in dollar strength is clearly due, but what if – as Jawad argues – we are seeing a major shift to an entirely new macro regime?

It’s worth noting that Jawad made this weaker dollar call several months ago. HSBC analysts and others are beginning to agree with him. The US dollar is the single most important factor in global macroeconomics; so do your homework, consider the antithesis to your closely held beliefs, and ignore Jawad’s thoughtful analysis at your own risk.

I was in Switzerland for the last week, meeting clients and speaking in Zürich. I kept asking the question, “Where is Draghi going to get €60 trillion in European bonds, month after month?” He is reportedly already behind the curve for this month’s purchases. I get no satisfactory (to me) answer. Maybe he does, but he wants to buy more than governments are issuing, and no pension company or insurance company is going to be able to sell him their bonds if they have a positive yield. Maybe he gets creative in what he buys. I will write more about this over the next weekend, but we are in the Twilight Zone for bonds. French yields are negative out to five years, and to get 1.5% you have to buy a 50-year French bond? Can anyone do that and seriously be considered a prudent fiduciary? Have you looked at France’s balance sheet and total commitments, not to mention the country’s politics? And don’t even get me started on the rest of Europe. Half of Northern Europe’s debt has negative yields.

I had the very real privilege of having dinner with William White, former chief economist of the Bank of International Settlements and currently consultant to seemingly everyone. He will be at my conference this year as the final speaker, and it will be a very impactful speech. On several occasions during dinner, I got him to agree to say in public what he said in private Tuesday night. I have long been a fan of his candor and style, and that evening I felt like a student. He is now my favorite (ex) central banker.

I want to thank so many of you who wrote to me expressing your condolences about my Mother. It meant a lot. Truly.

My sister flew in from Victoria Island, where she lives with her sons. I cornered her the first night she was there and told her that her other brother wanted us to sing at the graveside the lullabies that mother sang to us as children when she put us to bed (and which we all vividly remember). I tried to convey the clear impression that I thought it was a bad idea, but I was amazed that she agreed with him. “I think it is a marvelous idea, and mother would agree. You will do it.” How can you tell your little sister no when she looks at you that way? So, there I was, singing in the rain, or trying to. I don’t think I actually made it to the end of “Tura Lura Lural.” In the moment it was much more than an old Irish lullaby.

Your doing a lot of pondering analyst,

John Mauldin, Editor

Outside the Boxsubscribers@mauldineconomics.com

USDCAD Overnight Range 1.2475-1.2520

US Durable Goods orders were far worse than expected, dropping 1.4% vs. forecasts of a rise of 0.2%. Crummy weather along the US East Coast and Mid-West may have played a factor, but for now, no one cares and the US dollar is offered.

USDCAD remains range-bound. Overnight, it drifted aimlessly as traders licked their wounds following Tuesday’s whip-saw day. Risks are seemingly balanced between additional US dollar selling on an FOMC rate hike delay and soft oil prices and weak economic data for Canada. Bank of Canada governor, Poloz speaks Thursday, in the UK, on Central Bank Credibility and Policy Normalization.That speech may not be a good thing for the Loonie as the domestic economic data has been weak and oil prices low.

Asian markets ignored comments from Chicago Fed President, Evans arguing (as usual) for a rate hike delay.Kiwi shrugged off a weaker than expected trade report and moved higher while JPY traders are just waiting for year-end (March 31) to pass. EURUSD moved higher in Europe, supported to a degree by a positive IFO report from Germany.

USDCAD technical Outlook

The intraday USDCAD technicals are bearish while trading below 1.2520 but need to break through support in the 1.2440-60 area to extend losses to 1.2340. A break above 1.2520 targets 1.2550 and then 1.2620. For today, USD support is at 1.2480, 1.2460 and 1.2440. Resistance is at 1.2520, 1.2550 and 1.2590

Today’s Range 1.2450-1.2520

![]()

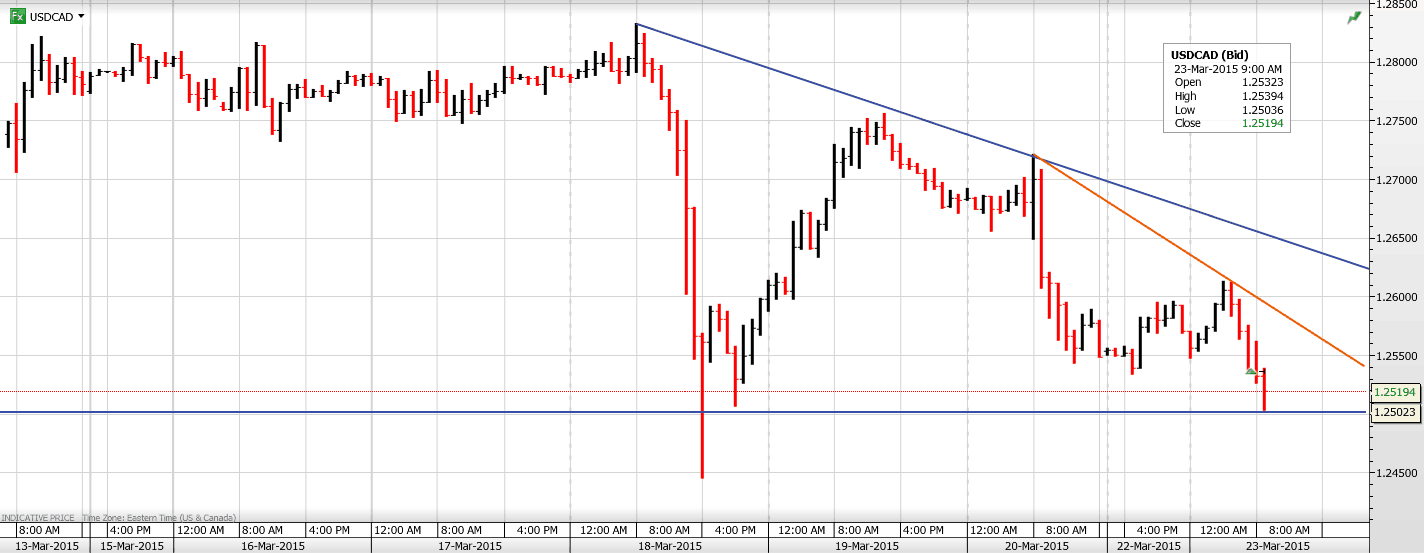

USDCAD Overnight Range 1.2509-1.2613

The US dollar is in full retreat, especially against EUR on the back of rising expectations that a US rate hike is a lot further down the road than previously expected. The Loonie is benefitting from the move and ignoring bearish remarks from the Saudi oil minister. He said that Saudi Arabia would only consider production cuts if non Opec nations cooperated. WTI oil prices are off their lows but the technicals remain bearish.

The US dollar opened the week trading lower in Asia. NZDUSD surged on better than expected consumer confidence data taking the Aussie along for the ride. USDJPY was quiet on the approach to Japan’s fiscal year end of March 31. The US dollar bounced early in the European session but those gains faded rapidly. Positive sounding headlines on Greece debt negotiations and ongoing US dollar position adjustment, post FOMC, drove EURUSD toward 1.0900.

There are two Fed speakers on tap today, Vice Chair Stanley Fisher, and John Williams. President of the San Francisco Federal Reserve

USDCAD technical Outlook

The intraday USDCAD technicals are bearish while trading below 1.2650. This morning’s break of 1.2530 supports additional losses below 1.2510 to the 1.2340-60 area. To the top, a move above resistance at 1.2550 would lead to 1.2590, which if broken points to 1.2650. The uptrend from the November low remains intact above 1.2440-60 area.

Today’s Range 1.2490-1.2560

![]()

We’ve maintained our bullish US Dollar bets with CAD short positions (we “coulda/shoulda” been more aggressive given the US Dollar upside breakout) and we’ve maintained our bearish bets on WTI Crude. Three weeks ago we took an initial short position in US stocks.

The US Dollar Index has surged higher the past 3 weeks…up 25% since July 2014 at fresh 12 year highs. It has recovered about half of what it lost during its 2002 to 2008 bear market…we think it has a lot more upside…

…..continue reading commentary & view 5 more charts HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair