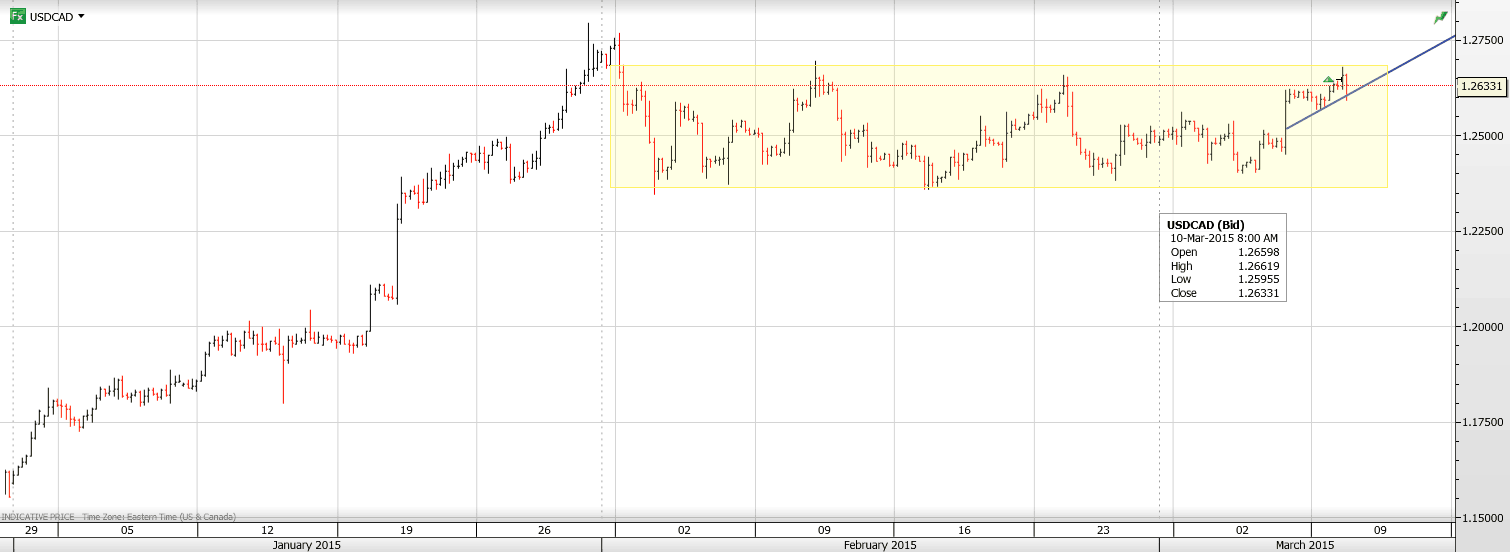

Currency

USDCAD Overnight Range 1.2600-1.2680

USDCAD hit resistance at 1.2680 overnight and has been tumbling ever since, touching 1.2500 just recently. It did not move in a vacuum but as part of a widespread US dollar retreat as a lack of fresh stimulus led to profit-taking.

Overnight, it was a different tale. The US dollar stormed higher in Europe despite a lack of a clear catalyst for the move. The US gains were impressive and across the board, gaining nearly 1% vs. EUR and over 1% vs. NZD and AUD. In a speech, Dallas Fed Chairman, Richard Fisher, his last as a member of the Fed, called for the FOMC to raise early.While nothing new, in the face of last Friday’s strong employment report and the start of QE in the EU, traders started buying US dollars again. The break of key support levels (107.60) in EURUSD point to further losses ahead.

However, so far in New York trading, EURUSD is about where it started while the dollar lost ground against GBP, JPY CAD and AUD

USDCAD technical Outlook

The intraday USDCAD technicals are bullish following the break of resistance at 1.2580 and again at 1.2620. However, it appears that resistance in the 1.2660-80 has contained the rally and until 1.2800 is decisively broken the current USDCAD 1.2360-1.2680 range remains intact.

![]()

Let’s step back in time. As we all remember, on January 15th, a surprise decoupling from the euro peg caused the Swiss franc to rally up to 23%, an unprecedented move in the currency market. Why was the peg introduced and later removed?

The SNB pegged the franc to the euro on September 6th, 2011, in the very middle of the Eurozone debt crisis. A few peripheral countries, whose debts had been downgraded to junk status, asked for bailouts. Therefore, investors ran from euros and moved into the Swiss franc, a traditional safe haven. The SNB introduced a minimal exchange rate at CHF 1.20 per euro (0.83 euro per franc) in order to resist the currency appreciation (the CHF gained 28% since the beginning of the Global Financial Crisis). Although gradual appreciation is positive and reflects the strength of a currency, sudden capital inflows and exchange rate fluctuations may be quite detrimental, and therefore the SNB began printing and selling francs to keep the currency from exceeding 0.83 euro.

The peg worked quite well, but not without costs. The SNB expanded its balance sheet to 80% of GDP and the foreign currency reserves doubled from around 250 billion to 500 billion francs. At one point the SNB was buying half of the new government debt issuance of the Eurozone.

Thus, the SNB removed the peg due to concerns about the large expansion of the money supply. Not only did the monetary base expand but also broad money (Chart 1), which actually increased as it did in Ireland or Spain before the Global Financial Crisis.

Chart 1: Swiss money supply (M3) from December 2004 to December 2014 (in billions of Swiss francs)

According to the SNB, 70% of the increase in the M3 money supply, which occurred between October 2008 and October 2014 (311 billion francs), can be attributed to the increase in domestic Swiss franc lending. Between 2011 and 2014 the bank’s lending rose from 145% to 170% of the GDP, which set off a property boom. Swiss real estate prices rose by an average of 6% per year between 2008 and 2013, and flat prices more than doubled since early 2007 until now. Consequently, the real estate bubble index published by the UBS found itself in the ‘risk zone’. Thus, the SNB’s move could have resulted from adopting a tighter monetary policy to avoid a further bubble and followed the housing collapse that crippled the economy in the early 1990s.

Perhaps, the gold referendum in November, 2014 added some political pressure to tighten the monetary policy, while the expected announcement of the QE in the Eurozone on January 22 might be responsible for the timing of the SNB’s decision. Note that its move came just a day after the European Court of Justice paved the way for a program of sovereign bond buying. Additionally, as Thomas Jordan, the president of the SNB, pointed out, “The euro has depreciated substantially against the US dollar and this, in turn, has caused the Swiss franc to weaken against the US dollar.” For once, one of the reasons of keeping the peg was removed.

What are the possible consequences of the SNB’s move for the global economy and the gold market? The removal of the peg caused significant franc appreciation, which harmed exporters (strong currency is not bad for the economy, but abrupt exchange rate movements are usually harmful) and banks which granted international loans. Due to the Swiss franc’s safe haven status and low interest rates, lots of loans in Europe are denominated in Swiss francs, which creates a new risk in the old continent (for example, Austrian borrowers hold 10% of GDP in CHF loans). Removing the peg could entail the European mortgage backed security crisis, which would be supportive for gold, the ultimate safe haven.

Theoretically, it could cause another shift from the euro into the Swiss franc. The ECB’s QE would also strengthen the Swiss franc. However, the SNB lowered the interest rate for balances held on sight deposit accounts from -0.25% to -0.75%, in order to deter the capital inflows and currency appreciation, inducing banks to conduct more “real” lending to boost the economy. Interestingly, the SNB introduced the negative interest rate in December, 2014 to a large extent in order to stem a tide of money flowing in due to Russia’s financial crisis.

The predicted slight recession in the 2015, a possible bursting of the real estate bubble, and banks’ problems with the international non-performing loans would also weigh on further price appreciation. Therefore, after some depreciation (initial movements in the currency movements are often exaggerated), the Swiss franc may likely trend sideways in coming months (unless the Eurozone collapses). However, investors should be aware that the negative interest rates between 1972 and 1978 introduced by the SNB did not prevent the 75-percent appreciation of the franc. The long-term future of the Swiss currency depends to a large extent on the pace of printing money and whether the SNB is willing to abandon price stability in favor of an exchange rate target.

In the short run, the winners would be the greenback and gold, because there is one less safe-haven currency in town. The yellow metal and the U.S. dollar can additionally gain if the SNB re-allocates some of its euro-denominated holdings into them, which seems to be logical step after removing the peg to euro. Although some foreign investors (like Russians, which is quite understandable, taking into account the ruble’s uncertain future) still want to hold Swiss francs and pay 0.75%, gold has become relatively cheaper to hold as a safe-haven. Any further decreases of the Swiss interest rates, thus, would positively affect the gold prices.

Would you like to know what the major central banks’ action mean to the global economy and gold market? We analyze the recent surprising SNB’s action in our last Market Overview report. We provide also Gold & Silver Trading Alerts for traders interested more in the short-term analysis. Sign up for our gold newsletter and stay up-to-date. It’s free and you can unsubscribe anytime.

Thank you.

The premise of a currency war is that by devaluing its currency a country is able to sell things overseas more cheaply, which gooses its growth at the expense of its trading partners.

If it actually works that way, then you’d expect this chart of the euro plunging against the dollar..

…to be reflected in some sort of strong-dollar related downturn in the US. And right on cue, the Fed reported this morning that American manufacturers are now in the sixth month of a new-orders slowdown:

If things continue to play out according to script the coming year will be slightly better than expected for Europe (but only slightly because of all the other messes those guys have made of their common currency experiment) and quite a bit worse than expected for the US (because we actually think we’re recovering).

Then comes the next and final stage of the cycle, where the US realizes that it’s tipping back into recession, with all the unacceptable things that that implies for the equity bubble, tax revenues and campaign contributions, and shifts gears from tightening to open-the-floodgates loose, hoping to push the dollar back down against the euro, yen and yuan. The difference this time around will be that, as Europe is now discovering, easing monetary policy when interest rates are already zero means pushing into negative numbers. And that means yet another leap of faith into uncharted, experimental, very possibly disastrous territory.

USDCAD Overnight Range 1.2410-1.2484

The Loonie has held on to most of yesterday’s gains despite broad-based US dollar strength against the majors. A sleepy European session was jolted awake when Mario Draghi started speaking. EURUSD bobbed and weaved within a 1.1000-1.1100 during his remarks even though he didn’t seem to say anything EUR negative.

Earlier, US jobless claims provided a disappointing result, rising to 320K but traders seemed to have shrugged off the result.

The Canadian Ivey Index rebounded to 50.8 from 42.8 in January but hasn’t really impact USDCAD trading. The recent series of lower, highs in the daily ranges combined with a neutral BoC and firmer oil prices in an environment where traders are already well long USDCAD argues for another test of the 1.2340-60 support area. However, that move will be on hold until after tomorrow’s US payrolls data.

USDCAD technical Outlook

The intraday USDCAD technicals are bearish below 1.2490 and looking for a break of minor support at 1.2410 to extend losses to 1.2340. A break of this level puts 1.2060 in play. A move above 1.2490 argues for more 1.2400-1.2550 range trading

Today’s Range 1.2420-90

Chart: Larger USDCAD hourly with post BoC drop shown HERE

Over the last year, the US Dollar has had an incredible surge in value of 11%. It appreciated against all main currencies in the world in 2014.

Meanwhile, gold also actually increased in value when valued against the vast majority of world currencies but the dollar was the only currency that it could not conquer.

What is behind this surge in value for the dollar?

In our opinion, it is a very easy explanation: as investors abandon all other options, they continue to look for safe havens. With central banks such as the Swiss National Bank and the Bank of Canada making surprising interest rate or pegging decisions, everyone is looking for safety and predictability. The ECB and Bank of Japan are piling onto the problem by fighting deflation with massive quantitative easing programs.

These are also the reasons why gold has also seen a recent bounce back as well.

The question is: how long can the USD remain the safe haven of choice? With moderate economic growth still happening, investors still seem to have confidence in the United States. However, if that at all falters and economic growth slows, there will be nowhere to hide. Remember that it only takes one event to cause a ripple effect and the US Dollar bull run could be over.

To quote Mr. Warren Buffett: “Only when the tide goes out do you discover who’s been swimming naked.”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair