Currency

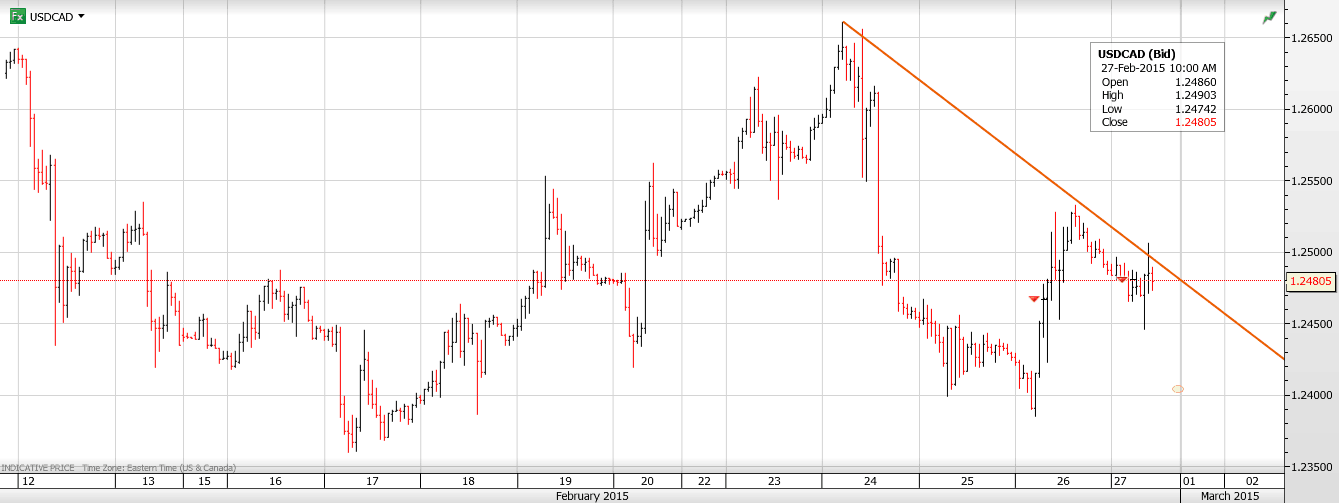

USDCAD Overnight Range 1.2450-1.2520

USDCAD has backed off of the overnight peak and dipped down to 1.2453 just prior to the release of the US GDP data which, at 2.2% yoy, modestly beat the forecast of 2.1%. The subsequent bounce back above 1.2500 was less a factor of the data but more likely due to a drop in EURUSD to 1.1175 from 1.1245. The Chicago PMI was weak (45.8 vs. forecast of 58.0) and leaked early, adding to the FX market confusion. The weakness has been attributed to weather and the port strike so the data will be ignored.

Overnight, AUDUSD on a renewed rate cut debate ahead of Tuesday’s RBA meeting. Will they or won’t they? Initial AUDUSD losses were recovered but the currency pair is still trading with an offered tone.

Today is the last day of the month and therefore, portfolio rebalancing day. There are reports that the 16:00 GMT fix (8:00 am PST) will lead to selling of US dollars against the majors, including CAD. However, the prospect of that one-off, intraday flow is struggling against renewed US dollar demand due to the prospect of higher US rates, sooner than expected. Furth gains in WTI from $49.10 could add to Canadian dollar demand.

USDCAD technical Outlook

The intraday USDCAD technicals are bearish while trading below 1.2505-10 with a break of 1.2450 suggesting further losses to 1.2380-1.2410 today. A break above 1.2550 risks further upside to 1.2640. For today, USD support is at 1.2450, 1.2410 and 1.2380. Resistance is at 1.2520, 1.2550 and 1.2610.

Today’s Range 1.2410-1.2510

Chart: USDCAD hourly showing intraday downtrend still intact

Sideways trading was the norm for the rest of the G-7 currencies overnight. Janet Yellen’s Congressional testimony did not satisfy hawks or doves while the EU/Greek buffer deal has put that crisis on the back burner. Even Russia threatening to cut off Ukraine gas supplies on Friday hasn’t raised much of a stink.

The rather uneventful overnight session has turned rather robust with data and Fed comments sparking renewed US dollar demand. US Durable goods (2.8%) were much higher than expected while core CPI mitigated deflation fears. EURUSD broke support at 1.1300 and is sitting at 1.1250 with 1.1000 in sight.

USDCAD has gone for a wild roller coaster ride. After having a peek at support at 1.2390 in Asia, it edged up to 1.2470 prior to the Canadian CPI release. Traders appeared confused with the data. The headline said CPI rose 1.0% in January (yoy) and they sold USDCAD. The monthly data noted a 0.2% decline and then the bought USDCAD, helped by bullish US data. Meanwhile, core CPI was unchanged.

USDCAD technical Outlook

The intraday USDCAD technicals are mixed. The bounce from 1.2390 and subsequent break above 1.2460 argues for further gains to 1.2550. On the other hand, the drop below support 1.2550 keeps the focus on 1.2340-60. The reality is that USDCAD is directionless within the context of the 1.2350-1.2550 range.

Today’s Range 1.2440-1.2510

![]()

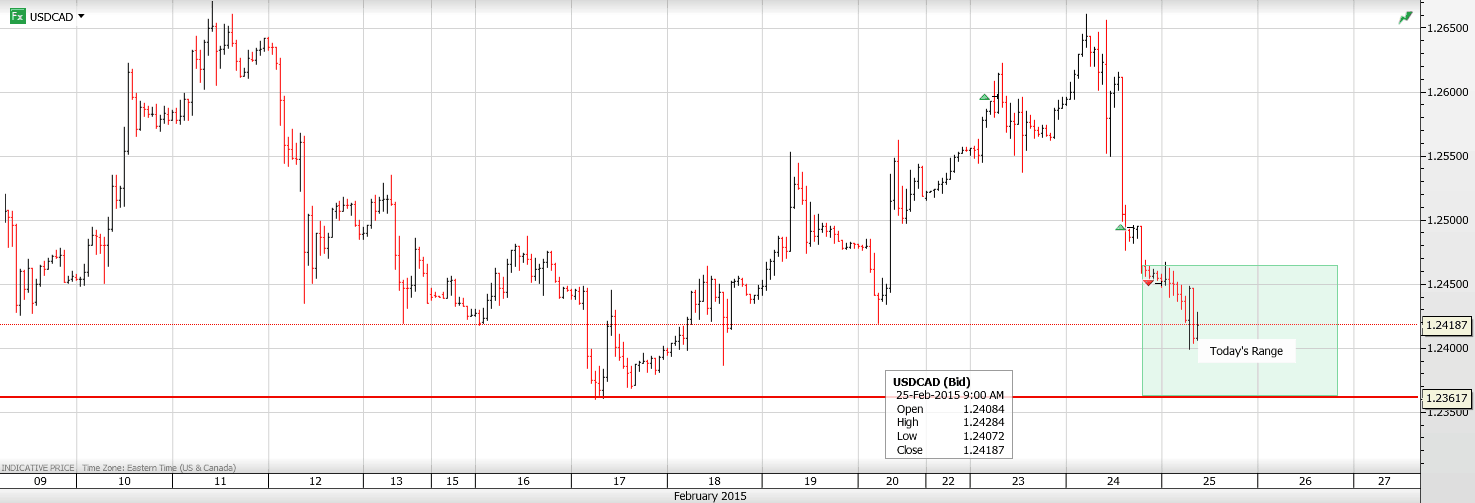

USDCAD Overnight Range 1.2405-1.2496

It appears that Mr. Poloz has taken the 1980 Devo song to heart and decided to whip the FX markets and whip’em good. After whipping the Loonie to Fifty Shades of Down last month, he used yesterday’s speech and lashed the Loonie Fifty Shades of Up. Last month’s rate cut was blamed on “falling oil prices being unambiguously negative for Canada”.Yesterday,not so much. The rate cut was just insurance. March rate cuts predictions were tossed out the window while Mr. Poloz gleefully clapped “it’s an exciting time to be a Central Banker.” Expectations for another rate cut on Tuesday were tossed out the window along with USDCAD bulls and the Loonie gained over 2 cents.

Meanwhile, the debate rages as to whether Ms. Yellen’s speech was hawkish or doveish. Her comments were fairly upbeat leaving scope for a June hike on the table.Unfortunately,it seems that FX markets expected her to declare June, FOMC Rate Hike month and were disappointed.

Tomorrow’s US economic data releases will be important signposts as to whether a June rate hike is still on the table.

USDCAD technical Outlook

The intraday USDCAD technicals are bearish following the break of 1.2490 and 1.2440 which targets the 1.2340-60 area. A break here risks further losses to 1.2050. For today, USD support is at 1.2405 and 1.2380. Resistance is at 1.2450 and 1.2470

Today’s Range 1.2380-1.2450

![]()

It’s no coincidence that the stock market’s steep rise in February began just days after an equally steep rise in the dollar stalled in late January. The dollar has been moving sideways ever since, extending a monotonous sine-wave correction that is setting up the dollar’s next powerful rally. It projects to at least 96.30, a relatively modest move of about 2% that would leave DXY a tad shy of a small but technically important peak at 99.25 recorded in August of 2003 (see inset). The dollar has already blown past a more significant ‘external’ peak at 99.25 from 2005, so it’s got nothing to prove. But if the next upthrust eventually exceeds the 96.30 target as I expect, it would add a robust new dimension to the bull market begun in earnest last year. It would also put considerable pressure on U.S. stocks, perhaps even ending February’s joy-ride on Wall Street.

![]() Confounded Interest just posted a nice summary of a McKinsey report on the growth of global debt during what some persist in calling the “great deleveraging.” Turns out that since the crisis of 2008, debt has actually risen by $57 trillion, and the ratio of debt to GDP is up 17 percentage points to 286%. Meanwhile, central banks are monetizing 100% of newly-issued sovereign debt.

Confounded Interest just posted a nice summary of a McKinsey report on the growth of global debt during what some persist in calling the “great deleveraging.” Turns out that since the crisis of 2008, debt has actually risen by $57 trillion, and the ratio of debt to GDP is up 17 percentage points to 286%. Meanwhile, central banks are monetizing 100% of newly-issued sovereign debt.

The obvious response to this is 1) wow, nothing has been fixed; in fact just the opposite, and 2) these stats, horrendous as they are, are incomplete because they don’t include unfunded liabilities of governments and private pensions, which are just as real as any other kind of debt.

But unfunded liabilities must be getting better, what with the stocks and bonds in pension fund portfolios soaring lately. Right? Since that’s an effortless Google search, that’s what I did. And the results were both counterintuitive and scary. It seems that even with pension fund investment portfolios booming, obligations to future retirees are rising even faster, making these entities even more underfunded today than in 2007. Here’s a sampling of the headlines just from February, in the order they appear in the search window:

Unfunded liabilities and the investment smokescreen

US teachers state pensions near $500 billion in underfunded liabilities

Teacher pensions: the math adds up to a crisis

Unfunded pension liabilities up for Pittsburgh

Cascade report exposes $26 billion unfunded liabilities

Prescott unfunded pension liability surpasses $70 million

Sacramento’s ‘wall of debt’ grows dangerously high

Absent from this list is the US federal government’s number, though that’s also easy to find. From Forbes: You Think The Deficit Is Bad? Federal Unfunded Liabilities Exceed $127 Trillion. That’s about 6 times the reported federal debt.

Now, easy money advocates argue that the solution to this and all other unbalanced economic equations is to borrow and spend enough new cash to get asset prices up and put people back to work. But stocks and bonds are currently at record highs and the unemployment rate is below 6% (peak-of-the-cycle kinds of numbers that have historically preceded corrections in which investment returns and tax receipts both plunge, raising unfunded liabilities).

So it looks like we’ve thrown our best punch and the problem is still standing there, wondering if that’s all we’ve got. Which leaves the US and the rest of the world — where debt and unfunded liabilities also continue to rise — with the question: If debt was the thing that nearly destroyed the global financial system in 2008 and debt — both narrowly and broadly defined — is way up since then, what happens in the next downturn? The answer is who knows, because this is uncharted territory both in terms of the size of the imbalances and governments’ policy responses.

The only thing that’s certain is that there are more cities, states and related pension funds poised to blow up than ever before.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair