Currency

Quotable

“Hubris is one of the great renewable resources.”

P. J. O’Rourke

Commentary & Analysis

What if almost everybody is wrong about the euro?

I have to confess, I have been a long-time doomer and gloomer on the euro. And the last time I was as gloomy as those are in the market now, was just before the currency blasted off for a 25 cent rally against the dollar back in June 2012. Back then I knew it was finally over for the euro. I was extremely confident price action was confirming my brilliant fundamental thematic analysis. My long-held target of parity would soon be realized. Gee, wasn’t I just grand.

Mr. Market shared with me what it means when you are only looking to confirm your own brilliance and not remaining open to data to suggest you may be wrong. The year 2012, my year of maximum confidence in my themes, turned out to be far and away my worst year’s performance in the currency market. at my point of maximum bearishness the euro began its journey on a stunning 20 cent rally. And it turned out to be my worst year ever trading currencies—by far. Hubris kills!

What did I learn? Or should I say, what did I re-learn?

Extreme in speculation = Extreme in price

Of course determining extremes in speculation is easier said than done, I grant you. And this isn’t about picking exact bottoms or tops. But is about being open to sentiment—quantitative and qualitative measures. Or as the great John Percival puts it: Being aware of flashing yellow lights.

If everyone you know is talking about the demise of the euro, especially those who have no business doing so, that is a flashing yellow light to suggest the trend may soon change. It is the way the market works. It is the way the market must work.

When I suggested just recently in a promotion for my service, maybe the euro was putting in a bottom given the one-way extreme levels of speculation as evidenced by open interest levels in the currency futures market, it drew some feedback from readers. These readers shared all the fundamental themes and very solid rationales as to why the euro is done for. They made perfect sense. But the funny thing is, I have heard them all before. It seemed a déjà vu moment all over again.

Today, we are seeing a sharp rally in the euro. It may suggest indeed some type of interim bottom is in place. Or it may be just a bounce. I do not know; though I have my betting suspicions. But given today’s price action in the face of overwhelming euro bearish sentiment, I am sharing two things: 1) a quote from Woody Dorsey explaining why abiding faith in fundamental themes over the technical analysis may be misplaced at times (the full piece from January 2013 can be found here), and 2) a plausible alternative scenario to the consensus theme of Eurozone economic demise.

1) Fundamental themes are ephemeral too…

Where can we find all the latest cultural concepts and investment themes? It turns out that if we want to get a glimpse of market culture, we have to go to the Concept Café. At this kind of café, we don’t order the soup du jour, we listened to the stories du jour. To really understand this we may need to play the part of the flaneur. A flaneur is a gentleman of leisure who frequents cafés and observes the spectacles of street life purely for pleasure. His observations and inferential focus is an apt metaphor for the process of determining the Investment Themes, or the Mind concept of Triune Theory. A flaneur may be in the crowd but is not of the crowd. The life of the street, the culture of the city, and the concerns of the citizens are seen as opera or a story to be both observed and savored. Everything the flaneur sees, every vignette is an open investigation. The flaneur detects everything while no one detects him. The Concept Café is where Investment Theme, or the ephemeral and fickle stories circulating in the market, can be seen and heard. Most people believe the fundamentals are real, solid, authentic, reliable, and durable reasons we can count on to explain the market; however, the flaneur, or a behavioral trader, knows differently. In fact, we have to take into account the reality that the marketplace is full of propaganda or what we call spin. Spin has been an aspect of human behavior from the beginning.

…Descartes had a huge influence on what philosophers call the mind and body question, also known as Dualism. Simply put, the still unresolved problem revolves around the relationship between the body (technical analysis) and the mind (fundamental analysis). Which influences which? What are their natures and how do they interact? We have two natures or live in two different worlds, the world of our minds and the world of our bodies. Descartes came down on the side that the mind is immortal and immutable compared to the body. This presumption is at the heart of the fallacy of “rationalism.” On Wall Street they still think that the Mind, or Investment Themes, rule everything. They’ve always dismiss the body or, the “Technicals,” just because Descartes effectively told them to.

Woody Dorsey, Behavioral Trading

Just maybe Germany was right after all. Just maybe those taking the hard medicine are in fact showing signs of recovery. Just maybe the euro will be around a lot longer than most are betting…

2) Saxo Bank economist Steen Jakobsen discusses why quantitative easing by the ECB could be a huge mistake because the periphery is already showing signs of recovery relative to Germany and he expects Germany to grow strongly next year:

ECB about to make biggest policy mistake in history (12/4/14)

Now a look at EUR/USD Daily…

Thank you.

Jack Crooks

President, Black Swan Capital

The U.S. dollar is having a tremendous run. A 10% move is significant for a currency like the dollar. So, the fact that it’s made its way that much higher is a big deal. Typically, you’ll see the dollar measured against the euro, but now the dollar-yen trade has really taken on a whole new weight of gravity in terms of the yen moving lower and the dollar moving higher.

The U.S. dollar is having a tremendous run. A 10% move is significant for a currency like the dollar. So, the fact that it’s made its way that much higher is a big deal. Typically, you’ll see the dollar measured against the euro, but now the dollar-yen trade has really taken on a whole new weight of gravity in terms of the yen moving lower and the dollar moving higher.

The Japanese basically are saying that they’ll pull out all the stops to get inflation rates up toward 2% and get the Japanese economy and export market moving. The debt of Japan is currently about 225% of GDP. So, it’s already pushing the envelope — and that’s where you can start to have problems in terms of trying to put out more debt to pay for all the stimulus. It will be interesting to see how that shapes up.

Over in the eurozone, the European Central Bank is faced with the same uncertainty. The ECB is seeing the latest data show consistent contraction of the key measures over there: the ISM, the PMI and other types of business-confidence numbers. That’s really where we’re starting to see a contraction of growth numbers and inflation numbers in Europe as well.

Now compare that to the U.S., where economic reports are generally showing progress and the greenback has a lot of potential for further appreciation. I expect that the appeal of U.S. dollar-based assets will keep U.S. equities as go-to avenues for growth and income, especially with so much downward pressure on interest rates. Along those lines, here are two high-yield funds that are uniquely positioned to benefit from this environment.

First up is the Legg Mason BW Global Income Opportunities Fund (BWG), a debt fund that takes advantage of strength in the dollar to invest about 50% in foreign assets and generate a current 9% yield. BWG came down a little bit when the emerging markets were hit in October, but it has leveled out right in the mid- to low $17 range. BWG looks fine here, and I see it as a really nice way to play the strong dollar against the weaker foreign currency trade that is currently dominating the forex markets right now.

Let me also call your attention to the DoubleLine Income Solutions Fund (DSL). DSL is Jeff Gundlach’s fund, and he’s considered to be one of the smartest people in the entire bond-market universe. DSL is paying 8.5% right now. Jeff Gundlach has taken advantage of using the strong dollar to invest in the foreign markets, those that have good sovereign-debt ratings as well as the potential for really good exchange currency swaps.

Warning: Dangerous Market Curve Dead Ahead! These 5 high-quality blue chips are head-and-shoulders above the rest in terms of weathering the coming drop and rebounding strongly. I call them my Rotation Rally “Return Giants.” Click here now to get their names so you can start profiting from them immediately.

Both of these funds pay monthly and are trading pretty much within a one-point range for the last few months; DSL is currently trading right around $21. The International Monetary Fund has been lowering the outlook for global growth.

As long as there’s no inflation out there, we have still a case for a decent fixed-income market…as long as you’re not way out on the yield curve, and I really don’t see that as a threat right now. Right now, the U.S. dollar just buys more out there on the market than it would if it were not up 10% against everything else in the world. So, it’s a great time to invest in foreign assets — and BWG and DSL certainly are doing it right.

About Bryan Perry

A leading expert in the world of high-income investing, Bryan Perry has been bringing his wealth-building insights to individual investors and institutions for nearly 30 years. In 2009, Bryan launched his flagship Cash Machine advisory service. At Cash Machine, Bryan investigates hundreds of income-producing vehicles each month so he can identify the small handful that can generate safe, steady and big income to his subscribers. You can find complete details on his latest batch of high-yield picks in a new Special Report: “10 Big Safe Income Doublers Over 10%.” Click here to find out how to get your copy absolutely free!

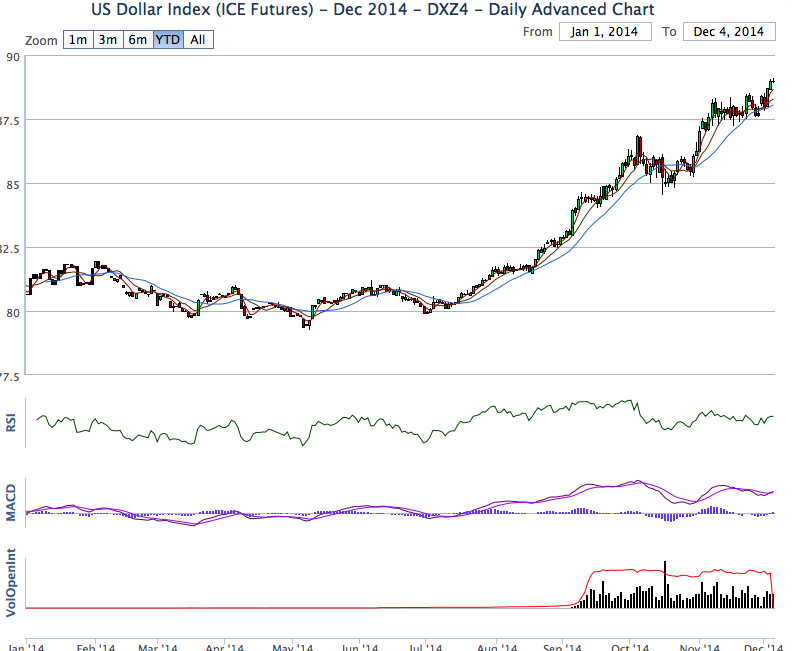

We have been resolutely Bullish the US Dollar this year…all of our trading in the currency futures and options market has be predicated on a Bullish Dollar view. We have repeatedly recommended to our readers to NOT take net short positions against the US Dollar. We have traded currencies for over 40 years and we have learned that currency trends often go WAY further than seems logical or reasonable.

The USD Index closed last week at 8 year highs…it began to accelerate higher in July and is up ~11% since then…

The major commodity indices fell to new 4 year lows last week…down 32 to 36% from their 2011 highs…as the US Dollar rose to 8 year highs…

Central Banks outside the USA are fighting deflation…falling commodity prices will force these banks to intensify their simulative actions…thereby adding to the market’s perception of a widening “split” between the FED (tightening) and other Central Banks (easing)…this perception is US Dollar bullish.

The Yen is at 7 year lows…down ~36% in the last 2 years…down 17% since July…

The Euro is at 2 year lows…down 13% since making a Weekly Key Reversal Down in May.

The weak CAD (now at 5 year lows) has been a “shock absorber” for the Canadian economy…if the CAD was still above par, unemployment would be rising …not falling. As a long term currency hedge in 2007 we began switching a significant chunk of our net worth into USD….at an average exchange rate above par. This strategy was not a “trade” but rather a currency diversification once we realized that we had hugely benefited from “being in the right place at the right time” while the CAD rallied from 62 cents to well above par on the back of the 2001 – 2011 credit driven commodity bull market. We expect to see the CAD lower against the USD in 2016….but…

We continue to expect CAD to strengthen against other principle currencies…

WTI Crude Oil fell ~38% since June…hitting 5 year lows…

Here’s what happened to the currencies of some oil producing countries since June:

US Dollar Index: UP ~11%

Canada: DOWN~ 6%

UK: DOWN ~9%

Mexico: DOWN ~11%

Norway: DOWN~18%

Russia: DOWN ~60%

The collapse of the Russian Ruble shows how a weakening currency can lead to a stampede of capital flight when markets lose confidence and panic…

The Gold Market: made new 4 year lows in November…but rallied $80 from overnight lows on December 1. If gold had closed last week above $1210 it would have created a Weekly Key reversal Up…that didn’t happen…but we are watching gold closely. The 3 year downtrend in gold remains intact (that strong US Dollar hurts!) but a December close above $1250 in this bullish USD environment would be very interesting and would likely led to more gains.

The Stock Market: We have been skeptical of the stock market for the past 2 years. During that time we have opportunistically traded it from the short side. We have made some money…but we would obviously have made much more if we had simply “gone with the trend” and been buyers…especially if we had embraced a “Buy the Dip” mentality. We may be slow learners but we have changed our minds…where we used to see stocks as “over-valued” because of Central Bank printing…and therefore likely to “collapse” once the Central Banks “changed their ways”…we now think that stocks may be “the only game in town” as pension funds and other institutional pools of capital “rebalance” their portfolios away from low yielding fixed income and into stocks. In a deflationary world Central Banks are likely to keep interest rates low for a long time…especially outside the USA. So we foresee a possible “double-whammy” of a global multi-trillion dollar rebalancing of institutional money into stocks…and a global flow of capital to America in search of safety and opportunity driving US stocks higher…perhaps much higher. (A possible reprise of the 1995 – 2000 period when the USD rose by 50% and the S+P tripled!)

Of all the problems with fiat currency, the most basic is that it empowers the dark side of human nature. We’re potentially good but infinitely corruptible, and giving an unlimited monetary printing press to a government or group of banks is guaranteed to produce a dystopia of ever-greater debt and more centralized control, until the only remaining choice is between deflationary collapse or runaway inflation. The people in charge at that point are in a box with no painless exit.

Of all the problems with fiat currency, the most basic is that it empowers the dark side of human nature. We’re potentially good but infinitely corruptible, and giving an unlimited monetary printing press to a government or group of banks is guaranteed to produce a dystopia of ever-greater debt and more centralized control, until the only remaining choice is between deflationary collapse or runaway inflation. The people in charge at that point are in a box with no painless exit.

Prudent Bear’s Doug Noland describes the shape of today’s box in his latest Credit Bubble Bulletin:

Right here we can identify a key systemic weak link: Market pricing and bullish perceptions have diverged profoundly both from underlying risk (i.e. Credit, liquidity, market pricing, policymaking, etc.) and diminishing Real Economy prospects. And now, with a full-fledged securities market mania inflating the Financial Sphere, it has become impossible for central banks to narrow the gap between the financial Bubbles and (disinflationary) real economies. More stimulus measures only feed the Bubble and prolong parabolic (“Terminal Phase”) increases in systemic risk. In short, central bankers these days are trapped in policies that primarily inflate risk. The old reflation game no longer works.

In other words, most real economies (jobs, production of physical goods, government budgets) around the world are back in (or have never left) recession, for which the traditional response is monetary and fiscal stimulus — that is, lower interest rates and bigger government deficits. Meanwhile, the financial markets are roaring, which normally calls for tighter money and reduced deficits to keep the bubbles from becoming destabilizing.

Both problems are emerging simultaneously and the traditional response to one will make the other much, much worse. Some more specifics from Noland:

Let’s begin with a brief update on the worsening travails at the Periphery. The Russian ruble sank another 6.5% this week, increasing y-t-d losses to 37.9%. Russian (ruble) 10-year yields jumped another 146 bps this week to 12.07%…

Increasingly, emerging market contagion is enveloping Latin America. The Mexican peso was hit for 1.6% Friday, boosting this EM darling’s loss for the week to a notable 3.0%. This week saw the Colombian peso hit for 4.3%, the Peruvian new sol 1.1%, the Brazilian real 0.9% and the Chilean peso 0.6%. Venezuela CDS (Credit default swaps) surged 425 bps to a record 2,717 bps. Brazilian stocks were slammed for 5% this week and Mexican equities fell 2.2%…

Declining 1.3%, the Goldman Sachs Commodities Index fell to the low since June 2010. Crude traded to a new five-year low. Sugar fell to a five-year low, with coffee, hogs and cattle prices all hit this week.

And a quick look at the bubbling Core: The Dow 18,000 party hats were ready, although they will have to wait until next week. The S&P500 traded Friday to another all-time record. Semiconductor (SOX) and Biotech (BTK) year-to-date gains increased to 31.4% and 48.1%, respectively. The week also saw $4.0 Trillion of year-to-date global corporate debt issuance, an all-time record. Italian (1.98%), Spanish (1.83%) and Portuguese (2.75%) yields traded to all-time record lows again this week.

What differentiates today’s reflation from those that “worked” in the past? The current reflation has overwhelmingly manifested within the Financial Sphere. And that’s the essence of why I believe the Bubble is now running on borrowed time. It’s a critical issue that goes completely unrecognized these days: In the end, Financial Sphere inflations are unsustainable…. The entire world believes central bankers will support stock, bond and asset prices. Everyone believes central bankers will ensure liquid markets. Most believe global policymakers will forestall financial and economic crisis for years to come. And it is these beliefs that account for record securities prices in the face of a disconcerting world.

We are, in short, down to the final myth that animates the blow-off phase of most bubbles: that of the omnipotent government/central bank which likes the status quo and has the power to maintain it. They don’t have that power, of course, or else financial bubbles would never burst and we’d still be living in the golden age of junk bonds, dot-coms and subprime mortgages.

What’s different about this iteration is that instead of being confined to a single asset class, the bubble is in financial assets generally, including fiat currencies, government debt, corporate bonds and equities, along with all their related derivatives. Where previous bubbles accounted for hundreds of billions or at most one or two trillion dollars, this one is denominated in hundreds of trillions spread from emerging market bonds to money center bank interest rate derivatives. The number of moving parts and the magnitude of the hidden risks guarantee that when it comes, the dissolution of today’s myth structure will be like nothing any of us have ever seen.

The U.S. dollar is extending its advance as the divergence theme moves into overdrive. The dollar has drawn close to JPY119.50. The euro has fallen to new lows near $1.2320, having been turned back from $1.25 on Monday. The Australian dollar has been pushed briefly below $0.8390.

The main exception is sterling, which is holding its own after a stronger than expected service PMI. Although it slipped below yesterday’s low, Monday’s low near $1.5585 remains intact, and sterling is trading around 3/4 a cent above there near midday in London.

The divergence theme has been underscored by the comments by Fischer and Dudley reaffirming the signal by Fed leadership that the mid-2015 rate hike is still “reasonable”. The disinflationary impulse from the drop in energy prices is temporary. Instead, they emphasized the growth implications.

[Read: End of U.S. Dollar Hegemony – Not]

There has been a backing up of U.S. interest rates too. The 2-year yield is near 55 bp, which is the upper end of the range seen in recent weeks, and represents a 10 bp increase since Monday’s lows. There is increased speculation that the “considerable period” phrase in the Fed’s statement is likely to be diluted or dropped as early as this month. Meanwhile, the 10-year yield is near 2.30%, which is a 15 bp increase since Monday’s lows.

In Europe, the service PMI was slightly disappointing at 51.1 from 51.3 of the flash and 52.3 in October. Germany was unchanged from the flash (52.1) but France’s downward revision wipes out the improvement that the flash suggested. France’s service PMI slipped to 47.9 from 48.8 of the flash and 48.3 in October.

The pleasant surprise came from Italy. The November service PMI rose to 51.8 from 50.8. The consensus was for 50.2. It was Spain that disappointed. The service PMI fell to 52.7 from 55.9. The market had expected a smaller decline to 55.2.

In addition, the euro area October retail sales in October rose 0.4%, slightly less than expected, and managed to retrace only a small part of the 1.2% decline in September (was initially -1.3%). This week’s data provides a poor backdrop for tomorrow’s ECB meeting. Everyone agrees that the ECB staff is going to cut its forecasts again and that Draghi will be dovish. This goes practically without saying. The key issue is whether the ECB expands the assets it is purchasing (to include supra-nationals, like EU, EIB, EFSF, ESM bonds – the “low hanging fruit), or does it announce its intentions to buy sovereign bonds, as some expected.

[Listen to: Michael Pettis on Why We Need a New Global Monetary System]

The market took the Australian dollar lower in response to the poor Q3 GDP figures. The economy expanded by 0.3% on the quarter, less than half the pace the consensus expected. The RBA statement earlier this week had spurred a reassessment of a rate cut the market was pricing in for next year. However, today’s weak growth figures have seen such pressure renew. However, ahead of tomorrow retail sales and trade balance reports, the interest rate adjustment is modest. The 2-year yield is off 5 bp today to 2.38%. It had reached 2.45% earlier in the session. The low before the RBA meeting was near 2.36%. This level should be taken out as a cut is further discounted.

China reported service PMIs. The official one ticked up to 53.9 from 53.8. The HSBC measure also ticked up, from 52.9 to 53.0. It does not impact expectations that the PBOC is likely to cut the reserve requirements in the next week or so. The dollar has quietly firmed against the yuan and reached almost CNY 6.1550 today, its highest since late September. Because the yuan shadows the dollar, despite the flexibility the PBOC claims it has introduced, the yuan has appreciated on a trade-weighted basis. It will continue to do so, even if it edges lower against the dollar.

The North American session will be busy. The Bank of Canada meets. It is expected to leave rates on hold. We look for the Bank of Canada’s statement to emphasize that it is looking through the pick up in price pressures as transitory. There are three U.S. reports to note: ADP, ISM services and the Beige Book. Note too that UK’s Osborne will make the Autumn Statement (budget). Separately, it has already been announced that the Funding for Lending Scheme, which aims at increasing credit to small and medium-sized businesses has been extended for another year.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair